Thanks For detailed thread. Since I am not tech background I have not much idea about how this industry works. I looked the site and have followed tac security page on twitter where they mention about how can they save from various threats on daily basis. I might not good person to comment on the product since I have no idea.

On shareholding kedia family have 20% stake but they invested pennies per their appetite.

I totally agree clients are already big and revenue is small. Might be very low ticket product. I saw their site and found they have 2 product for small business one was $900 and another one was $1800.

I think they are planning to tapped small business with this product. I think margin should be very high here since once product is ready. Every new client will almost flow to bottomline

I too have doubt that they have not much achieved with what client they said but saying that the company is just 6-7 year old and founder is immature in business. But I think still at this small tenure he achieved many thing as per the various articles. He has honoured by Punjab govt. Some pics with kamla Harris and IT Minister of Karnataka. In such age if he has achieved and if maturity comes with some good finance person they can be so big since cybersecurity will have huge TAM and if that will be there for decades atleast.

On certificate they mention that they are first company to achieve this certificate.

Disc: Am not invested and not intent to invest in TAC foreseeable future. However I am looking for small Tech companies for investment purposes, hence taken TAC overview.

As per AR, they have 63 employees, if you deduct director remuneration it comes to 3.11 cr for 61 employees, which is somewhat in the range of 40K/Month. This seems fair.

However in AR, pg 98 says “TAC Security INC Receivable from subsidiary 953.42” - out of 10 cr revenue? This seems fishy.

Agree with you for all others points, one should invest with extra care.

Forensics and the art of triangulation this is the appropriate thread for tac infosec I think we should not discuss about this company any further on this thread.

We cant coat tail Vijay Kedia ji… He has hundreds of crores to burn… We guys will hit exit button with shaking hands once the stock hits lower circuit<>

Yes, it is strange, but the website of ITC Labs also showing the same status. So either they are changing something or website might have been hacked or even worse, they didn’t renew their domain.

Sorry to be a party pooper but I just want to add a different perspective to this discussion.

Best way to invest in micro-caps of unknown provenance is to answer the following question.

Between two investment options where First gives you 100% return with 75% probability of losing your money and Second gives 25% guaranteed return with no loss of capital, which do you think is better option?

Rational folks will say that both options are equal.

However in investment world many retail investors believe option 1 is better as they only look at potential return (100%) and ignore risk premium (75%). This is what drives rush for micro-caps stocks because they can rise really fast in a bull market when there is a relentless gush of liquidity in the market. But when liquidity dries down, and often without advance warning, drawdown can be severe.

On the other hand high quality companies with a track record of building moated businesses, credible management and strong cash flow generations are ignored because they over long time compound money ONLY at 15-18% (not exciting for someone looking for a multi-bagger in 1 year). One of the reasons they are avoided by retail investor is that they are “well discovered” names.

In my long association with equity market (since before dotcom time), I have seen quite a few bull markets. One consistent principle across all of them, I have seen playing out, is the belief that one wouldn’t lose their capital in micro-cap stocks because of quality of their research or will be able to get out of them in time with good returns. Part of that confidence comes from analyses done on reports, commentary and exciting growth guidance given by the management which during a bull market can be very credible.

I am not an Oracle but by simply extrapolating history I will confidently be able to bet that 20% of the companies giving 20% growth guidance will not survive next 10 years and another 50% will be average investment giving returns not justifying the risk premium. Only a handful will probably make their investors make money.

Not all micro or small cap investments are bad. But evaluating management’s ability to execute well and good intentions to act in shareholders’ best interest is much much harder than many people think it is. There is no free lunch in equity market. More money in short time comes with a lot of risks and some catastrophes.

totally agreed sir.in these scenario I feel better stick on

1-technicals entry and exit with proper stop loss .

