i think you can check last quarter’s conference call, Garg already answered it I believe.

Decent sales figure. Area of concern: Trade receivables and other expenses keep increasing. Net cash flow reduced to less than a Cr.

Collections wud obviously hv been impacted by covid 19 and the logistical bottlenecks arising therefrom.

Is there a concall this time?

1 Like

It was taken against FD/MF for working capital requirements of big order from Brazil. They pay 3% over what they earn.

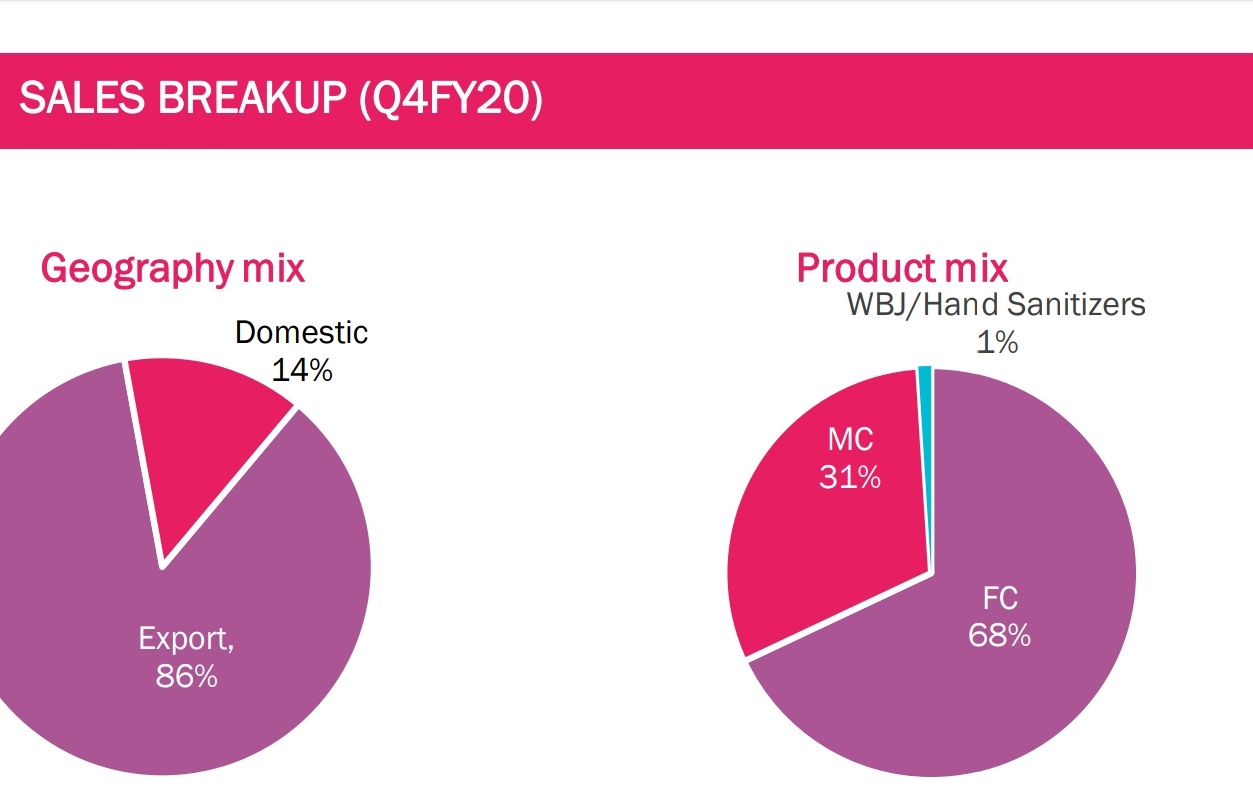

Trade receivables are higher due to payment terms of 90 days for Brazil order

Other expenses could be due to USFDA & marketing expenses of new geographies

No concall as per Company Secretary

3 Likes

These are an excellent set of results for the year… I had never expected the company to have 160 cr topline with 40 cr bottom… as we were struggling to even get 100 cr topline earlier.

There is a lot of demand for the product in the international market and they seem to be in a duopoly with having a cost advantage to veru.

This year should be very exciting as USFDA clearance should come through.

I would like to hear from the management on sales of hand sanitizer… did we do any meaningful sales these few months. If anyone is planning to write to cs , please ask about this as there is no concall qtr due to covid.

1 Like

That would be after March… so I meant how the sales are doing in q1… before that there wasn’t much of a coronavirus scare … I’m asking because I remember mr garg saying sanitizer has 40% margins… which is great

1 Like

Hi All,

I analysed the company and see a lot of positives about the company but there are some big negatives which i am putting below:

- The business’s prospects depends on the high margin female condoms and acceptance of these is something i am not able to understand. The easy of use of Male condoms is very simple whereas the female condoms usability is a tough one. So why will people start switching from male to female condoms.

I checked the ratings in Flipkart and it is 3.7 and the negative comments clearly suggests my perspective above.

-

Ageing Management. I did not see any young managment.

-

CFO<Net Profit 6/10 times in the last 10 years and so is the cumulative one for 10 years. This indicates the company is not able to convert Operating Cash Flow into Profits

I am seeing the above as good negatives to stay away from the company currently.

