Yes, quite a move yesterday and a decent follow-up today too. I am not a technical trader and primarily look at price-volume action to just understand what others think. While the results were good, it was not so crazy good either. I think the key thing is to do with their business model which is not the same as most retail-focused banks. I can’t say for sure, but in the current environment, this feels like a bit of a flight to safety move as well.

2 Likes

9b4374c7-9f3f-46a1-994c-887193bfbdd8.pdf (2.5 MB)

Latest CUB results. Good results but in my opinion DCB Bank performed much better in comparison to CUB. On asset quality, gross and net NPA decreases Q/Q and Y/Y basis. Why still provisions increased is yet to understand? Bank grew its business almost by 12 % when GDP is languishing on approx 6%.

Holding both CUB and DCB. Yet to hear concall which will give more clarity.

1 Like

Missed Mr. Kamakodi in the conf call (until the end) who generally gives a good qualitative view as well to questions, but Mr. Vijay Anandh covered well and was on top of the numbers!

Overall, pretty good across the board - quite a well run bank indeed. I just wish they are a bit more ambitious on their growth. While the growth numbers are good, their strong operational focus in running a tight ship and keeping slippages down seems to constrain higher growth. Maybe secured retail can boost the growth a bit more, but they are very careful to under-promise there. Let’s see if they can over-deliver on that. It was also good to hear that the MSME book is not seeing stress as things stand. Beyond the implications for the bank, it’s a good sign for the economy too.

Don’t know how the stock will do going forward, but the bank is doing quite well, and relative to most other banks, much better too.

7 Likes

Lots of new branches being opened this quarter, and interestingly, most of them outside Tamil Nadu. This one https://www.bseindia.com/xml-data/corpfiling/AttachLive/0504bc59-8b74-4176-8df7-4be5b8e95ad3.pdf is just the latest in a sequence of half a dozen disclosures on branch openings that I have come across in the last couple of months. Good to see the expansion though I guess it may also have an impact on the cost-to-income ratio in Q4. Not sure what the pace of branch openings was in previous quarters, but it seems to have accelerated.

4 Likes

The branch expansion continues - saw two more circulars in the last two days! Also, a good and short Q&A with the CEO https://www.youtube.com/watch?v=brfhPrXs1hA.

Positive about growth though still sticking to the 14-15% target. He remains cautious about unsecured (CUB’s unsecured portfolio is less than 1%) though they have tied up with CSK and SRH for co-branded credit cards.

3 Likes

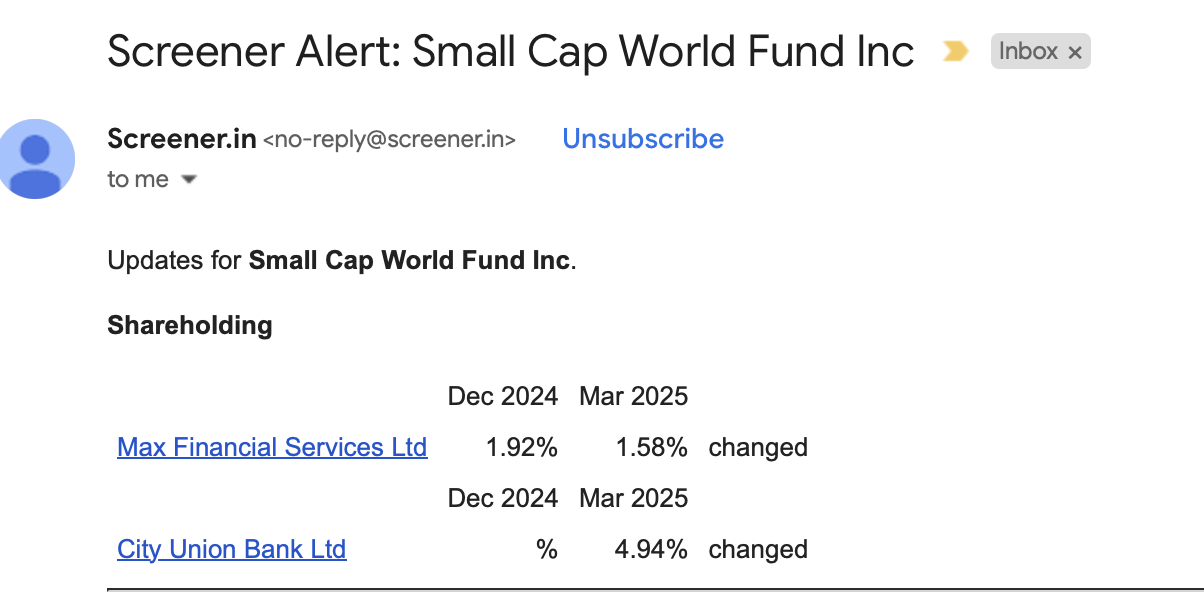

The CUB holding is not a fresh entry - they have held it for a long time and it’s at the same level for the last couple of years.

