Cochin Shipyard Ltd. (CSL) was incorporated in the year 1972 as a fully owned Government of India

Company. Now Govt holds some 75% share. So assume it is a PSU and will not comment further on management attitude towards minority shareholders

Products & Services:

It builds and repairs ships - Merchant ships, navy ships, off-shore vessels and structures

Building ships - 70% of turnover

Repairing Ships - 30% of turnover

Totally CS has built about 125 ships in its entire history and delivered it to USA, Some european countries and middle-east also.

Current order book:

Vessel Type - Nos

Indigenous Aircraft Carrier for the Indian Navy, P-71 - 01

Technology Demonstration Vessel (Special Purpose Vessel) for DRDO- 01

500 passenger cum 150 MT cargo vessel for A&N Administration - 02

1200 passenger cum 1000 MT cargo vessel for A&N Administration - 02

Tuna Longliner Cum Gil netter Fishing Boat (3 boats delivered) for Tamil Nadu - 16

Ro-Pax vessels for Inland Waterways Authority of India for NW1/ NW2 - 08

Ro-Ro vessels forInland WaterwaysAuthority of India for NW3 - 02

Brows & Pontoons for Indian Navy 02

Marine Ambulance Boat for Kerala Government - 03

Mini Bulk Carrier of 8000 T for Utkarsh

Advisory Services Limited (JSW group) - 04

Floating Border Outpost vessels for Ministry of Home Affairs - 09

Employees are just 1700 (I thought shipbuilding needed lots of people)

Commentary:

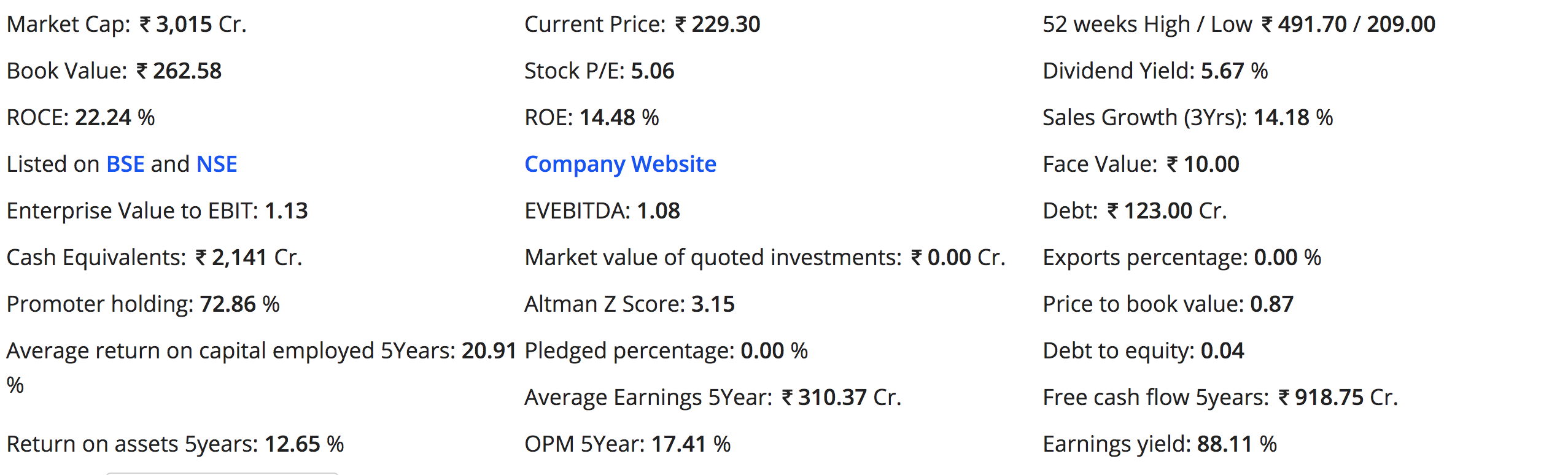

Pros: - Screaming low valuation. EV/EBIT is 1.1 as per screener… => If I am able to buy the company, I will get the entire money back in an year

Is of strategic importance to govt. This is helping the navy. They are building an indigenous aircraft carrier

Has lots of cash and hence will not go bankrupt

Cons:

Don’t really understand the business, competition etc.