Can forum members share your thoughts?

Regards,

Ravi Krishna Yendru

4 Likes

One thing that is not clear from 1277 replies is which other competitor is listed in stock exchange. Any light on it shall be helpful

There are no listed competitors, as far as I know (In India). The only players in the B2G Global Condom market are:

- Cupid

- Veru-FC (A division of Veru, a Pharmaceutical company in the USA)

- PATH (https://www.path.org/) is an India non-profit

A small, Chinese player was competing a few years ago. But they lost their WHO qualification recently.

Out of these, PATH produces negligible volumes. The entire market is controlled by Cupid and Veru-FC with an almost equal market share.

6 Likes

Just did a SWOT analysis as part of my annual review of the Company (I own the stock).

Strengths

- One of three companies worldwide approved for selling female condoms

- The Female Health Company doesn’t seem to be making profits and recently a Chinese manufacturer had to shut shop

- On the other hand the company claims to have a unique design and more attractive cost of production

- Effectively winning repeat orders amongst different countries creating a relationship driven business

- Male and female condom capacity is easily interchangeable

- High Gross Profit margin business with 15-20% on male condoms and 45-50% on female condoms

Weaknesses

- Currently does not have a CEO and has been working this way for a few quarters and the promoter is now 77 years old

- High concentration with 40% of revenue coming from South Africa

- This is offset to an extent by the fact that the buyers don’t rely on donations

- Business is heavily dependent on tender based bulk orders from governments of developing countries like South Africa, Tanzania and Brazil

- Capacity utilization in the current FY has reached 86% and 92% for male and female condoms, respectively and further growth without Capex seems difficult

Opportunities

- Scope to expand in the Latin America and African region due to high HIV rates

- Female condoms are a highly growing industry (expected to grow somewhere between 16-20% CAGR) with limited competition (3 major players globally)

- Company is making a foray into in-demand lubricant products

- Plans could materialize for setting up a JV in South Africa

Threats

- A cut in government budgets in the coronavirus scenario could highly impact sales and receivables

- Company faces tough competition in the male condoms segment from low cost manufacturers in China and Thailand

- Stop on bulk government and UN orders could drastically affect revenues

- High quality standards required in the business which if compromised could damage the business

This is just my analysis which I’d be glad to receive feedback or even respectful criticism. Do reach out to me in the comment section if you want to see the full report along with my valuation model (Valued it around Rs.170). Don’t worry I’m not charging anything so don’t worry.  Just trying to learn.

Just trying to learn.

9 Likes

Veru owns them & are biggest competitor for Cupid

It is discussed widely. Currently promoter is old but managing operations efficiently. Once he stops active participation in routine operations, his spouse (veena) should be able to manage till they appoint a CEO. I know there has been discussion in multiple concalls on this topic but if someone seriously looks for a candidate, I don’t think it should take more than 6 months. While commenting this I know that tender business requires one-to-one personal unique relationship & mutual understanding.

This concentration should get diluted with US business in next 3-4 quarters

The product mix provides comfort to clock higher topline. Other than this management has spoken about subletting lower margin business once they achieve 100% capacity utilization. Anyway capacity expansion does not require big extended timelines.

Current order book is good to serve till Q1 of FY22. Do we see covid impacting the budget allocations of next FY as well? HIV is not a small threat in African continent and can’t be ignored for budget.

3 Likes

Thanks for the feedback. There are a few things you’ve mentioned that I wasn’t aware about.

I have my doubts over how well his wife or an external CEO walking right in and taking the reigns. I’d prefer seeing a new CEO coming in and the Mr. Garg moving to only being a Chairman and showing him/her the ropes. This is even more important when management seems like a one man show.

I don’t have a personal view or haven’t valued this geography. Prefer to see the numbers first because this isn’t a developing economy like all the others.

I see the management is striving towards becoming a female condom company but the FC share has varied anywhere between 45-70% and management has also guided to 50-50 mix for the next year.

Order book is strong for sure but my investment horizon is looking towards at least the next 5 years. I know the importance of preventing unwanted pregnancies and STDs for these countries but government budgets are budgets. However in the long term I think government healthcare spending is going to go up.

Durex condom sales are slumping as ‘intimate occasions’ disappear during the coronavirus pandemic

1 Like

The consumer business of durex and cupids b to g business are vastly different… it’s like comparing hul sales with tata steels… please don’t waste time over all this

2 Likes

B2B or B2G or B2C, the end users are same. The link gives a good idea about what is happening, I’m sure some of us might have thought “because people are at home, the condom sale will go up, because no other activities” but this news gives another picture.

Even if we think about B2G, where these condoms go? Who are end users? If to spread safe sex, govt is providing condoms to brothels or sex workers that business is halted completely. So the news is very much related to Cupid imo.

4 Likes

3 Likes

Found this short video on the company’s YouTube channel:

I know this isn’t much. But good to know at least they are following all safety procedures properly.

3 Likes

Wrote about almost everything I know and could gather about Cupid Limited. Posting it here so it could be a one-stop-shop for someone wanting to understand the company, at least for starters.

13 Likes