Rise in Oil Prices could Further Damage Sentiments, says CLSA

Cuts price targets on OMCs, says consumer staples and paint cos may feel the heat, too

Our Bureau

Mumbai: The rise in oil prices is increasingly becoming a matter of concern for investors. Hong Kongheadquartered brokerage CLSA on Thursday said that a further rise in oil prices could damage investor sentiments and raise the twin deficit fears.

Brent crude oil futures crossed $74 per barrel on Thursday, the highest level since late-2014. India imports 80% of its total oil requirements.

“Oil is now firmly above $70 and there’s talk of it moving to $80. This could further damage investor sentiments, as the economy doesn’t have a lot of cushion, especially in a pre-election year,” said CLSA in a note.

As the current year is a pre-election year, a rise in oil prices to $80 per barrel could prompt the government to maintain petrol and diesel prices at current level and there could be a cut of ₹4 per litre in fuel excise duties, implying an impact of ₹50,000 crore on tax revenue, said CLSA. The firm added that the government’s petroleum subsidy for the current financial year could be higher by ₹30,000 crore than budgeted if oil were to average $80 per barrel.

Finance Minister Arun Jaitley had allocated ₹24,933 crore for petroleum subsidy in the Union Budget for 2018-19. The subsidy allocation is a 2% increase over the revised estimate of ₹24,460 crore for last financial year.

CLSA on Oil Price Surge

“Overall, we estimate that crude at $80/bbl can have an impact of as much as ₹750-850 billion (₹75,000 crore-₹85,000 crore) (40-50bp of GDP) if the government takes the entire hit from hereon. The revenue shortfall risk from weaker GST collections is 30-40bp (basis points) and therefore the cumulative fiscal impact would be 70-80bp,” said CLSA.

CLSA said the twin deficit issues could re-emerge with current account deficit moving up to 3% of the gross domestic product and fiscal risks to the tune of 40-50 basis points of GDP. The weak US dollar and strong RBI reserves would limit the currency impact, but the era of rock-like stable rupee may be behind us, the firm said.

In terms of sector impact, oil marketing companies could be at risk if the government passes on some subsidy burden to them. In a separate report on Thursday, CLSA cut target price on the three oil marketing companies — Indian Oil Corporation, Bharat Petroleum Corporation and Hindustan Petroleum Corporation — by 17-20% citing macro concerns. These oil retailers hit 52-week lows in Thursday’s trade.

CLSA said rising oil is also a negative for users of oil-based chemicals industry including consumer staples and paints. The brokerage added that a potential weakening of the rupee will be positive for exporters.

Market need to brace for another bomb whether Trump will stop or renew sanction waiever on Iran…coming in May…more volatility

Can anyone here explain how are RIL’s earnings affected by rise in oil prices? Its share price is stable though not certain if the same can be said for earnings and refining margins. What I believe is, crude is their key input so its negative for them. But market seems to know better. Though I understand for RIL’s its much more complex than just that. Thanks!

On the refining front it does not impact them much, the refining margins remain largely intact as both the input cost and output price are hedged simultaneous. However, if the domestic fuel prices remain low despite increase in crude prices, then its margins by retailing are impacted. In such a situation, the company may export higher to protect margins, but loses out on marketing margins. Experts in the sector, may feel free to correct me.

Disc: Invested in Reliance Industries

Regards

SJ

Hi @jitenp i am bullish on hotel industry cycle i had upload my small write up below

on seperate thread could you please advice

regards

Good post. Keep it up. Hotel sector, I am positive.

Your views on alluminium after the recent developments

Still positive. Short term upmoves and corrections keep happening.

I was planing to invest in monnet Ispat 6 months back ,buy Luck didn’t invest

In a bankruptcy case, shareholders are last in the pecking order. I couldn’t understand how one can think of investing in NCLT companies, without knowing what the equity dilution will be ? Not knowing the value of one’s equity, post the resolution.

