Is anyone know why they stopped paying Dividends even after having repeated profits from last couple of year?

Seems this bank is technological very far behind from the competitors by going through many customers review feedback.

Some can be found below:

Happy Investing,

Karthik

Disclosure: Not having any exposure to this counter. Tacking this Bank with DCB Bank due to good valuations

Private sector lender CSB Bank on Friday reported a 10 per cent rise in net profit at Rs 133 crore in the second quarter ended September 2023 as bad loans declined. The Kerala-based bank had posted a net profit of Rs 121 crore in the year-ago period.

Total income rose to Rs 836 crore from Rs 600 crore in the same period a year ago, CSB Bank said in a regulatory filing. During the quarter, the bank earned interest income of Rs 687 crore as compared to Rs 555 crore in the same period a year ago.

On the asset quality side, the bank witnessed improvement with gross non-performing assets (NPAs) fell to 1.27 per cent of gross advances by the end of September 2023 from 1.65 per cent a year ago. Net NPAs too declined to 0.33 per cent from 0.57 per cent in the same quarter a year ago.

Source:CSB Bank Share Price, CSB Bank Stock Price, CSB Bank Ltd. Stock Price, Share Price, Live BSE/NSE, CSB Bank Ltd. Bids Offers. Buy/Sell CSB Bank Ltd. news & tips, & F&O Quotes, NSE/BSE Forecast News and Live Quotes

Earlier there was a regulatory restriction. However, this should not be an issue now. Had asked the management, waiting for their response

Fairfax is ready for an “all-cash” deal to acquire IDBI Bank.

CSB bank looks interesting, and seems to be one of the best-run banks in terms of KPIs: it has great NIM, ROE, CRAR and NPA ratios.

Sharing Rajeev Agrawal’s thesis for investing in CSB bank from June 2023: https://youtu.be/WkAf1w3JRGA?si=ms6sPzYDr0_0p2QU&t=554

Some questions that I’m still not very clear about:

- What is CSB Bank’s moat exactly?

-

Is it just their history, bank branch network and customer relationships? What is preventing the other banks from taking market share from them? If it is just the branch network? Would their moat potentially decline in the future, when more people start using mobile and digital banking? If that happens, the branch network becomes more of a liability than an asset, as you need to rent out the branches and pay staff even though branch footfalls decline.

-

On a national level, how can CSB bank compete with the likes of HDFC, ICICI, Kotak (traditional) and Jio finance / PhonePe (digital / neo-banks)? The traditional banks have much bigger scale and investment power, while the new digital banks are much more agile in terms of offering mobile and digital banking solutions. CSB seems to be somewhere in the middle of these two

- Gold loans: their loan book is heavily skewed towards gold loans (~48% of total loan book). What would happen if gold prices decline? Looking at historical gold prices, there have been periods with large declines: gold price dropped ~40% from 2011 to 2015. Would CSB be able to absorb this sort of decline? They hold 11,818 Cr. of gold on their books as collateral. If gold price declines 40%, that is a decline of around 4727 Cr. (close to their current market cap of 5718 Cr.). Of course, it wouldn’t be a direct loss for the bank, as the gold is not “owned” by them, but rather owned by the customers who’ve taken a loan against the gold. However, in a recession-like scenario, where loan defaults increase while gold prices drop, would it cause an existential crisis for CSB bank?

Disc: researching; not invested

Thanks,

Sharad

OpenSourceInvestor @ Substack

1 Like

- I don’t think there is any moat. Banking industry is quite vanilla in nature itself. The point in favor of CSB bank is small market cap and small geographical presence and thus a headroom for growth. Under the leadership of Pranoy Monday(2022-present, he has also roped in new senior management), bank has aspirations of going pan India which should inevitably bring growth at such low market cap.

Kerala - 30%

Tamil Nadu - 29%

Maharashtra - 23%

Karnataka - 5%

Others - 14%

Recent partnership with Jupiter (5M playstore downloads) shows intent in the areas of modernization

On the other hand, CSB bank’s own apps look lackluster.

2 Likes

Thanks for the reply!

