agree margins will come down this quarter.

Also, sales will not increase much as there could be reduced export demand due to slowdown in Europe and US. Domestic sales will compensate a bit.

inspite of these valuation is very very attractive. promoter has bought at 875.

buyback is unlikely as company does not have so much of cash. they will prefer to pay off debt.

Zigly needs to be hived off and PE investors should fund its growth.

1 Like

I think market is expecting drastically poor results in Cosmo, given price levels. It is true that SRF reported poor results for the Packaging Films Business. However, Cosmo is different from most other Packaging Films companies in 2 respects (which has impacted the performance the most)

-

Cosmo is till now a pure BOPP (with some CPP)play. BOPP margins though down are still respectable. Its BOPET which is under higher stress. All other than Cosmo are majority BOPET (>60%). Thus margin erosion for Cosmo, will be limited.

-

Most players have production facilities in Europe - which are hit by high power costs and have created a drag on margin. Cosmo on other hand manufactures almost all in India (except for a small facility in Korea). There is NO impact of “European Crisis” on Cosmo.

This quarter will be the real test of Cosmo’s claimed “Speciality” volumes and it being insulated from commodity margin movements. If it stands this test, results are likely to be in the range posted above on 1st Oct. If it happens, I hope market to acknowledge.

Note: Invested. On Wait and watch mode.

4 Likes

| Polyplex | Cosmo Films | UFLEX | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Q2-23 | Q1-23 | Q2-22 | QTRs | Q2-23 | Q1-23 | Q2-22 | QTRs | Q2-23 | Q1-23 | Q2-22 | |||