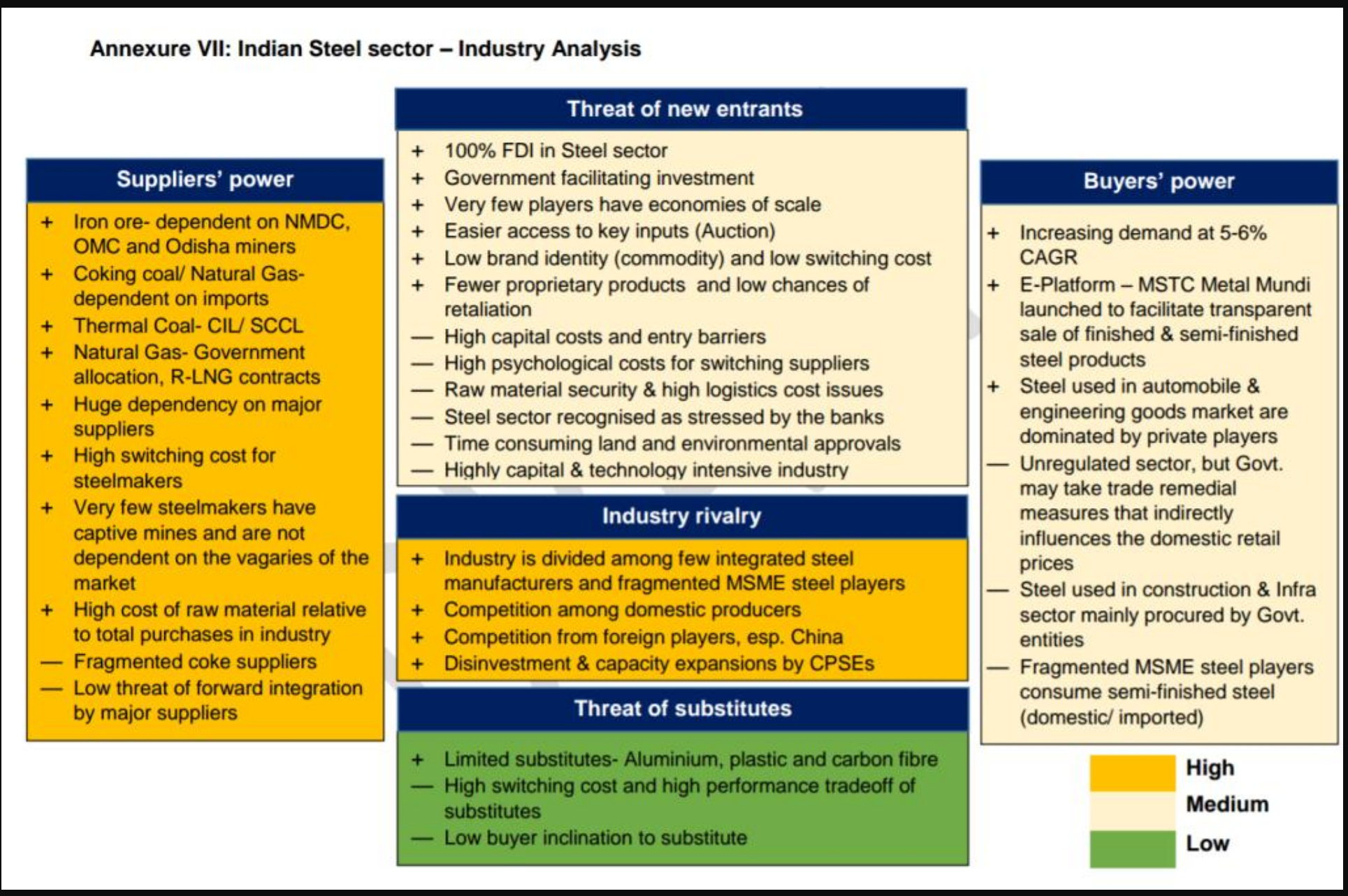

CARE view on steelsector

What r yr views on Prakash Industries result? Good performance on power but not so good on steel. If it has to buy power instead of generating it performance would have been very poor. Debt reduction not as promised. They talk more than could deliver, specially future guidance.

