It’s been a wonderful learning experience in the 3 months since the last update.

- Lesson - All sectors, even seemingly secular stories, have components that are cyclical, and the turns of these cycles harm/benefit different players within the industry. In some cases, it’s harder to know when head/tailwinds are structural, and when they’re temporary. Even after knowing that US generics companies have no pricing power, I invested in Strides, believing that their pipeline would be enough to stay on the treadmill, and we’d have clarity on the Stelis demerger. Management were confident of meeting their targets, but as @gurjota has recently written about, guidance given by these companies have been revised/withdrawn almost immediately.

-

Diversification across sectors doesn’t guarantee that cyclicity will be averaged over. Example: raw material inflation (temporary or otherwise) has impacted multiple sectors in Q2. Diversification then should be between those that are harmed from raw material inflation, and those that benefit / can still deliver in these conditions.

-

I’m now amending my allocation framework and weighting conviction by my own projections for forward numbers. These are based on management guidance/ industry landscape and I try to assign probabilities for scenarios. Following on from 1), well executed diversification shouldn’t see multiple portfolio companies turn bearish or lower base case probability from the same headwinds.

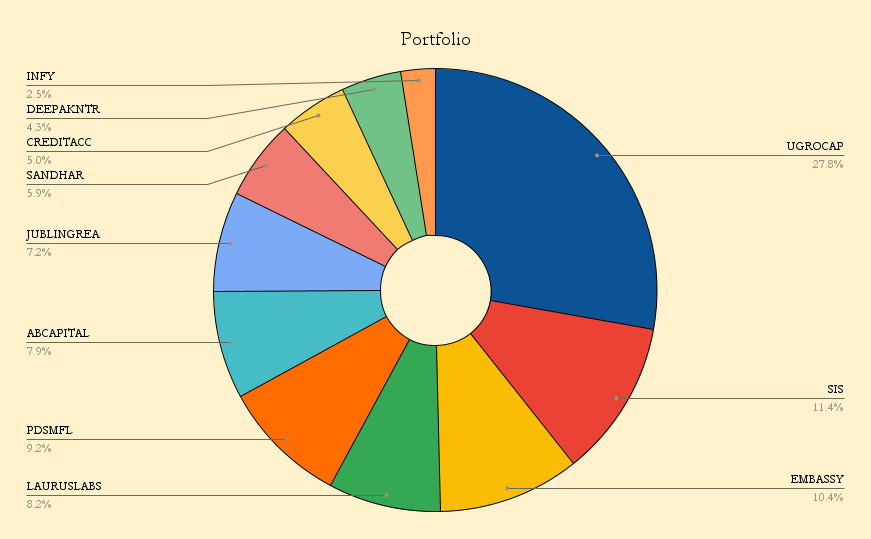

Current Portfolio

I have reduced the number of companies from 15 to 11.

-

Sold Tata Power for two reasons: 1) forward multiples are quite expensive, market is pricing in a lot of growth. 2) after deploying cash, position size fell to around 2.5%. Returns from the first tranche were 4.48x.

-

Sold Trent for similar reasons, and I’m finding it difficult to gauge value in companies that are given premium multiples. Companies like Astral, Trent, BajFin, Aavas fall into this basket, and this is something I’m going to work on for the next year.

-

Sold Caplin Point as there are two theses: 1) they’re incredibly small fish, going after molecules other people won’t want to compete in; 2) they’re doing this to generate cash, building stronger businesses over time. With their aim of entering the US markets, I’m not confident in projecting their margins at 30%.

-

Sold RPSG Ventures. The only time we’ll get a detailed view of the subsidiaries is during the annual report. For a company of this size, would prefer concalls or detailed disclosures quarterly. Still on my watchlist and will pick it up if the holding company discount to FSL widens.

-

Ugro has the highest earnings potential in my coverage universe, and after the last two concalls, I’m very confident of them being able to scale successfully. The monthly updates from the business helps tremendously in following execution.This is reflected in the allocations, and I’m happy to continue buying more.

-

I’m lucky that despite being punished in Strides, it’s come after a relentless run, where the position in Strides was built out of profits in the first place, and my portfolio was up over 100% in the last year. (I’m sure everyone has seen similar returns during this run) Lesson learnt on how quickly a cycle can turn. The US generics business has hit the bottom, I don’t think there’s much downside from here, but it’s hard to predict upside since management has pushed guidance, and other companies should outperform. Will wait for concrete news on the demerger.

-

Still have a small tracking position in Sequent, will revisit the basket of pharma companies when I find time.

Want to thank everyone at this forum for constantly sharing their domain expertise, and their own frameworks, especially @harsh.beria93, @gurjota, @OmkarT and @Investor_No_1 . (There are so many more to name)