I am midway reading into coffee can investing book by ambit employees. They have so far not talked anything about insurance at all, be it health or life term…what’s others view on that. Is insurance not a financial investment …a coffee can to break in case of a rainy day?

Also, he speaks of REIT and similar infra … i think these commercial real estate would also be very risky? Regarding residential, since 2013 i have known friends who invested in small residential land in their hometown tier 2 cities and have made significant returns… so all residential should not be taken in same light i feel…i think they speak more on experience of metro cities…pls let me know your thoughts…thanks

Just a guess …may be insurance companies were not listed at the time it was written .

As all most all insurance companies git listed only during last 2-3 years atleast from private sector .

-

When making an investment in general, I think we should ask ourselves (based on our abilities) if the said investment can generate at least 15% cagr with some degree of certainty. If this question cannot be answered with some degree of certainty & quality rationale then it might not make sense to even consider the investment.

-

Many investors have experienced the draw downs of small and mid caps and suddenly 18% cagr seems like a difficult task in our minds. Truth is it was always difficult and only very skilled investors can do across an entire cycle. But the bull market made it seem like 18% was normal and 15% was low.

-

I think knowing our limitations as investors is what can have us come out ahead and make money in the long run. Spotting a page inds at 500cr market cap is not something that all of us can do, let alone deep dive into the business and do a lot of primary research to build the thesis and to garner conviction to hold.

-

This is why I feel like as learners we should target a 12% cagr over a very long period of time. With such a target in mind, you are able to buy good businesses at reasonable valuations and further get the confidence to add to the position during a decline or good results. The two well known index funds namely N50 & NN50 should with a high probability deliver such returns over a long period of time for investors, at least with a 10 year view I think in India they should deliver that return. If the index funds can deliver such returns then it warrants a thorough look at the portfolio. Can the portfolio companies deliver higher returns with some certainty risk-adjusted?

-

For long term investors opportunity cost is a big cost. If you cannot deliver over the index over a long period of time then in essence you have been a poor investor let alone on a risk adjusted basis.

-

There are great businesses in India that can cagr at 12% for long periods of time, even if you take into account some de-rating (not saying pay 80x for such companies!). In many cases you can snag a good yield as well. That yield only keeps getting better over long periods of time as the company grows.

-

The dividend yield is what makes such investments attractive over the long run. A doubling of the dividend yield on your investment alone can have a big impact on your long term returns. And dividend income is far more predictable than capital appreciation as it is not linked with the market movement, but the profits of the business.

-

I do think the two indices make great candidates for a coffee can portfolio. In addition to coffee can stocks that are cash generators. Holding onto such companies for long periods of time can not only compound your capital but also give a fillip to your portfolio through dividend yields, increasing your overall return on the portfolio during bad times and enabling you to perhaps outperform on a portfolio level during rough markets. The index funds of course decrease the risk of opportunity cost on stock selection in the portfolio.

