Entering a new segment is always a significant positive development. what is the word order value of these 2 vessels?

Updates from management interview on the new order:

|-|Order for 2 autonomous electric vessels with an option for 2 more vessels, will be the 1st such vessel in the world (from company called ASKO Maritime, Norway; partly funded by Norwegian government)

|-|Order amount: 125 cr. (including both vessels)

|-|Operating at 90% levels in main yards in Cochin and Mumbai

|-|Building an order of 23 electric small hybrid boats for Kochi water metro

|-|Ship repair business doing quite well (with some demand from China shifting here)

|-|Current pipeline of bids > 10’000 cr.

6 Likes

There is a contingent liability of 2000CR that is being highlighted, can someone please shed some light on this?

About 1513 Cr is bank guarantee.

1 Like

Although my knowledge of Free Cash Flow might be restricted for now, but I found that CSL has an inconsistent history of Free cash. This is the only point in my current model that is a Red Flag for me.

With that said, the company enjoys a healthy cash position.

Now my only doubt was whether the reason for a low and sometimes negative FCF is high Trade Receivables? And is it common for PSUs to have low Free cash flows?

Eying opportunities in inland water, coastal, fishing vessel segments: Cochin Shipyard’s CMD - Business Line - https://www.thehindubusinessline.com/economy/logistics/eying-opportunities-in-inland-water-coastal-fishing-vessel-segments-cochin-shipyards-cmd/article32534577.ece

2 Likes

Last 10 Years Cumulative CFO is approx 1/3rd of Cumulative PAT. Seems a lot of cash is getting stuck in working capital since the business itself is lumpy. But shouldn’t that normalize over a decade?

Disc :Not invested.

FYI- RK Damani and Professor Sanjay Bakshi’s Value quest fund hold Cochin shipyard, check Annual report 2020.

2 Likes

No, cash is not getting stuck in working capital…due to lumpy nature of business they always have kept good cash on their BS. Over the years, especially after the IPO, this cash has generated lot of other income which is mainly interest income and is not accounted in the CFO. If you remove the other income (after tax), PAT would be 2/3 of the CFO which makes sense asuming a 30% tax rate. This is my understanding. I could be wrong.

1 Like

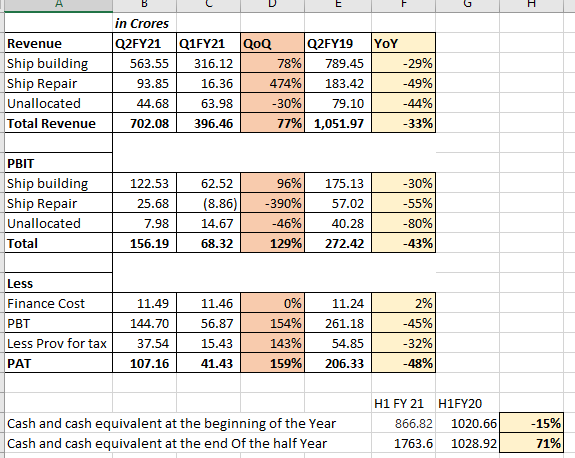

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/0db34576-1b78-469e-8741-655c89f5fb23.pdf

During Quarter II, in order to meet the challenges facing the Company, the Company extended hours of operations by working in two shifts. This has impacted depreciation to the tune of Rs.134.88 lakhs during the quarter

Obviously we cant compare it YoY due to the company & economy reviving from the Covid impact - labour, social distancing norms etc. will be interesting to hear the commentary from the mgmt.

2 Likes

Hello, i presented on this company at our meet over the weekend.

Link to the presentation:

Please feel free to poke holes and identify any gaps in the thesis. Contemplating investing in this.

