Cupid reports stoppage of production since 23rd march. Surprised that other companies are provided licence to produce sanitizer, mask etc to fight against corona and companies producing such products are forced to shut down their plants, obviously reasons may be different but all help must be provided to ensure that adequate production is happening in India.

4 Likes

Agreeing to what @hitesh2710 said, I am also very uncertain of future growth prospects of the company. What are the growth drivers for the company, if any?

- Targeting better product mix - This is highly dependent on FC orders in the future. However, from the reviews, I read online, women like this product. But I am not sure about the future majorly because of lack of awareness.

- US FDA - I see a lot of boarders excited about this. What is the reason? Is the company going to take the B2G or B2C or contract manufacturing route to US markets? CEO gave a 2-5 million USD opportunity size. How difficult would it be to capture this?

- Scaling up - Since the plants are operating at 99% capacity, further scaling up is a good opportunity. I feel more orders from African continent is the key. Good news here is that it takes only few months to ramp up capacity

- Diversification - The company is not a B2C brand and therefore diversifying into B2C products like hand sanitizers doesn’t seem like a great idea for me(Corona might help in increasing volumes in the short run though)

- Acquisition - I feel this is where the opportunity lies for future growth. But I am really unhappy with the management’s response that they are merely open to these opportunities instead of hunting for opportunities aggressively. There might be some women healthcare companies with a decent brand name available at cheap valuations because of drying up of capital amidst this crisis.

There is good visibility of earnings in the short run. But the company currently lacks a viable long term growth strategy.

Disclosure - Just started tracking the stock

4 Likes

Due to redirection of most discretionary financial resources towards covid-19 by major relevant organizations, Cupid future orders will likely take a big hit.

1 Like

I don’t disagree with this. Most likely donor funding will take a hit, as most funding will be diverted towards fighting COVID19. I’m still waiting for Mr. Garg’s update on the business.

On a related note, I’m interested in understanding how Veru is going to survive this crisis. At least Cupid has the “capacity to suffer” (Good and Strong Balance Sheet), whereas Veru is in a dire situation. So, looking forward to Veru’s next quarter’s notes as well.

1 Like

Its true that donor funding will get a hit & it will impact Cupid, Veru and other companies in this business. The impact will depend on severity of corona in countries where cupid gets most of its orders. US situation must impact Veru more than Cupid and if Veru share prices are any indication, seems they are getting some support after a minor hit.

Cupid remained silent on one of its biggest expected orders in Q4, as they had declared very small order in recent notification to exchanges, I take it as a miss of order and will wait for management to come up with reasons (deferred or lost) in next media interaction / Q4 con call

1 Like

Production to start in tranches:

I emailed the company, for some strange reason Mr Garg continues to expect to receive South Africa and Brazil tender. I appreciate his optimism.

1 Like

Any specific reason behind quoting strange reason on management’s optimism. These are tenders and each vendor remains optimistic till tender is opened or the process is aborted (due to any reason… in current scenario many people are guessing that funding will be stopped but we haven’t heard anything from respective institutions)

i just think realistically female condoms are probably not an immediate concern for health departments of governments. They are probably more concerned with getting PPEs, covid testing kit, temporary hospital beds etc. So was quite surprised that he was still expecting for such tenders to progress. In my view these would be postponed indefinitely - at least until the virus comes under control.

2 Likes

While corona is dangerous and has affected whole world and has no vaccine / medicine available for patients, cupid products help world protect from another danger namely AIDS. While healthcare budgets of many countries / institutions would be aligned to fight covid but I don’t think that it makes allocation towards other medical requirements nil. At the most, they may prioritize and divert part of funds to emergency requirement of fight against covid. Moreover if institutions have already allocated funds for ongoing tenders, management will wait for official communication regarding abortion of initiated process.

4 Likes

Production again shut-down due to COVID-19

1 Like

INR has depreciated and hence EOU are beneficiaries. Latex prices have come down and hence CUPID is beneficiary. huge tailwinds. Product has perennial demand. Market cap is close to 40% from the 52W high while it is 10% down for Veru. Company has 35 Rs / share cash, no debt. Q2 results of Veru and concall shows that demand remains robust, no overcapacity hang in world. Maybe company buyback 10% from open market , promoters would have more than 50% stake post buyback if they do not participate.