With the above in mind I look forward to ideas from forum members

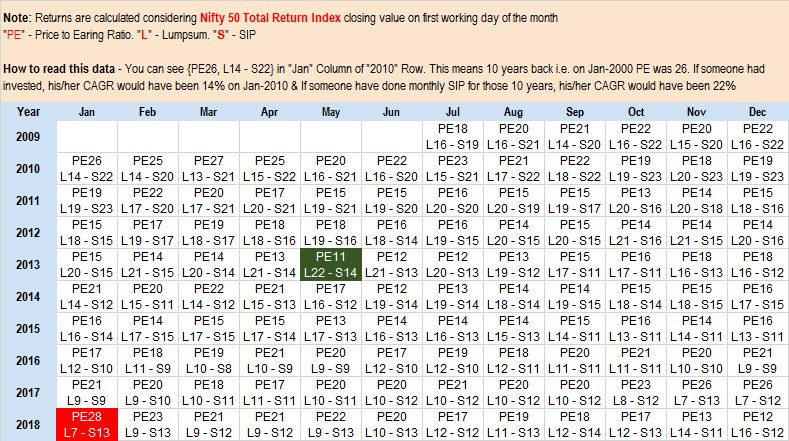

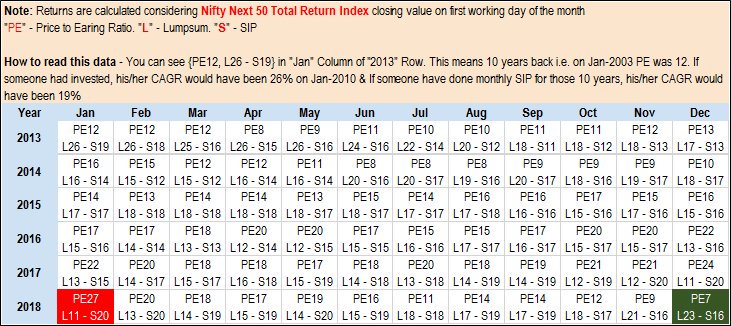

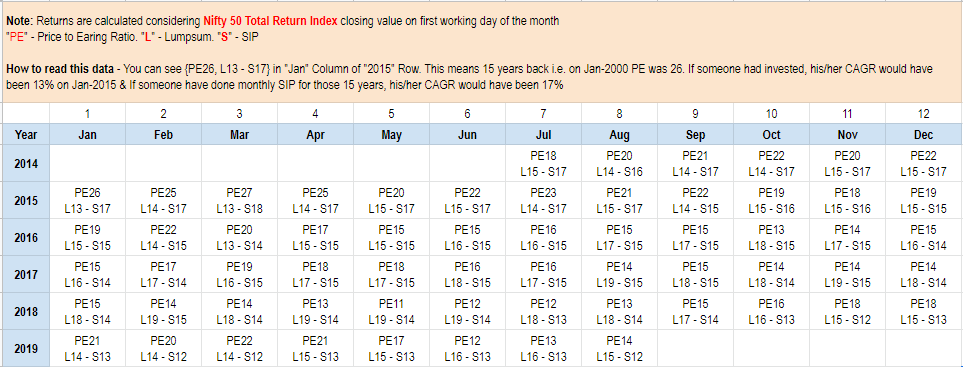

Requesting @Hocuspocus32 to share an image on the index fund coverage of the listed universe. He has studied index investing in India more than most in my opinion.

11 Likes

Image Credits : To the respective owners who has created it these are not mine, I have gathered this from google.

Historical index returns can be seen here : Historical Returns

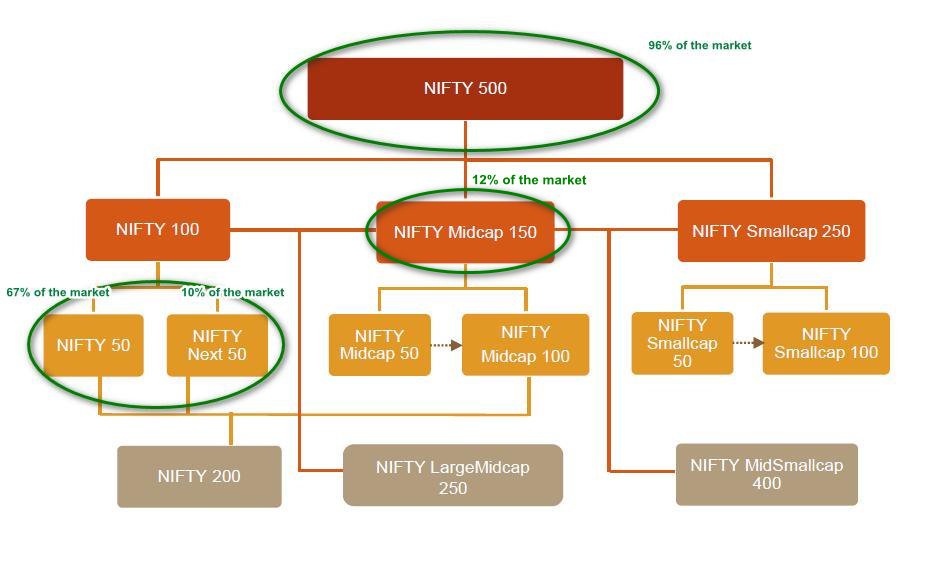

The images are self explaining and if we are passive investor running in a SIP mode or Lumpsum , over long term the Index has provided very good returns in the range of 10-12% , which is pretty okay to me as capital grows the main priority for me is NOT to loose the capital, returns being lesser is acceptable but loss in capital is not. In my view doing SIP in N50 and NN50 itself covers 77% of the market and Indias top 100 listed companies, so if you go a little further and add NMC150 to it then you just covered 89% of the market, in my view thats more than enough to grow your capital at a normal pace.

