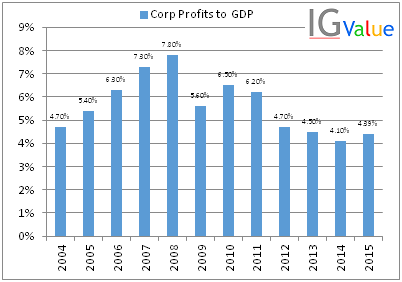

Corporate profits to GDP is a metric that Buffet is fabled to be using. He thinks anything over 6% is too much. India has gone through its share of ups and downs on this metric.

My detailed thoughts on this topic are at: http://www.igvalue.com/2015/04/macro-factors-corporate-profits-to-gdp.html

(Did not post them here to avoid verbosity)

The following graph shows that there does not yet seem to be an earnings bubble even though the NIFTY P/E was over the 87.5 percentile of the last 15 odd years when it was at 8800. Now its below that percentile point.

The questions that I am trying to answer are:

- Given the change in the mood of the country over the past year - will the expectations of earnings growth be actually realized?

- If the expectations are realized which areas of the listed companies will take a larger share?

- If the earnings growth numbers are not realized can corporate profits to GDP continue to languish at under 5%? Given the cyclical nature of the economy I find that hard to believe.

- Is my data - which has been pieced together from several news stories (largely from the Telegraph, TOI, ADB, and others) really correct? Would someone know a better source of this data in India?

In the book Capital in the 21st Century by Thomas Piketty - the author did not present several data points for India citing lack of data availability and willingness of the authorities to make the data public. I hope this is going to change in the future as it does not bode well for our markets. And after all - all value investors in long only type strategies benefit from the market returns.

Thanks.

3 Likes

My two cents - Interesting topic. I think corporate profits to GDP may remaining low only for companies which serve Indian customers as this is the age of information(internet), cut-throat competition and globalisation. Every company knows what every other company is doing and every customer knows which company is offering the best deal. So profit margins squeeze even as GDP expands.

Most profitable areas of investment will probably be the usual ones - pharma, financials and IT.

IT and pharma has low cost advantage. Pharma will grow the maximum as more people are growing old, more affluent relatively and more are getting medically insured.

@vicky_7900 I completely agree with you on the fact that companies serving Indian customers who are not brands will hurt especially where the markets are not growing rapidly (like Pumps). And exporters are golden because the rupee will continue to slide.

Pharma also seems to be area of Corporate profit growth. The question is about IT - can it really continue to grow? It already is a very large percentage of the pie.

Financials profits are not real because the real financial profits have to be seen over a period of a decade - Your loans are doing just fine until they’re not!

About IT - Noticing that the promoter holding is reasonably high in large caps (in TCS, which is 8.x% of nifty-50 by weight, it is ~74%), which indicates that promoters believe there’s growth to be had. But the pace will be less than pharma of course, as indicated by P-E ratios.

While I agree with the promoter holding point - I would also say that a promoter company like TATA Sons is unlikely to sell stakes in anything. They would typically just increase the dividend payout and invest elsewhere or have that company invest in another venture. This factor reduces the importance of promoter stakes.

Infosys on the other had has diluted promoter involvement and stake.

If TCS’s valuation is correct it need to catch up to over 60% of the scale of IBM or Accenture. That is a very tall ask. Not that I don’t believe they can but the international branding required for it is immense.

I worry that in IT the market size is going to become a limiting factor.