I have worked in collaboration with @Darshan_Gala the larger credit goes to him for putting lot of effort, I have tried to only put it here in a presentable format

About

Creative Graphics Solutions India Ltd. (CGSIL), headquartered in Noida, is India’s largest flexographic plate processor, with a legacy dating back to 1998 and formal incorporation in 2014. In May 2022, the group forayed into pharma packaging through Wahren India Private Limited. The company was listed on the NSE SME platform in April 2024. Today, CGSIL is a dual-vertical packaging specialist catering to leading FMCG and pharmaceutical clients across domestic and international markets.

Management

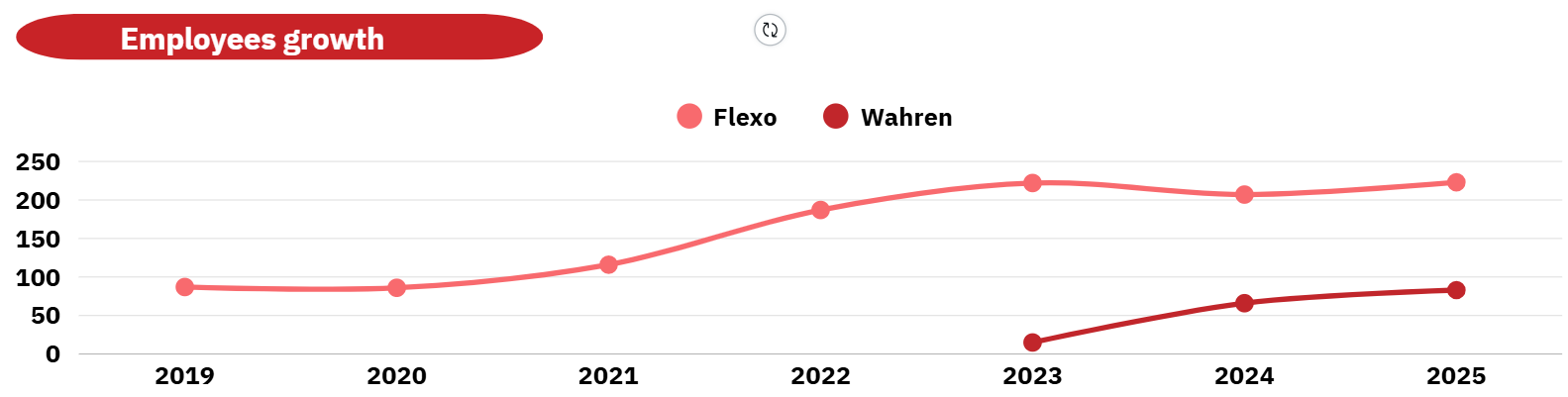

The company was founded in 2001 by Mr. Deepanshu Goel, a first-generation entrepreneur who began his journey in 1998 and has built Creative Graphics Solutions (CGSIL) from a bootstrapped Flexo startup—now a market leader in the segment—into India’s fastest growing Alu-Alu pharma packaging group. An alumnus of IIM Lucknow’s Strategic Management program, Mr. Goyal continues to lead the company as Managing Director, supported by a professional leadership team including Mr. Sanjay Sakale (CEO) and Mr. Pulkit Agarwal (CFO). The company today comprises a team of over 400 people, and potential delegation of leadership, onboarding a dedicated CEO for the Flexo division

Business Segments

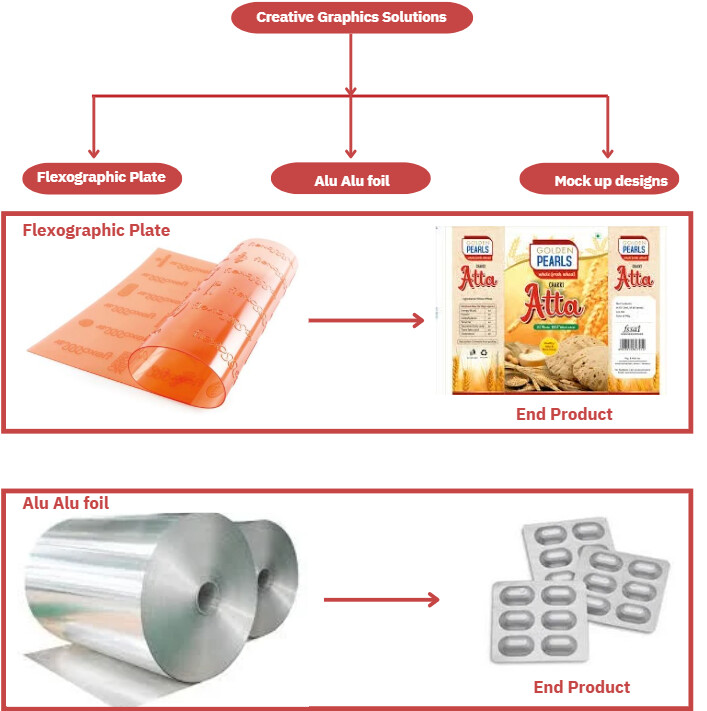

CGSIL owns two WOS: Wahren, which specializes in pharmaceutical packaging, and CG Premedia, which provides premedia services.

Flexographic Plates

Creative Graphics Solutions is a leading pre-press flexographic plates processing company used for high-resolution packaging applications as a critical consumable across a wide range of industries. These plates are used to print on labels, wrappers, pouches, sachets, and flexible films, serving sectors such as FMCG, dairy and beverages, pharmaceuticals etc.

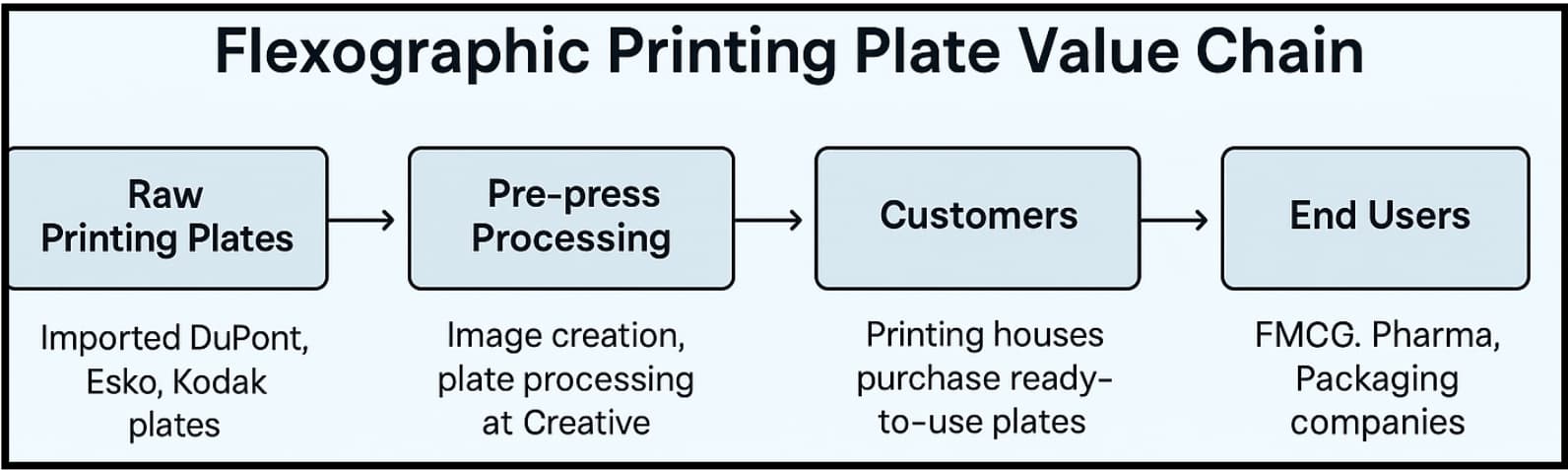

Value chain

- Blank photopolymer plates imported from Kodak etc etc

- Artwork processing → Laser exposure → Development. Core value-add with Esko/Kodak tech

