Hi Friends,

This is my first attempt to share my analysis with you guys. I use to read this blog a lot and also follow a couple of great minds present over here. I would like to share my one of the favorite stock which I own in my PF (allocation of 10%). I will try to rationalize my analysis over here. Share your thoughts on this. Lets dive in but first pls note: I am not a registered advisor.

CSB Bank

History:

- It’s a century-old bank earlier known as Catholic Syrian Bank. Mainly serving Southern India.

- Prem Watsa, Canadian Warren Buffett (he is the same person who bought Fairchem, IIFL, etc), had purchased around 50% capital in 2019 at an average cost of Rs.140 per share.

- IPO came at a price of Rs.195/share. Oversubscribed and went to Rs.300 on the listing.

- The new management started cleaning the Books which led to high write-offs and provisions.

- Previously the employees were on the IBA pay scale, now started recruiting on a contractual basis which led to the hiring of 3 younger staff at the cost of 1 IBA staff.

- Hired Pralay Mondal from Axis Bank.

- Added a board member from PWC

- Branch expansion began across geographies. Currently, there are around 450 branches and they are planning to take it to 1000 in 5 years.

- Huge hiring from Axis Bank and Bajaj Finance was done to introduce new product lines e:g Bike loan, etc. as the bank was mainly in Gold/SME Loan.

- Given VRS in this quarter to around 200 staff which will lead to an impact of Rs.80 crore in this quarter.