I am planning to buy at this valuation primarily as this feels like a heads I win and tails I don’t lose much kind of stock (Dhandho investor philosophy).

Views on stuff not apparent to me at this surface level analysis are welcome. My purpose of posting here before buying is to understand why the market undervalues this so much! What’s the catch? Grateful if anyone knowledgeable on this can throw some light.

Dear @alexander

I would suggest to deep-dive cash flows, receivables and revenue recognition policy. While the stock does look optically cheap and a cash bargain, one of the key risks here could be how much of accounting profits actually translate to the cash.

On the flip side, being a PSU a healthy dividend yield can be expected (as Govt. will demand to fund budget / fiscal deficit).

There doesn’t seem to be any such issue. There is continuously positive free cashflow for last few years. They have 1.5k cr of cash and another 0.6k cr of liquid investments and their market cap is 3.1k cr. Unless their future revenues are impacted by some unknown things not available in any news source, market cap is not making sense to me.

CSL is very cheap indeed - decent growth and profitability, decent order book, expansion plan, no/very low debt, good dividend…PSU promoter is the only negative

Hello respected member… suppose i’m investing in cs for long term… only on thing which main consened that if any kind of big natural disaster come there… like tsunami, earthquake , air cyclone mainly affected most because its total activity near port area… so what kind of security company have… any special insurance policy or other kind of steps which cover its total demage… if it act like silly than ignore it… just thinking before longterm investing…

lot of cash is earmarked for particular projects. its an advance received from Navy etc to complete the project. hence you will have to subtract those funds from Cash. Net of that cash will be close to 500 cr as per my calculation

Agree on the valuation part but issue with these companies is same as EPC companies that quarterly growth is very difficult to predict and order inflows are lumpy. Currently most of the orderbook will be completed by FY23-24. It is bidding for new orders but there is no guarantee it will get new ones. Hence EBIT numbers can move a lot based on year to year. Plus its a PSU and orders are mostly from defence / govt so payments can be hugely delayed.

No need to worry about winning orders in the future - they will surely get preferential treatment from the Govt. >80% orders are from the Govt. They are doubling their shipbuilding capacity and they have taken over the ship-repair business from Mumbai and Kolkata ports. They are nicely poised for growth. Orders are lumpy but QoQ are not so…

Dividend policy is - 30% of net profit or 5% of net worth. Share buy back happened in 2018 - one could expect the same in the future

This company is also on my watchlist for my satellite portfolio. Everything around the core operations, order book and financial position of the company appears relatively solid from a 2-3 year perspective. The company also has an excellent track record since 1972 and never posted losses in all these decades. Also with the corporate tax cut - I think this is almost at 7% div yield now.

However, the tag of “PSU” can haunt investors in this. There is literally no end to how much lower PSUs can go! Keeping this in mind, I’d not advise betting big on such companies.

Interestingly the Q4FY20 shareholding pattern reveals government divestment of 2-2.5%. Not sure if there is any further planned divestments.

Disc: Not invested - planning to take small position around 200

Thanks @ajay81. Can you please point me to the source of this info.

But isn’t cash = cash? What I mean is they might have plans for that cash which is other than distributing to shareholders. But hopefully this cash also will be invested at a decent ROE of 15% as has been done historically => PE ratio will come down further from 5 to around 3. Also if they continue giving 30% dividend this translates to over 10% dividend yield.

I think defence business which contributes to > 80% of revenues is stable. Govt allocates money every year to Navy as part of the defence budget and has focus on Make in India which limits its options. (Shipbuilding is people heavy, so govt. will not outsource easily. Apart from 1700 FTE, CSL employs over 3k contractors to take care of demand fluctuations)

Apparently the repairing business has higher margins and hence they are expanding capacity for repairing ships. So, if things go well we can expect better margins & ROE in future.

