Zigly will launch its first store in Noida on July 1st 2023.

1 Like

Cosmo has entered into a definitive agreement to acquire business of 'Petsy Stores' for an cash consideration of an undisclosed amount. Acquisition to be completed by June 30th, 2023.

Last 3 years turnover of Petsy Stores , primarily in the Mumbai region:

FY21 - 3.38 crores

FY22 - 8.59 crores

FY23 - 5.22 crores (April 22 to October 22)

2 Likes

Will the amount be disclosed in subsequent stages?

Yes. Cosmo Ltd is a listed entity and hence acqusition details will reflect in its published accounts.

Source: HERE

Disclaimer: Invested. Not SEBI registered. I often go wrong and may change my views without informing anyone.

BOPP prices have crashed 30 Rs in last 15-20 days.

BOPET price now at 96.

As indicated previously, there is mismatch between supply and demand. Huge capacity additions had happened and cycle turned. I believe OPMS will further come down. Few companies in the sector may even show losses on net level.

4 Likes

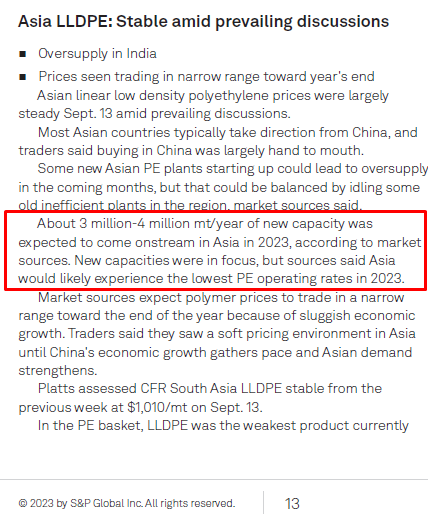

@jitnep If we further connect it to olefins supply-demand outlook…According to S&P reports and industry veteran’ comments, the supply of polyethylene (PE) is expected to lenghten due to many Chinese plants starting their commissioning. Initially, packaging manufacturers were predicting that the demand for polypropylene (PP) and PE would rise by the end of 2023, but the current outlook has changed.

There are noises about combined effect of inflation and Federal Reserve rates, there are concerns that the demand for the plastic packaging products in EU/US might stay slow for around 2 years.

1 Like

Can you share the S&P report? or the Source link?

Following corroborates to views of @jitenp

@Abha I can share part of it…these are subscription based 50 page weekly reports.

Following are comments on one of the PE grade… these comments are more or less same since many weeks and similar for other PE grades as well …like LLDPE, HDPE and others.

Following link is another good read on supply of PE.

China continues to pour money during this Overcapacity and weak demand cycle for commodity chemicals.

It is not mystery as to why they are still pumping money into petrochemical capex, They plan to move from making more basic petrochemicals for polyester fabrics and plastic packaging to manufacturing higher value products solar, EV,Wind etc.

As per my understanding from news and noises, I’ll go with analysts predicting demand and capacity rebalance in 2025.

According to me, for packaging products, end-use demand remains key and its related to existing higher interest rate conditions.

I might be negatively biased, Especially for export demands.

3 Likes

Hello Jiten, have been reading some of your comments and additions of cyclical commodities since a few days now , I have recently joined in and just learning as much as possible.

Coming to my question at hand how is your holding in cosmo films currently, and knowing you are working in the flexible laminates space do you still stand by your views from 2016 about cosmo films.

I am trying to learn this company more and more and learning about its capex growth in the last few years and seeing how the company is of a cyclical nature , current levels seem very attractive to capture the upcycle move, similarly the charts also show a good cup formation, ideally seeing the sector it had its peaks in 2016-17 then 20-21 and looks like it might pick up again , profit margins of the company and how they have been moving for competitors (nahar poly, jindal poly , polyplex, uflex) seem to be responding in tandem with the cyclical nature hence hinting an upward soon.

Could you please share your views on this?

i have no holdings in any Polyfilm stocks. Further to that, will not comment on any stock.

2016 views in any cyclical stocks may not be valid today as far as cycle goes. For that matter, even a 2022 comment may not be valid.

6 Likes

Just to qoute what Jiten has said before, play when the ROE and OPM’s are at yearly low levels of 6-8% and exit at the top. Keep in mind though about the new lever which may trigger in shape of Pet Care business as the this will be huge if played properly.