10 Likes

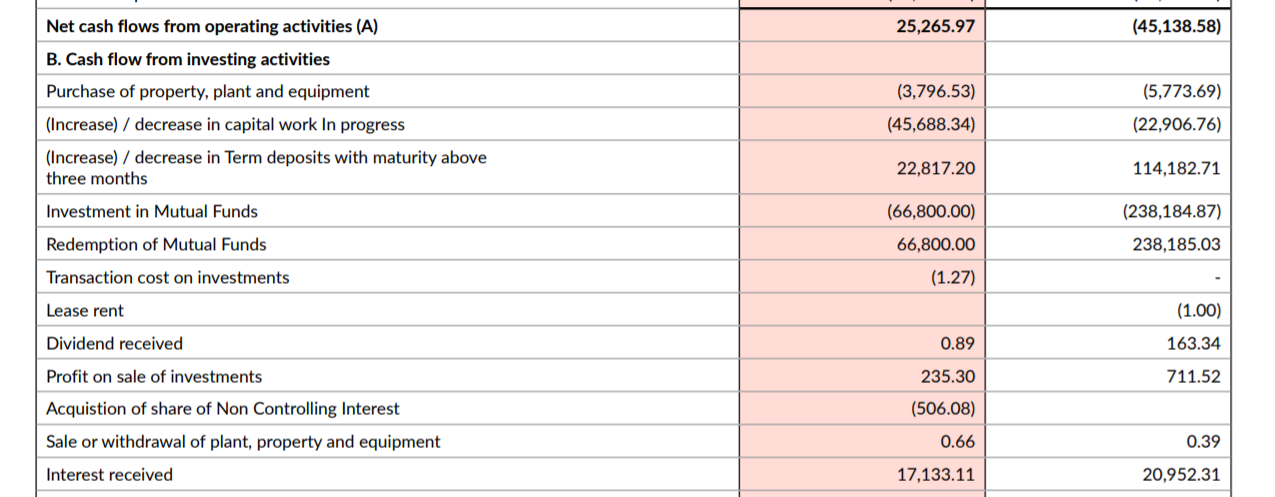

Hi I have a concern regarding the Cash flows generated by the company. Past 3 years the cash flow is -400CR, despite making profits and accruing cash on balance sheet. Is this because of investments in gross block? However even operating cash flows are showing a negative trend for past 2FY.