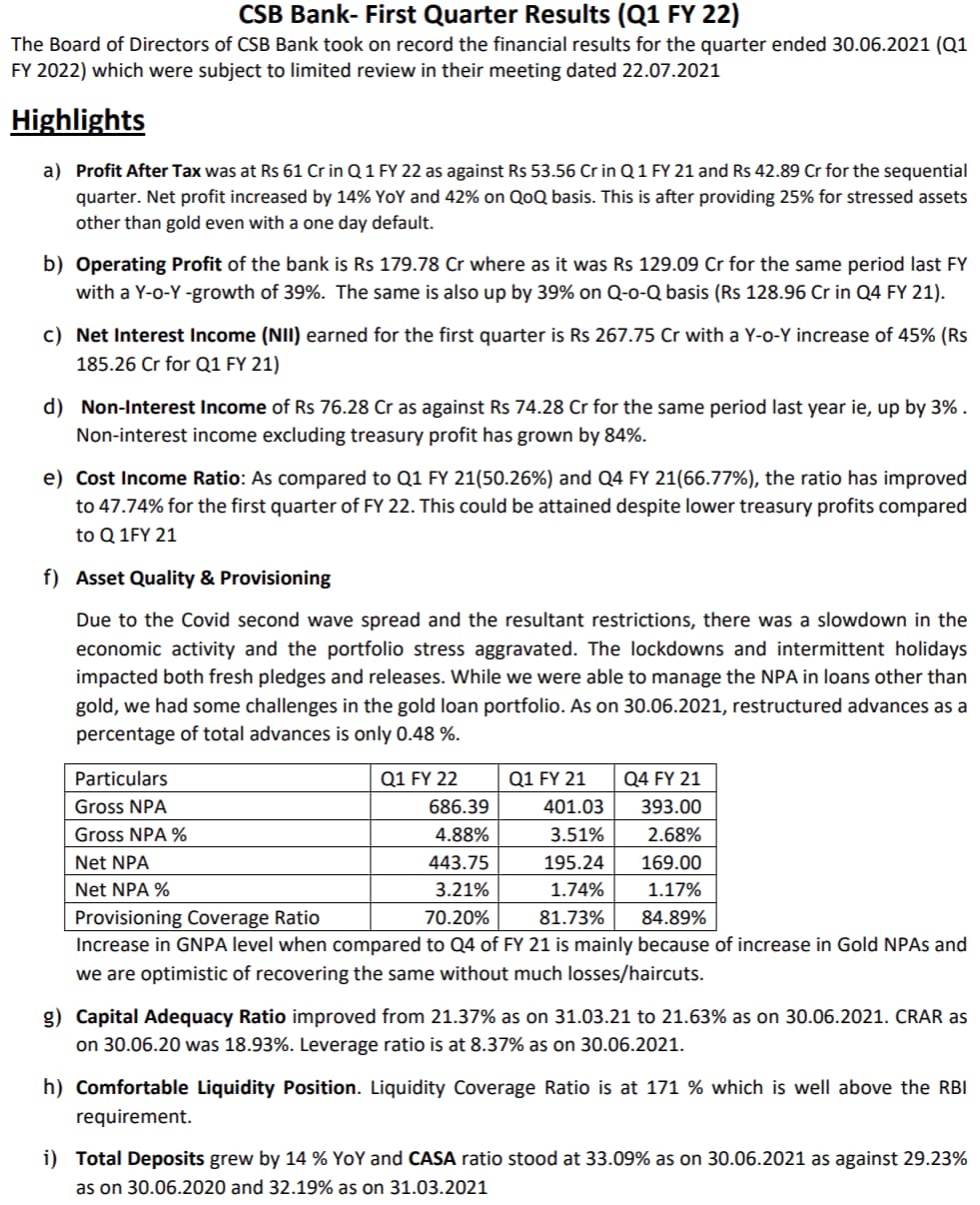

This was an update to date. Now let’s look at financials. Unlike other companies, financial parameters for evaluating banks and NBFC/ FI are different. Let’s look at key parameters.

Yield on Advances – Up from 10.72% to 10.98%

Cost of Deposits - Down from 5.91% to 4.91%

NIM – Up from 3.92% to 5.17% (However this might not sustain, it will be b/w 4-5%)

Yield on investments – Up from 6.33% to 7.00%

RoA (annualized) of 1.07%.as on 31/12/20

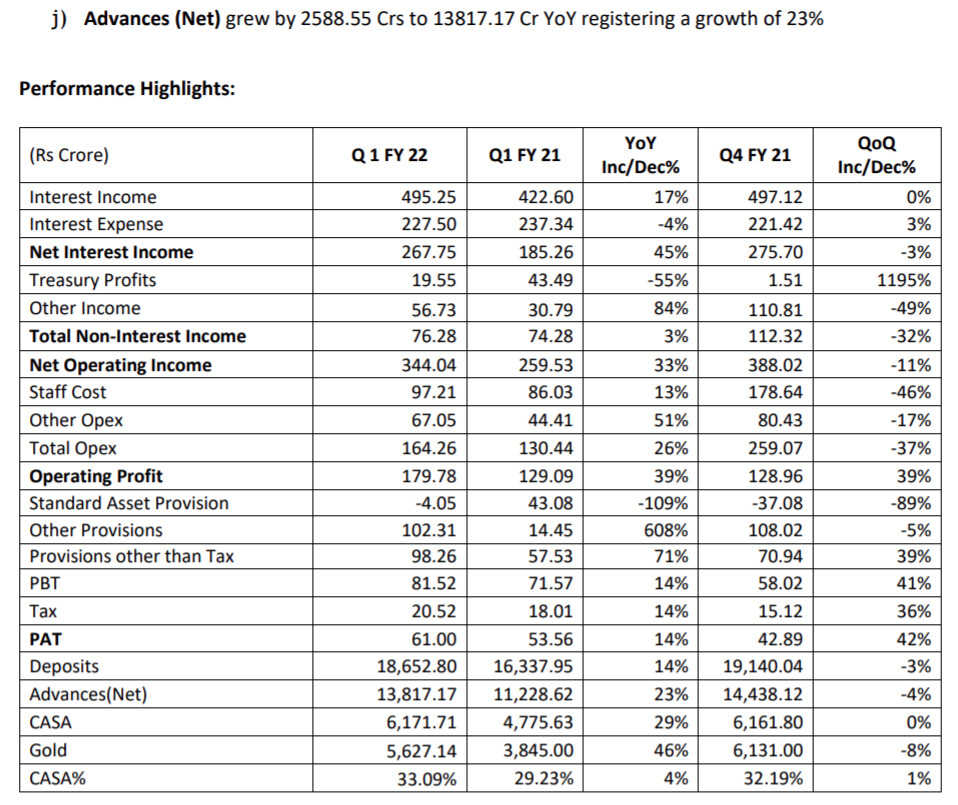

Total Deposits grew by 16% YoY

CASA ratio stood at 30.4% as on 31/12/20

Cost Income Ratio from 69.53% to 49.25%

Gross NPA decreased from Rs 387 Cr as on 30.09.2020 to Rs 235 Cr as on 31.12.2020.