@jitenp, any idea if they have any ownership in Heads Up For Tales ( Pet care business as well ) ?

Does Cosmo have exposure to this entity if you know?

Thanks,

Abhishek

After Spending Good Time Here’s My Take

Industry Overview

The global flexible packaging market, which accounts for more than 60% of the total packaging market is expected to grow at a CAGR of 4.8% from $ 249 Billion in 2022 to $ 316 Billion in 2027.

Indian BOPP Industry has been growing at almost double of the India’s GDP growth rate over long term

As per a report from Grand View Research, the global speciality chemicals market size was estimated to be $ 616.2 Billion in 2022 and expected to grow to $ 641.5 Billion in 2023. Additionally, the industry is expected to grow at a CAGR of 5.1% to reach $ 914.4 Billion by 20307.

As per KPMG, the Indian speciality chemicals market represents 22% of the country’s chemicals and petrochemicals market with a valuation of $ 32 Billion. With the industry expected to grow at a CAGR of 12% from 2020 – 2025.

The Masterbatch market was estimated to be valued at $ 11.1 Billion in 2020 and projected to grow at a CAGR of 5.1% leading up to 2025 with an estimated valuation of $ 14.3 Billion. Synthetic Paper – Durable alternate to paper. Global market 100kMT (India 6k MT) - immense potential to grow.

The Indian pet care market may be smaller compared to the global market, valued at ₹ 5,100 Crore and it is growing rapidly with a projected annual growth of 25% from 2023 to 2027

Company Profile

Established in 1981, Cosmo Films Ltd.is the pioneer of BOPP Films Industry in India. Promoted by Mr. Ashok Jaipuria, the company is also the largest BOPP film exporter from India.

Cosmo Films Limited produces specialty films for use in labelling, lamination, and packaging. The films that it offers are cast polypropylene (CPP), biaxially oriented polypropylene (BOPP), and soon to be available, biaxially oriented polyethylene terephthalate (BOPET).

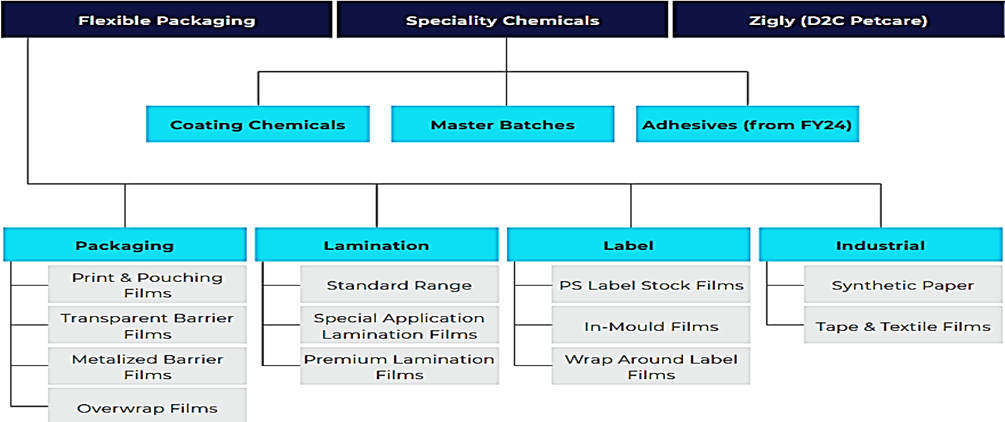

Cosmo First has expanded its portfolio to include Cosmo Speciality Chemicals having three vertical - master batch, coating chemical and adhesive and Zigly, a pet care brand that offers a full range of services and products for pets.

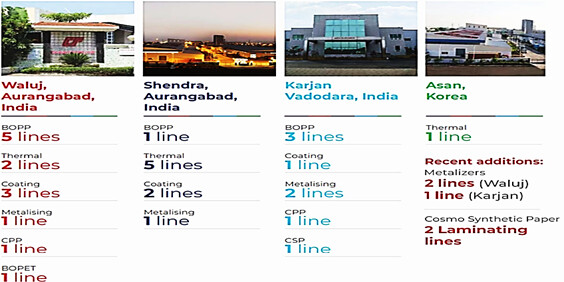

Company serves to 100+ countries and has 2 R&D labs with most sophisticated equipment and instruments, one in India & another one in USA.