Ohh yes i just verified on screener, any idea why it is showing nothing in previous quarter.

For March 2024 and Dec 2024.

No idea, maybe some reporting issue. I have recently seen a couple of stocks (e.g. Everest Industries Ltd) that show 100% delivery on NSE everyday though it’s not the case. Even sent them an email about it, but didn’t hear back.

Pretty solid results again with NIM holding firm and asset quality in good shape as well. Strong deposit growth was the highlight for this quarter and loan growth was good too. Also indicated that loan against property (LAP) is growing well in the retail portfolio (95% secured). While retail growth is still to take off, should contribute more next year - indicated 3-4% of loan book in FY26. Other income also grew strongly, driven by commissions on various products, insurance primarily (I think). Overall, it’s been a strong year for the bank. The market’s not rewarded it as well as I had hoped, but so long as geopolitics and tariffs don’t throw a spanner in the works, FY26 should be as good or even better. Management commentary was positive, though as always, they are cautious in what they promise.

Investor presentation here - https://www.cityunionbank.com/filemanager/May25/CUB_Investor_Presentation_Mar2025.pdf

3 Likes

Good read - EA Sundaram on City Union Bank

BR Core Value Newsletter May 2025.pdf (770.9 KB)

5 Likes

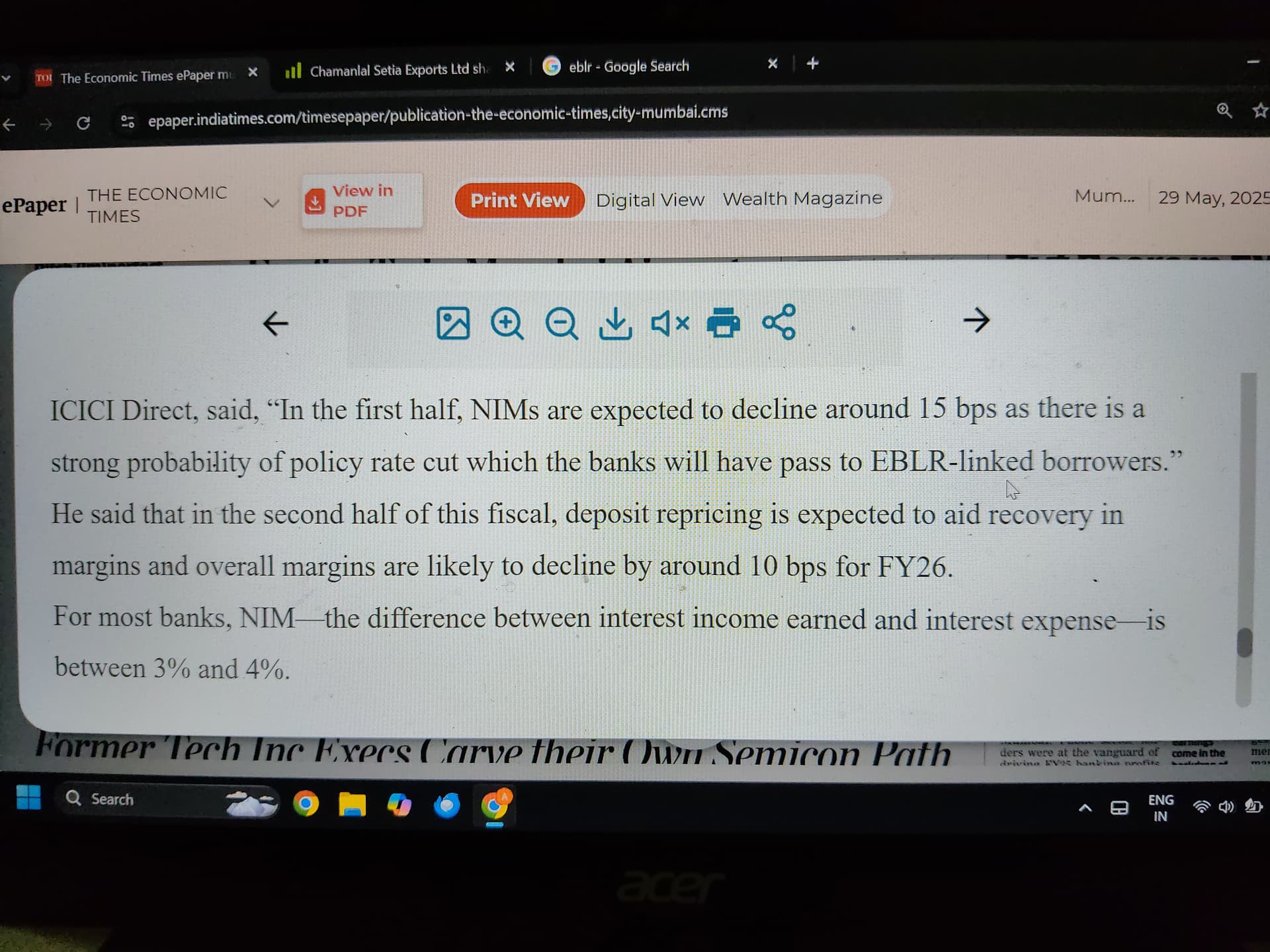

NIMs are important, but only one piece of the puzzle. There are other factors that are just as important, if not more - growth metrics, asset quality, RoA, CASA share among others. We have to look at it holistically. Also, how the prospects of each bank stack up relatively as well, for the coming 6-12 months.