Gross NPA as a percentage of advances is at 1.77% as on 31.12.2020 whereas it was 3.04% & 3.54% respectively on 30.09.2020 & 31.03.2020

Net NPA decreased from 164 Cr as on 30.09.2020 to Rs 89.5 Cr as on 31.12.2020

Net NPA as percentage of advances decreased from 1.30% as on 30.09.2020 & 1.91% as on 31.03.2020 to 0.68% as on 31.12.2020

Capital Adequacy Ratio improves from 19.69% as on 30.09.2020 to 21.02% as on 31.12.2020.

Leverage ratio is at 7.7% as on 31.12.2020.

Liquidity Coverage Ratio at 200%

Tier I ratio of 19.77%

This shows that the bank has a very strong balance sheet,

Management is also exploring acquiring a bank.

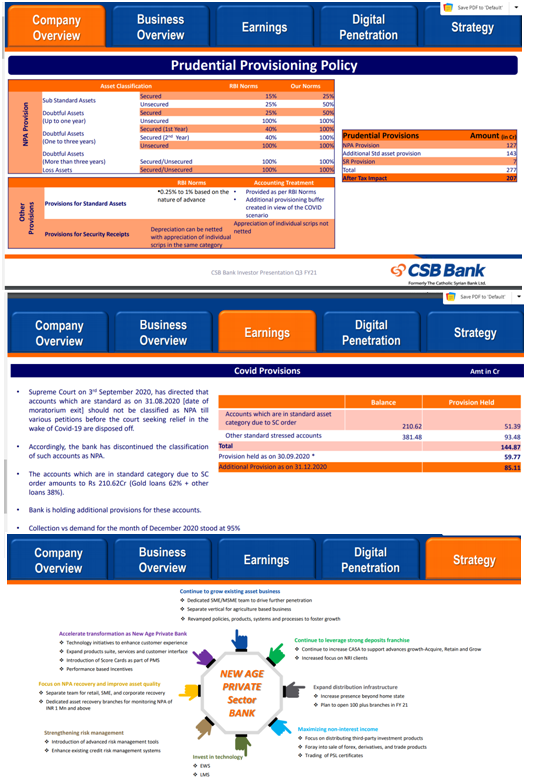

Below are the few snapshots of Presentation which shows that they have made provision in excess of RBI’s requirement which show conservative approach and a snapshot for future strategy.

Now the main part

The negatives and the positives

First the Negative aspect.

-

There is a risk of an increase in NPA once the moratorium lifts off. However, the bank has prudently provided provisions on that loans too (Rs.210.62 cr of loans are standard due to SC order as on 31.12.20 yet bank made provision of Rs.51 cr on these loans) Out of these loans, 62% loans are Gold loans hence the chances of getting NPA/write off is less.

-

bank’s NPAT in the last quarter was Rs.53 crore and in this quarter they are giving VRS to the tune of Rs.80 cr hence we might see loss/bare profit in this quarter.

-

Company is into full fledge expansion route hence there will be incremental expenses like staff cost, office setup cost, etc in the near future. Normally the cost of the branch begins on the date of setup whereas it takes little time to turn it into profit. So the benefits of expansions will be reflected after say 6-12 months.

-

This quarter might see less income from investment as yields have risen sharply thereby M2M profit will reduce.

Now the positive aspects

-

It is a very small bank with Mcap of just Rs.4500 crore and is doing all the right things to grow. Branch expansion lead by new management will surely take it to another level.

-

It had leadership in Gold Loans whereas now a new team with domain expertise will launch new products. Thus with the increase in branches and new products launching, we may expect a good jump in top line and bottom line in near future.

-

It has an extremely good balance sheet and adequately capitalized thereby can withstand any unforeseen circumstances and also there are possibilities of inorganic expansion.

-

Thus fundamentally it is very well placed but right now, u can say, it is in the gestation period.

Thank you for reading. Please share your views.