Above report states

“CSL is undertaking capex for developing an International Ship Repair Facility (ISRF) at Cochin Port Trust at an estimated cost of Rs.750 crore. Additionally, CSL plans to augment the capacity by building a dry-dock in its premises at an estimated cost of around Rs.1,600 crore. At present, entire capex is proposed to be funded through internal accruals and using surplus funds present in the form of free cash and bank balance. Timely completion of the above two projects within estimated cost while maintaining comfortable capital structure is critical.”

Any excess from the estimate will have to be funded by taking debt or diluting equity.

Another problem is that whenever the price will rise, government will reduce its stake. This will lead to oversupply and put strain on stock price.

Growth rate is highest among peers but poor in comparison to other industries. The industry has history of wealth destruction.

Neither do I. This should be enough for me to avoid it. Invest if you have strong conviction. If everything goes as planned value stocks can give multibagger returns.

This is a technical issue that may or may not affect price in the short to medium term and never to be treated as a reason while analyzing a company fundamentally for long term. In fact, if price is going to come down only due to such govt stake sale reason and not based on fundamentals, then it should be positively considered as a buying oppurtunity which is not available in MNCs.

I am holding this share from the time of IPO . Very good dividend yield , healthy order book, CSL took over ports in kolkata, andaman , mumbai and currently modernizing them for ship building and repairing. Construction of ISRF and new dry dock expected to get completed

by mid-2022

Drawbacks

Recently CSL is added to CPSE ETF which was a big negative . Every time they come out with the offering , PSU’s share price took a hit

A theft was reported in under constructing aircraft carrier and it was that hard drives contain sensitive information were stolen . These incidents certainly questions CSL credibility

Defense budget will be reduced due to covid -19 . Need to see if construction of second aircraft carrier will be delayed . Also tendering for new vessels , navy boats etc might get delayed

hi, I’ve been invested in this firm for >2 years now. In the current environment there are 2 negatives going for it.

Budgetary resources from the country (its biggest customer) will be diverted to health care

being a defence stock - ESG philosophy driven FII funds no longer favor defence/sin stocks.

Given that Returns in Equity are driven by Div Yield + PE re-rating, there’s only dividends in favor of this stock.

Quote from the article

“So why are PSU stocks serial underperformers? The usual answers to relatively weaker financial fundamentals of PSUs include ‘public sector inefficiency’ or ‘constraints of working under the 3 Cs – CAG, CVC and Courts’. A key reason, however, is that as minority shareholders, investors play on an uneven field with the government on the other side as a dominant shareholder as also as a customer of these PSUs. This duality of the government’s role puts at risk the efficient use of capital by PSUs, as well as the longevity of their earnings, which then reflect in the low multiples.”

As a minority shareholder it will be good if the promoter and our goals are same. These things should be taken into consideration while deciding on long term investment. It will increase conviction and one will be able to hold the position longer.

