Craftsman Automation Ltd. is a versatile engineering company that caters to the automotive and industrial OEMs. With a strong presence in various segments, the automotive sector contributes to 73% of their total revenue.

Craftsman Automation holds the title of being the largest player in India when it comes to machining cylinder blocks and cylinder heads in the M&HCV and construction equipment industries.

Their product lines are neatly categorized into three divisions: automotive power-train, automotive aluminium, and industrial & engineering. The company is headquartered in Coimbatore, Tamil Nadu, and operates 12 plants across India.

Product Offerings:

Craftsman Automation Ltd is a proxy for both sectors Automobile as well as Industrials.

Automotive - Powertrain and Others: The range of products available encompasses various engine components, including cylinder blocks, cylinder heads, camshafts, transmission parts, gearbox housings, turbochargers, and bearing caps.

Automotive - Aluminium Products: The offerings consist of crankcases and cylinder blocks for two-wheelers, engine and structural parts for passenger vehicles, and gearbox housings for heavy commercial vehicles.

Industrial and Engineering: This segment can be further divided into two sub-segments. The first sub-segment focuses on storage solutions, providing comprehensive options for both conventional and automated storage systems. The second sub-segment specializes in high-end precision products, manufacturing aluminum products and offering services such as sub-assembly, material handling equipment, metal cutting, non-metal applications (such as washing and leak testing solutions), as well as tool room, mold base, and sheet metal capabilities.

Some positives :

- High rate of Free cash flow for the last 4 years.

- FII & DII Continually increasing their stake.

- One of the top four-component manufacturers of cylinder blocks for the tractor segment and has long-term relationships with major OEM

- Reinvesting a major parts of its profits at a high rate of return, (high capex and ROE)

Some of the negative factors:

- High debt - debt to equity is 0.99, but they are constantly reducing their debt. It was 1.4 in 2019. Also interest coverage ratio increased from 2 to 4 in the last 4 years

- Some promoter sold all their stakes.

- No insider hasn’t bought Craftsman Automation stock in the last 6 months

- Industry itself cyclic in nature

- Increasing receivables

- The top four customers accounted more than 40% of the company’s revenue

- The powertrain division accounts for about 50% of revenues and includes exposure to several engine components like cylinder blocks, cylinder heads which are related to ICE and evolution of EV is a potential risk for this segment

Growth triggers

- Rise in CV industry will help the power train business -The commercial vehicle industry in India recorded a 2% year-on-year growth . The powertrain division has substantial dependence on the Commercial Vehicle industry

- Acquisition of DR Axion - boost its presence in PV segment

- Company aspires to scale up its aluminum operations to at least USD500m over the next 2-3 years while the size of top 10 players is between USD1b to USD4b

- Current capacity utilization is around 65% and will increase to roughly 90% for individual segments.

- The structural trend of light-weighting, led by stringent emission norms (shifting towards aluminium castings to meet tight emission norms/EV needs) and an increasing electric vehicle (EV) mix, is likely to spur the usage of aluminum in the ICE and EV segments.

- EV opportunities - Company’s existing facilities in this segment - in Bangalore and Coimbatore

are in close proximity to major EV 2 Wheeler OEMs including Ola Electric and Ather,

