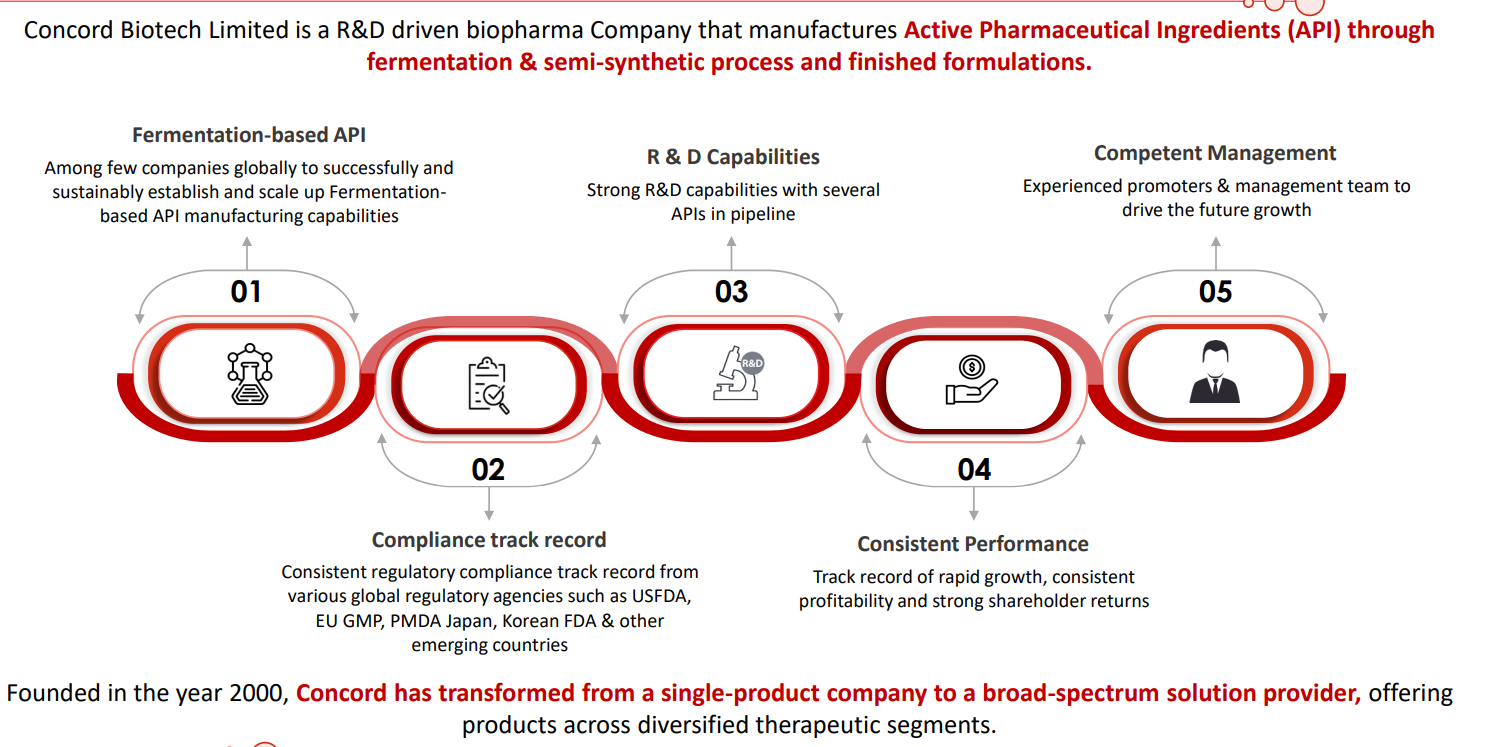

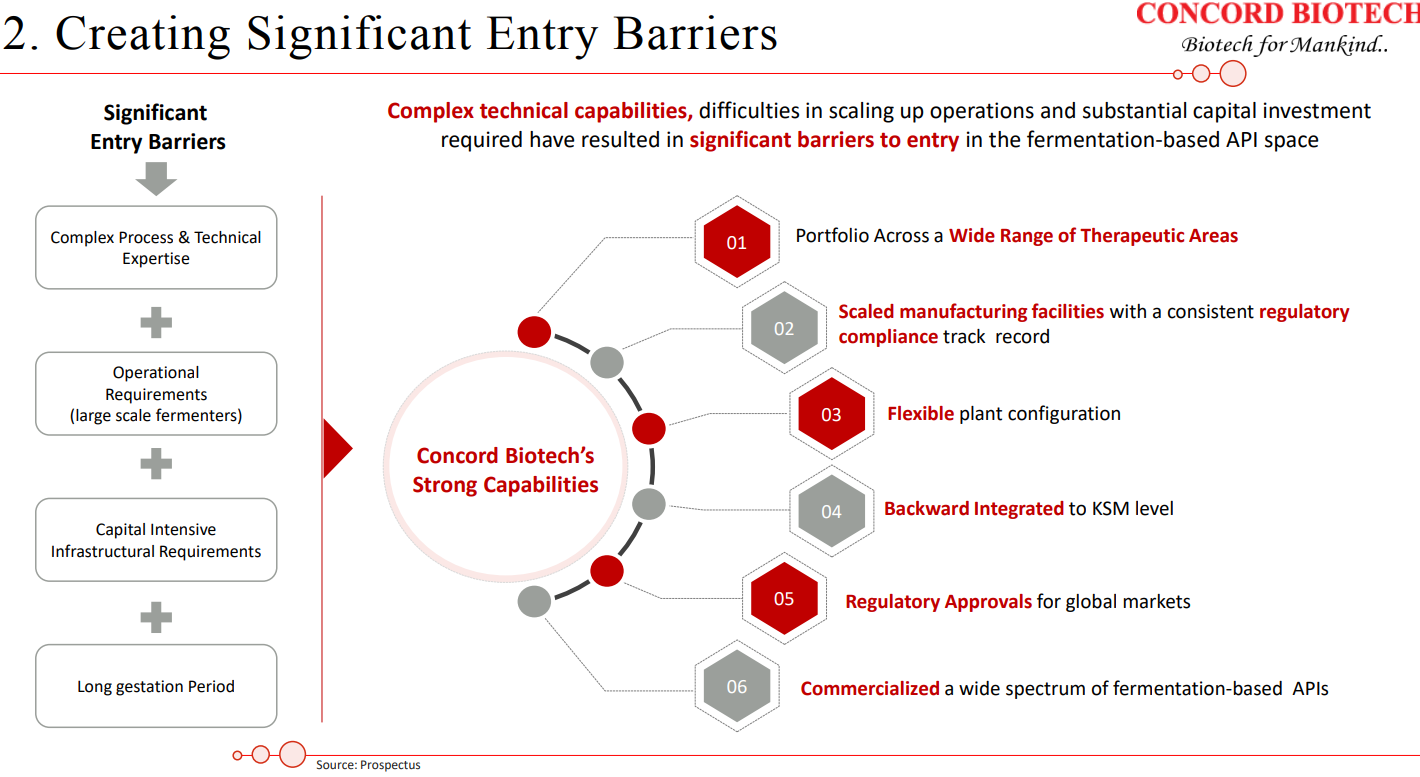

- **Concord has strong competitive advantages in the Fermentation API space. Also, the Fermentation space has high barriers to entry **

It is very rare for a company to earn a strong ROIC in this space. Historically, this business has been a graveyard for Indian companies. 3 decades back, India used to have many companies in the Fermentation API space. These companies eventually died because they could not match the scale and cost economics of Chinese players.

Concord has been operating in a niche and technically complex space and enjoys strong economics.

