Hi,

This is my first attempt on VP. I have started my investing journey two years back when market is just started to correcting. I am thinking of making a portfolio of the concentrated bets of strong companies for monthly SIP / Lump sum (whenever market corrects). Rational behind selecting these companies are No brainer /strong management/ low to Nil Debt /sector leader / long runway /proven business models. The following are the selected list of companies for long term investment mostly following the VP blogs only (thanks for the immense knowledge hub).

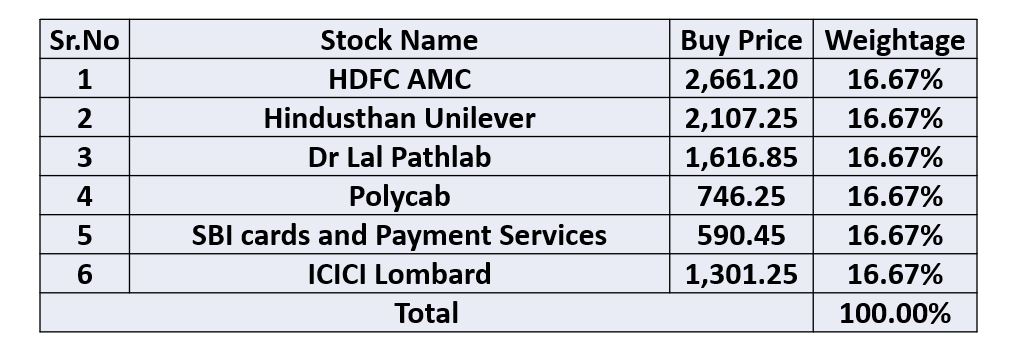

SBI cards and Payment services : low penetration / only listed player / long runway/ top among the sector

ICICI Lombard : Unique business model / very few listed players / strong brand /long run way

This is the historical performance of the portfolio if one has started in early 19 :

Comments and suggestions from the VP members are kindly requested.

Few Suggestions from my side for creating portfolio for long term.

Although you have mentioned concentrated portfolio, portfolio of 6 stocks is very concentrated. Significant impact on even 1 stock can be detrimental for overall portfolio return. Ideal diversification includes from 15-25 stocks. So, you may think of increasing the diversification.

Out of 6, 3 stocks belong to financial sector (HDFC AMC, SBI cards, ICICI Lombard). 50% concentration to just 1 sector can be very risky. Impact on economy financial sectors for a significant time can have adverse effects on portfolio returns. Remember, things go wrong all the time and our investments should have necessary risk-protection

I am not commenting on stock selection, valuations etc.

Thank You for kind words. I totally agree with your Financial Part suggestion. I am thinking to add few more stocks including nifty 50 etf / motilal oswal overseas fund (max 4 more) and re balance the weight based on market cap / sector allocation. Any suggestion for sectors to choose, how to balance the portfolio or any stocks to start dig into?

My suggestion will be to invest in only those sectors which one understand. Diversification should not be done for the sake of it.

You can take NIFTY 50 or NIFTY 50 + NIFTY next 50 for study and check sector allocations.

Sector weightage keeps changing, however, major sectors are Financials, FMCG, Metals, Auto, Pharma, Telecom etc. You can choose sector and stocks as per your understanding of the sectors/ companies. Pick with the sector which you understand.

For stock selection picks, pick a few top names in each sector and study them. Check opportunity size, valuations, management quality and past track records. And what seperates winner in the sector from others. Once you have fair understanding, you can dive deep into the sector and so on

If one doesn’t has much experience in some of the sectors, opting for MFs/ETFs are good option to take advanatge and meanwhile those time can be used to increase knowledge of that particular sector/ stocks.

NIFTY ETFs + Overseas Funds provide good diversification, so that’s a good approach. However, ETFs and MFs are already diversified, so there shouldn’t be many of these in portfolio. 3-5 can be considered ideal.

Concentrated portfolio is really a brave step to go about investments and so you need to be extra sure about your picks here, as already someone pointed out that return on one stock can affect your portfolio in a huge positive or negative manner. So every company you choose should have either proved themselves as a market leader or company should be addressing something which others are not i.e. differentiator. You can’t place commodity companies in a concentrated portfolio as they tend to become cyclical.

All the portfolio companies look good.

My only concern is …

—buying SBI Cards and Payment Services at rich valuations only reason being… “only listed player” ??

Do you see anything special in SBI Cards? It would be very interesting to know.

– Also if you can explain your rationale on polycab India?

Thanks for the suggestion and brain stimulating questions. I am rethinking /studying about the polycab and sbi cards . However from the reports about SBI cards there are few interesting points that i would like to share : 1) Increasing consumer demand, rapid urbanization, the growth of e-commerce platforms, and Increasing acceptance of digital payments (lockdown may somehow enforced on this)

2) Future Growth of Credit card industry

3) Top 4 players accounts two third of credit card spends

4) Average spend per transaction Growth rate is increasing than pears

5) Increased acceptance of credit cards by millennials (what i personally observed)

Yes there are valuation risks, economical downturn risk which may result in cyclic behavior of the business, regulatory risk.

Can you suggest some other good names to start look into if possible?