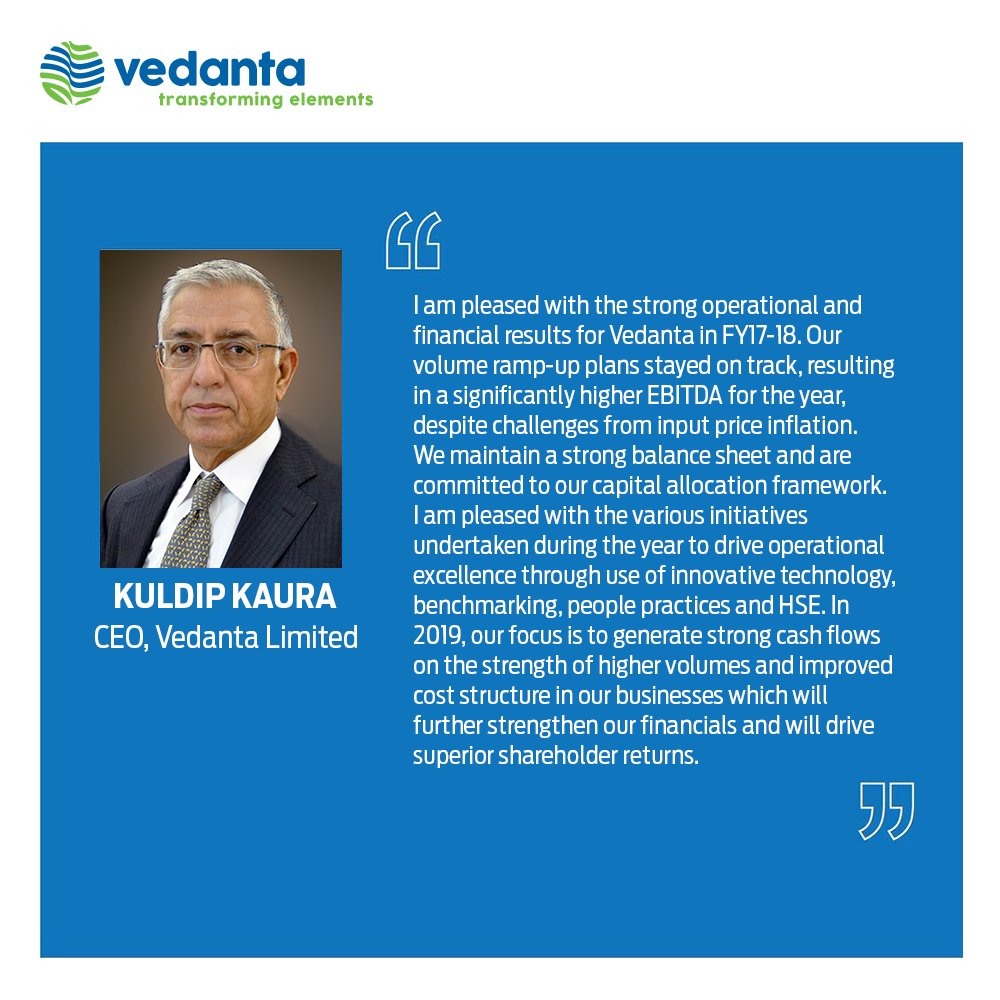

Good results from vedanta…

Investor Ppt - https://www.bseindia.com/xml-data/corpfiling/AttachLive/b5d3b34f-6748-4956-b2fa-aa5493c79d56.pdf

Disc: Invested

Prakash Industries has reported EBITDA margin of 23% in Q418 and Godawari has it at 28.4%. Does anyone know what has been typical peak EBITDA margin in previous cycle tops and for how many quarters these margins sustain before the reversion to mean starts happening ? I hear generally peak margin has been 25% in previous cycles but do not have historical data to validate this.

Disc : Invested in JSPL. Trying to understand how much more time we have before cycle turns back.

Is anyone following the strike at imfas plant?They price has corrected because of that. And additionally if anyone is following ferrochrome cycle, please share views.