DRHP and the latest presentation are quite insightful

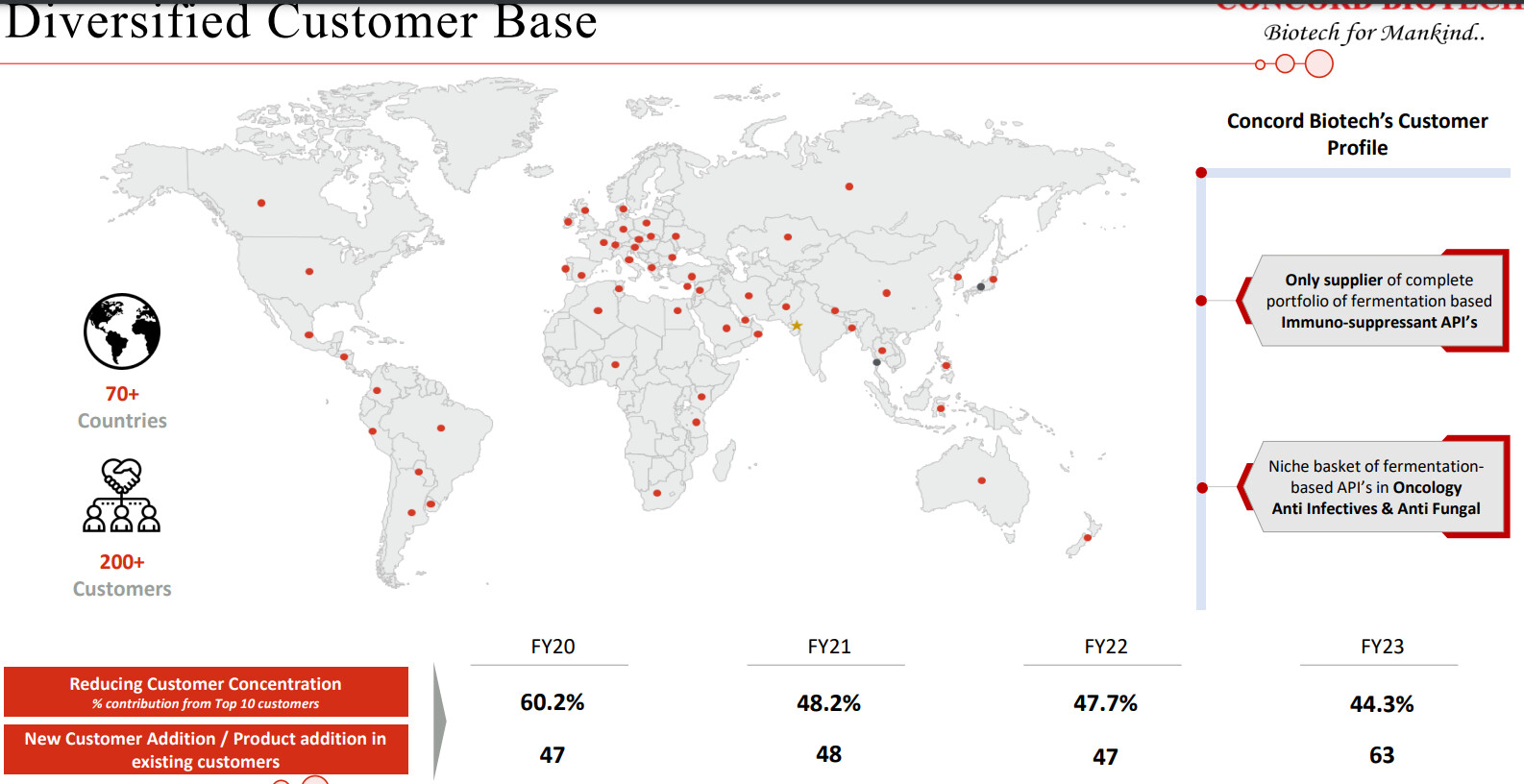

Concord has been able to crack customers in Japan, which is a big feather in their cap since entry barriers to the Japanese market are relatively higher owing to the fact that customers have high qualification criteria

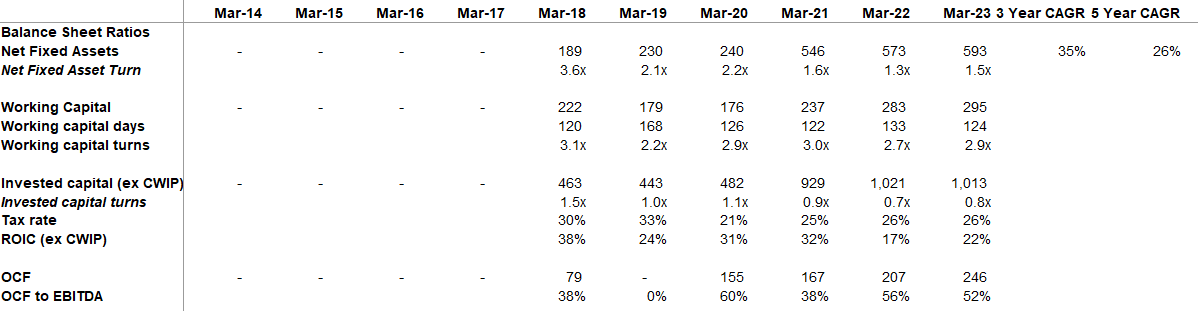

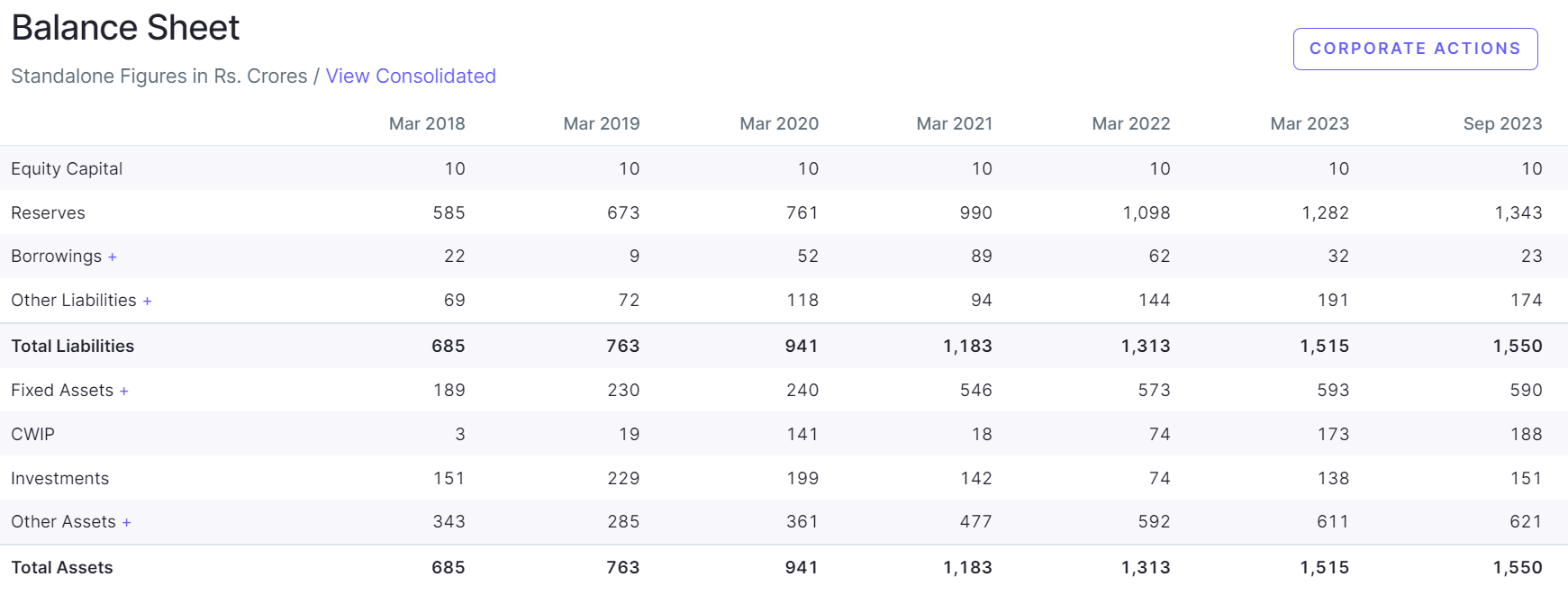

- Balance Sheet is pretty healthy

IPO was 100% OFS and all of the OFS was done to give an exit to PE Investor. So, Promoters still have motivation to create value.

