Cords Cable Industries

OVERVIEW

The company operates under a single product segment i.e. Cables. The company mainly focuses on specialized cables which differentiates it from other cable players in the country.

The vision of CORDS is to be recognized as a leading global player, providing products and services, offering comprehensive solutions to the electrical and data connectivity requirements of businesses as well as household users. It focuses on capturing new markets by developing customers in new and existing territories, to provide new cables for special applications like solar, marine, low temperature cables, cables for automobiles etc.

Clients

New Clients added in last two years - EPC contractors like Bombardier, Welspun, GE, ABB Global, Alstom Transport etc.

existing customers - L&T, Siemens, EIL, NTPC, BHEL etc.

Future Outlook

Infrastructure Boom: Company is engaged in cable manufacturing products used in projects hence demand is likely to increase significantly as Government of India has focused again on infra projects and approvals and investments in new projects will entail higher turnover of the Company which will ultimately increase the profitability of the Company.

Efficiency: Also, company has been continuously working upon achieving better efficiencies, cutting costs at every stage of production, better preventive maintenance, making product mix having higher contribution and achieving higher production so that company can achieve the scale of economy and maintain higher margin of profit. Expectation of company in terms of increase in its profits is in line with the increase in its activity and market penetration in the potentially improving macroeconomic scenario in the country.

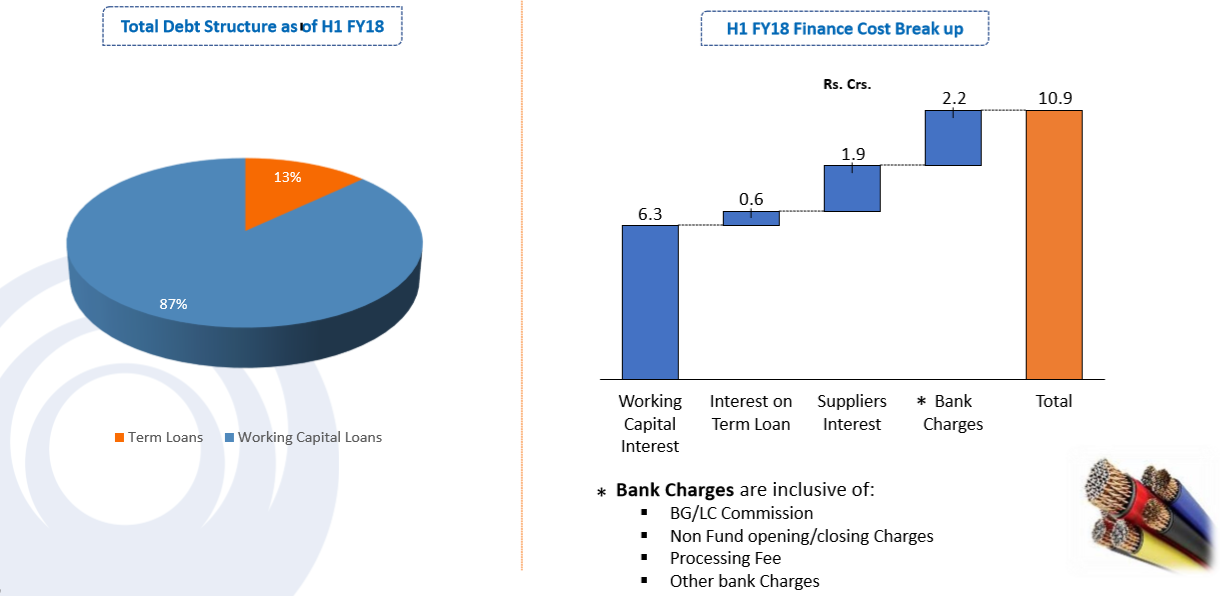

Debt Reduction: Further, interest rates are likely to soften in near future and your company is expected to save significantly on its interest outgoes. Additionally, with the ongoing repayment of term loans availed for project financing, your company is expected to save on its financial expenses

(Already 30% debt reduced this year)

Huge Opportunities

freight corridor, smart city, railway signalling and protection system and infrastructure projects.

Promoter Holding

51% (all unpledged)

Risks

Promoter Holding decreased from 58% to 51% (Partners exited at 31 rs per share to current promoter)

Since IPO in 2008, the share price has remained in very strict range (not sure about the reasons)

No Dividend Payments since 2010-11

Promoters don’t have any set goals (in terms of revenue guidance and growth for future)

Income Statement of Last Five Years

Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015

Sales 289.61 376.81 385.44 262.99 265.03 283.32

Expenses 264.57 341.19 347.09 237.17 237.75 259.47

Operating Profit 25.04 35.62 38.35 25.82 27.28 29.26

OPM 8.65 9.45 9.95 9.82 10.29 10.33

Other Income 1.28 1.51 1.71 1.86 1.91 1.9

Interest 14.10 22.93 22.64 19.66 19.99 20.87

Depreciation 4.34 6.77 8.40 4.99 5.41 5,41

Profit before tax 7.88 7.44 9.00 3.02 3.80 4.87

Tax 2.51 2.07 2.92 0.98 1.10 1.77

Net Profit 5.37 5.36 6.08 2.03 2.70 3.11

EPS (unadj) 4.70 4.63 5.16 1.62 2.20 2.51

Rationale

I believe, this is again coming into same cycle of 2012-2013 which was very high growth.

With huge opportunities in infrastructure in next 3 years like freight corridor, smart city, railway signalling and protection system and infrastructure projects, this can gain huge benefit

More over it has been under valued over a period of time . At current EPS of 2.51 , PE stands at 17.9X while other peers (V-Guard, Finolex) are trading at PE of 30 approximately

I believe, debt reduction and sales growth in next 2-3 years can bring back company to EPS of 5-7 approximately (very much conservative)

Opinions invited.

Disclosure : Holding less than 5% of portfolio