4 Likes

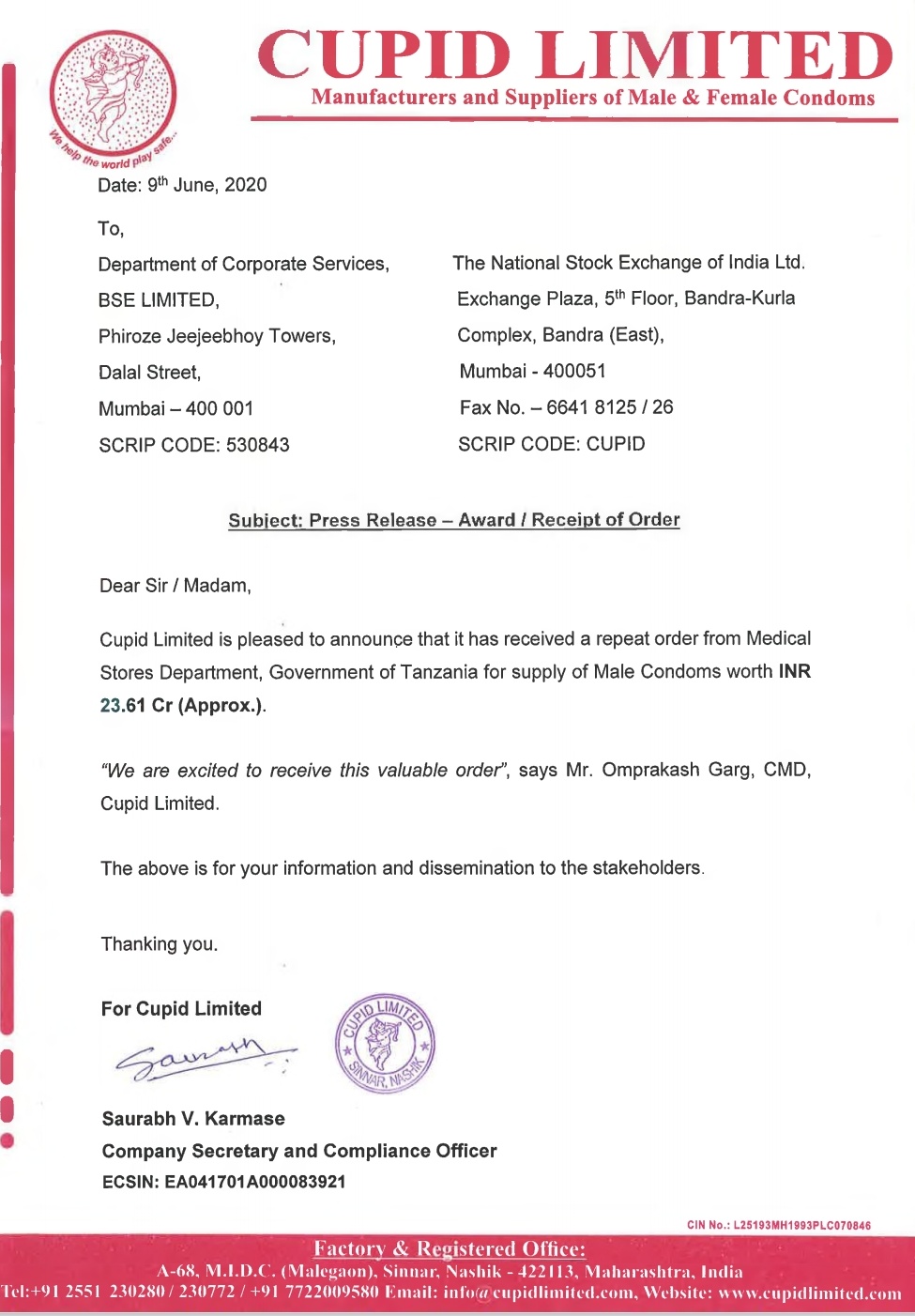

Cupid received a repeat order from Medical Stores Department, Government of Tanzania for supply of Male Condoms worth INR 15.5 Cr (Approx.).

Getting such big repeat order in negative economic environment is appreciable.

5 Likes

Official notification of COVID impact on Cupid

- Revenues and profitability of the company will be adversely impacting in Q1FY21

- we can hope that the business situation should normalise from Q2FY21

- Availability of labour is hampered due to COVID - 19 pandemic

- Manufacturing facilities remained shut from March 23, 2020 due to lockdown and partially reopened w.e.f. April 25, 2020,

- Operations impacted for the period of around 1 month

3 Likes

Receipt of Order

http://www.bseindia.com/xml-data/corpfiling/AttachLive/b699f9a2-ab44-4d9d-804f-fc736211bee3.pdf

3 Likes

Good to see big orders pouring in. One concern may be on margins as recent orders in Q1 worth 39+ Cr are exclusive MCs. let us wait for management commentary but prospects look good as of now

I have been tracking Cupid for a while and understand that the management is very transparent but I am very uncertain about the company for a couple of reasons.

- They do not seem to have any apparent or hidden moat (No brand name, network effect).

- The B2G condom space is highly uncertain. There is absolutely no certainty that this company will scale up or even stay at the same level.

However, I am positive towards the overall space. They are in an absolutely wonderful position. They are a condom manufacturer in a highly overpopulated country. And I know that they are not in the B2C space (in a meaningful way), they do not even supply to any major Indian condom brands (maybe because of lower margins or because the established brands have their own manufacturing units).

If Cupid was somehow able to exploit the massive opportunity available in the consumer space in India (whether through manufacturing or retailing), this would make me optimistic. However, it seems as though they are not able to do this (for whatsover reason). This does not seem like a long-term investment idea to me. However I welcome any opposing views.

This, plus they are still searching for CEO, so there’s no clarity on succession yet and if I have read it correct, they are also open for sell(con call 2018).

Disc:- Invested.

decent set of numbers released although covid only struck in april, may. so q1 numbers could be worse. order book is healthy but could be all male condoms.

1 Like

Why have they taken a large short term debt and parked the same in FD?