I first noticed Crisil while screening for stocks with a high ROCE factor.

I lately dug deeper into the Crisil business model and found out that apart from ratings, they sell reports on companies.

They also went through the 2008 crash quite well without losing more than 50% of scrip value.

Please forgive my lack of details as fundamental analysis is still new to me. I gather that as investment interest in India grows (both domestically and internationally) Crisil should grow as an investors go to company for investment information.

I’ve got a very tiny amount for a portfolio while I refine my current investment style. There are sectors/companies with stronger sector growth potential but I think that Crisil should be on par or outperform the best banks or next best financial sector scrips. Had I more capital for investing (maximizing allocation on my best scrips before allocating into the next best scrips), Crisil would be in my portfolio.

While a premium may be paid, I think the scrip may not have much attached risk. Please do note that fundamental analysis is new to me so my analysis may be off.

Crisil is a steady compounder, that will increase your wealth at 12-15 % for next many years, a fantastic stock to own. Stocks like Crisil only rarely will be cheap

In Rating business, Bank Loan Ratings and SME Ratings continue to do well and volumes were strong in 2014. However, there were lot of challenges in terms of increase in competition and retaining clients. Further, the bond market and debt market including the corporate securitization business was very low in 2014. All these continued in Q1 2015 as well, and the margins were under pressure in Rating business.

Going forward, while the management believes that the bond market and particularly the corporate side should improve in 2015 and also with large papers hitting the Primary market both equity and debt, Rating business volume should improve. However, margins will continue to be a challenge given the increase in competition. Particularly, the surveillance fees are getting hit badly.Scope of BLR and SME Ratings continue to remain healthy, with more than 25000 companies yet to be rated.

On geographical basis, about 35% of total revenue comes from India business, about 34% from USA, 25% from UK and rest from various other countries.There were some forex losses in Q1 CY 2015 due to adverse forex movements of Pound currency.Management expects the economy at ground level should improve as we go ahead in 2015. While based on the discussions with corporate world, the balance sheet is getting healthier and management believes there will be more upgrades than downgrades going forward.

Management also believes that while rate cut will help in reviving the investment decisions, the government policies will play an even major role in kick starting the economy.In Global Research and Analytical (GRA) business, both Irevna and Pupil continue to do well. The outsourcing business on risk related analysis for various international banks has increased. Management continues to remain optimistic about this segment and growing business segments within the Research and Analytical business. Company was able to add marquee clients in financial research, analytics and model validation.Going forward, management is confident of a better CY 2015 than CY 2014. Margins in Q1 CY 2015 will stabilise, if not improve.

@Vivek, thank you for letting me know about your positive take on the stock.

@Srinivas, the stock is indeed above fair value but I thought I’d share the stock and put it on the radar in case it ever is available at a discount.

I recently found historical financial data that indicates that this is a strong company that only had poor performance in 2008-2009 according to March 2009 results. Not really a VP stock but it is a company worth watching.

A detailed article on how a new startup is trying to enter the rating industry in the US. All the tactics, strategies that can create an opening.

2008 was the perfect storm to disrupt the status quo in the ratings industry but this is what happened, “That’s where I scratch my head,” says Powell. “You can’t dispute that the ratings agencies were complicit in the financial crisis, yet investors are still requiring them to rate deals.”

And this captures the entry the barriers very well, “Even though the scandals made an opening for new competitors, breaking into the business has still been a long slog.”

The article also provides the failings of an investor paid model and regulator assigned rating agency. Investor have their own biases which they would want to be reflected in the ratings, same as companies do now. Also, there is the case that ratings should be publicly available and no investor wants others to free ride on their investment.

In a regulator assigned or rotating agency model, the article says that any incentive for thorough research is eliminated as the rating business is assured. I somewhat agree with them, the problem this model creates is of differentiation. A rotating model would ensure perfect division in market share, this would mean that the only way to increase earning is with reducing costs, and all agencies will reduce research costs to maintain the same amount of quality level.

What is to be noticed is that even after being given the perfect point of entry after the GFC, disruption in this industry is a very slow process. If at all, it is the regulatory disruption that could swiftly change the landscape of this industry.

Despite of league of Pioneers in the management I wonder why the stock is sailing at the 5 year lowest level. However, the current scenario of pessimism about the rating agency comes in to picture from couple of last years. The company watch out for industry ecosystem for disruptions and opportunities yet they are not able to watch their own stocks and adding value to the common investors. This leads to many questions. they maintain the rating of more than 30000 companies across the globe yet they not able to introspect within.

In my opinion the at the end of the day, rating agencies’ evaluations need to be taken with a grain of salt yet they had done a remarkable work to helped investors identify levels of risk . But the RATING of the RATING AGENCIES is questionable and lots of grey side is these companies . The history of some credit agencies are found here

Why I avoid the CRA because

There is a gap existed between the credit ratings issued to different companies and their financial ratios, raising doubts regarding the correctness of these ratings.