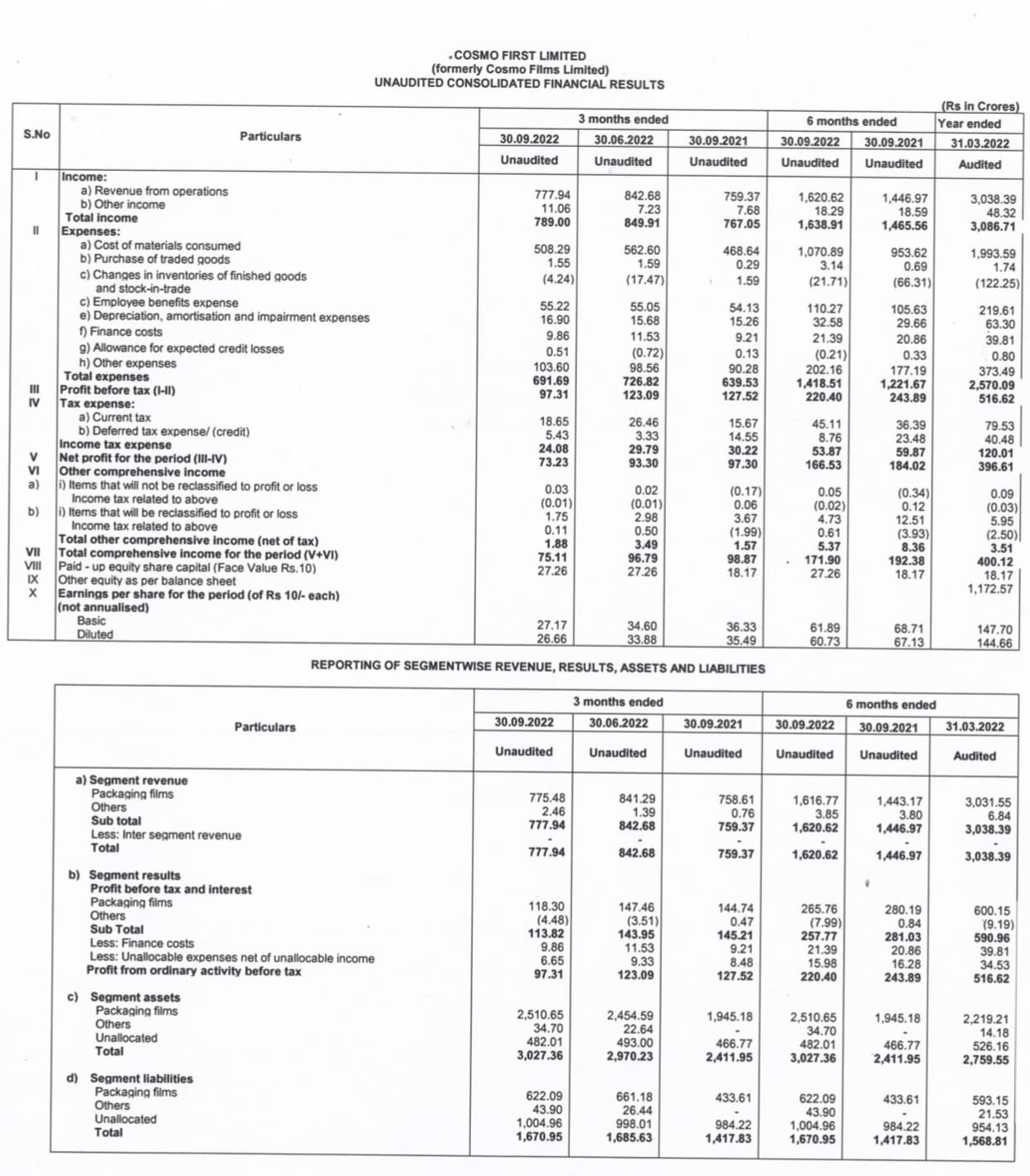

| Sales | 208929 | 203258 | 154758 | Sales | 777.94 | 842.68 | 759.37 | Sales | 373755 | 399446 | 298390 | ||

| Gross Profit | 74134 | 87400 | 66088 | Gross Profit | 274.34 | 295.96 | 292.03 | Gross Profit | 131838 | 155693 | 114551 | ||

| EBITDA | 32732 | 43473 | 27661 | EBITDA | 124.07 | 150.3 | 151.99 | EBITDA | 49320 | 72496 | 42451 | ||

| Gross Margin | 35% | 43% | 43% | Gross Margin | 35% | 35% | 38% | Gross Margin | 35% | 39% | 38% | ||

| EBITDA margin | 16% | 21% | 18% | EBITDA margin | 16% | 18% | 20% | EBITDA margin | 13% | 18% | 14% |

Please check polyplex origina values without additional income and some currency exchange added value things.

cosmofirst speciality worked and co. Posted descent results in this turbulence time. Just margins dropped from 17% to 15% as management said 30 to 35% of their biz is exposed to commodity. If you compare peers like UFLEX margins drop from 18% to 11% when comapre to previous quarter. So i believe management is walk on talk and without words speciality business had showed up in results.

2 Likes

Yes. The revenue is excluding non operational items for all.

1 Like

went through the investor presentation. all seems to be exceptional. slight drop in margins this quarter. with commissioning of new plant EBIDTA and cash flows will be higher. Is there anything being missed… stock crashed to 52 week low…

1 Like

I turned out to be partially wrong. Not in terms of reasoning on both points, but in terms of underestimating extent of margin fall and something totally unexpected - fall in speciality volume. Whatever may be the reason, bottomline is - result is far below expectation on absolute basis.

However, I also did an across the industry comparison of topline and PBT - other income to isolate impact of other income and differential tax rates to understand how the companies performed relative to each other. Here is the table without comments.

| Q2FY23 | Q1FY23 | Q2FY22 | Change QoQ | Change YoY | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Listed Companies | Rev | PBT* | Rev | PBT* | Rev | PBT* | Rev | PBT* | Rev | PBT* |

| Cosmo First | 777.94 | 86.25 | 842.68 | 115.86 | 759.37 | 119.84 | -7.7% | -25.6% | 2.4% | -28.0% |

| Ulfex | 3767.76 | 160.93 | 4031.91 | 462.49 | 3027.31 | 206.40 | -6.6% | -65.2% | 24.5% | -22.0% |

| PolyPlex | 2089.29 | 161.98 | 2032.58 | 282.20 | 1547.58 | 188.77 | 2.8% | -42.6% | 35.0% | -14.2% |

| Jindal Poly | 1414.40 | -30.97 | 1592.21 | 313.02 | 1456.43 | 288.50 | -11.2% | -109.9% | -2.9% | -110.7% |

| SRF - PFB | 1331.02 | 101.44 | 1496.00 | 295.17 | 1071.74 | 179.51 | -11.0% | -65.6% | 24.2% | -43.5% |

Notes:

*PBT is taken as PBT Less Other Income to isolate impact of other income and differential tax rates

** In SRF - EBIT Instead of PBT, as it is in multiple business and hence, PBT for packing films not available

Going Forward, Q3 margins are still under pressure. So I feel Q2 may not be bottom, but Q3 could be. Given BOPET present bad shape, the new plant couldn’t have started at a worse time. Would be happy if it manages to breaks even at EBITDA level in Q3. In absense of knowing margin data from day to day, I can only work on management commentary. And so far they have tended to downplay the fall - so I am taking a rather pessimistic view of Q3. Some additional points:

-

Q3 is slightly lower demand quarter due to seasonality.

-

Plant shutdown for maint, is also typically done around Diwali.

-

Incremental burden of BOPET plant Depreciation and Interest will be there.

-

Q4 is generally a strong quarter demand wise

-

They would possibly get some speciality products going in BOPET by Q4. Even at 10% of capacity it will make a positive difference.

-

Some margin improvement possible in BOPP hopefully in Q4 as demand starts catching up.