For more information on Index investing you can track :

https://twitter.com/IndiaEtfs

https://twitter.com/PassivefundsIn

4 Likes

I would like to add another one. S&P BSE MidCap Select Index.

I want to highlight the human-tendency to start out by looking for good things, the returns, as opposed to uncovering the challenges that will come-by. It is more important to look at the entire picture, as opposed to the selected past or the recent past.

Reality of Investing in ETFs could be very different from the expectations of 10 to 15% CAGR. The internet has a lot of data but only for last 10 years. Some might even fish out 15 years data. This is a folly, because our markets have been at their best behaviour in the last 14 years. Its the ten years prior, to these 14, that the market was challenging and bad. So much so, that there is an entire generation of smart and experienced people that have washed their hands of the markets. Look around, and take their opinion, find out why they say what they say.

There were scams, bloopers, sideways market, sluggish economy, no government push or interest. Most people lost money, and other lost patience. And it shows in the numbers.

Nifty50 High of the year 1992 was 1260 and high of the year 2002 was 1201, which gave its investors a CAGR of a negative 0.48% for the whole decade.

In that period, all other modes of investment did well, and the Stock Markets weren’t impressive. FDs, PPFs, Gold, Silver, Real Estate, Proprietary Businesses etc. Yes, a devastating fact.

Therefore, it could be injurious to ones health, financial and otherwise, to focus on the returns. It is a folly to think that if I reduce my expectation from 15% to 10% I am automatically getting some kind of a right to assured returns.

I have a very strong feeling that the markets will be in a huge lull for the next decade, because everybody and his neighbour is now involved. People have the bravado to put a chunk of their money in every script that corrects, as they “know” that it will now only go up! This is so far from reality. I believe, there could be free money in Vegas, but not in the stock markets.

5 Likes

Hi Vivek,

I think retail investors do not make such analysis or images. They don’t think like that. It is the fund houses that make these brochures to sell their products. They show you a selected part of the reality, to convince you to buy their products. They aim to massage that lingering idea in your mind that Stock Markets is easy money, and to their benefit, the recent decade is irrefutable proof.

I would not fall for it. I know I will have to dig deeper, if I want to survive for the very long term.

Now since you told me not just look at a particular period , what you have did is the exact opposite of what you have told me not to do.

Now regarding the performance from 1992 to 2002 I have to check how the performance would be for a lumpsum investment, but I am 100% sure that an SIP return will be good from 1992 to 2002 period.

For selective 5-10 years periods many bluechips has also not given returns like RIL , ITC etc, so if you have a better way to make the 10-12% then please do share.

for those who needs to know the levels https://www.niftyindices.com/reports/historical-data

1 Like

Again… positive assumption at the onset. Why the assertion? We are looking at historical data, from the comfort of our chairs. We have managed to breeze through twenty years of anguish, greed and fear in just one single candle stick chart. A lot can change in real time.

I asked my friends here to not be optimistically selective, get all gung-ho about investment for the wrong reasons and find themselves in a muck.

You show little faith in my way of thinking, and in the very next paragraph you ask for “a better way”. I too was pointed in the right direction by somebody and I was happy, thankful, and eventually grateful. Instead of taking the idea forward by asking constructive questions, and promote mutual learning, if you want to bring me down. Then, I’d say the effort will be counter-productive.

For the sake of completion… Index investing in Nifty50 gave a return of 8.38% CAGR since the top of 1260 in the year 1992, till the top of 12000 in 2020 (made an assumption/prediction). Not impressive at all.

My whole point is people who don’t have the calibre to find great companies and read financial is better of with index investing.

Passive vs active investing styles that’s all, both has merits , so the investor should choose what he needs and should understand what his skills are and take a call.