3 Likes

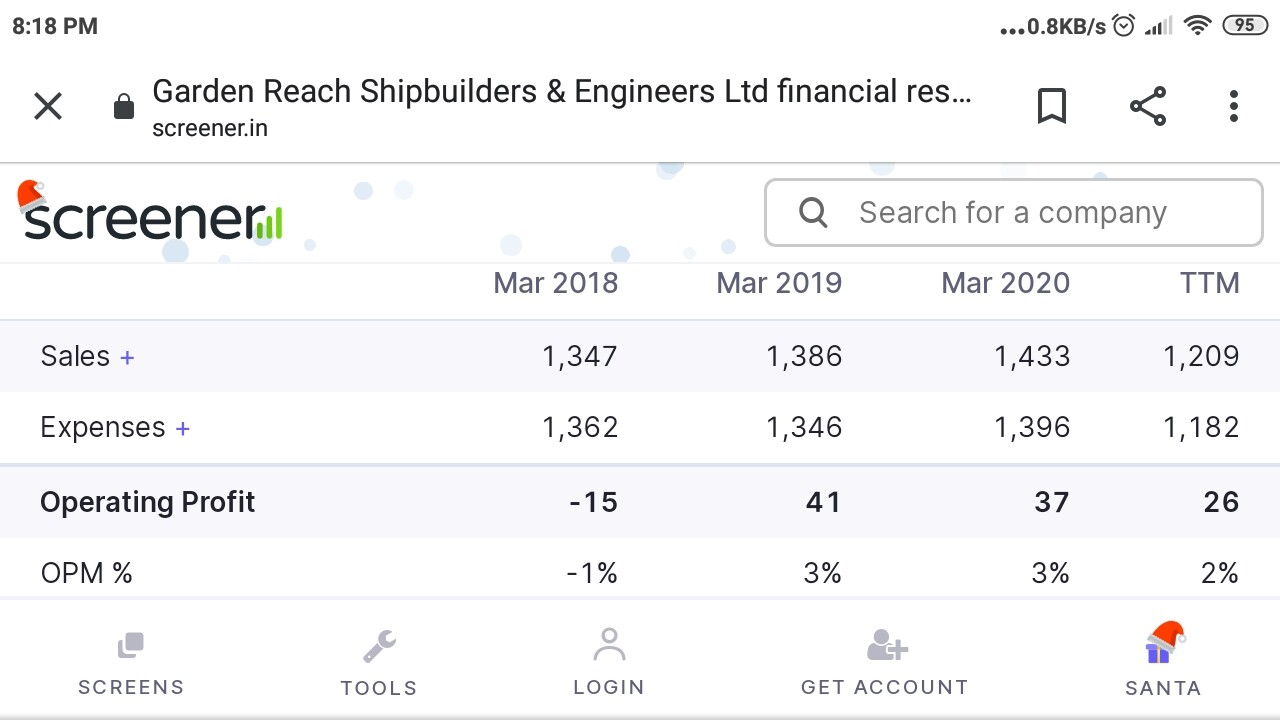

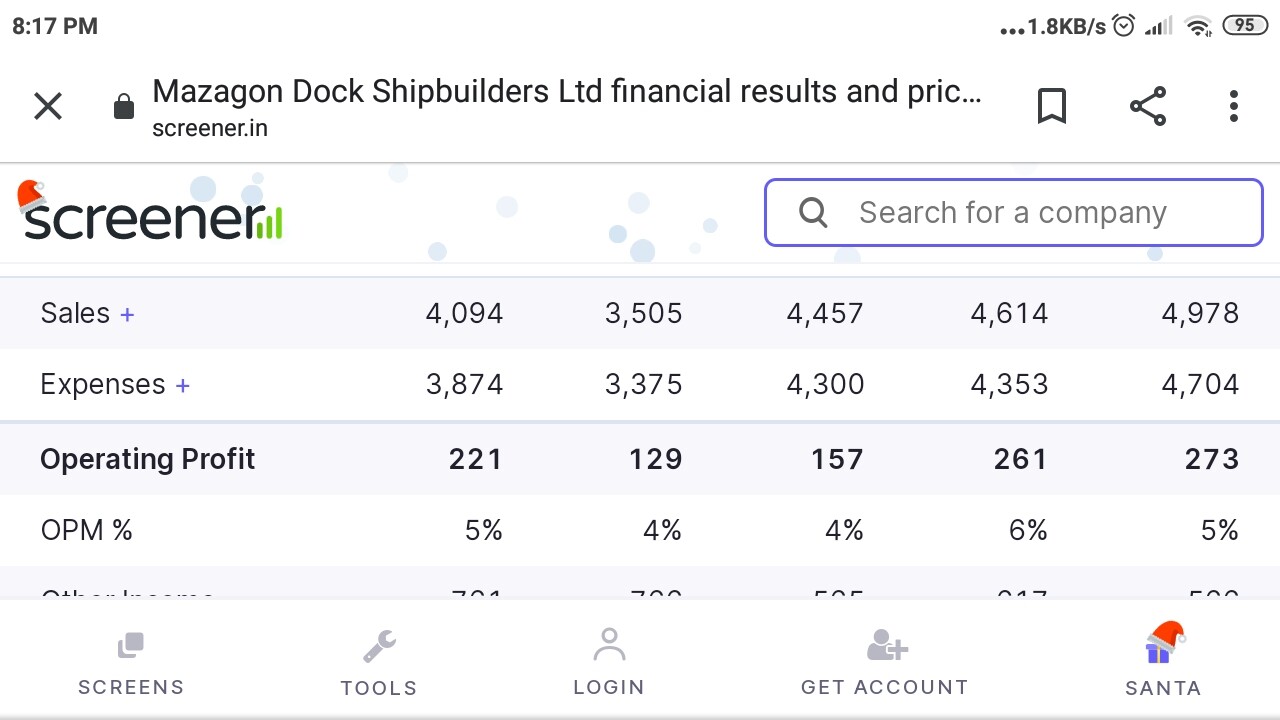

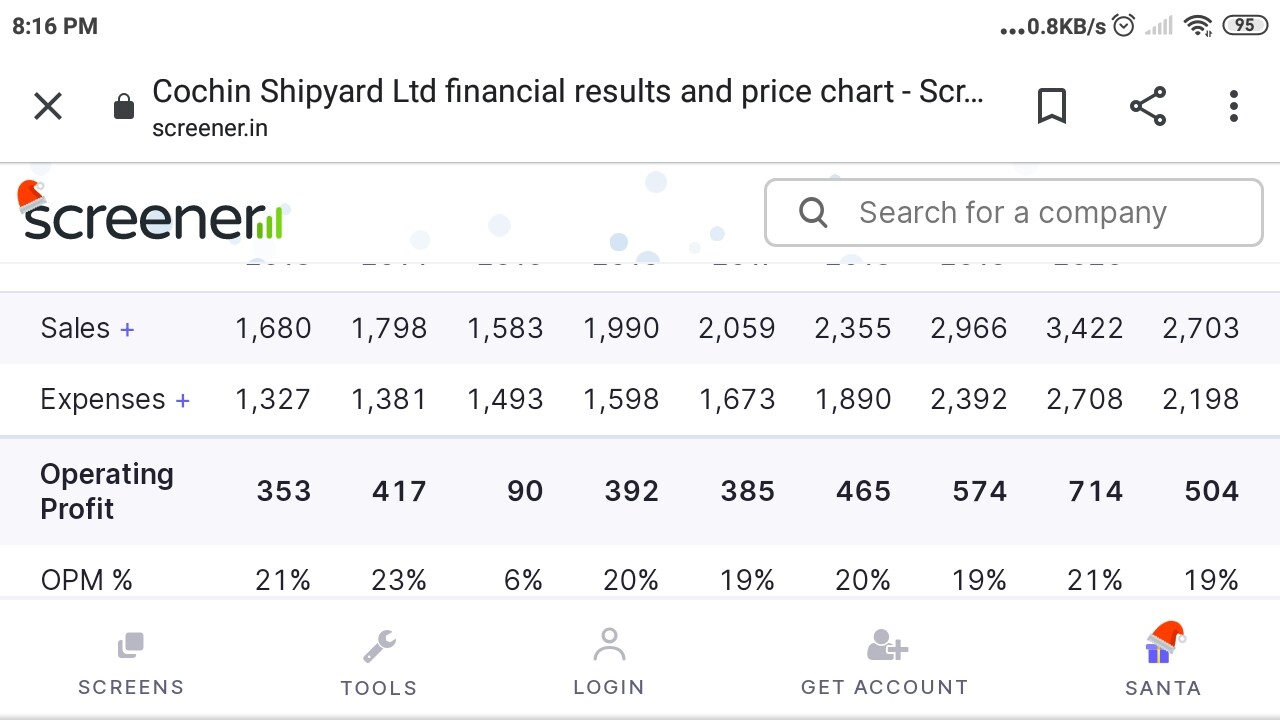

Good Analysis, however, one point that I am not able to understand while comparing Cochin shipyard vs Mazagon vs Garden Reach.

Why operating margins of Cochin Shipyard is way better off (20%) consistantly over others (3-5%) over multiple years.

Can anyone help?

High Margin due to Ship repairing & maintenance works. As far I know, others two players do only ship building works. Cochin Ship yard does both Ship building & Repairing works.