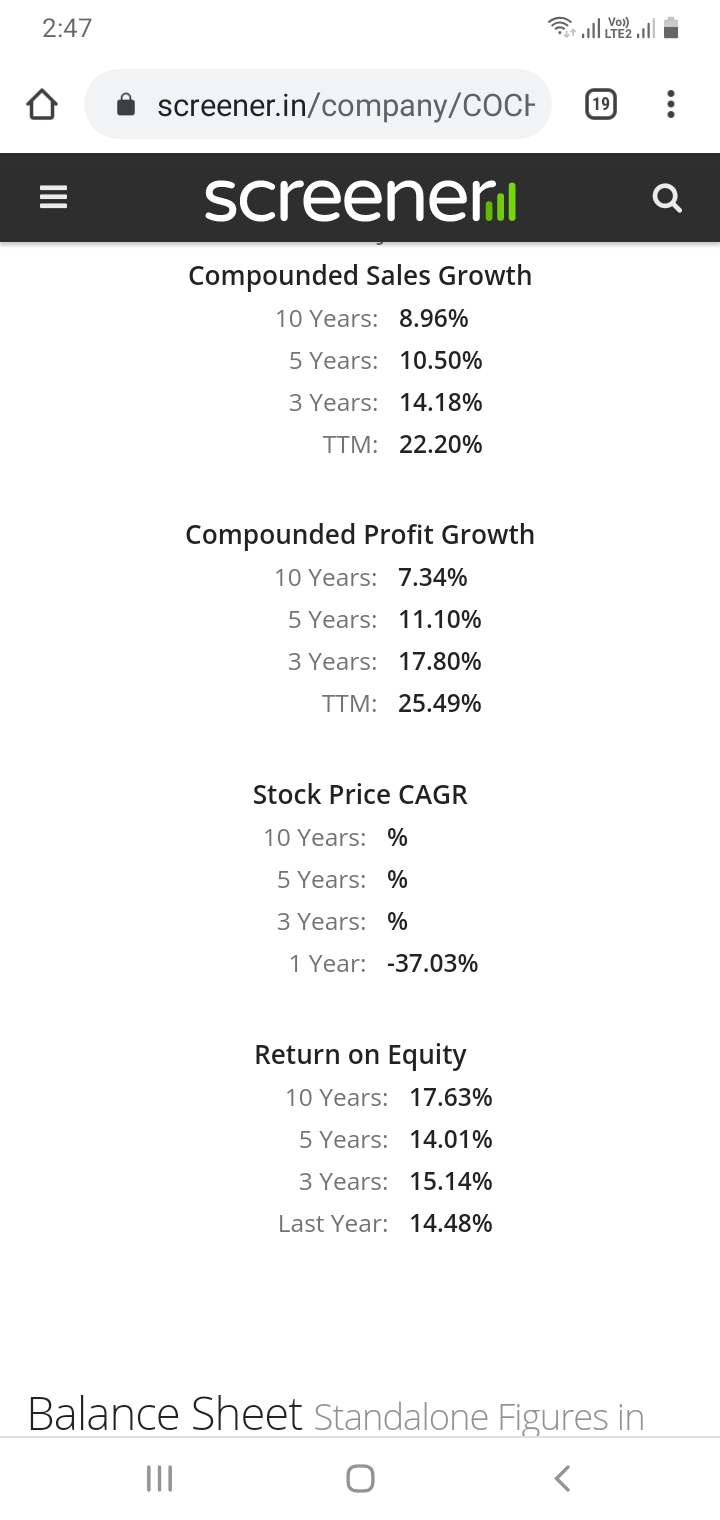

9% sales growth and 7.5% profit growth over 10 years for a stock valued at 5 PE is ok I think.

At 5 PE, if the company doesn’t grow significantly but just survives for say 15-20 years and promises to deliver similar profits till then, ideally the value of the company should become 3-4x easily (including dividends). This will be irrespective of the market sentiment as the company will generate that much cash only. [Doubling every 5 years is 15% CAGR which is pretty decent]

You don’t need marcellus to disprove efficient market hypothesis. The fact that they exist and we are also trying to beat the index is also because we don’t believe in efficient markets (Voting machine v Weighing machine analogy from Graham).