2-you have to take position in any script if the risk reward ratio is favor (if a stock is in continues up trend keep 21 DMA as a exit it may differ for others )

3-don’t go for bulk entry took staged entry keep pyramiding while stock showing strength

4-if it is not following you please position sizing

5-don’t exceed more than 5 Stocks in your portfolio (initially one can entry 10 stocks keep pyramiding while showing strength exit if not and reduce the number .try to concentrate the portfolio as much as possible with proper exit plan

6-only portfolio make you rich not stocks

7-creating wealth you need to have proper stock allocation system

It was just an illustration to show the concept of risk premium that people ignore when chasing high returns in highly risky micro cap/small caps.

Here is an excerpt from my original post.

On the other hand high quality companies with a track record of building moated businesses, credible management and strong cash flow generations are ignored because they over long time compound money ONLY at 15-18% (not exciting for someone looking for a multi-bagger in 1 year). One of the reasons they are avoided by retail investor is that they are “well discovered” names.

Landmark: cash conversion is inexplicably low given 36% (& growing) of Merc business is at nil inventory.

Dream folks: Interesting business but have following concerns:

Regulatory risk: Merchant discount rates revision by RBI.

Governance: No CFO till 2021. Further CFO is paid just 30 lakhs annually vs 3 cr+, the company’s CMD draws annually. This highlights the lack of quality talent available to the company.

no pricing power: No scope of GM% expansion. Through operating leverage, ebitda can improve though.

Entry barriers: Very low. Nothing proprietary as a platform. Anyone can enter, anytime.

These need to be clearly mentioned. A company that blind sides you on 60% of their current customers and only mentions the 40% they are going after who also happen to be some of the largest fortune 500 companies is suspect.

Mgmt guided for 30-35% growth in FY25 in an interview; Revenue up by 23% & PAT up 53% in H1

Company has also announced 440cr which will come live by March’26. As per the numbers provided on conference call, company will be making 110cr PAT from this CAPEX (for reference, company’s TTM is 115cr)

Currently trading at 26x trailing P/E

Read more on key growth drivers & risks in below post

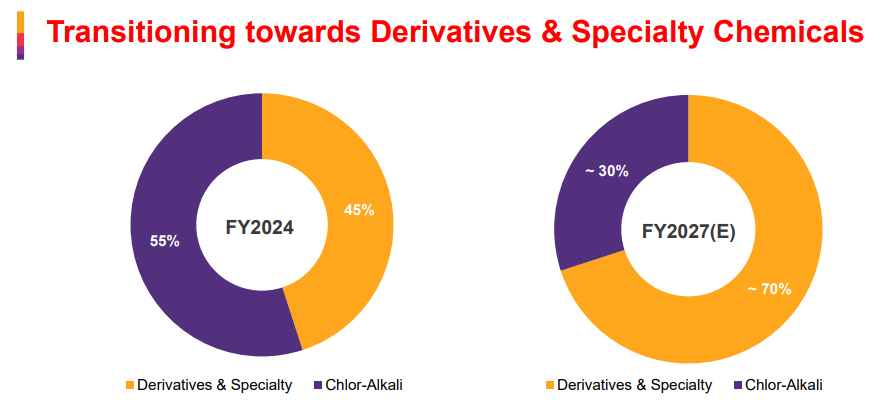

Epigral (formally known as Meghmani Finechem) is a chlor alkali product mfr (like caustic soda, chlorine, chloromethanes, etc) but is shifting to derivatives & specialty chemical products which will help them manage the cyclicality issues.

Mangement has guided for 20% volume growth for next 5 years, and is targeting mainly domestic customers. Few of the products are industry first in India. Further, government has extended/introduced the antidumping duty on CPVC / ECH for next 5 years which will help them in maintaing margins. Have guided for aggressive CAPEX of 700cr in next 1-2 years & recently raised funds through QIP.

Summary:

Market Cap: 8000cr

Sales: 2000cr

Trailing PE: 28x

ROCE: 28% (without CWIP assets); company has focus to maintain 25% ROCE for future CAPEX

Guided for next 5 year volume CAGR of 20%

Pricing support + Operating leverage, if any would be additional

To be noted, that there was a transaction in 2018 for buying out stake of the company by promoter, which investor believes was not favorable for minority shareholder; Mgmt has accepted that in one of the interview; I believe management and company do evolve over time but important that we we know this factor before making any investment