- Plate dispatch + optional mounting support. Integration into converter workflow

- Mounted plates used to print the final product. Indirect impact via the plate quality

How does it work ?

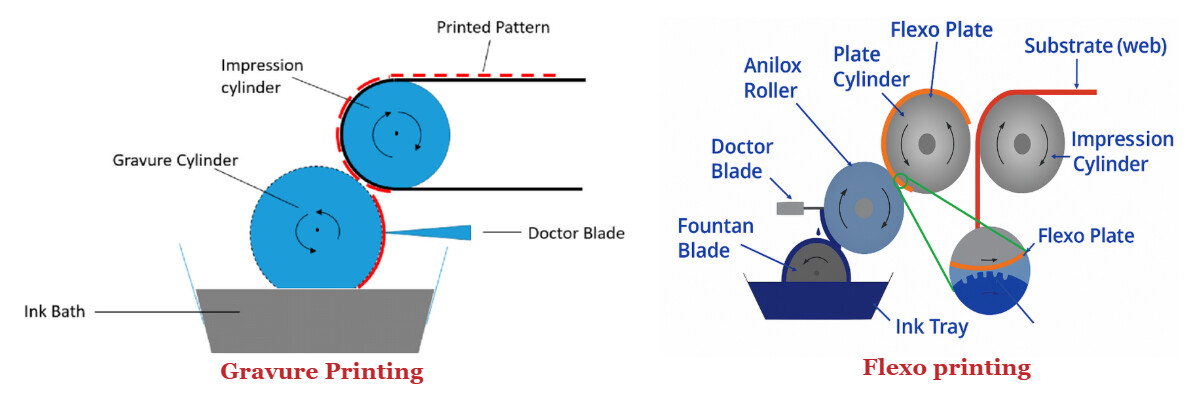

Flexographic printing involves creating a mirrored 3D relief image on a rubber or polymer plate. Ink is picked up by an anilox roller—engraved with microscopic cells for uniform transfer—and applied to the plate. A doctor blade removes excess ink to ensure precision. The substrate is pressed between the plate and impression cylinder to transfer the image, followed by quick drying to fix the print. (Image ref, under Gravuer to eco friendly flexo)

Manufacturing process

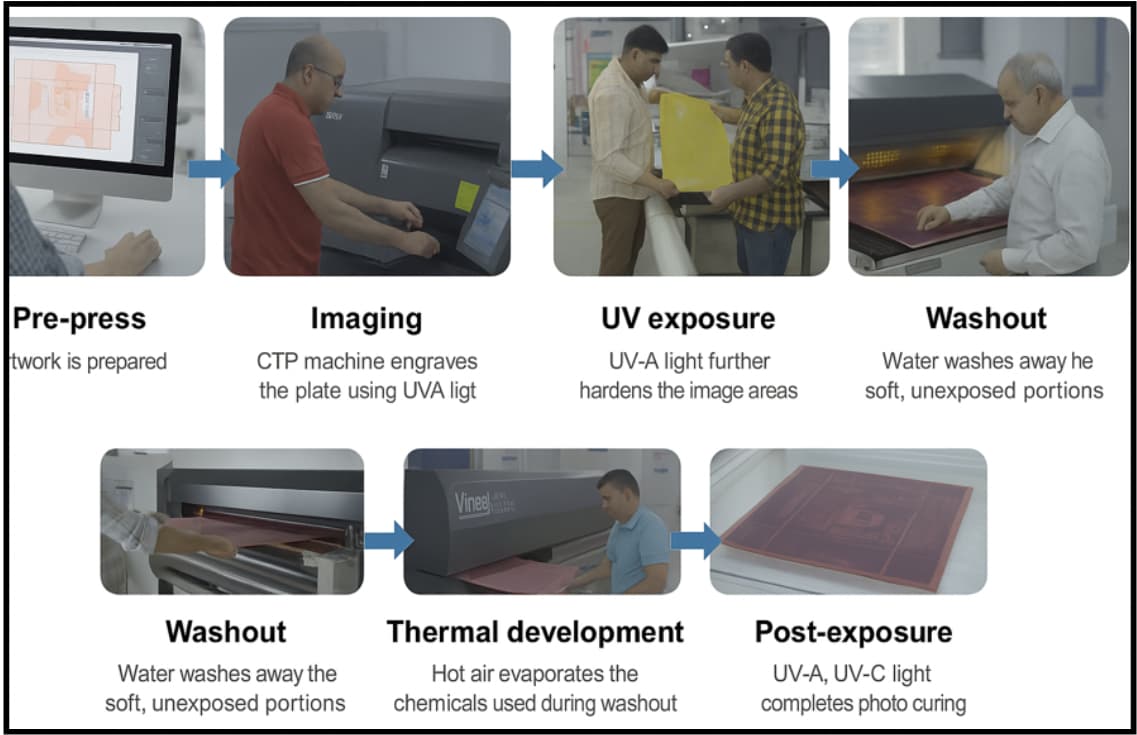

- Pre-Press: Design Design files are prepared digitally using tools like Esko, CorelDRAW, and Adobe Illustrator. The artwork is optimized for flexo printing with color separation, trapping, and layout settings. This ensures high-precision reproduction of the final print on the substrate.

- Plate Imaging : Digital files are transferred to imaging units (e.g., Esko CDI or Kodak Flexcel). High-power lasers engrave the image onto the raw photopolymer plate with exact dot precision. This step determines the sharpness and tonal quality of the final print

- UV Exposure: The plate is exposed to UV-A light to harden the imaged portions. Unexposed areas remain soft, forming the relief that holds ink. This process defines the raised printing surface of the plate.

- Washout: The soft, unexposed polymer is washed off using water or solvent washers like DuPont or SBR. This reveals the final 3D relief structure of the image on the plate. The plate is now ready for drying and hardening.

- Thermal Drying / Development: The plate is dried using warm air to remove moisture and residual chemicals. Machines like Vinod EVO or DuPont dryers are used at ~60°C. Drying stabilizes the plate for high-speed press usage.

- Post Exposure: The plate is re-exposed to UV-A and UV-C light to fully cure the material. This step enhances durability and eliminates any tackiness. It ensures the plate is press-ready for long-run print jobs.

