Hi Guys ,

At current market price 195, mufti lis trading at a multiple of 16

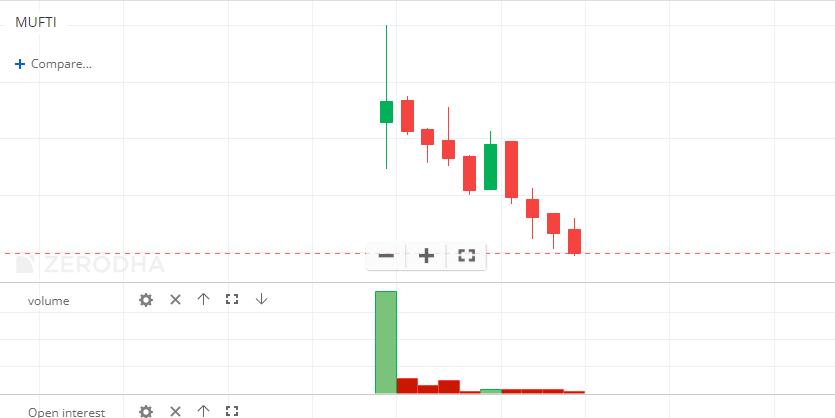

Credo brands mufti came to ipo on 28th December , with issue price of 280. It was oversubscribed with lot of interest from institutional investors. With market conditions it is beaten down to 200 levels, which makes to think about market behaviour

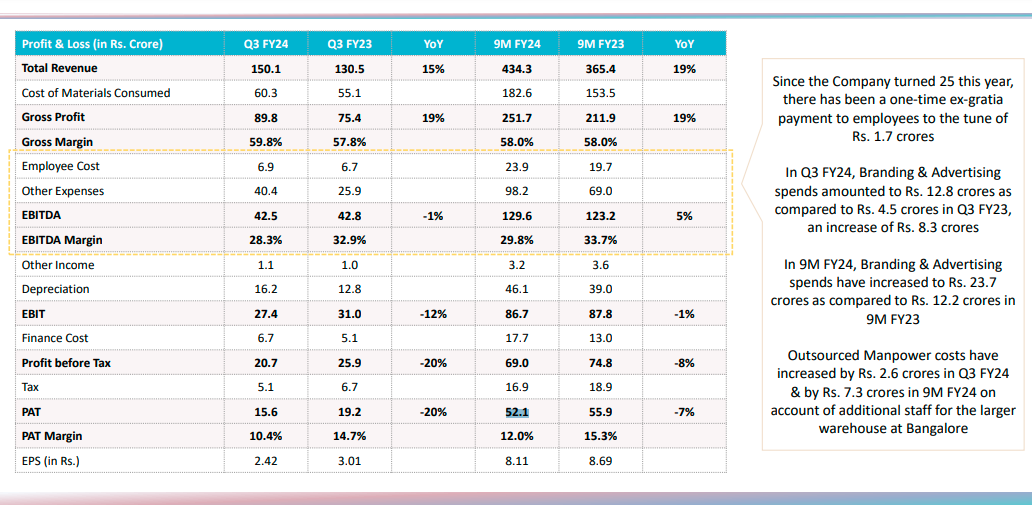

Even in 9Mfy24, their PAT margins are at 12 % and at cmp 224.5 its trading at a pe of 17.

Fundamentally looking very solid. Also Its peer cantabil retail still quoting at a pe of 31. Company guided for growing at 20 percent yoy . What Am i missing here?

As per management this year expecting revenue of 600 cr and ebitda around 30 percent. Next year growth around 20 percent. They have increased advertising spend in q3 which led to reduction in ebitda

Also since free float is just 15 percent , this took lot of beating . So volatility is expected. No reco, take your call

I haven’t analysed in detail. But here are my thoughts:

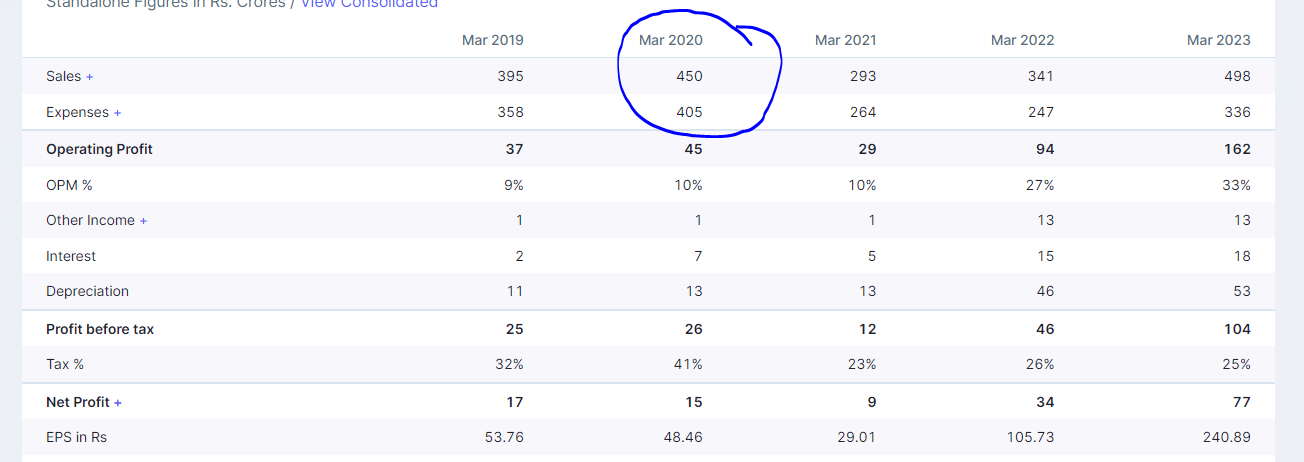

Credo Brands reported doubling of sales in 2023 as compared to 2021. What caused this sudden spike in sales and OPM to zoom to 30+ from 18-20 percent?

If I am being totally conservative and assign pre 2021 OPM of 20 percent on sales of 500 crore, PBT will be around 50-60 crores and PAT to be 40-45 crores based on 25 percent tax. Total number of outstanding shares are 6.5 crores. That gives us an EPS of 6-7 and P/E of about 30 on CMP. Things to ponder:

Why did the sales double in just two years of time? Has management given us a concrete reason?

Will they be able to maintain this rate? I think market is not sure about this and that’s why the price is down 40 percent from listing.

Based on CMP of 200-210, it appears it is priced to perfection.

Thank you. My bad, I stand corrected on sales part.

But employee and other costs have reduced drastically in last 2 years which contributed to the spike in OPM and bottom line. They are planning on expanding their stores though EBOs which will increase the costs and depreciation as well.

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/others interested can look to edit the post in order to meet prescribed guidelines. We have the responsibility - especially the thread initiator (assumption is he/she is a savvy investor) - to cater to bringing everyone on same page - quickly - if you know what we mean.