3 Likes

markets discount the future cash flows… analysing only Q3 is not correct. there are many more quarters and years to come.

the value add products they are getting into like adhesives will surely improve sales and margins. domestic demand for these products is increasing.

one good thing to notice is that while they have plans for capex, it will happen 2 years later and by then the new plant would stabalise and give enough cash flows to go for expansion from internal accruals alone.

1 Like

Regarding the unrelated business of Zigly. Petcare is a booming business in India. There are so many players which have raised money at high valuation. going forward there will be consolidation as well.

While it may be negative cash flow right now (which helps in tax reduction), it has great future. But one critical point is the business needs to be hived off at the right time… to enable raising capital and M&A opportunities. To my mind promoters should do it by Sept 23. - almost 2 years since start. Beyond that it will prevent growth and also inorganic growth opportunities which is typical of such businesses.

4 Likes

Agree. But market are extremely short term focused right now, particularly so when the performance falls. It then tries to assess by when reversal will happen.

All the new business and even the new BOPET line will take time to show results. Today people are extremely wary of uncertain future cash flows and literally discount it to zero, as opposed to bull markets when mere announcements are sufficient …

I may for one believe, if zigly is done right than that itself will be worth the current market cap of Cosmo in 4-5 years (At 500 crore revenue, 4x time sales = 2000 crore - this wasn’t unheard of in 2021). Reality - today even the cash flows of its film business is undervalued and cosmo is available 0.65 times sale.

4 Likes

Buy-back meeting announced. Smart move. Pathetic valuations and despite lower commodity margins, cash flows are still sizeable. Lots of cash/equivalent on books.

Hope they do a max (25%) or near to max at 1100-1200 per share.

Would be interesting to see if promoters will participate in the tender or not (I am assuming tender route, 10% open-market buyback will be a pity).

Disc - Still invested.

1 Like

Infosys has also opted for this route. Though personally I may lose on the sale of a few shares to the company, but I felt that Infosys buying from the market may send a bigger message to the market. It seems that they will buy at their preferred rates whenever it suits. However, in this case (Info), their buying of 5 crore shares from the market should affect its price. Shouldn’t the Cosmo shares also benefit by their buyback from the market?

Just my two cents. May be my logic is not correct.

my belief is Polyfilm cycle will struggle. Best maybe behind. Lot of capacity coming up in the next 3 years.

5 Likes

On a short term basis Q3/Q4 FY22 were the best and indeed they are behind us. Q3/Q4 of FY23 are not likely to be anywhere close to it in terms of margins/kg.

Would you have some kind of compilation of capacities coming up in the next 3 years in India, by technology (i.e, for BOPP, BOPET, CPP) alongwith the base (capacity and demand) for today?

That would provide a meaningful base to judge likely weakness/strength in the broad segments.

listen to Cosmo concall for the details. We have to understand that whatever companies say, this specialty is something which we have to take with a pinch of salt. What is specialty now, may become commodity in 12 months. There will be some films which will have higher spread, but generally they are a small percentage. What one needs to find out is the blended spreads. We also do have to understand that in this business, 20% EBITDA margins are not sustainable for long time. I think margins will shrink more.

Not commenting on any stock. More on the BOPET and BOPP industry.

4 Likes

I would like to bet more on promoters rather than betting on stock alone. Till now they have given a good reward to their investors. if we read the older concall we would know that they believe in walking the talk. The stock belongs to Commodity category but we must remember that company is trying hard to get away with the commodity business. Their apporach towards other business is proving the same. They are hard working guy and I firmly belive that are going do something good for company. I would like to have an update on their Heat protection film. Once or twice they hinted that they are devloping film which going to be used on glass to reduce the inside temp. Presently most of the company are importing trading it buy importing from China. Cosmo is devloping this at its own. It may be a game changing factor for a small company ike Cosmo Film. Valuaiton are still attractive. We have to look beyond Commodity for this company.

Discl: Invested

2 Likes

Fully agree.

Also value added products will always have better margins. As supply will not increase so easily given technology and investments to be made.

In commodity business All players are aware that too much capacity addition will lead to glut. Only those companies which have done investments at right time will benefit. Cosmo has surely done it at right time and commissioned before others. They have learnt from past mistakes!!

Operating Margins can come down but on company level ebidta margins will improve due to scale.

Moderate debt is also a very big positive of the company.

1 Like

Agree. Speciality is transitionary and blended margins are what matters. However the key question looking forward is - are there enough opportunities to have a pipeline of innovative products which can keep replacing the ones which are turning into commodities and does a company have capability to do that consistently both from a research and operations perspective. If answer to both can be yes, then you have a potential outperformer.

Unfortunately, I don’t have the background in this industry to answer either question independent of management commentary. If more knowledgeable folks can help us understand this, we can perhaps make a more informed choice.