Manufacturing Units

With 8 manufacturing units across India—Noida (since inception), Vasai (2014), Chennai (2017), Baddi (2018), Hyderabad (2018), Ahmedabad (2021), Pune (2022), and a JV facility in Kolkata—Creative Graphics boasts the widest manufacturing reach in its segment, enabling unmatched proximity to key pharmaceutical and FMCG clients. Two upcoming facilities, in Bengaluru (FY26) and internationally in Oman (FY26), will further deepen its domestic scale and global presence. Its widespread infrastructure allows it to serve both high-volume clients and short-run, quick-turnaround jobs—a key differentiator in a market shifting toward SKU fragmentation and faster packaging cycles

Flexo Growth Beyond India’s Borders

Creative Graphics has become the first Indian Flexo plate company to establish a plate processing facility in Oman—the first of its kind in the country. Set up under a hub-and-spoke model, the facility will rely on primary pre-press operations in Noida, with plates shipped to Oman for final processing. Initiated by a major anchor client—positions Oman as a gateway to the broader Middle East and Africa, enabling faster service, reduced turnaround times, lower costs, and improved margins

Industry Structure/ insight

The Indian flexographic plate processing market is estimated at ₹600–700 crore, growing at 7–8% annually, aligned with end-use segments like FMCG and dairy. The market remains highly fragmented, with over 50–100 unorganised players controlling ~65–70% share. Creative holds a 15–17% share, followed by Veepee Graphics (5–7%) and Numex (5–7%).

As of 2024, the global photopolymer plate processing market is valued at approximately $375 million, representing about 25% of the total flexographic photopolymer plate market. This segment includes companies that process plates and provide value-added services such as digital imaging, development (thermal/solvent/water-wash), and finishing. The broader market is estimated at an average $1.4 billion, with projected growth to $2.07 billion by 2030–2033, indicating a CAGR of 5.3%

Competitors Attribute Creative’s Rapid Growth to the Following

- Creative shook up the market with aggressive yet profitable pricing—undercutting rivals while keeping margins strong

- Pan-India presence, enabling faster turnaround times and deeper customer penetration.

- Superior service quality

Creative has delivered a 20–25% revenue CAGR since FY22—well above the industry’s 6–8%—driven by strong organic/ inorganic growth, and market share gains

Creative’s M&A Playbook

- 2017 – Acquired Color Dot Madras (Chennai) for ₹2.55 crore

- → Strengthened South India footprint; contributed ₹5.95 crore (6.6%) to FY23 revenue.

- 2018 – Acquired Bwin Digiflex (Baddi) for ₹4.11 crore

- → Unlocked North India presence; contributed ₹9.72 crore (10.8%) to FY23 revenue.

Other Insights

- Every Flexo press (Creatives customers) has a unique “fingerprint” — a calibration of plate, ink, substrate, and machine. Creative has India’s largest fingerprint database across 2,000+ printers, enabling first-time-right plate delivery with minimal waste. This deep calibration ensures consistent quality and protects customer IP — a key competitive edge and entry barrier

- Customer stickiness is strong and lower TAT (24- 48 hrs)

- Business is both capital and labor intensive.

- Utilization levels typically range between 60-65%, with peak load utilization being even higher.

- Although there are many small players, they generally cannot provide the same level of quality service, and continuous technology upgrades are necessary

From Gravure to EPR friendly Flexo (Optionality)

In packaging, monolayer structures are made from a single type of plastic (like LDPE or PP), making them fully recyclable and compliant with India’s EPR (Extended Producer Responsibility) norms. In contrast, multilayer films—commonly used in gravure printing—combine multiple materials. These layers can’t be separated during recycling, rendering the entire structure non-recyclable. Flexo printing, however, can print directly on monolayer substrates, offering a more sustainable and circular packaging solution that aligns with global and domestic recyclability mandates.

In flexographic printing, initial wastage during press setup is typically 50–60 meters, whereas gravure printing sees higher setup wastage — often 150–200 meters or more. While such losses may seem negligible in a long 20,000-meter run, they become significant in short- and medium-run jobs. This lower setup waste, combined with faster changeovers and lower plate costs, is driving a shift of short and medium run jobs from gravure to flexo, especially in SKU-fragmented categories like FMCG and pharma.

Flexo printing uses fast-drying, water-based or UV-curable inks that are more eco-friendly compared to solvent-based inks used in other processes. These inks have lower VOC emissions, making Flexo a more sustainable and environmentally responsible choice for packaging and labels.