1 Like

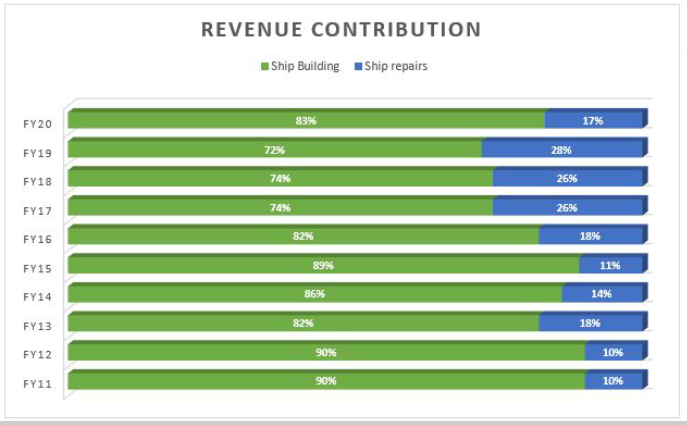

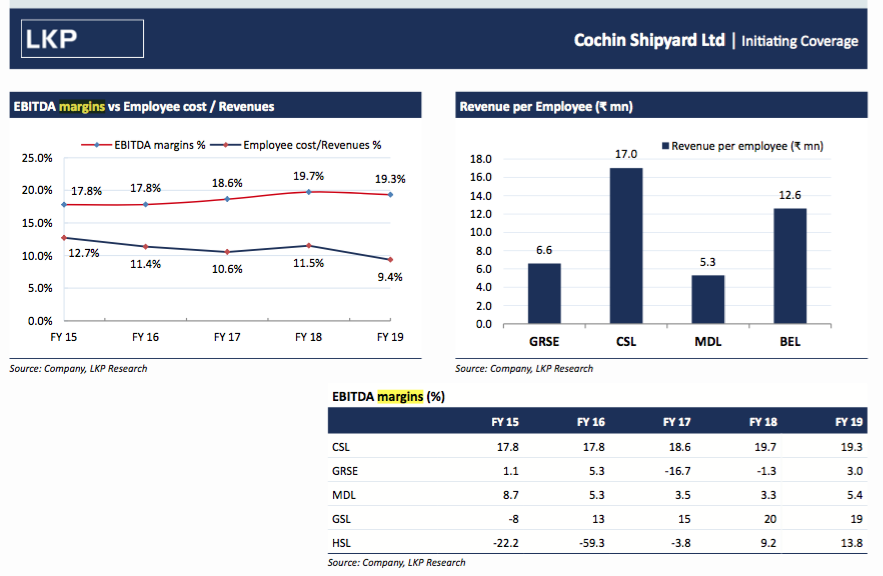

Thanks for the response, however, note that Ship repairing accounts for hardly 20% of revenues (see graph below), and hence it does not look that high margins from ship repairs can move the margins from 4% (which is the average of peers) to 20%.

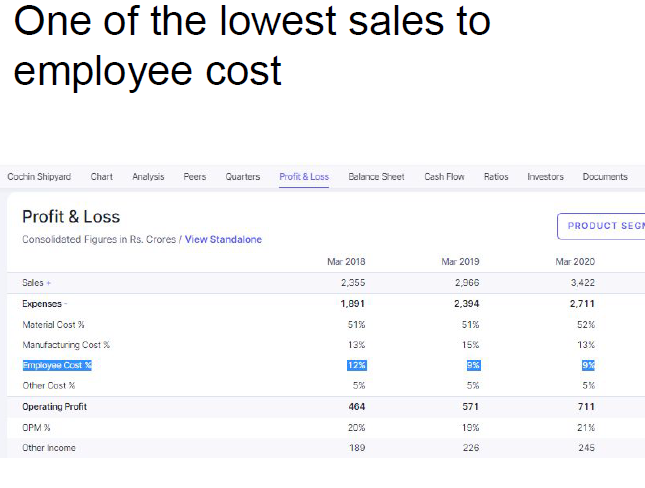

But probably, another reason can be attributed to extremely low employee cost compared to peers. In case, if it is true, the question is , how CSL is able to have low employee cost compared to peers despite being a PSU?

@ganeshrpl Can you throw some light on the reasons of CSL having lowest employee cost compared to peers?

3 Likes

That is right @Amit2saxena - you already pulled that info from the AR.

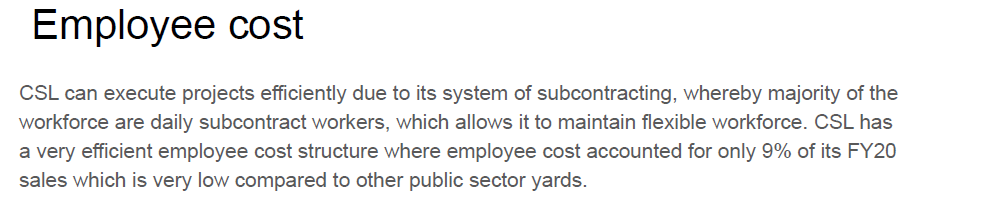

They have the lowest cost in comparison to their peers - which is achieved by the flexible workforce they can hire through sub-contracting. if you dig deeper in to the AR & connect some dots, you would have also noticed that having full-time employees comes with various requirements like pension, maintaining benefits, the satisfying president, government required mandated guidelines like OBC, SC,ST, etc… ( “Cochin Shipyard has been strictly complying with the Presidential directives and guidelines on reservation for Scheduled Caste (SC)/ Scheduled Tribes (ST)/ Other Backward Classes (OBC)/ Economically Weaker Sec ons (EWS) and Persons with Benchmark Disabilities (PwBD) issued by the Government of India from time to time…”)

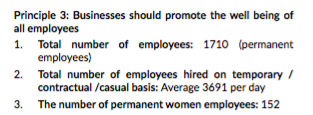

From AR:

Look at the below screen on the avg. temp employees per day!

!

!