Yeah, but what if he chose passive investing, expected smooth sailing and a pot of gold (12 to 15%) at the end of the rainbow. Then, he’d be in for a surprise of his life. I clearly see that this investor’s mind is not ready for investing, and he’d thrown in the proverbial towel in any of the following cases:

- A sharp fall, where he would stop SIP, and even consider getting out partially or entirely.

- A dull sideways market for two years, and he needs the money to buy a property or even a car. Pay loans, medical bills, education etc. All real world problems, which the candlestick chart does not encapsulate.

- A sharp rise, where he may feel that his sins will be redeemed if he gets out now. He does not want to feel the way he did in the recent past, when his PF of hard earned money was XX% down

I can continue this fiction till the cows come home, but you get the point.

I intend to put across the fact that investment is simple, but not easy. Just investing in Nifty50 ETF will not cut it. Primarily, a psychological overhaul is required. And then an investment strategy. Doing SIP in ETFs won’t do the job.

The investor must have a fair idea as to what his journey of investment will demand out of him, and not a watered down version of it. This will depend on the chosen strategy (this is where it gets really interesting). An aggressive strategy will have wide swings, but it will be really very hard to reach the finish line and see it through the whole decade. A passive strategy like SIP Nifty50 ETF will swing less in comparison, but won’t fall short of being a psychological challenge. The returns too would make me feel that I am leaving a lot on the table. I have planned to fall somewhere in between.

3 Likes

I am both an index investor and a stock investor. I invest in Nifty 50 and Nifty Next 50. A couple of years ago, while I was absolutely new to any kind of market-linked instruments, I had invested in an equity fund and I used to look at the movement of Sensex around 2 PM or so and thought I could predict the movement of my fund’s NAV. I thought if this Sensex goes down, my fund will go down, so the NAV will fall, there by I will get more units if I purchase that day before 2.30 PM or so, sometimes it happened, sometimes it did not. Little did I know that there exist index funds that when invested on the day the index falls, I will get more units.

While having experienced the absolute growth of capital through FDs, I wanted to be absolute with equity too (didn’t know about asset classes). Later I came to the conclusion that index investing is the close I could come to absolution in equity instruments. Absolution to me in debt is FD in a PSU bank, in equity the index. No matter the constituents, if it delivers 12%, it will be great, although the journey of volatility (particularly in the case of NN50) is real and the destination of return can be talked about only when we get there, assuming we will get there.

I have both booked some profits from Nifty and staring at a small loss in NN50, so I am yet to experience a big drawdown of 30% or 40% in either of the indices.

If the regular folks of our country keep on SIPing, I don’t know we will see such falls (I’m yet to experience and in fact waiting for it, so that I could buy the whole Nify 100 for a great bargain).

Also, I am not too optimistic about the regular folks and the inflows of SIPs, many of them will stop, as they are not educated enough about the market cycles, non-sequential returns of equity, PE expansions, exodus of foreign money, heated markets waiting for any news for a negative trigger.

My little experience is obviously not enough to predict.

So, while testing the waters with stocks, I also invest in index, although these past few months, I am not seeing the kind of fall in the indices I had seen before (particularly in NN50), so I cannot invest in them, so waiting for the indices to fall and waiting for the big fall. And I don’t want to wait on sidelines either, so nibbling in stocks. If you are afraid of the whiplashes, you can never tame the bull (pardon my metaphor).

Here are a few educational articles on index investing from freefincal.com which I am a regular reader of first, then VP. For a non-finance person like me, these are more than enough to get educated, inspired, and achieve good returns, and for others too, these will be good as the time and effort put in by the author Professor Pattabiraman Murari is amazing to say the least, and I take this opportunity to thank him. He is a VP member @pattu

Here is the category

https://freefincal.com/category/index-investing/

Here are the articles which are not in the above category, I may have missed some, but nevertheless, these will give the you the idea.

A couple of additional articles in relation to index investing

6 Likes

@jamit05 I think it was suggested as a part of the portfolio. But I’m very sure many active mutual funds have underperformed the indices in the long run. And these funds are run by far more capable fund managers.