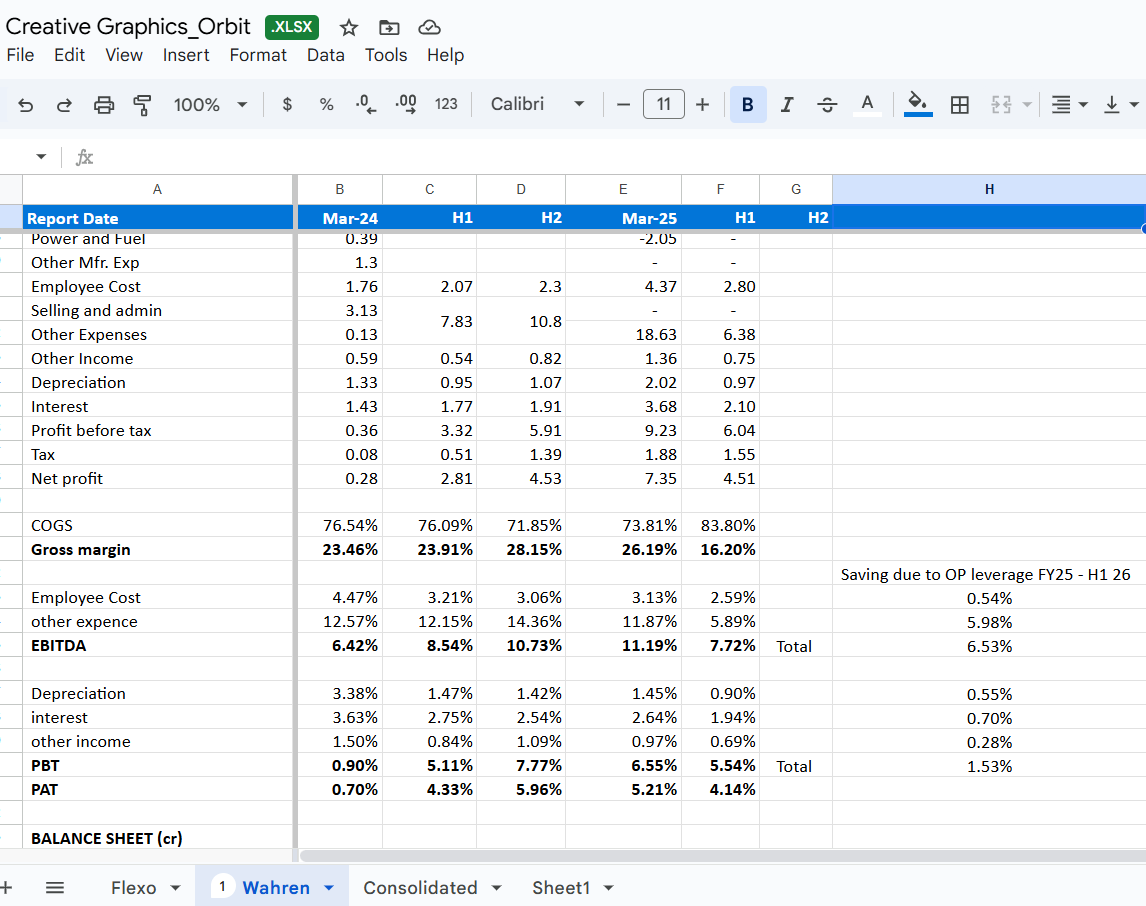

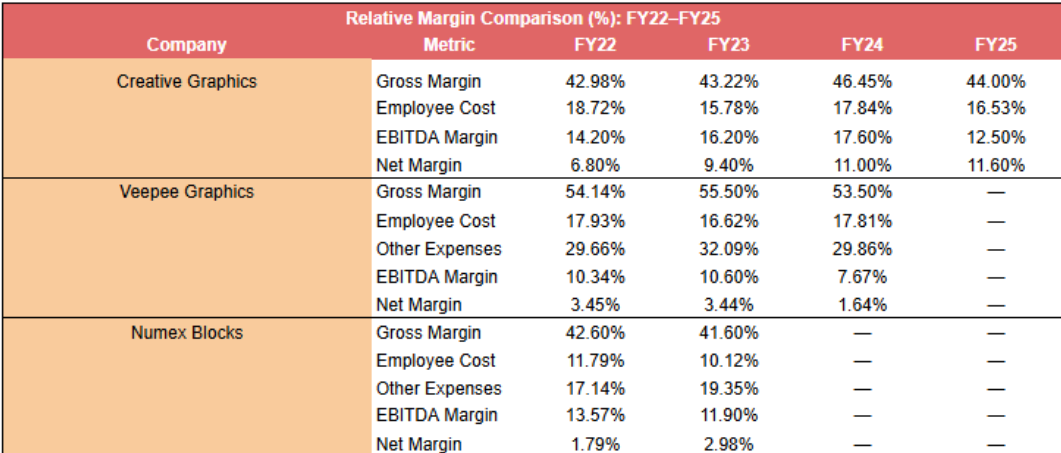

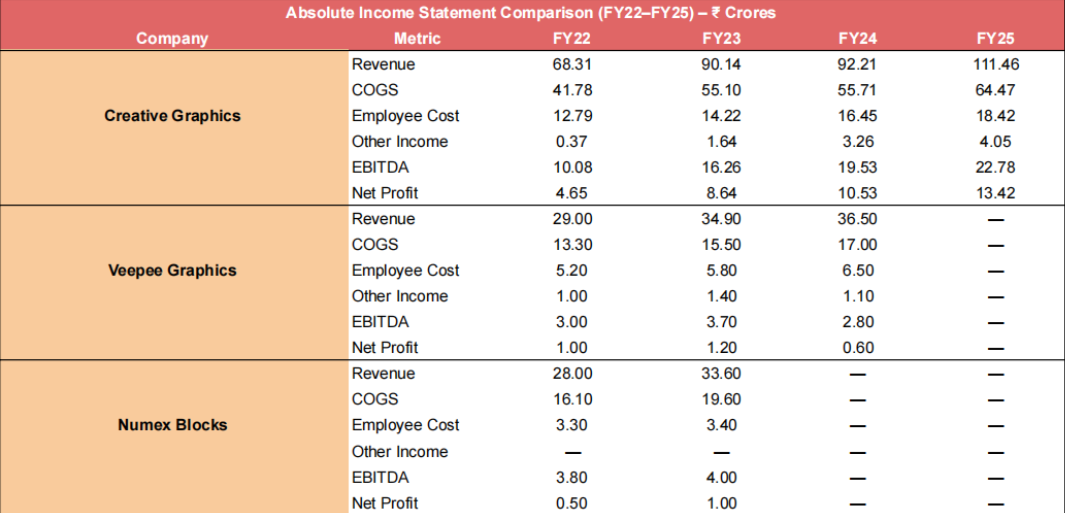

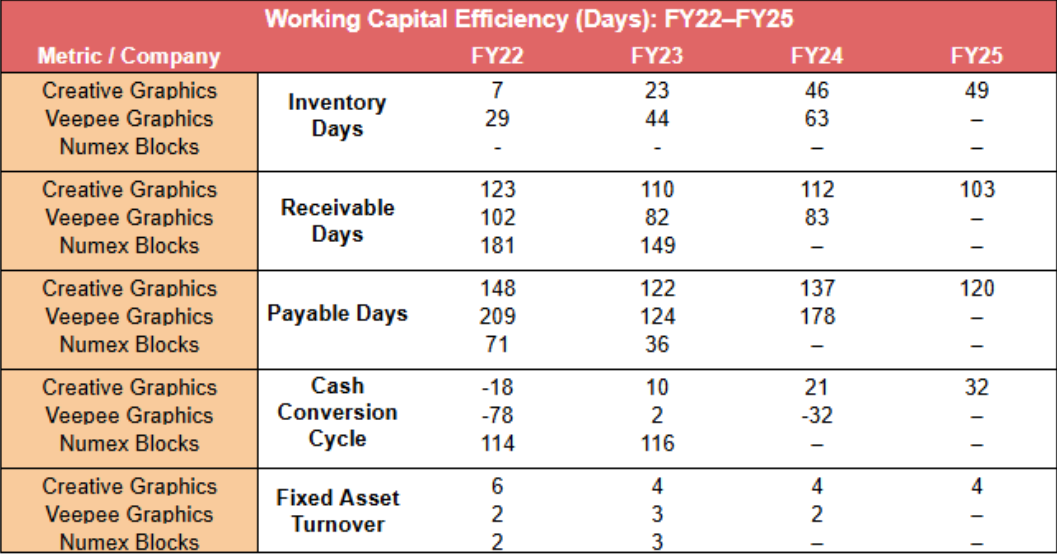

Financials & Peer Comparison (Flexo division)

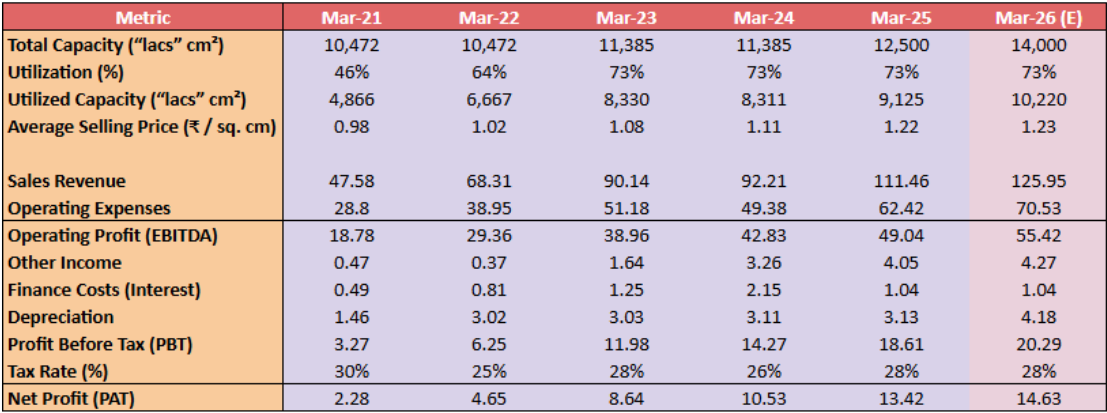

Forward Estimates

These have been purely made based on publicly available guidance

Wahren (CGSIL’s Bet on Pharma Packaging – A Proxy to India’s CDMO Boom)