KTAs from Earnings Call:

| Sep 2023 | |

|---|---|

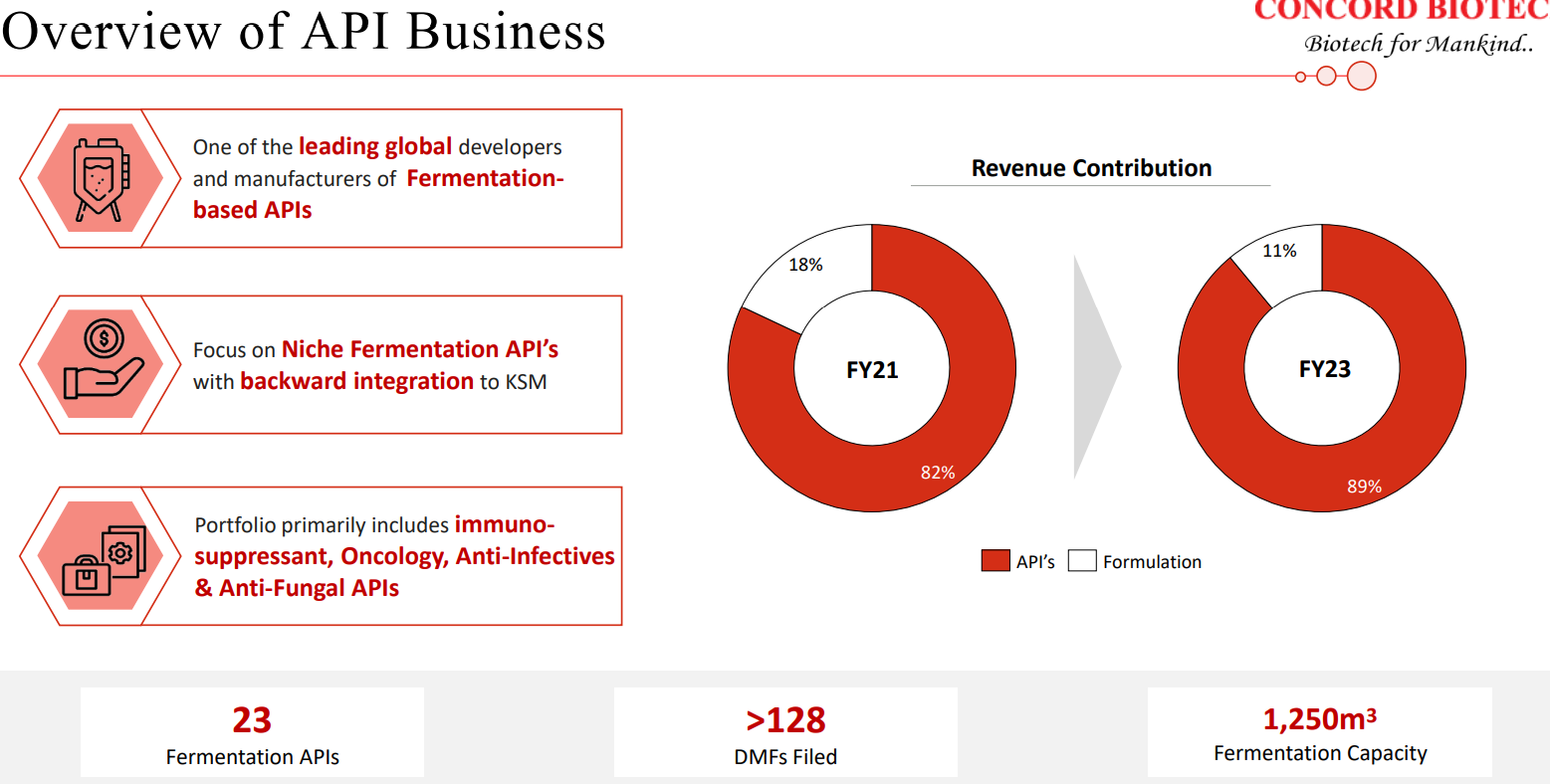

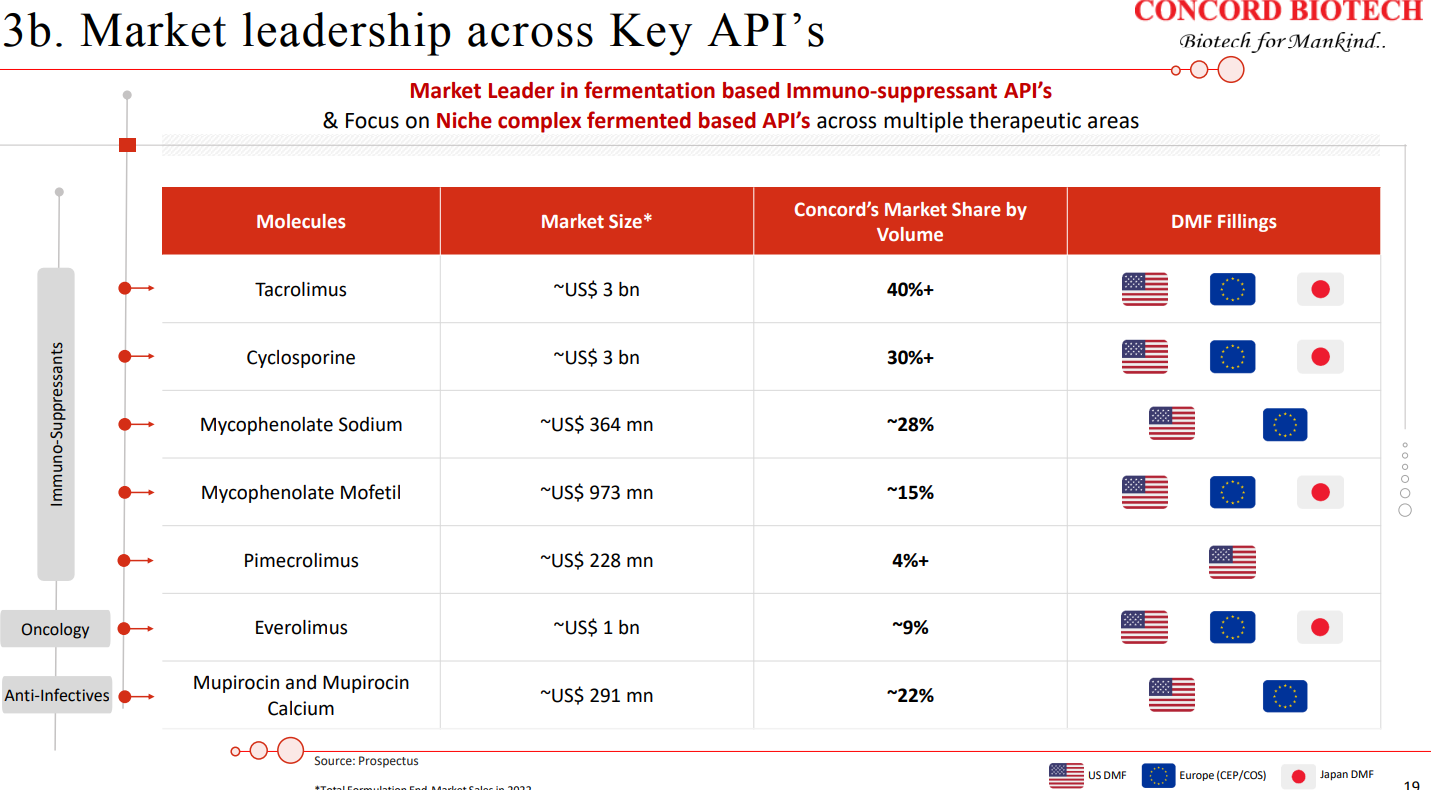

| The global API market can be broadly segmented into therapeutic areas such as anti-infective, oncology, immunosuppressants, and others. Of these immunosuppressants accounted for 7% of the market and is expected to grow by approximately 9.7% and oncology market which accounted for 19% is expected to grow at a CAGR of 19.7%. | |

