Why would coal supply go down if china stops importing?

1 Like

Mines that are profitable will be closed

Coal mines are several meters below ground level and it’s not generally easy to restart them

Existing inventory in warehouses etc will cushion initially but eventually run out

not able to understand. if china has decreased import of coal then why global price will increase

Coal price increase has already happened. Both thermal and coking coal prices are not just at skyhighs, there is physical shortage too.

Global demand supply has a very delicate balance. China tried to mess it up by stopping Australian imports an year back. Result- Australia reduced supply- mines stopped increasing production, some marginal mines closed down.

But did global demand reduce. No, Global demand is still increasing every year. So, we have scenario of reduced supply and increased demand leading to sky high prices and shortages.

Same can happen in steel industry too. China is reducing steel output over next 5 yrs.

But, is global demand reducing? No… Global demand is increasing every year…the possible result is steel shortage in coming yrs + sky high prices.

However, there is big difference between Coal and Steel.

Coal will eventually be replaced by renewable - say in 20-30 yrs.

But Steel has no replacement. And it is no longer profitable to build steel plants in most parts of the world like Europe or USA.

India is the only large country which can expand steel capacity- but India has limited iron ore availability due to auction of mines and long gestation periods to build a new steel plant. Most of growth that happened in last 5 yrs is because one player acquiring another, and not because of new steel plants in India. Example- Tata steel acquired Bhushan steel, Usha martin etc.

13 Likes

Chinese steel inventory (stocks) drop to 8.5 months low because of fall in output. If there is gap between demand and ouput, this inventory will keep dropping.

China’s domestic steel prices, especially those of long steel items, have grown steadily as market sentiment improved with the substantial fall in steel production. As of September 22, the national price of HRB400E 20mm dia rebar touched a four-month high of Yuan 5,754/tonne ($889/t) including the 13% VAT, gaining another Yuan 197/t on week, according to Mysteel’s data.

https://www.steelmint.com/insights/China-mills-steel-stocks-drop-to-8-5-month-low-246560

4 Likes

Are you tracking chloromethene price ? Please if u can get it . I have heard it has also gone up very much .

no, not tracking chloromethane. caustic soda lye has gone up to 42k. caustic flakes upto 45k.

dealers expect 50k in coming weeks. generally price revision is fortnightly. next revision will be on 01.10 and then 15.10. let us see.

disc:- personally booked out major quantity from GACL. was a value buy at 300 in feb. now not so sure. last cycle it went till 900 when chlorine was negative. this time around chlorine is also positive. but i try to book out when i feel my MOS is gone. i might lose some major/minor upside from here, but all part of the learning process

2 Likes

I am not tracking GACL , but sure all company in caustic will make bumper profits. I am tracking TGVSL. It had approx 500 cr turnover from caustic. Their production was down due to covid and low price of caustic. Avg realisation must not be over 23, 24 last year. So with price of 42 or 45 they can easily add top line of 300 cr average and bottom line will be substantiall higher for all caustic manufacturers. Their RM is mainly salt and power cost wich has not gone up that much

Disc invested and having trading position also in TGVSL

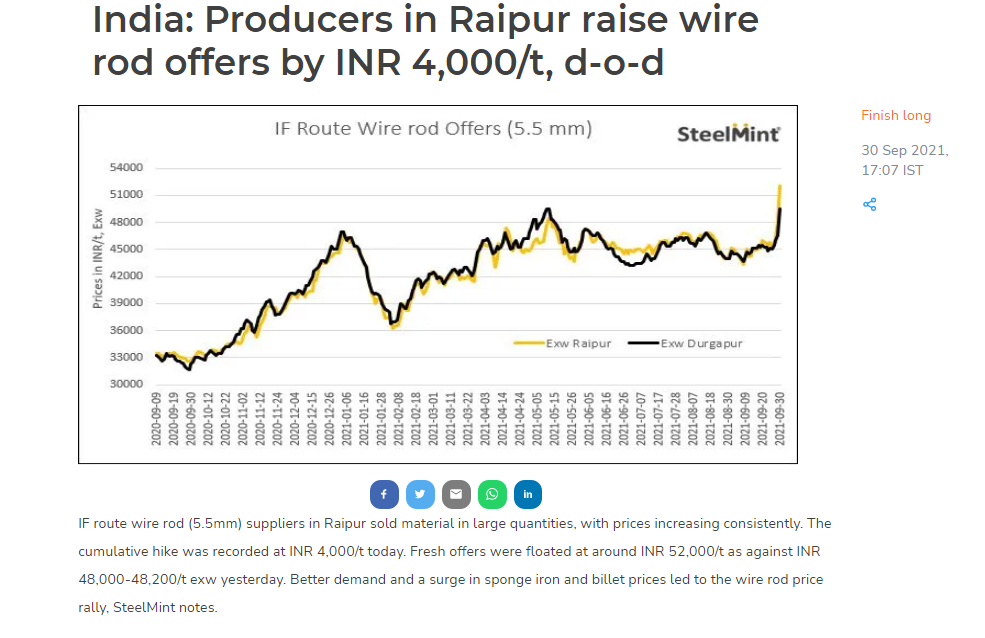

Seeing a sudden surge in steel prices. . Any idea what’s driving this?!

Coal prices going up, and This was expected as per my posts above. GPIL is expanding Billet capacity and substantial sales will come from billets and wire-rods going forward.

{kind=link}

Pellet prices raised to 12000-12300. This is contrary to what many investors were expecting given the fall in Iron ore prices.