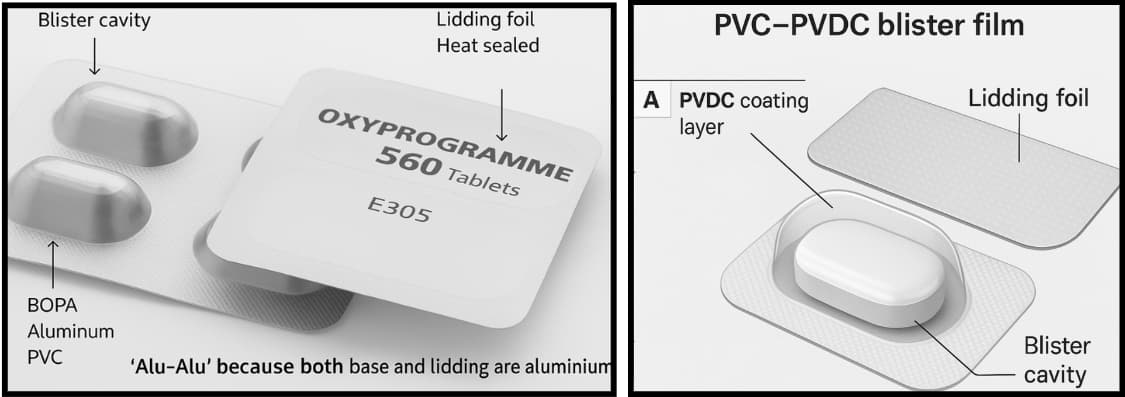

Wahren India Pvt. Ltd., incorporated in May 2022, marks CGSIL’s foray into high-barrier primary packaging for solid oral drugs such as tablets and capsules. Specializing in Alu-Alu foils, Wahren offers packaging that comes in direct contact with the medicine, providing the highest barrier protection against moisture, oxygen, and light—ensuring drug stability, shelf-life, and regulatory compliance

Wahren manufactures:

- Alu-Alu (Cold Form Blister Foil):

- Alu-Alu foil, also known as cold-form blister foil, is a specialized 3-layer laminate widely used in the pharmaceutical industry for packaging solid oral drugs like tablets and capsules. It offers the highest barrier protection against moisture, oxygen, and light, ensuring drug stability and regulatory compliance.

- The foil is made of three key layers: OPA (25 micron) for formability, Aluminium (45–60 micron) for barrier protection, and PVC (60–72 micron) for sealing, all bonded using adhesives, with a total thickness of approximately 135 ±10% microns.

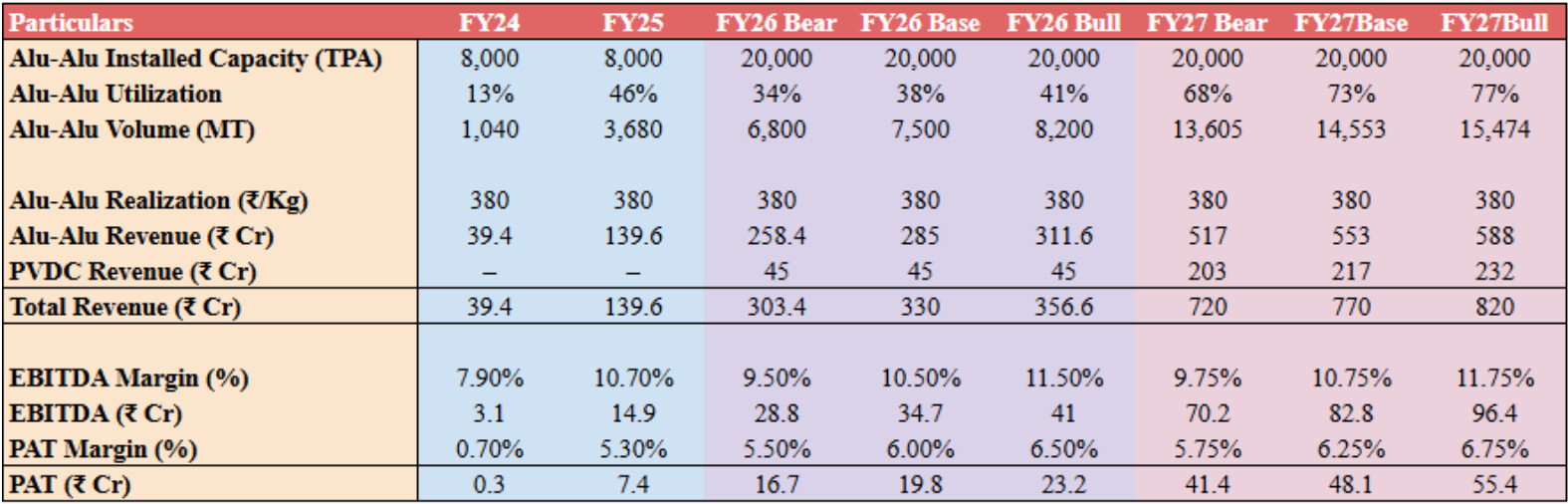

- Wahren’s current capacity stands at 8,000 TPA, with a planned expansion to 20,000 TPA by H2FY26, positioning it among the largest player in this space. (⅓ of indian market)

- PVDC-Coated Films (Upcoming):

- Polyvinylidene Chloride (PVDC) is a chemical that is coated onto a PVC monolayer to create a packaging material.

- PVC–PVDC is a widely used pharmaceutical packaging structure offering a balance of product visibility and moisture barrier. It consists of a PVC base (200–350 microns) coated with a high-barrier PVDC layer (40–120 GSM), enhancing protection against oxygen and water vapor — ideal for moderately to highly sensitive drugs.

- Unlike Alu-Alu, it allows visual inspection while still meeting regulatory stability needs. With commercial rollout expected in Q2FY26 at 1,000 T/month capacity, Wahren will enter a 5000-5500 T/month Indian market, competing with players like ACG ,Caprihans, Amartara.

Inside India’s Alu-Alu Ecosystem

- India’s Alu-Alu packaging market has long been controlled by legacy players, with high entry barriers and deep-rooted buyer relationships. Svam Toyal, though operational since 1981 entered the Alu-Alu space in 2011 and formalized its pharma foil business in 2018 through a JV with Toyo Aluminum, Japan. Bilcare (est. 1987) has been active in barrier films since the late 2000s, while ACG, part of the 1961-founded ACG Group, entered the segment in 2018 via its Shirwal facility.