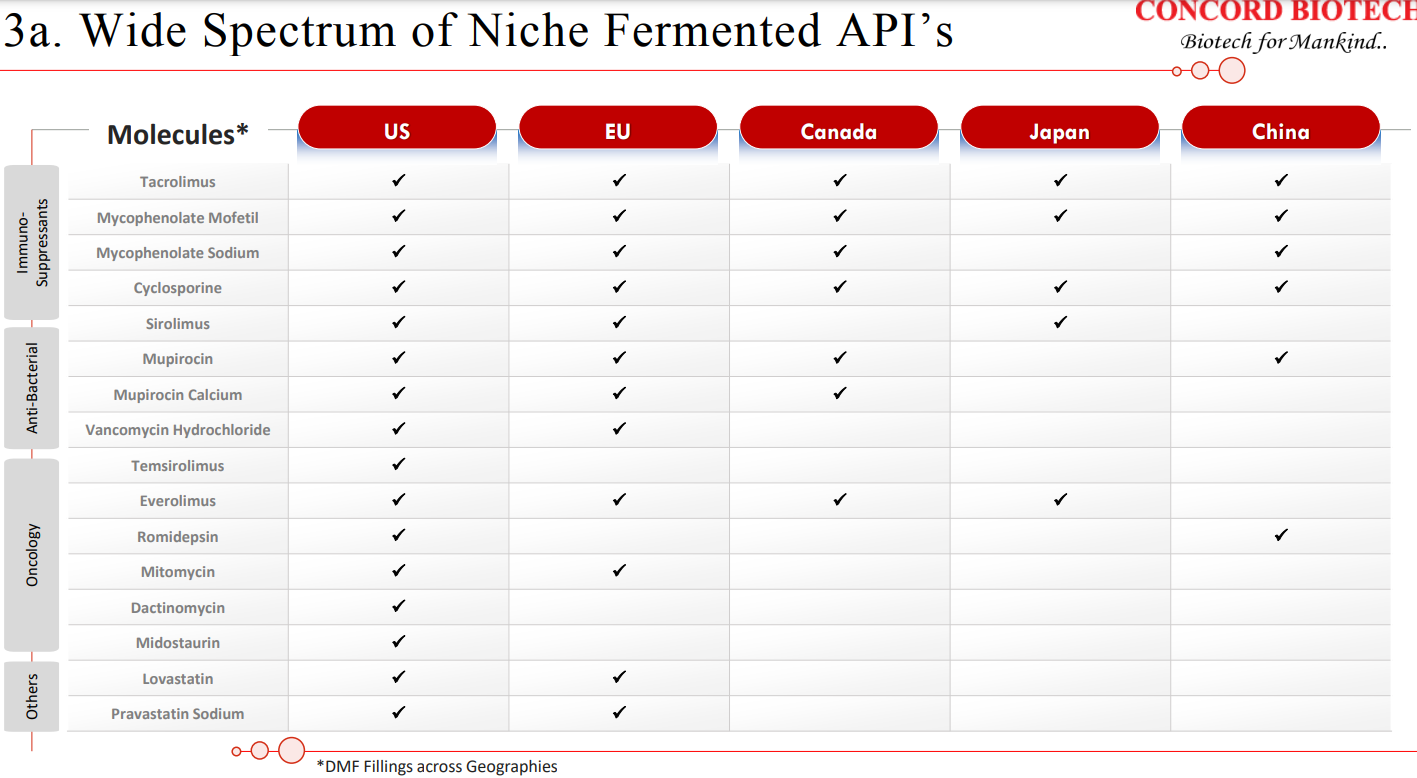

| At Concord, we are the market leaders for immunosuppressants and the only supplier in the world having complete portfolio of fermentation-based APIs for the immunosuppressants. Alongside, we have also developed our capabilities into niche fermentation-based APIs in oncology, anti-infectives, and antifungal APIs. | |

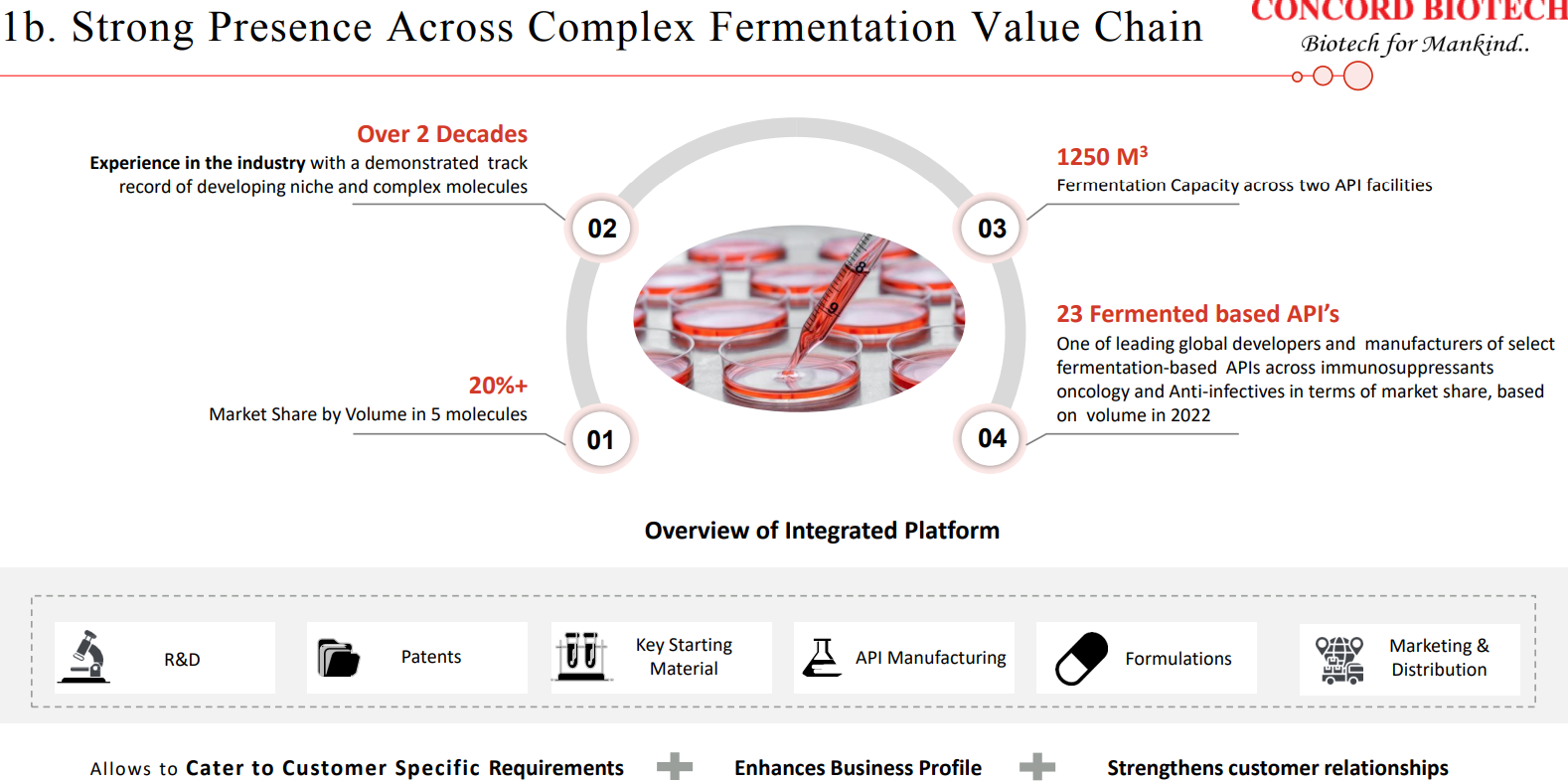

| Initially started with production of enzyme with just one manufacturing block, but with an experienced team of biotechnologists, especially in the field of fermentation. Over the years, company has made remarkable strides and currently operates approximately 41 manufacturing blocks across three manufacturing units, offering a wide range of products, spanning diverse therapeutic areas and segments. | |