CUB has done well, close to the Rs.200 I was expecting. I don’t know whether it will rise more or fall again to slightly lower levels, but fundamentally, the business is doing fine at present.

3 Likes

Impressive Q1 results, and even more so, in the context of the sub-par results reported by almost all banks. Earnings call link here - https://www.bseindia.com/xml-data/corpfiling/AttachLive/0dd71c05-c557-4aa7-a903-f7ed98ce6910.pdf

A beat on almost all dimensions, really. Advances growth, deposits growth, asset quality, RoA. NIMs reduced just marginally though Q2 NIMs will reduce a bit more given the deposit rate reductions only come into effect towards the end of Q2. Amazing to hear the management say that their portfolio hasn’t seen any stress so far with SMA-1,2 etc. not deteriorating. This is contrary to literally every other lender’s commentary. There is an RBI audit going on - hopefully, that doesn’t uncover some issue. I don’t expect it will, but never know.

Retail loan book’s picked up nicely - 825 crores now, almost all of it secured. On track to the 3,000 crore number for the full-year that they were targeting.

Trustworthy management - ears to the ground, conservative bankers. A rare breed these days.

14 Likes

Q2 results once again highlight CUB’s consistent performance. A great defensive bet over the last two years, yet little has happened in terms of rerating.

In the past, CUB would trade at 2.5–3x Book Value with these fundamentals — 15% PAT growth, 20% deposit and advances growth, 14% ROE, and sub-1% net NPA. Even if it gets halfway there, that would get the stock to ~300.

3 Likes

Another fantastic quarter. A beat, or at least, “met expectations” on every dimension. Even their NIMs surprisingly went up marginally, which I was not expecting. I was hoping for some question on the IFC $50M loan for green finance to MSMEs. I expect that’s at a favourable rate of interest and should help accelerate the growth in their loan book a little bit. The most positive takeaway from the earnings call is that they are not seeing their customers facing much stress due to the tariffs. I am not 100% convinced about this, it’s possible some of that impact may show up next quarter, but their book of business in that segment is not so high (at least rather lower than I had initially thought). Also, a pleasant surprise to hear that recoveries will continue to be more than slippages for another quarter or two.

It’s like they are batting on a different wicket compared to nearly all other banks. It’s a bit of a bear market right now, so hard to say how the stock will perform, but business fundamentals certainly remain solid.

A sudden spurt in branch openings over the last month, and many outside TN too. Post the all-time highs that the stock hit after another excellent quarter (Q3), it’s corrected over 20-25%, falling over 30% at one point. Will be interesting to see their Q4 numbers, particularly provisions. While Q1 FY27 will see more of the impact of the Iran war, it’s not clear to me which parts of the economy are being hit the most. I suspect that CUB, being a conservative bank, may frontload provisions partially in Q4 itself.

2 Likes

More a hundred branches since April 2025 (less than 13 months). CUB usually starts off with five people per branch (one BM, along with RMs and associates). How sustainable is this? CI ratio in for a spike over the next few quarters?

They have mentioned this in the past. It is intentional expansion. Cost-to-income ratio has already been higher than average for a few quarters. Q3 was a bit of a blip as they didn’t open as many branches. Given their intent to expand secured retail and expand a bit more outside TN to reduce geographic concentration, it’s required. Will have to wait and watch how it plays out over time. Near-term impact of higher costs I am not that concerned about, the issue is broader economy. No matter how well run a bank is, if there is a breakdown in key parts of the economy, inevitable that it will be affected. The longer this war goes on, the greater the chances for such problems.

2 Likes

7 more branch openings - up to 987 now. I get the feeling Mr. Kamakodi wants to end his tenure with 1000 branches, which is why they have upped the pace of branch openings. ![]()

Update: Just noticed Q4 results are out. Another solid quarter on most dimensions though corporate/wholesale book seems weak. Not sure about the reasons - have to wait for investor presentation/earnings call for some clarity on that. Maybe war impact on working capital loans or something else. Provisions went up (expected), but the good news is that GNPA and Net NPA continued to decline. I thought that might inch up a bit. Bonus issue declared too - wasn’t expecting that. Lowers tax outgo for long-term holders.