- Svam has traditionally dominated the CFB market, often acting as a single-source supplier across key accounts, with little formal competition. Bilcare and ACG serve the upper end of the market with high-spec offerings but are generally priced above market, limiting their presence in the mid-volume pharma space.

- The Alu-Alu segment has seen a post-COVID influx of new entrants, attracted by its high ROE profile (30–40%), but the industry’s structural barriers have led to a high mortality rate. Players like Finepharmapack, despite commissioning a large 12,000 MTPA capacity, are already facing operational setbacks and exploring an exit. This highlights the difficulty of both formalising the unorganised market and displacing entrenched incumbents, reinforcing the rarity of success.

- Wahren India, founded in 2022, has quickly broken into this closed ecosystem, especially by entering accounts where Svam was previously the sole supplier. Becoming a parallel supplier alongside Svam — a benchmark player — reflects Wahren’s ability to match stringent quality standards in a market defined by legacy-driven procurement and high technical barriers

Market size

India’s Alu-Alu (cold-form) The pharma packaging market in India is estimated at over 60,000 metric tonnes annually, valued at approximately ₹2,400 crore, and is growing at a robust 12–15% CAGR. The industry is moderately consolidated, with Svam Toyal leading through a capacity of 16,000+ MT and holding around 25% market share. Svam, along with Bilcare, ACG, and Wahren, collectively accounts for 45–55% of the market. Wahren, is poised to become the largest player post-expansion. The remaining 50–55% is catered to by fragmented, unorganized players with limited scale and inconsistent standards.

The global Alu-Alu pharmaceutical packaging market is estimated at USD 3.5–5 billion, growing at 6–7% CAGR, with Constantia Flexibles as the largest player globally.

Raw Material Sourcing

Alu-Alu foil, or cold-form blister foil, is made using a three-layered structure — BOPA, aluminum, and PVC — bonded using polyurethane-based adhesives. The aluminum foil (8021 pharma-grade) is imported from China, from players like Henan Mingtai Technology Development Co. Ltd. The BOPA film is also sourced from China, through suppliers like Xiamen Changsu Industrial Corporation Ltd, known for high-quality biaxially oriented polyamide. The adhesives (polyurethane resins) come from South Korea, from companies like Kangnam Chemical Co. Ltd. The PVC layer is domestically available in India, aiding in cost and supply flexibility.

Precision, Scale & Trust: Why the Alu-Alu Market Resists New Entrants — and Wahren’s Rare Playbook

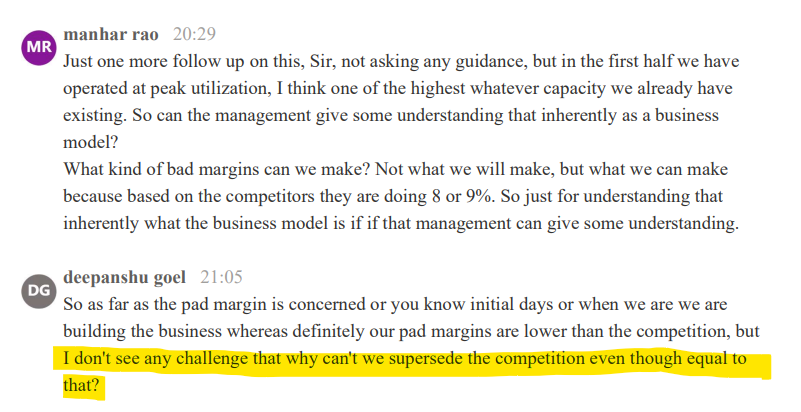

The Alu-Alu market in India is broadly divided into two segments: branded pharma companies and CDMO (Contract Development and Manufacturing Organization) players. Branded players, who sell medicines under their own name, are highly quality-conscious and typically prefer established vendors, even at a premium. In contrast, CDMOs are more cost-sensitive; a price difference of ₹5–10 per kg, combined with acceptable quality, is often enough to win business. This segment is primarily served by the fragmented 50% unorganized market, where vendors compete largely on price while meeting minimum quality parameters.

For new entrants, the go-to-market typically starts in the unorganised segment, where competition is intense, pricing cutthroat, and margins razor-thin. Most newcomers undercut incumbents just to keep factories running and gain initial share. However, they often struggle with working capital, as early customers—usually small, unbranded players—are weak paymasters. More critically, many fail to manage rejections or meet the stringent quality norms of the pharma industry. As a result, most either stagnate at sub-scale or exit within 2–3 years. In this context, Wahren’s ability to capture 5–7% market share in just two years and deliver a 6% PAT margin in H2FY26—despite competitive pricing—demonstrates strong cost control and sharp execution. With meaningful sales starting in FY24, Wahren is now at a key inflection point. Any breakthrough in exports or deeper wallet share with branded clients could further improve margins and working capital efficiency, enabling scalable, profitable growth.

Client Evolution: From Early-Stage to Established Pharma

Wahren’s client profile has evolved significantly since its early days. Based on FY25 numbers, nearly 80% of supplies are now directed toward smaller branded pharma companies, with the remaining 20% to CDMOs. The company has already begun supplying to leading names like Torrent and Intas, while audit processes are underway with Aurobindo and Sun Pharma. Large players such as Cipla and Dr. Reddy’s remain untapped opportunities. Going forward, deeper wallet share from these A-grade clients, along with traction in export markets, will be key monitorable

Quality parameters:

In Alu-Alu packaging, the biggest quality concerns are pinholes and leaks, which can compromise moisture-sensitive drugs. The foil must also withstand the cold-forming and filling process without tearing during production. Given the 1.5 to 2-year shelf life, actual validation of quality happens over time, making long-term product stability crucial. It typically takes up to 2 years to fully stabilize a plant to meet these stringent requirements.

On the customer side, regulated market clients typically take 12–18 months to onboard due to stringent stability testing and product registration cycles. If a vendor is changed, the buyer must re-register the product in the target market and undergo fresh stability testing—often lasting 6 to 12 months—before approval. This makes switching both time-consuming and costly, which is why regulated clients rarely change vendors. As a result, cracking into this segment presents not only a significant entry barrier but also a long-term opportunity for Wahren, offering high customer stickiness and premium pricing potential.

How did they do it?

Wahren’s rapid success can be largely attributed to a strategic hire from Svam—Dhan Singh, the key manufacturing head who had amassed 20 years of experience at Svam. Deeply involved in setting up Svam’s plant in partnership with a Japanese company known for its stringent quality standards, Dhan Singh brought strong technical expertise and an extensive network across the ecosystem. His move to Wahren played a crucial role in helping the company achieve exceptional product stability and gain client trust in record time.