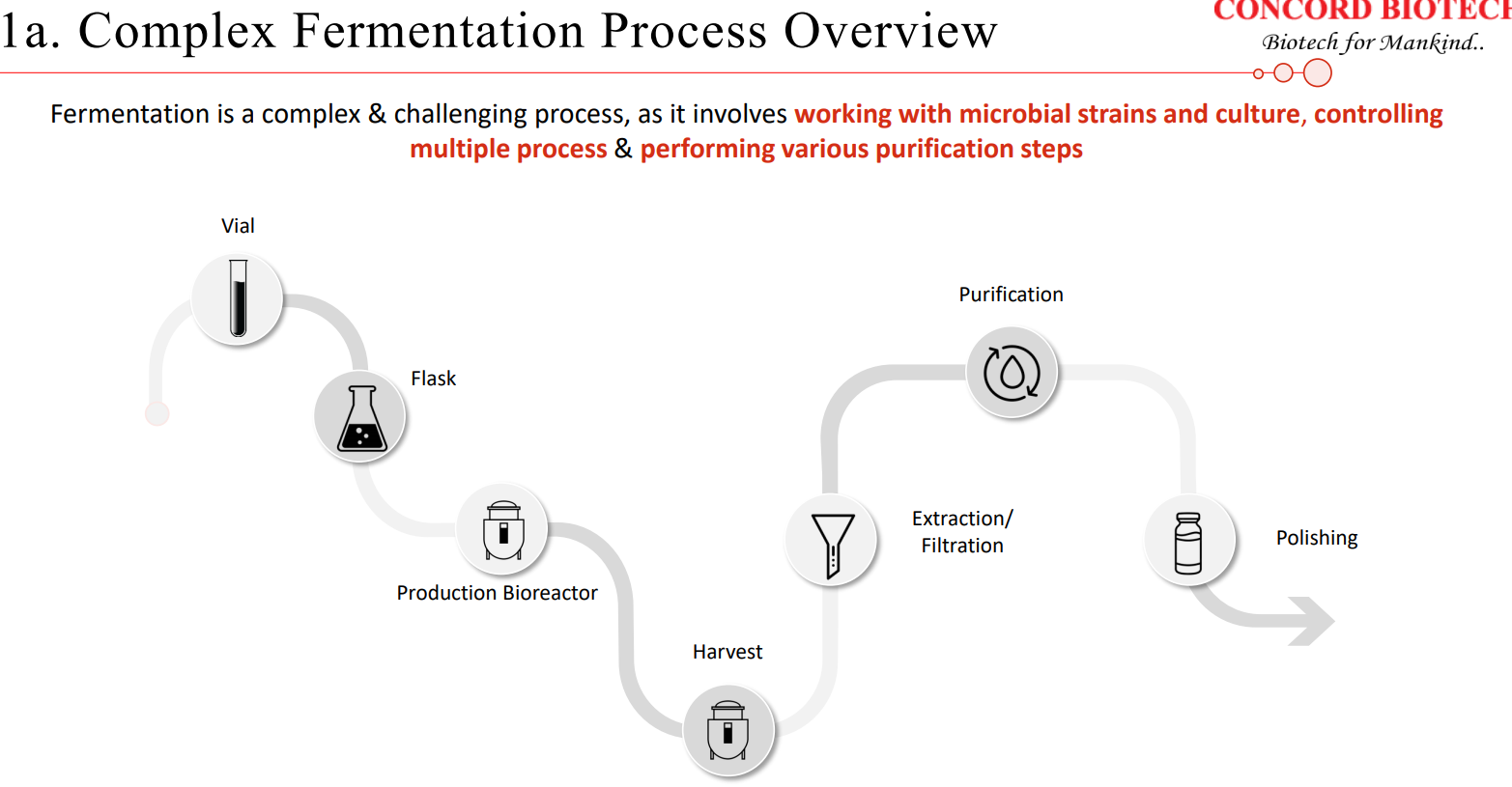

| Notably, Concord stands out on the global stage as one of the few companies that have effectively and sustainably established and expanded their capabilities in the fermentation-based API manufacturing. Furthermore, Concord proudly holds the distinction of being the only supplier of a complete production portfolio for fermentation-based immunosuppressants APIs. Fermentation as a core component of our manufacturing process presents unique challenges. It involves the intricate management of microbial strains, the precise control of multiple interconnected processes, and the execution of various purification steps. | |

| The slightest adjustment to this process can yield significant variations in the final output. As a result, this approach stands in stark contrast to chemical synthesis, requiring a highly specific, scientific, and quality-centric approach. As we expanded our market presence in the specialized fermentation-based API industry, we took a strategic step of entering into the formulation business back in 2016. Our Valthera facility was established with the purpose of producing forward integrated formulations for oral solid doses. Over time, we have successfully developed and are now manufacturing products and catering to both domestic and international markets. | |