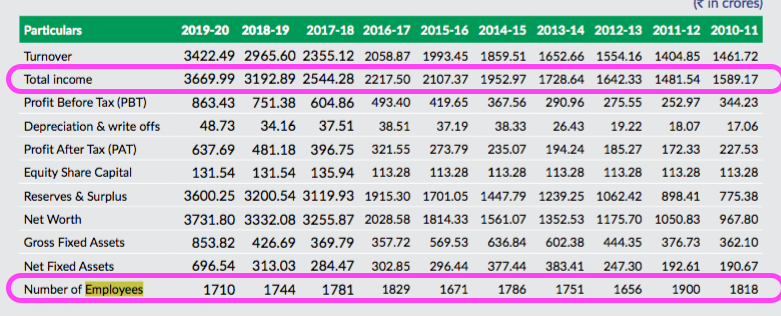

Look at the employee count over the years:

And finally, if you look at the details shared in the LKP report above, they have highlighted similar reasons too on Margins.

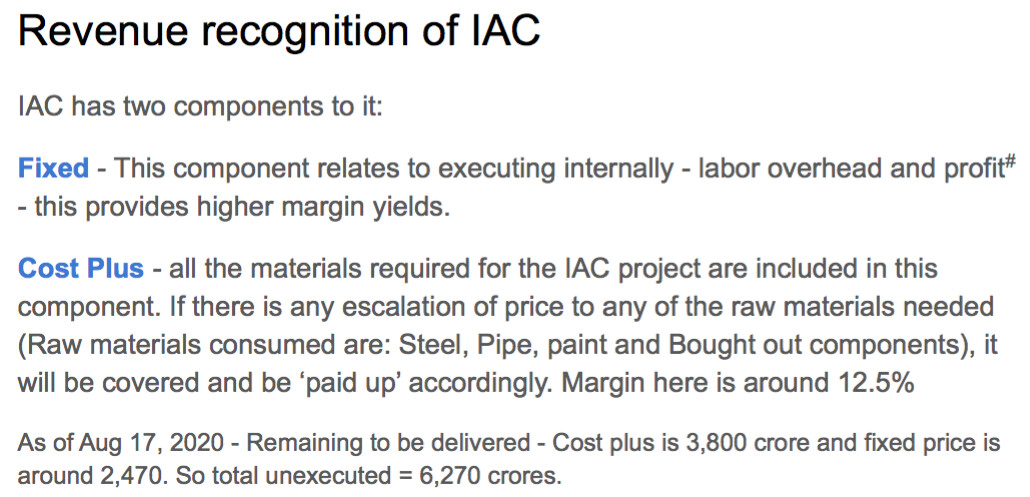

At the end of the day you are right that the ship repair biz is a relatively a smaller portion to the ship building segment - but in the ship building segment for the past few years, the major contributor is the IAC (& will continue to be a for a couple of more years) and this one has a fixed and a cost plus model. the below screens shot is from my slide number 5 in my presentation. so the fixed component helps bring in the higher yields.

They are one of the most efficient players in this industry. Hope this helps.

5 Likes

I would have similar concerns. FCF for 2019 and 2020 were -735 and -605 Cr respectively.

1 Like

CS declared as lowest bidder for construction of six numbers of Next Generation Missile Vessels (NGMV) and the estimated total order value is around Rs 10,000 crore

3 Likes

Why I think this is a 2.7X- 3X opportunity in next 10 years.

CMP INR 349

My hypothesis:

- They have a vision of 6-8x growth in next 10 years. However I assume a more modest 7-8% growth over next 10 years. We should see sales at INR 6200 crores approximately. However, If we see even 3x growth - This is probably a share that can get you 5x returns from the current valuation.

- No orderbook overhang anymore. Orderbook stands at close to INR 23,000 crore.

- Assuming the margins remain constant at 20%. I.e Profit of INR 1240 crores profit. Post tax net profit - INR 920 crore.

- Hence EPS after 10 years - INR 70 approx

Now assuming they pay 40% dividend today i.e INR 15 annually and this grows by 6% annually. We are looking at INR 300 as dividend per share over 10 years (Assuming you make 8% on dividend).

With EPS of INR 70. Stock price even if stays at current valuation has to be INR 665 - INR 700. However ideally it should be higher then this.

INR 665 + INR 300 (Dividend per share) = INR 965 - INR 1000.

Disclosure - Invested

8 Likes