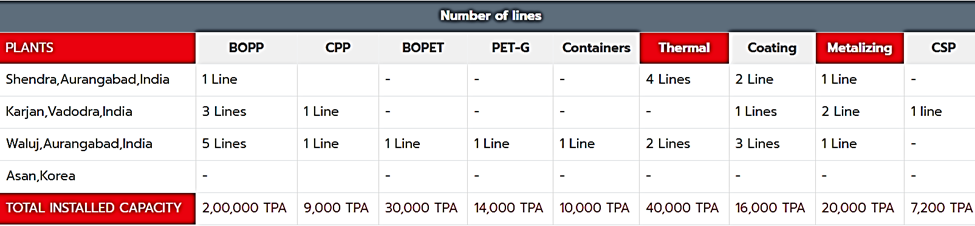

The Company has 4 state of the art manufacturing facilities - out of which 3 are located in India and 1 in Korea. The total installed capacity is as follows:

Why Fall?

-

Supply overhang and margin compressed across the industry leads to correction in the earnings

-

During FY23, the BOPP & BOPET industry faced excess supply due to bunching of several new production lines. Although demand continues to grow, the bunching of supply caused a margin drop and impacted the whole industry.

-

Currently India BOPP production capability is estimated at approx. 850k MT per annum. India domestic BOPP consumption is approx. 650k MT per annum and remaining is broadly exported.

-

Inventory loss

-

Fall in Volume More than Expected

Why We Are Studying?

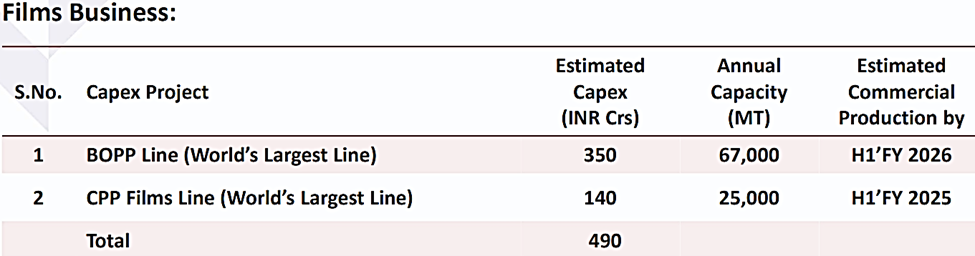

- Taking into account all four assets—BOPP, CPP, metallizer, and a PET sheet line—the company intends to spend about Rs. 490 Cr on CAPEX over the next two years, primarily on BOPP and CPP lines. total amount of all four is the CAPEX that company have committed.

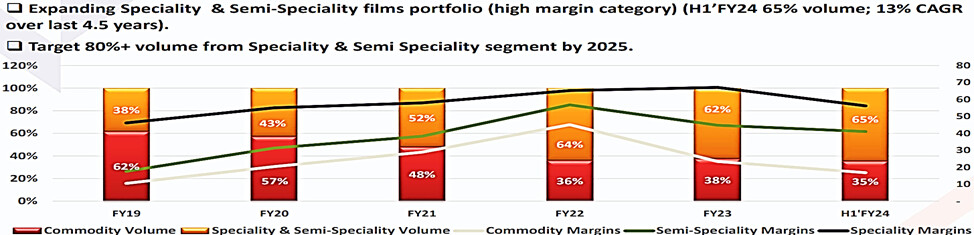

- By the end of the year 2025 the company hopes to Attain 80% of its volume from specialty products (currently at 65%), which will have an incremental impact of 2.5% to 3% to our EBITDA.

- Company with diversified businesses with target 20% CAGR topline growth in next 3 years coupled with commensurate return growth

- The Speciality Chemical subsidiary has got good initial response with its Packaging and Lamination adhesives and shall scale up the same in a phased manner from H2, FY24. Many of these new business initiatives post higher capacity utilization in the next 3-4 quarters will drive growth.

- The company has restructured its operations in South Korea during Q2 of FY24 and is currently moving its extrusion coating plant from South Korea to India in an effort to reduce costs. As a result, INR 3 crores in one-time restructuring expenses had an impact on the consolidated results, which would give the profit in the coming quarters.