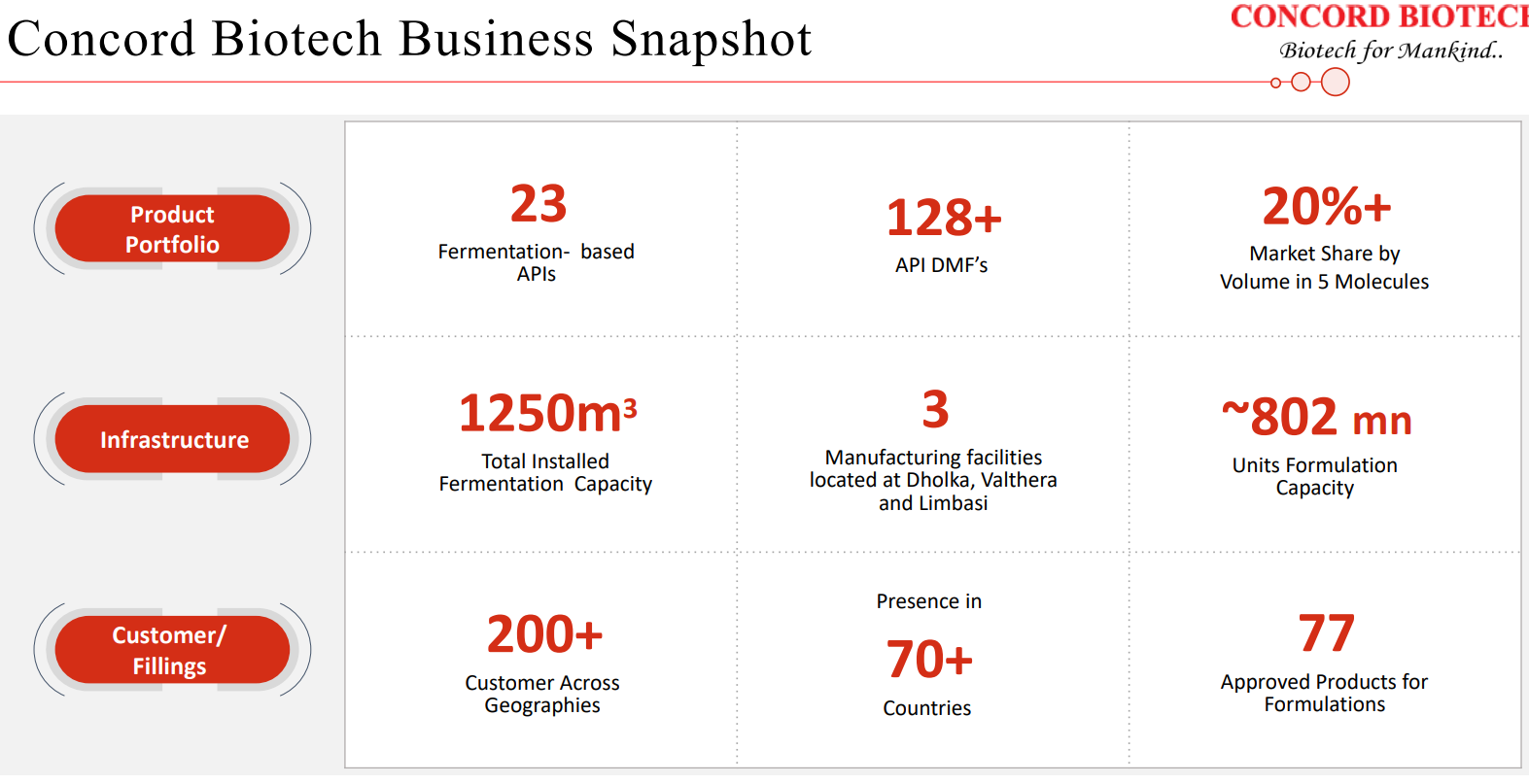

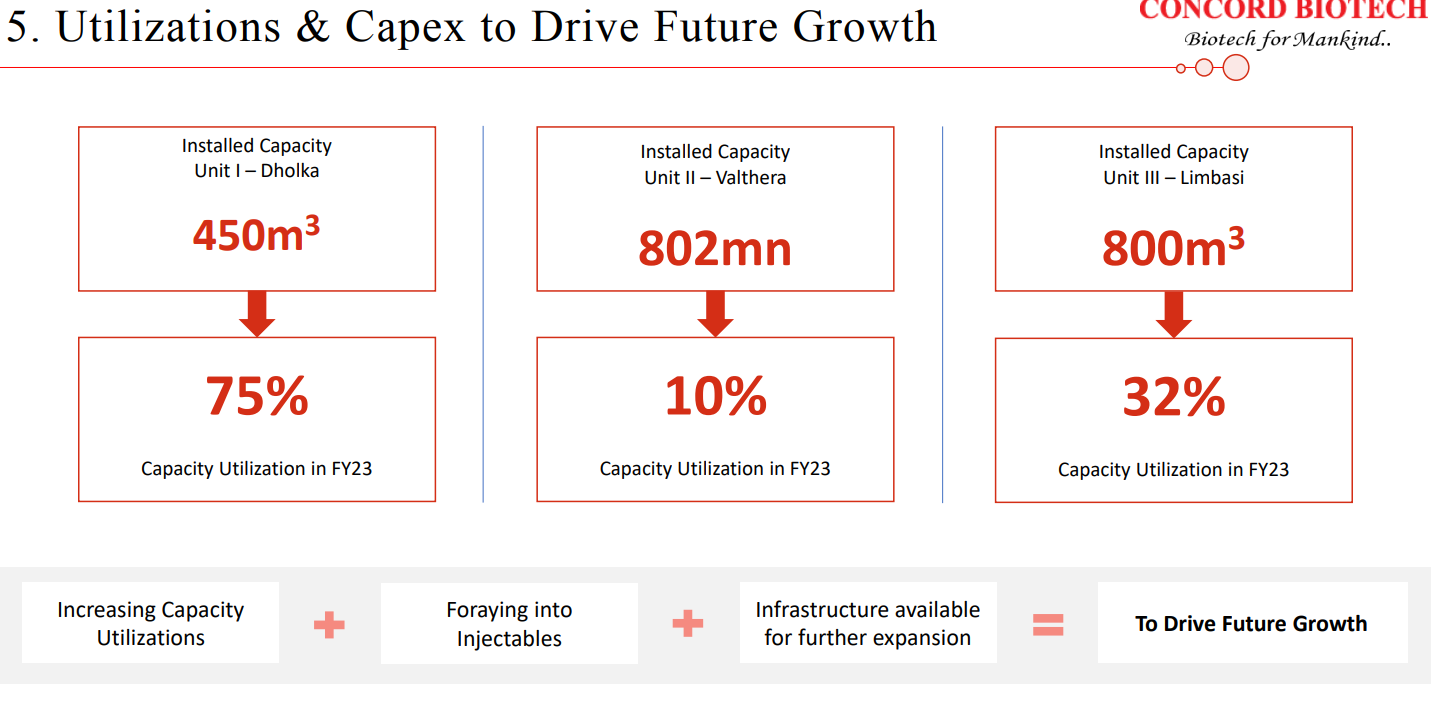

| At present, our Valthera facility boasts an impressive capacity of approximately 802 million units. Furthermore, as part of our commitment to strengthening our position in the formulation business, we are in the process of establishing an injectable facility. We anticipate that commercial production at this new facility will commence by the first quarter of the next financial year. Over the years, Concord has diligently cultivated its capabilities and an extensive range of products, positioning itself at the forefront of the competition. We have steadily expanded our customer base across global markets. | |

| This strategic approach has solidified our reputation and enabled us to make deeper inroads by attracting additional customers and further penetrating our existing client space. The production of fermentation-based API is inherently complex, making us one of the very few global suppliers capable of manufacturing a comprehensive range of products under one roof. In recent times, the industry has witnessed significant consolidation of manufacturing activities. Several companies have encountered challenges related to the growth on the back of skill shortages, lack of scalability, and a limited product portfolio. This has presented us with ample opportunities to expand our presence in various markets and geographical regions, ultimately contributing to the growth of our revenues and market shares. | |

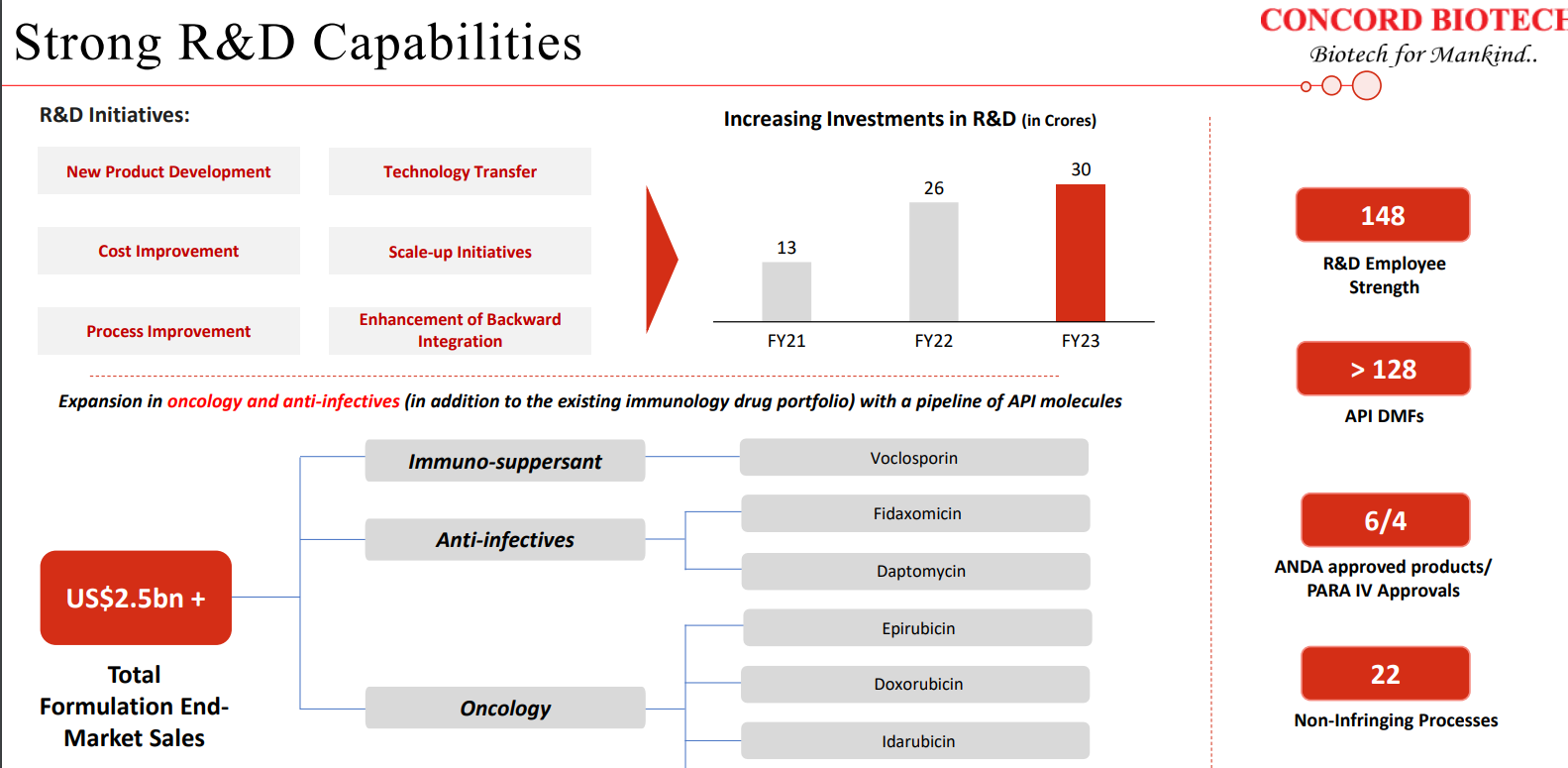

| Our strategic focus is on further expanding our API portfolio across therapeutic areas, especially in oncology, where we currently have 6 APIs for global markets, and anti-infectives and antifungal, where we currently have 7 products. Also, we continue to invest in R&D and have a strong pipeline of products under development across therapeutic areas of Immunosuppressant, oncology, and anti-infectives, which have an addressable market size of USD 2.5 billion at the formulation level. | |

| And this will allow us to cater to the regulated markets. I’m happy to inform you that USFDA authorities inspected our Limbasi facility from 26 to 30th of June of 2023. And the inspection was successfully concluded with zero 483 observations. We now have an EIR report for the same. So with this, customers have now initiated qualification of the Limbasi facility. I would also like to highlight that we have only one manufacturing standard across our facilities, which is followed irrespective of the end markets, be it regulated or semi-regulated markets. | |

| Further, we are in the process of enhancing our capabilities in formulation manufacturing through our injectable facility. Speaking of R&D, in research and development we have set up two DSR approved R&D facilities comprising of 148 members, a significant number of whom had full doctoral qualifications. Our R&D team has showcased its proficiency in moving products, even complex ones, from the R&D stage to full commercialization. | |

| Our product selection assessment encompasses a comprehensive evaluation of factors such as the market potential, competitive dynamics, technical feasibility, and the intellectual property landscape for each prospective product. As of now, we have successfully developed and brought to market 23 fermentation-based APIs with the valuable support of our dedicated R&D team. | |