On an unrelated point, I think Marcellus will burn their fingers in the next 10 -15 years. Forgetting valuations shouldn’t work. Let’s see…

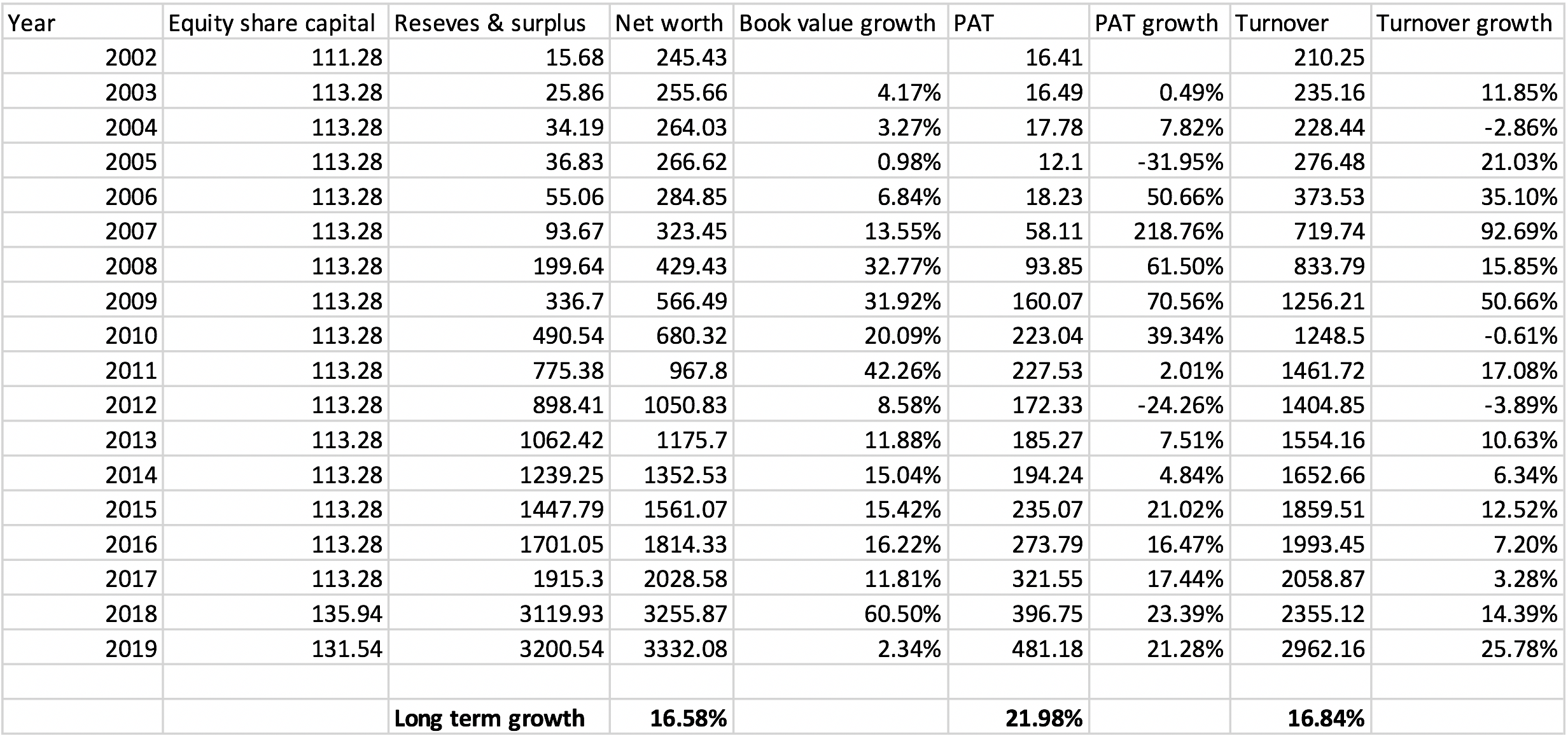

There are few business which have delivered these kind of numbers. However, this is historical. Since listing, they have returned:

FY18: Paid dividend of 180 cr.

FY19: Paid dividend of 200 cr. + buyback of 200 cr.

Given that the company is giving back half its profits as dividends and reinvesting the other half (expanding into Kolkata, Mumbai, Andaman, etc. + new dry dock + new ship repair facility), this business should be valued at a premium to its book. A P/E of 5 implies a P/B of 0.75 which does not make a lot of sense.