Markets have periods of lulls and then rallies and falls as well. If you are only going to look at one lull period then it may not make sense. Further one thing that the index as itself does not show vis a vis an index fund is the dividend that comes in and then is reinvested (growth option). I do not think the data presented for the “Nifty” in terms of cagr accounts for dividends. I could be wrong but this could add to returns significantly.

If you are going to bring in hypotheticals of each individuals psyche then its a pointless discussion. A sharp fall could stop SIP but what if the individual is obsessed with averaging down and doubles SIP during such a period? I think we should leave out predicting an individuals situation or thought process as that is something that is fairly irrelevant when it comes to “studying” assets. How a personality deals with lulls, rallies and volatility wont add much to our discussion.

I feel like we should invest looking forward. And looking forward I think the top 100 companies in India should grow earnings. I think the “India Story” is alive and well and I feel like expecting low double digit cagr from equities over the next decade or decade and a half is a fair assumption. Question is how do retail investors do this and not miss out due to error or opportunity cost so to speak.

1 Like

Before writing all these you should atleast know me right? How can you be so sure I will do all this?. Let’s see how things span out in future , only because @1.5cr told to post in thread I did it,I am not good at making you or others convinced to do anything, I just posted and if you have better knowledge take your decisions based on that not everyone should think along your line’s. If a person doing index investing will make money in long term or not is only answerable in future ,so I move and do things with Conviction you can defer and not do and find mutlibaggers ,I am not that skilled

2 Likes

Im uploading daily data of the nifty50 and nifty100 from the nse website from the nineties. Nifty100 only available from 03.

NIFTY 50_Data.xlsx (249.1 KB) NIFTY 100_Data.xlsx (150.0 KB)

Dhiraj Dave’s presentation on index returns is good material should anyone want to go through it. It has some good data that one can use. From what I have read in books, blogs, articles , letters etc - there seems to be a theme that the index has a tendency to return 13% over a long period of time

It should be 6-7% + inflation. Now inflation is lower than historical inflation, it should trend to 10-12%.

Hello Vivek,

I don’t think Amit was referring to you when he said “this investor”. I think he has a point, what he is saying is that no form of equity (even index funds and etfs) can completely take the investor’s behaviour out of the equation.

Thanks

1 Like

To further the discussion. I see that an investor may resort to low volatile types of investments thinking that because the returns are just a little better than FDs, so the comfort too should not be different. This, imo, couldn’t be further from reality.

I do not think that this Cycle will pan out anything like the last one.

My Expectation is based on the following logic:

Cycle 1: 1992 to 2004, 12 years, Returns were abysmally low. The Expectations that were based on the earlier cycle were clearly shattered.

Cycle 2: Then came, 2004 to 2019, the next 15 years Nifty50 gave 12% CAGR. Nothing too impressive, considering that this would be achieved if everything went 100% as per the plan, and nothing got in the way like:

*No withdrawls inspite of seeing sharp up-spikes and down-spikes for the whole period. This, I think is possible for someone with superhuman abilities.

*Same sized SIP from 2004 to 2019. Which does not sound practical.

If the investor increased the amount, esp towards the fag end of the cycle, which is highly likely considering that he would be doused in Recency Bias and would be better paid, then the returns would be diluted.

I know a handful of investors, and none has matched this standard. Each has been wayward, into smallcaps, derivatives etc, and called it a learning experience.

Now, we are in Cycle 3:

My expectation is clear to the extent that Cycle 3 is definitely NOT going to be like the very previous cycle, but more like the one before that. So, I am not professing that one should invest in the market for the returns in the near term, but for the “build-up”.

2 Likes

What your theory of cycles 1,2 and 3? Is it some economic or political cycle? Or just sensex movement is basis(then you are forming your theory on only 2 data points, huge extrapolation).

Why are you selecting 1992 as start point? Why not 1991? If you take that you have 12% CAGR excluding dividend. You can add 1-2% of dividend yield to that.

It is good to be cautious always with your hard earned money. But putting a theory which has no basis does not make any sense to me. We can always argue PE is high, we see a move against globalisation, slowdown etc or counter arguement like low PB, cleanup of corporate India, demographic dividend. That will make more sense than hypothetical cycles.

5 Likes