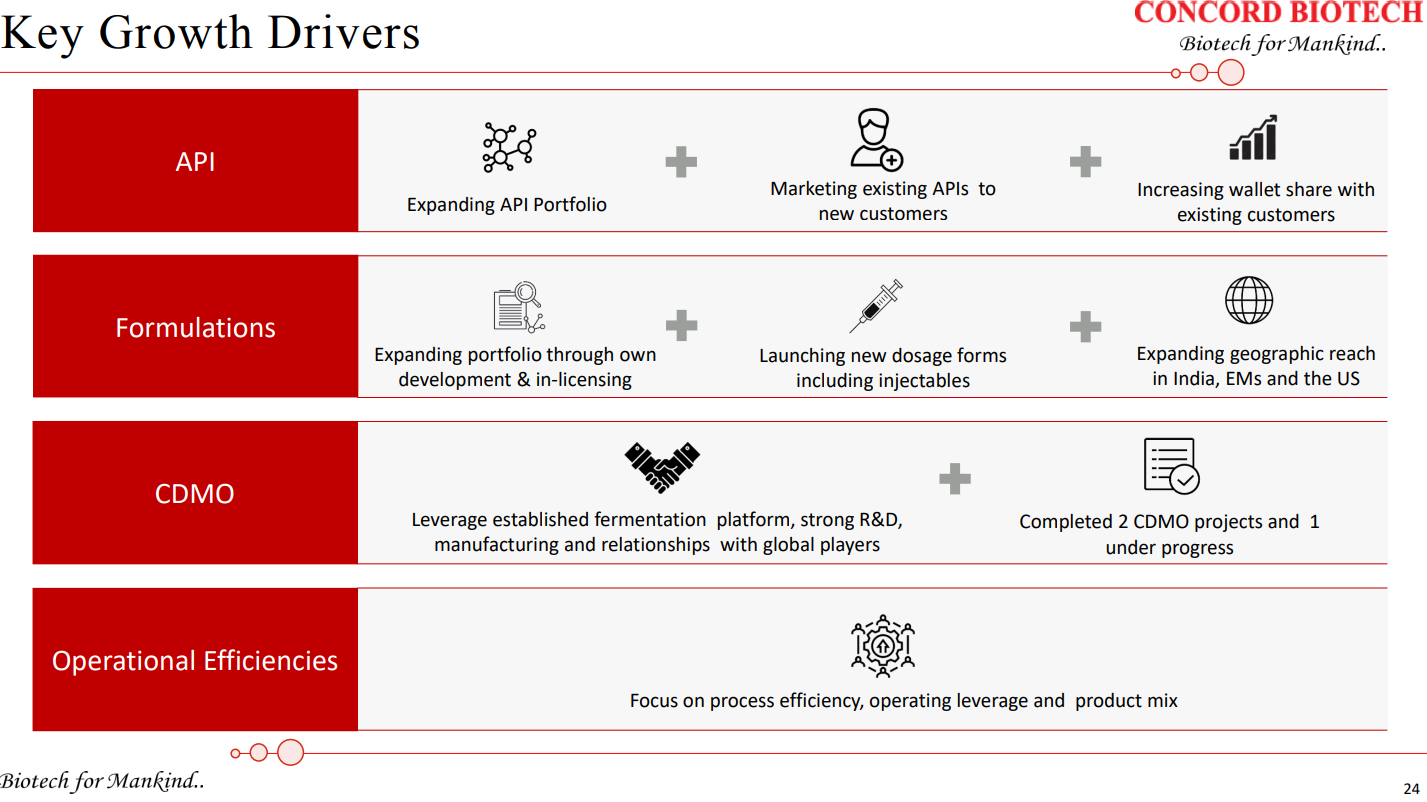

| With high quality niche products, we’ve been able to successfully add new customers across therapies and geographies over the years. We will continue with our endeavour of adding new customers and increasing in the share of wallet of our existing customers as well. To take you through our strategies going forward, our primary strategy is to continue to increase our market share and develop our portfolio of complex and niche products with high growth potential. API will continue to be the core focus of the business and we will continue to increase our wallet share among existing customers by selling them existing and new products across therapies. | |

| Also, our investments into new manufacturing capacity has enabled capabilities to grow our wallet share from existing customers. Secondly, adding new customers across different geographies with established product portfolio and with the commercialization of new products. Thirdly, increase our presence in existing formulations and add new formulations by adding geographical reach, launching new dosages, and expanding the product portfolio. | |

| And the fourth lever being the growth in the CDMO business. So, with the capacity expansion at our Limbasi facility, the China plus One strategy and given our expertise in the fermentation area, we see this as a growth opportunity for future growth in the company. And the last growth lever for us being the increased utilization of existing and new facilities by adding more customers, and products to be marketed and sold across geographies. | |

| So we have close to around eight to 10 molecules which are there in the pipeline across different segments such as the Immunosuppressants, Oncology, and anti-infectives and one would appreciate that it takes close to around six to seven years to kind of develop the molecule in the fermentation space. And there are products which are at different life cycles within the development, R&D development stage. | |

| But typically, I say that one can expect around one to two molecules that would become commercialized based on our historical trend is what I would point out. But it’ll be difficult to mention which specific product would become commercial because it will all depend upon the market dynamics about the state at which we are with respect to those molecules. | |

| So while, you know, we have been inspected by regulatory authorities, but still, this is a risk that we carry. However, we have a very strong theme of quality, QA, and QC, which ensures that quality standards are maintained on an ongoing basis. With respect to any other risk, I won’t call it a risk, but of course, any changes in the macroeconomic conditions could impact companies in the pharmaceutical space, whether it is through changes in certain raw materials or changes to certain power and fuel costs, which could affect us as it would affect any other pharmaceutical company. | |

| So as we have discussed in the past that our raw materials are usually the basic raw materials which are either agro-based or are the solvents which are typically used in the downstream recovery. And we have close to 150 to 200 raw materials that are being used for different range of products that we manufacture. So there could be an impact of seasonality on the agro-based compounds or as I mentioned due to global changes, which could affect the solvents. But then again, it may affect maybe some of the raw materials because of which there could be an impact, but it could be very, very minuscule because of it being impacting maybe one or two raw materials out of the 150 to 200 raw materials that we use. So the gross margins work in a very, very narrow band, if I would put it. And it is more about the expertise that is needed for the fermentation manufacturing, which makes the differentiation there. | |