What I feel is that problems in ratings had e contributed to the rising non- performing assets (NPA) crisis of India

I am sharing an report for the benefits of investors I personally recommend to go to the most of links in the report

In pursuance of the NCLT Order dated 06.12.2019, a meeting of the equity shareholders of CRISIL Limited will be held 12-02-2020 to segregate the Ratings business undertaking to its wholly owned subsidiary company – CRISIL Ratings Limited as a going concern by way of a slump sale for Rs. 22.43 Cr.

CRISIL will continue to provide other services viz. grading and assessments including those of small and medium enterprises, support for financial data and analysis services to S&P Global Ratings, global research and analytics and India research.

The Notice convening the meeting along with Explanatory Statement, Attendance Slip, Proxy Form and Postal Ballot Form can be downloaded from the following links and are also available Here

Post above arrangement, as consideration will be discharged in cash, there will be no change in the capital structure of the Crisil or that of CRISIL Ratings Limited

Posted an in-depth article on CRISIL. The article covers all of CRISIL’s segments:

(i) Ratings

(ii) Research & Analytics

(iii) Advisory

The post is quite lengthy as i wanted to cover all of CRISIL’s segments. Many interesting developments uncovered during the research process like: IBC code, LIBOR transition, MiFID regulations etc. Do check it out!

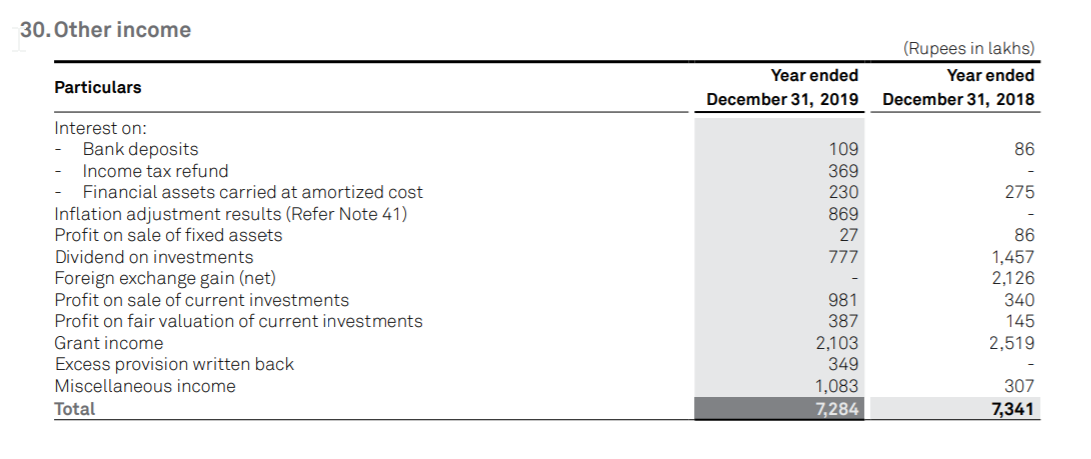

Hi Anirudh, i Read your research and it really nice writeup. And i also looked into thier balance sheet and found this Grant income from Govt .

Can you pls explain what kind of export they are doing to get this grant income ?

Hi Anirudh, A very good write up on Crisil. I have one question - What led to the significant margin improvement in the ratings business in the last one year ?

Is Crisil going to be a safe bet in the future with its ratings business. Or is there a probability of expansion of the research division (by getting research work from developed countries)?

Im sorry but im not aware of the grant income, couldnt find any proper disclosure for that amount. Actually CRISIL does not rate foreign subsidiaries of Indian companies and relies on rating provided by S&P if im not mistaken. It might be something related to that.

Hi Nemish,

Thank you. I believe that when the IL&FS fiasco happened, the reputation for CARE and ICRA got dented and many issues flocked to CRISIL. This gave them a good amount of pricing power to CRISIL as the rating fees does not form a material expense of the issue so issuers dont actually mind paying extra to get rated from a reputable agency like CRISIL. Moreover, we also saw increase in amount of issues to be rated from 2017 to 2019 which helped improve margins on account of operating leverage (most of CRISIL expenses are relatively fixed in nature)

CRISIL seems to be doing well on almost all parameters. The average 3-5 year ROE has been steady near the 32% mark and average 3-5 year ROCE has been steady near the 45% mark. The total annual net profits generated by the three listed credit rating agencies is approx. INR 527 crores, of which CRISIL alone generated INR 355 crores. Meaning CRISIL generated nearly 2/3 of the net profit of the industry. (Source: Value Research Website).

And yet, the stock of this company, which has a strong MNC pedigree has gone nowhere for the last 5 years.

For a company already having dominant market share, grabbing incremental market share from its competitors is unlikely to move the stock price needle by much. Since it has nearly zero debt, even debt reduction led improvement in return ratios is unlikely.

The biggest sore point seems to be the flat top line growth, indicating some kind of a saturation and lack of growth opportunities. Till we see a clear and sustained path to revenue increase, I don’t see how the stock prices can go up by much.