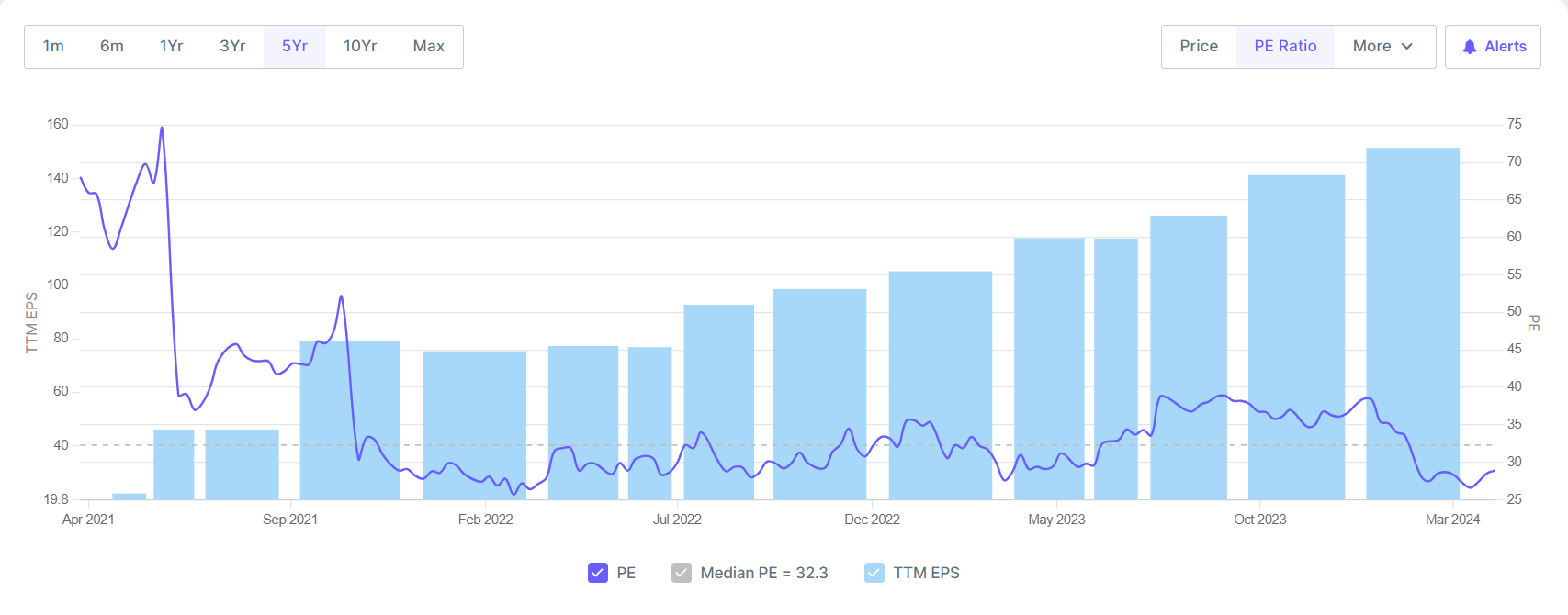

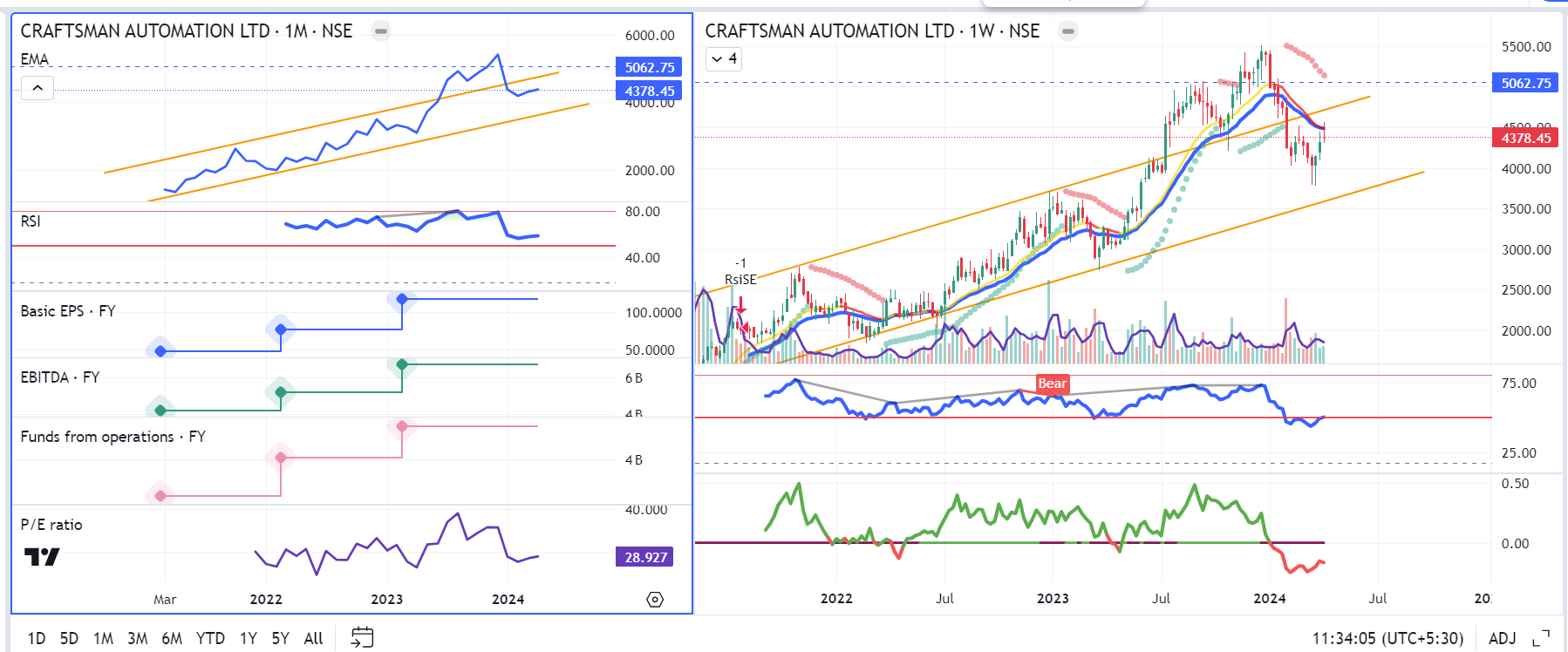

In Current dip stock seems to be undervalued now. (not a recommendation), currently being traded at PE of 27, boasting a 3.6 Enterprise value to Capital Employed ratio and a PEG (Price/Earnings to Growth) ratio of 0.7 suggest that the stock is undervalued when compared to its historical valuations.

4000-4200 seems to be buying area

Disc : invested in the current dip, will add more in the 4200 range