Anti dumping on aluminum Import

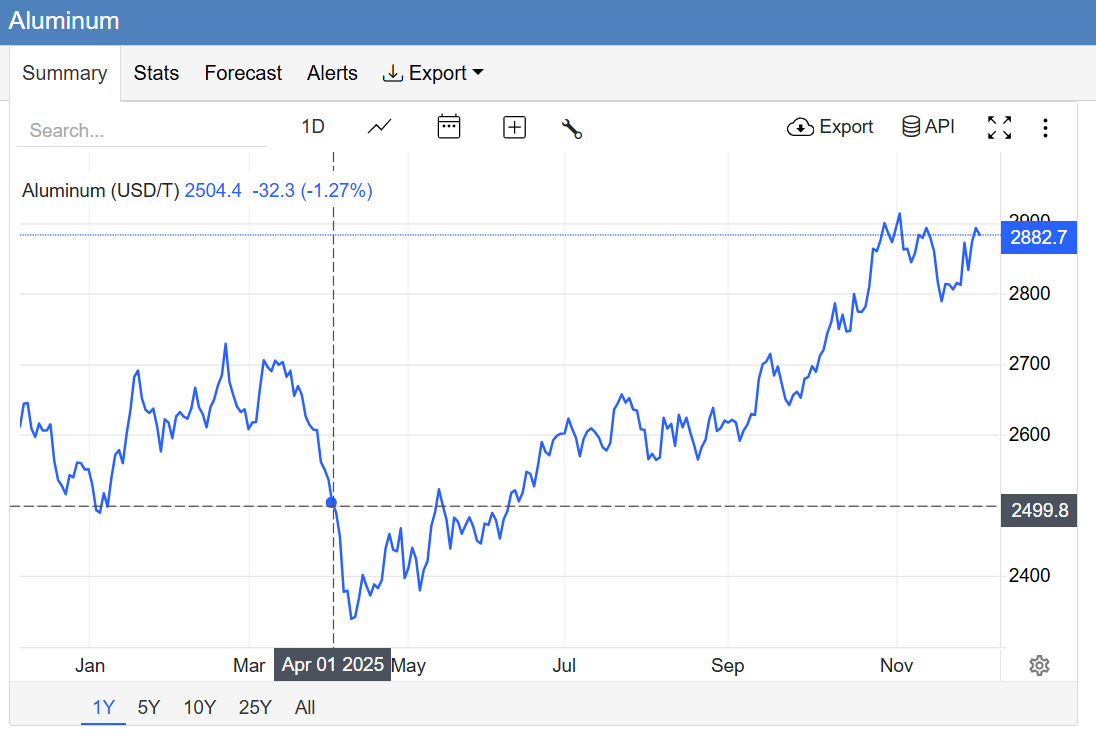

India imposed a provisional anti-dumping duty of up to USD 873 per tonne on aluminum foil imports (5.5–80 microns thick) originating from China, effective for six months, following a recommendation from the (DGTR). Later, on June 19, 2025, the government extended this measure to a five-year term, applying the duty on aluminum foil from China, as well as Taiwan and Russia, to safeguard Indian domestic producers against unfairly priced imports.

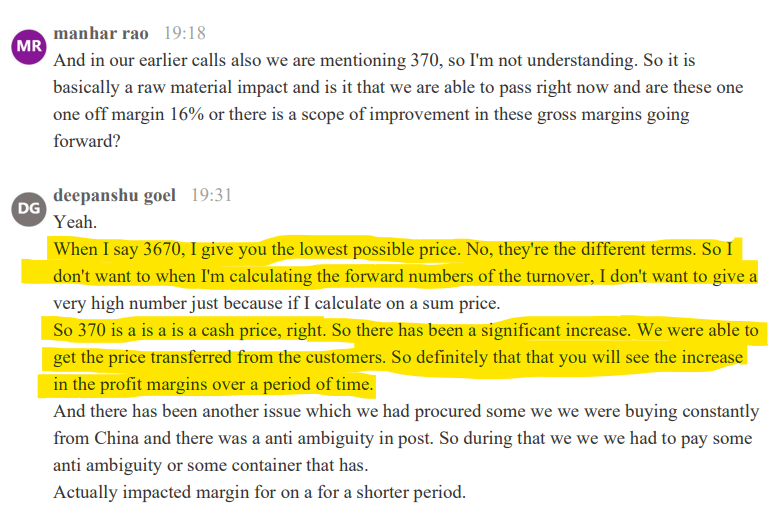

Since the majority of players import aluminum foil from China, we believe this is an industry-wide issue. Most players will now be compelled to source material from Hindalco—the sole domestic producer—or turn to alternative suppliers in Korea or Europe. Consequently, the incremental cost increase of 5–6% is likely to be passed on to customers. Moreover, pricing in this industry is typically reset on a monthly basis, which helps mitigate any significant margin risk or pressure

Most aluminum foil imports are in the 50-micron range, aligning with the typical 45–50-micron aluminum layer in Alu-Alu laminates. Recently, however, Wahren was seen importing 300-micron foil stock, indicating a potential partnership with a domestic rolling mill. With only 10–12 such mills in India, these partners could handle slitting, enabling Wahren to cut conversion costs.

Note : When you export a duty-paid product, the government issues a duty credit licence that entitles you to import inputs without paying customs duty, effectively offsetting the export-related duties.

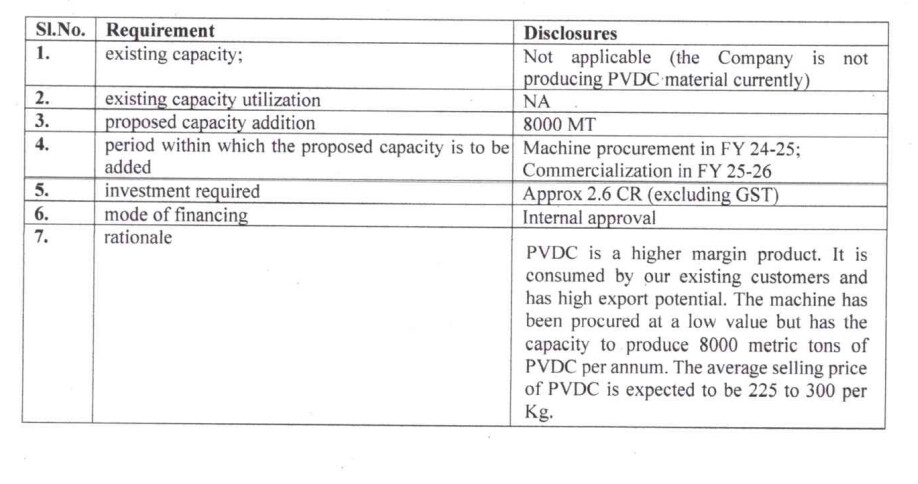

PVDC – Unlocking Competitive Edge in Pharma Packaging

- Wahren acquired a 1,000 MT/month PVDC coating machine from Radha Madhav Corporation Limited (RMCL) via NCLT proceedings at a fraction of its original cost (₹2–3 crore vs. ₹28–30 crore). The company plans to invest an additional ₹2–3 crore to refurbish it to world-class standards, giving Wahren an unmatched cost advantage and enabling it to compete effectively on both price and quality

- While similar capacity machines cost ₹15–16 crore, RMCL’s world-class 4-station PVDC line, valued at ₹28–30 crore, uses German Pagendarm technology to coat in a single uninterrupted run, ensuring higher quality, zero contamination risk, and superior efficiency.