1 Like

Very sharp spike in Pellet prices.

11,000 to 13,000 in 2 days flat!

2 Likes

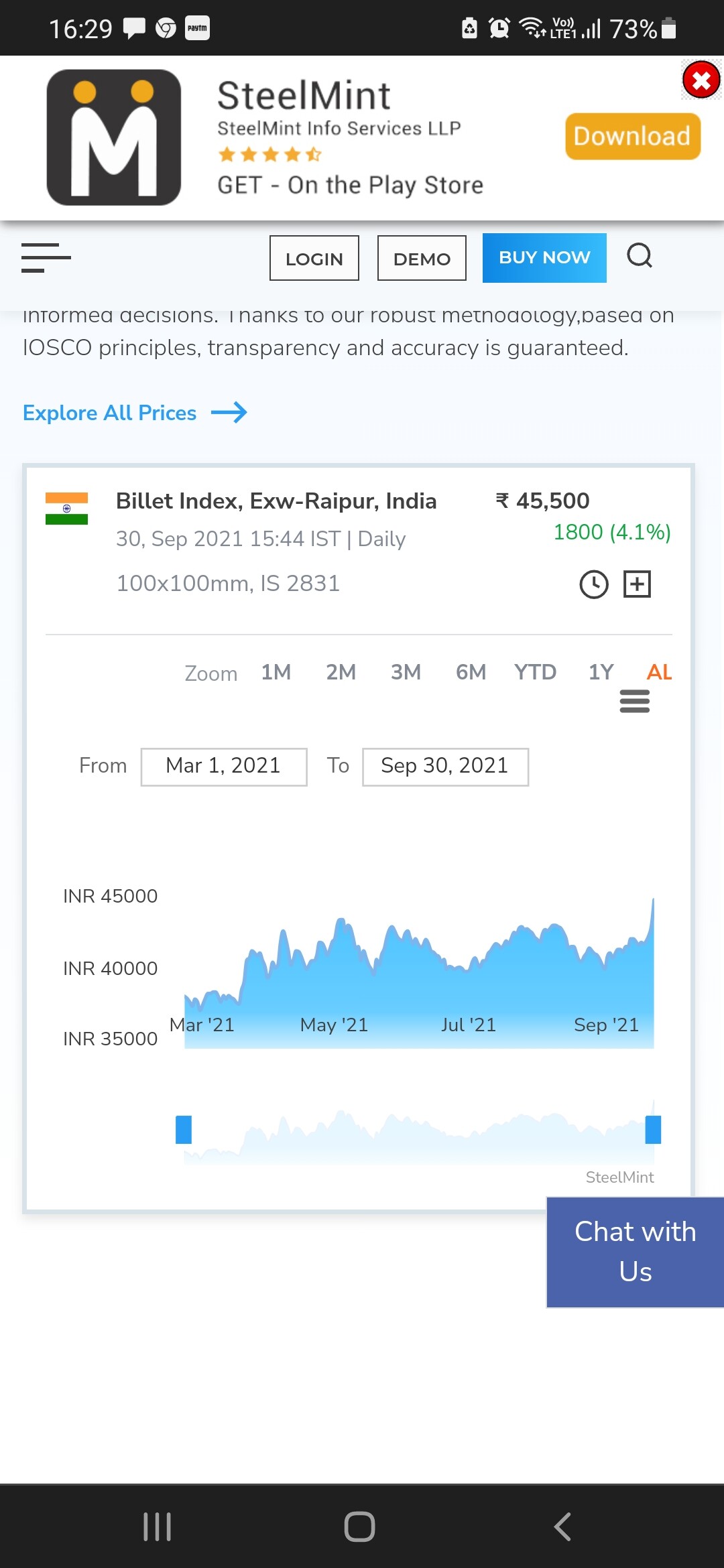

NMDC and GPIL building in worst case scenario on iron ore prices. This is in sharp contrast to high premiums being bid in iron ore mine auctions. Which one will be right? My views are as below

10 Likes

Sir, I don’t think it is fair to compare NMDC with GPIL. (Rather, one can compare GPIL with Shyam metaliks, and NMDC with MOIL)

NMDC has a history of huge capital mis-allocation over last many years and has a very poor quality promoter and management.

NMDC earned huge money over last 10 years, and remained debt free.

But what did NMDC do with that money?- it built a steel plant which hasn’t added much value.

Also, it gave the money away in Dividends (very high share as percentage of profits), as govt wants dividends from PSUs.

It spends extra money on CSR, donates to PMCare funds (over and above required limit).

It may earn huge money in coming years, but the issue remains how it invests that cash.

The employee bonuses, dividends, CSR as it did in the past? or some better use of money.

If money is spent primarily on dividends, then NMDC should be valued more like a bond or a REIT which are are valued on yield basis.

If shareholders are not getting that money compounded for their benefit, then what’s the value of that money for shareholders?

2 Likes

Well am neither comparing, nor recommending. Just saying what the stock price is building in. One has to build one’s own conviction.

3 Likes

Also, you have mentioned current pellet price as 11,000 in the table.

But as of today, pellet price is Rs. 13,000

@Rakesh_Arora sir, again a very good write up. This time around there were too many moving parts, which is fine given the problems in China. Sir, one thing which has been headache of this industry is coking coal prices. I heard in recent interview that JSPL will be having it’s own coking coal and steel prices are going to move up sharply once again. So, doesn’t this give jspl an advantage ? And will the steel prices correct if coking coal prices correct ?

Intention is not asking for a recommendation, just asked only out of curiosity, have no position there.