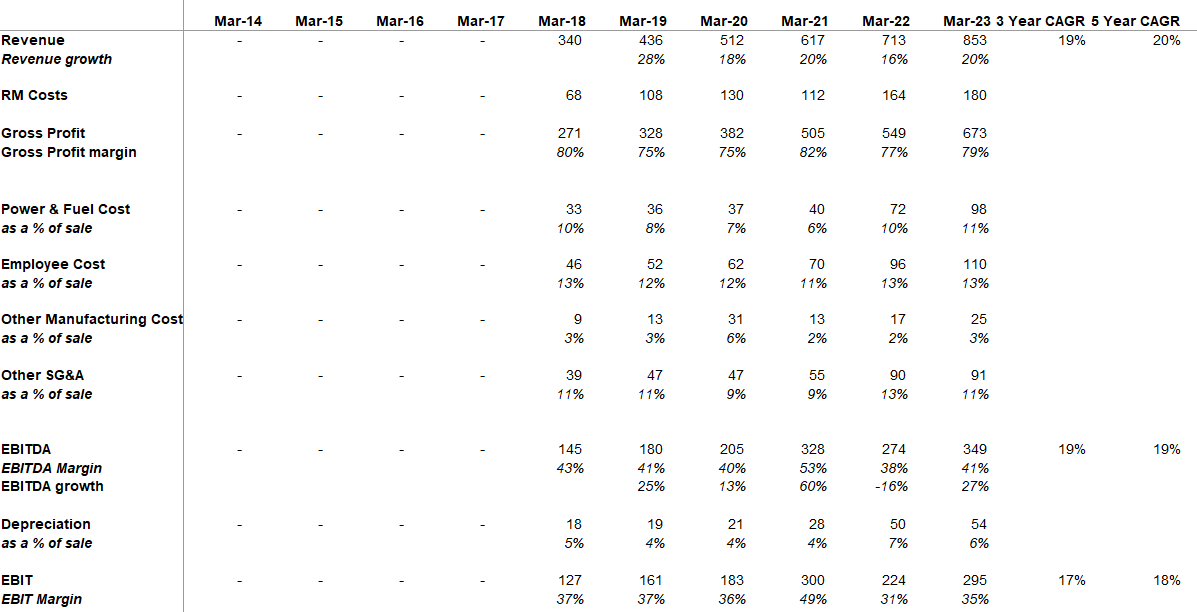

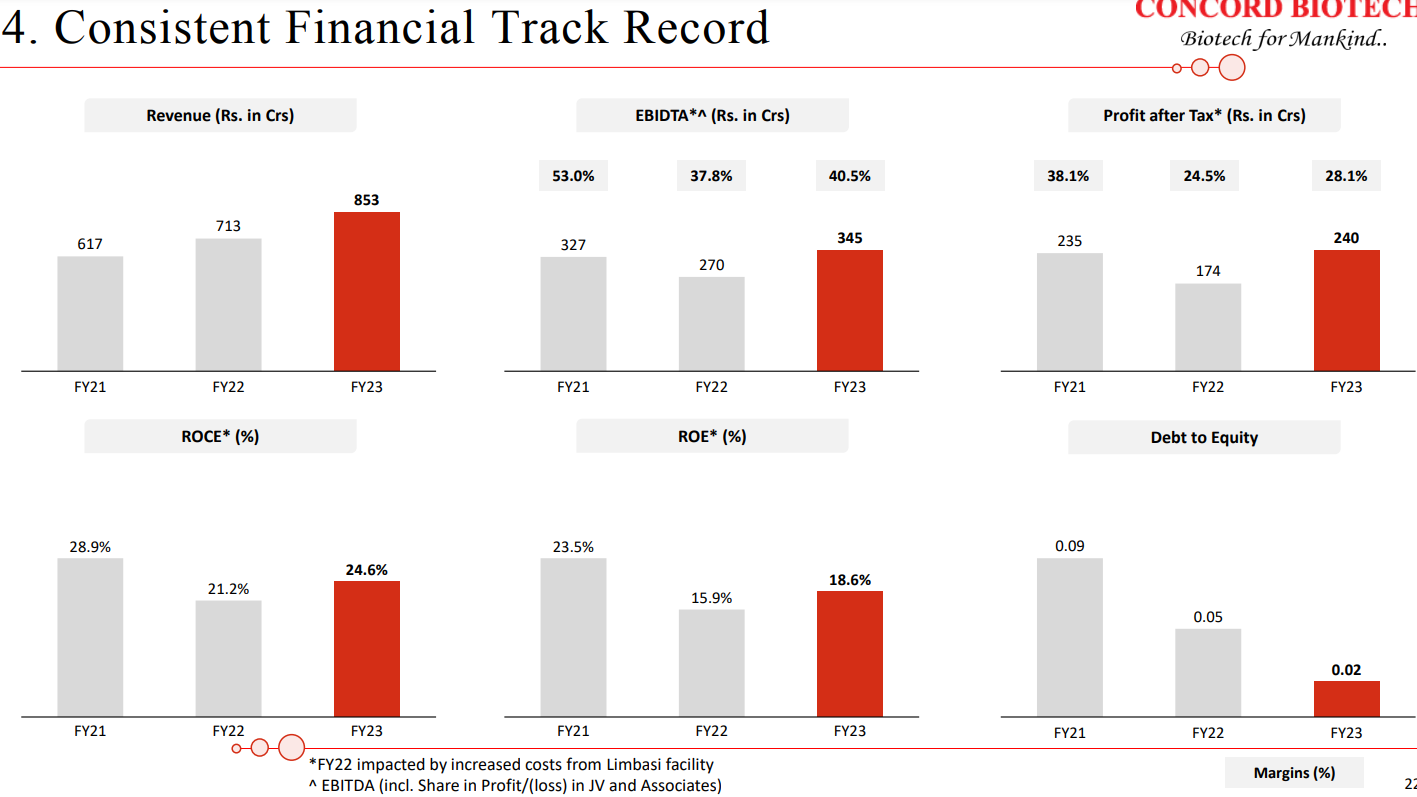

| Basically, historically, we have been growing at a CAGR of around 18% in the past for the last couple of years. In the last two years or three years, we have also built-up significant capacities with respect to the API and the formulations. And we expect to increase the capacity utilization and our growth may be better than what we have been doing in the past. So historically, we have been growing at a CAGR of around 18%, so going forward we may improve the growth per percentage. | |

| In fact, in Limbasi, we have invested around INR 400 crores of money in the capex. And with the 450-meter cube of the capacity in unit one, we are able to generate revenue of around INR 600 crores. So with an 800-meter cube of the capacity, you can begin to basically take it nearly to the level of around INR 1,500 crores, INR 1,600 crores of revenue from Limbasi facilities. | |

| Around 75% to 80% will be the right capacity utilization. | |

| So, the injectable project is running on track as we had envisaged, and we expect it to be ready by the end of this year and have commercial production by the first quarter of next year. Given that, the idea would be, the plan is to kind of first take it to the domestic market because the export market is more of a medium term to a long-term strategy for us because, by next year, we take the validation batches, put it on stability, do the dozier filing and get the approval. This is typically close to around 12 months to 18 months of time period. However, we will be going with the same integrated approach, where we have quite a few molecules, where we are the manufacturers of the API, as well as we’ll be going for the forward integration to the injectables. So you do not see many companies having that kind of fully integrated approach in some of these niche anti-infectives also, which are through fermentation. But in terms of timelines, I would say that initially we would start with the domestic supplies and then going forward, they would be, being targeted towards the export market. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| So CDMO is definitely an area, which is a focus to us and we now have the capacities in place, we are also building on our regulatory approvals and we have a longstanding relationship with our customers as well. So we are reaching out to customers and working with them to kind of build on the CDMO opportunity. But again, opportunities like these do take their time because customers wanting to evaluate and shift their complete manufacturing to a new site would typically be a time-consuming activity. | |

| As long as it matches these criteria, which we have internally defined, we are not therapeutic diagnostic. So we would be open to look at other molecules across different therapeutic segments as well. It just happens to be that some of the molecules that we are currently under development falls within these three therapeutic segments, which is the immuno, onco, and anti-infectors, anti-fungal. But we are not therapeutic diagnosed to these. | |

| No, so I, as we pointed out that we have growth levers in place for both the API and the formulations. At the API, the new Limbasi facility which will start ramping up and at the formulation level we have ramping up of the oral solid dosage facility and the build-up of the injectable plant. So while the base will continue to grow, we expect the revenue split between the two to be somewhere around 80%- 20% as we have had in the past. So do not expect any meaningful change in the allocation between the two. | |

| As far as the percentage of capacity utilization is been 32% in unit 3 as of 31st of March 2023 and in formulation, it is 10% and in Dholka, it is 75% | |

| So definitely, this will boost our sales to the US as well. But again, this Limbasi facility is for global markets because as mentioned in the past that we are working on close to around 70%, 75% capacity utilization at unit one. So now that we have regulatory approvals in place, this new facility is going to be catering not only to the regulated markets, but for global markets including India and the rest of the world. And newer products that would also come in would also be commercialized at this new site. So it will definitely boost our US sales, but it would also be used to cater to global markets as well. | |

| So I would say that the products which are made through chemistry cannot be made through fermentation and products which are made through fermentation cannot be made through chemistry. So, they are two very different areas of manufacturing. However, we do see moreand-more interest coming within the fermentation space because it creates significant barriers to entry because there are not many global players in this space. So there is a good growth prospect for the fermentation but it cannot be interchanged with the chemistry APIs. | |

| So, you know, Concord holds the leadership position on several of the APIs that we manufacture. The reasons of course are that we have economies of scale, we have global regulatory approvals, strong technical expertise, and offering a basket of products. So we are the only company in the world which actually manufactures the entire range of fermentation based Immunosuppressants. So when you have these kinds of capabilities and strengths, customers look at working with companies such as ours. And that is the reason why we’ve been gaining market share year-onyear basis. And when we talk about that kind of niche, highly complex products, you typically do not see much competition coming from China. As a matter of fact, that we are commercially, we have now got approvals in China to sell our products, our APIs, which shows that, and customers are also showing interest in terms of partnering with us for the API, which kind of shows the kind of advantages and the kind of strength that we have on the API, even with respect to some of the Chinese players. And when we talk about the European counterparts, European competition, people now are talking more about the China Plus One and Europe Plus One strategy because of what is happening at the global footprint with the Russia-Ukraine war, the power costs and other things and the salaries have gone up quite significantly in Europe. And they are looking at alternate sources which are more reliable and can consistently provide them with these kinds of products. So, I think we see a lot of companies shutting down in Europe also and other parts of the world. So, we see a lot of consolidation happening in the fermentation API space. | |

| So basically around 17% of the revenue in the export, or in the total revenue comes from the US market and the balance comes from the rest of the world. | |

| In terms of cannibalization, we are not looking at disturbing the market and we are looking at value creation and opportunities within the formulation space. And that is why while we are backwardly integrated, we would look at opportunities where we can be there in the market but at the same time maintain healthy margins for us rather than going all in and destroying the value for ourselves as well as for our customers. | |

| Annual operational cost for formulation facility is ~35cr. | |

| Most of the capex has already been done as far as the growth capex was concerned. Now it’s only the operational capex which will be required to be done in the future. It will be in the range of around INR 15 crores to INR 20 crores of per annum. Yes, very little amount is required to be spent to complete the project. Majority of the amount has been spent. And yes. | |

| So you know, the prices are more or less quite similar to what you would have across the globe because, while we see limited competition on our molecules, we still are not in a monopolistic market. So when formulation companies are looking at potential suppliers. They kind of evaluate new suppliers based on which is going to supply, and give the best price. So we also have many Indian companies which are targeting the US market and they have a good amount of clarity on what the prices are there in the global markets, including in India being offered by some other manufacturers. So I would say that there is not much of a difference between what the price you offer to Indian versus that to the US. |