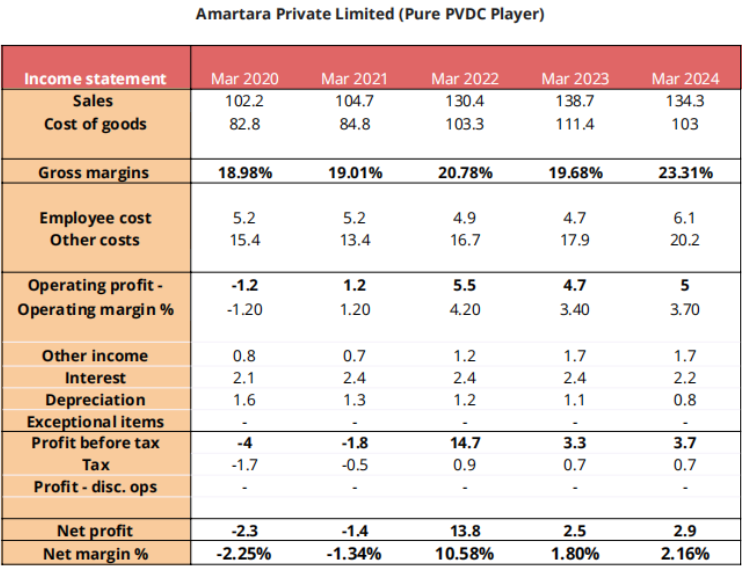

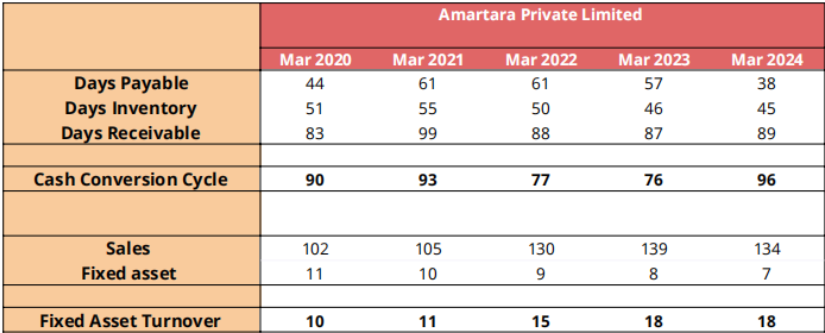

- In India, Bilcare and ACG are priced higher due to their superior quality. Bilcare’s patented inner coating is critical for complex formats like PVDC-inside, PVC-outside, where sealing integrity is essential — if not executed correctly, seal failures can occur within 6 months. Other players in the market include Amartara etc etc.

- In this industry, a basket-of-products approach offers a strong strategic edge, as clients for CFB and PVDC are largely the same. Wahren, already present in CFB, can leverage this base to enter customers with either product and cross-sell or up-sell others. With few competitively priced PVDC players—as Bilcare and ACG remain premium-priced—Wahren has a clear head start. If it delivers comparable quality, its low machine acquisition cost allows for aggressive pricing with strong profitability. The revenue potential from PVDC is estimated at ₹250–300 crore, implying a 40–50x asset turnover and making it a highly attractive return opportunity

Peer comparison and financials (Alu Alu)

Forward Estimates

For FY26, base-case PVDC revenues of ₹45 crore, assuming 15% utilization of the planned 12,000 MTPA capacity. On a combined basis, at peak utilization, Wahren’s capacities across Alu-Alu (₹760 crore) and PVDC (₹300 crore) segments have the potential to generate up to ₹1,060 crore in annual revenue.

Note: For FY26, we have assumed 70–80% utilization for the existing 8,000 MTPA Alu-Alu capacity, while the new 12,000 MTPA Alu-Alu line has been modeled at a conservative 10–15% utilization

All the above assumptions above are based on publicly available management guidance

Additional insights

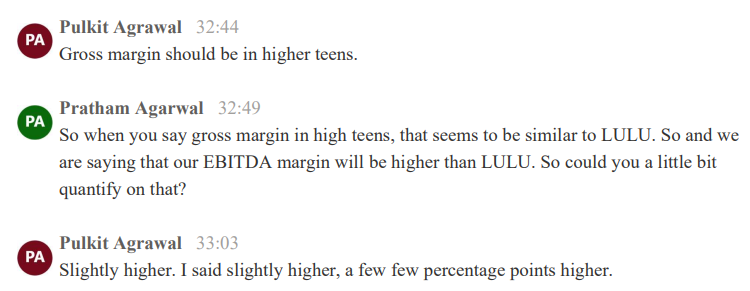

- Svam operates at 8–9% PAT margins with ~20% exports. Wahren, at 5–6%, has clear room for improvement through scale, exports (targeting 20% in FY26), and higher-margin PVDC, making 8–9% margins achievable over 2–3 years

- Exports allow 100% LC discounting, improving cash flows. With a better client mix and predictable offtake, Wahren can achieve working capital gains.

- While industry estimates peg the Alu-Alu packaging market growth at 10–15% CAGR, Svam has grown at ~30% CAGR between FY20 and FY24, even as Wahren entered and gained share. Meanwhile, GSM Foils, which supplies lidding foil (the sealing layer on Alu-Alu blister packs), has witnessed over 100% CAGR, further reinforcing the strong structural growth and downstream demand in the segment

Additional Info

While no reduction in debt or working capital improvement has been incorporated into our base projections, the management has indicated that both will be addressed through proceeds from a planned land sale. Creative Graphics Solutions India Limited owns a vacant industrial plot in Noida—Plot No. 57, Sector 164—measuring 4,000 sq. meters (43,055 sq. ft).

Risk

- Digital printing A Long-Term Threat, Not an Immediate Risk. Digital printing has been touted as a Flexo disruptor for over a decade, yet high ink costs and low throughput continue to limit its viability for mass packaging.

- Flexo graphy is a Small and saturated industry not leaving much room to grow

- Underutilization of Capacity with capacity increasing to 20,000 TPA (~2.5x current), any delay in export ramp-up or slowdown in domestic demand could lead to suboptimal utilization, affecting operating leverage and margins in the near term.

- Delay in PVDC Commercialization, The upcoming 1,000 T/month PVDC line was acquired distressed (from an NCLT asset sale). Any delay in refurbishing or qualifying the asset could push back revenue and margin upside from this vertical.

- Both the segments are heavily dependent on imports, epically Wahren is dependent on China

- Working capital pressure ,The pharma segment requires inventory stocking, long credit cycles, and batch-specific customization

- The company stocked inventory around Q3 FY25, which could lead to inventory gains in H2 FY25. However, margins in H1 FY26 may be depressed due to front-loaded costs from the upcoming capacity addition.

Disclaimer - I currently hold a significant number of shares in the company at an average price of ₹202, with transactions made in the past week, and my views may therefore be biased. Most of the points in this report are based on independently sourced information, which I will provide in the following post. All forward-looking estimates are based on management guidance publicly shared.