Most of the Stocks are newly listed so its difficult to find Past performance and extrapolate to the future. But i assume most of the companies are sector leader so overall portfolio return should be in the range 10-15%. If market conditions are good then historically returns have reached upto 40 % which is above the expectations .

Investments are of many flavours, and each has its own level of Risk. A successful investor is the one who takes on a risk, which is commensurate to his return expectation.

In your case, if you want 10 to 15% type returns, then you can get that from investing in ETFs. I mean, if you invested in Nifty ETF, from these levels you are highly likely to get 10 to 15% in the next three years. Why bother with individual stocks and that too newly listed ones in a concentrated PF. Even the best of market participants would call this risky.

In short, you should opt for ETFs; dont take on newly listed high PE stocks which are best reserved for industry experts who have these stocks well within their circle of competence.

Okay. I got you point. I dont like portfolio of 20-25 stock ( too big to handle and not able to monitor frequently so wanted to concentrate on sector leaders with developing personal interest ).But these are good companies which can accommodate in broad portfolio of 10-12 stocks.

I am not really sure whether these are good stocks.

Good stocks, in which I can put my time and money are the ones that make my ends meet, which means they should be good businesses, ethically managed and selling at “good” price. Since, all of these stocks do not fulfill the second point, I won’t be investing in them.

Not sure how long you want to hold on to these stocks. Just my remark on HDFC AMC: Most of their fees come from equity funds. going forward there will be switch towards ETF’s or Index funds which is not good news for HDFC AMC. More over quite a lot of HDFC’s funds are struggling to beat index.

Can you throw some light on some of my doubts regarding HDFC AMC if Poossible? 1)How much time it will take for changing mindset of people from active investing to passive investing ?

2)Will people not divert same money from active to passive in same AMC?

3) Whether Looking at brand Name people won’t buy ETF’s of HDFC AMC ?

4) If ETF are the only futures then there will be less fund managers, less salary to them , less infrastructure requirement ,whether it will re-balance somehow profit margin (not that much but it will definitely affect bottom line re-balncing )

It is already going on as you can see many AMC’s trying to launch variety of index funds. Yes, people would buy HDFC AMC’s index funds as well but most of their revenues are due to actively managed funds which would be impacted. Let’s look at positive side, overall population which invests in MF’s in India is very low which might grow significantly in the coming years but most of them might go towards index funds. Best index funds are those where tracking errors and expense ratio is low if HDFC AMC can maintain this then they may get lion share. but still an expense of ~1-1.5% of active managed funds cannot be replaced by ~ 0.15% of index funds. Remember HDFC AMC’s is trading at premium valuations so expectation is they continue to grow at similar levels else PE will be re rated.

Thanks for the insight, it is really helping in my thought process (Its like Whether to Choose AMC Business or its cost Effective Product for the same weight age of the portfolio). Actually my self only thinking while last few months (only sensex is moving up and most of the rally was few large cap driven based only. So why to give 1-2% extra for the fund manager if i get same returns in ETF).

Counter point to Active v/s Passive funds argument from Indian perspective is rise of hybrid equity/balanced funds. While ETFs can give higher returns as well as lower management costs, many middle aged people who want to earn more than FDs without taking full fledged risk of equity opt for balanced funds. As you can see from HDFC AMC’s portfolio, they have significant amount of AUM portfolio under these plans. People who normally invest in these plans are the ones who are investing in equities for first time and on the advice of Mutual fund agents. I think rise of Indian middle class directly co-relates with these funds as people from lower middle class who are transitioning to middle class who are investing for the first time prefer these schemes to ETFs even though they don’t perform as well as ETFs.

I don’t know how much balanced funds can compensate for the loss due to actively managed equity funds. HDFC’s balanced fund is performing terribly and couldn’t beat benchmark for last 3 years (Or may be 5 years as well). I have invested in this fund and i wouldn’t invest again if i have to start over again. In this corona induced downturn it fell more than some of the multi cap funds. Moreover when i started my investment journey i really didn’t knew what an 1% of extra returns can do to my portfolio in the long run. now that i know, I am not willing to invest in these funds any more. As more and more people get financially literate these not so useful (They neither give good returns nor prevents any downside risk) kichidi funds would be out of favor.

Hey, i like some of the companies that you have , HDFC AMC, ICICI Lombard, Dr Lal. Will recommend NESTLE or ITC instead of HUL.

I dont like the concentration on the financial sector. Thats too much of concentration on one sector. HDFC AMC, SBI CARDS, ICICI LOMBARD - 16.67 % X 3 thats a risk.

You can try the coffee can portfolio approach

Clean account books, market leaders.

Companies offering essential services / products.

High entry barriers, as high as himalayas.

Business that reinvest in the business using cash flows.

Think of the below portfolio 1:

3M india, CRISIL, HDFC Bank, ITC, Johnson Hitachi Controls, Nestle, P & G Hygeine, Pidelite, United Spirits.

Considering the current situation considering Portfolio 2;

HDFC Bank, Kothak Bank, Bajaj Finance, P & G Hygeine, United Spirits, Kajaria, Coal India, Oberoi Reality, ITC, VST industries.

All this stocks has its own might, just do your own research. Always but market leaders when the price is apt. Keep only 10 stocks, focused concentrated portfolio.