Business Model

Cosmo First Ltd. operates a diversified business model across three segments:

Company have B2B Model and Accounts 50% Export of overall Business

Work on Cost Plus Model, Thus does not cost Benefit from lower input Cost that is Volume and Operating Leverage can only help to grow the Company

Product Portfolio

Manufacturing

Revenue Split

Geographically-45% followed by Domestic 55%

Key Clientele

Pepsi, HUL, P&G, ITC & many more

Competitive Strength

- One of the top four players in the world for BOPP specialty films, second-largest player worldwide for thermal lamination films, and specialty label films the largest supplier worldwide in the field of industrial application films.

- when the market is good, company make a bit more money (2% - 3% more) than their competitors from value added products. But when the market is not so good, they can make even more (6% to 7% more) than peers.

- Company serves to 100+ countries 2 R&D labs with most sophisticated equipment and instruments, one in India & another one in USA.

- Capital Allocation History Sound

Future Outlook

-

The BOPP (10th) and CPP (commissioned by 2024) line projects are moving forward according to schedule. By March 2025, both lines will be the largest in the world in terms of production capacity , and they will gradually boost the company’s production capacity by almost 50%.

-

The company has also started metallization of capacitor film recently which shall serve the rapidly growing electronics industry in India with Cosmo’s capacity in Phase 1 shall be 600 mtpa by Q4 of this year & revenue will be close to 40-50 Cr

-

Company’s New Business of rigid Packaging (Initial 40 Cr Investment) will add capacity in Phase 1 shall be 4,800 mtpa which should be able to generate between Rs.70 Cr to Rs.80 Cr of annual sales in nex 12-18 months.

-

Specialized Chemicals (scaling up in coming years) – Estimated INR 50 Cr Capex in next 3 years

-

Company with diversified businesses with target 20% CAGR topline growth in next 3 years coupled with commensurate return growth

-

D2C Pet Care businesses (19 nos. of experience centers as at Sept 2023 – plan to significantly increase to100+ in a couple of years beside online business)

Risk

- The margins, in near to medium term BOPP and BOPET margins are expected to remain subdued, more so for BOPET film due to an industry wide supply overhang .

- BOPET industry is very fragmented, and when prices rise, players often add large capacities, which lowers product realisations. Since raw material costs make up 60–65% of sales, profitability is also susceptible to fluctuations in raw material prices.

- Significantly higher than anticipated capital outflow for unrelated diversifications, abrupt moderation in profitability, delay in ramping up capacity, and additional debt-funded capital expenditures (including any cost overruns) all contribute to a weakening of the financial risk profile.

- Polypropylene which is key raw material for Production of films basically a derivates product and source from RIL, HPCL, OIL etc if any contradiction happens company may suffer

6 Likes

I have a “mixed feeling” about this stock. Below are the reasons:

- When the company had started to share that they aim to have 80% revenue from Specialty, there was no “semi specialty” segment, whose margins are lower than Specialty, but better than commodity. This “in between” segment was introduced later (i have not tracked the company every quarter so dont know when this introduction was done).

- I read through the concalls from FY 2023 onwards, and felt that some product introductions got delayed, examples: heat control films, adhesives. I think that is ok as many a times there are some delays, need to give some leeway to the company.

- Zigly, is an unrelated diversification. What was the need for this when the core business itself needed capital, and also that would have diverted management’s attention. Co. justifies by saying that it is a low capital business, or they invested very less capital, there is a dedicated business head from day one, etc. etc. Zigly is still loss making, and they have acquired another company in pet care.

- As far as the core business is concerned, there will be ebb & flow until 2026, in terms of revenues, margins, EPS and hence the share price could be under pressure for that time. Stock is for sure down about 50% from the previous peak, but am concerned that it could still go down from here.

- Looking at the past, the share price consolidates and tests one’s patience for a long time. But at the same time, it has given handsome returns.

- A possibility that I imagine is that the stock could fall from here, consolidate for some time, and then when the fortunes turn, could be a multi bagger…BUT…WHO KNOWS !!!

Disc: no investment, tracking

9 Likes

All in all doesnt seem to be a good investment… lots of hype and no delivery…

What do you think about thier increasing debt?

They are in a bad cycle and will pull through but I would have felt more comfortable with lower debt levels than what they have now

And this has shown up in the Q3 results for all polyfilm producers (BOPET as well as BOPP). I believe downcycle can last for some time.

Disc: No holdings in any Polyfilm stocks.

7 Likes

How to track BOPP and BOPET price please guide anyone?

1 Like

check out this website for all commodities prices

1 Like