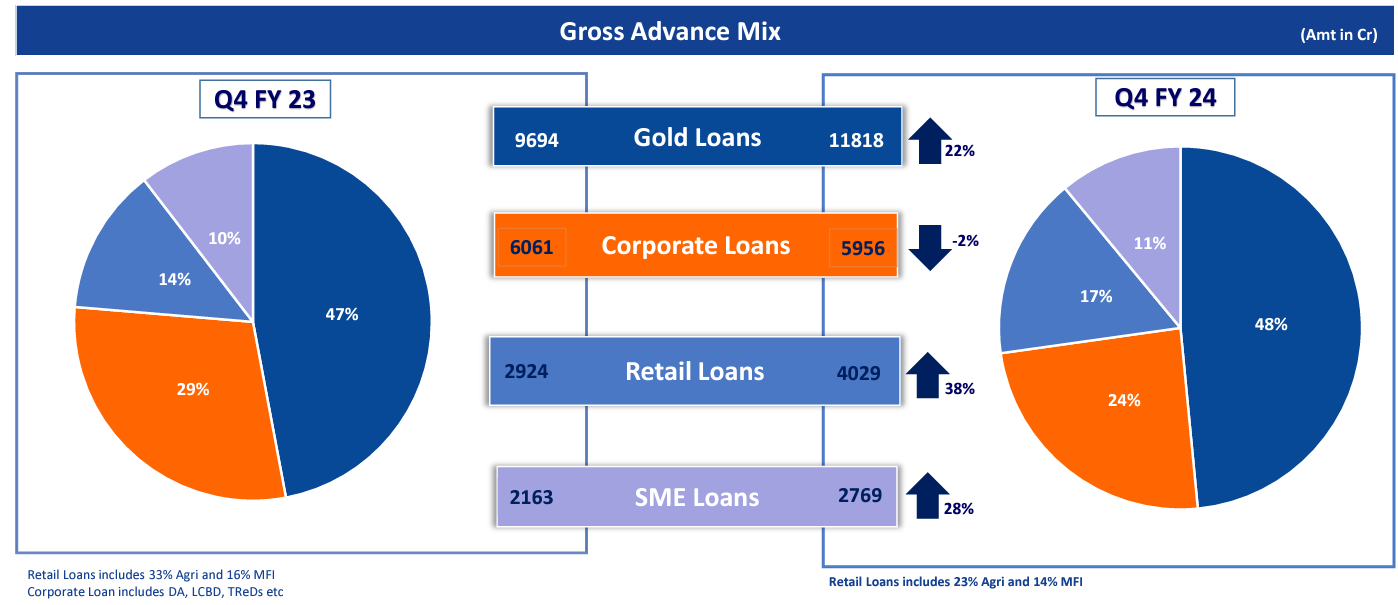

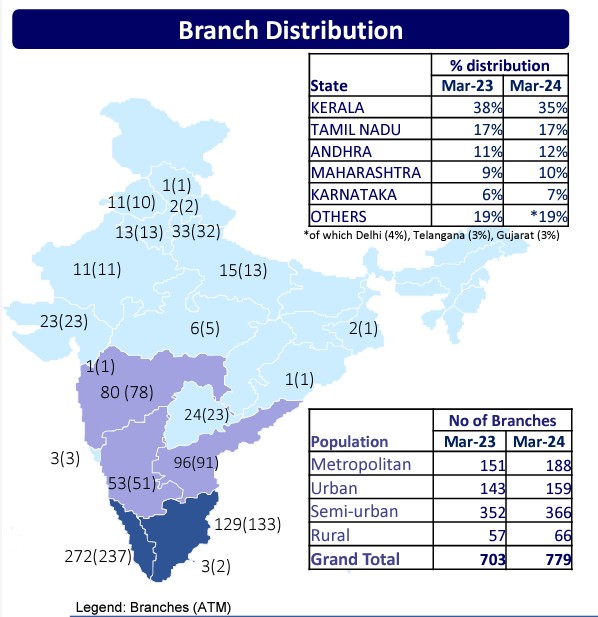

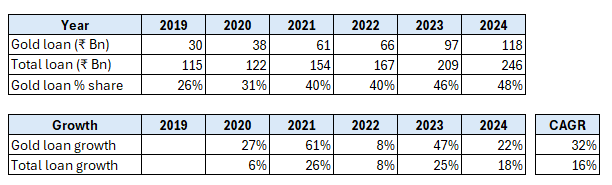

I did some more digging into CSB bank. I think I have identified one clear moat which has also been their growth engine for the last 6 years: gold loans. Since 2019, CSB’s gold loan book has grown 32% CAGR - going from 26% of their loan book to 48% at the end of Q4 2024. They have been able to do this, as they charge only around 9.5%~12% interest for these loans vs. Muthoot / Manappuram (the largest gold loan players) who charge 20%~25% interest. I think they charge less interest because they lend to more safe customers than Muthoot. This can be seen via their NPA ratios: CSB has 0.5% NNPA vs. Muthoot at 3% (meaning 6x more defaults at Muthoot). CSB’s gold loan book at ₹118Bn is 16% of Muthoot, who is at ₹729Bn. CSB’s moat here is low interest rates combined with being a trusted bank with a good branch network in Kerala and TN (seen below) - so people are not wary of trusting CSB to hold their gold safe.

Pralay Mondal (CSB’s MD & CEO) is cautious about gold loan growth. My guess is that the pool of safe customers for gold loans is limited. So, I don’t expect them to ever reach the scale of Muthoot / Manappuram. Mr Mondal also mentions that he expects “wholesale” and SME business to grow faster next year (which can be seen already from Q4 2023 to Q4 2024). Gold loans have a higher NIM and lower net NPA than Wholesale & SME Loans, so these will potentially both be impacted if gold loan share of total loan book reduces. Link to the interview.

However, if they manage to maintain their NIM at 4%~5%, I don’t see a reason for concern. For comparison: HDFC, ICICI and Kotak have NIMs of 3.6%, 4.4% and 5.3% respectively, while Muthoot and Mannapuram have NIMs of 11.6% and 15%. I double whether the latter is sustainable long-term, especially when loan customers get more internet savvy and are able to compare loan interest rates across banks/NBFCs.

In summary, CSB seems to be a promising bank , which will grow at 10%~15%+ in the next few years, as India is still very credit-starved and more people will move up the wealth pyramid from low-income to the aspirational / middle-class.

Gold loans vs. overall loan book:

Retail and SME is growing faster than gold loans:

Branches:

Disc: Have decided to start a small position and will monitor this stock in the coming quarters.

Thanks,

Sharad

OpenSourceInvestor @ Substack

3 Likes