About Chatha Foods Limited

(Ref:chittorgarh.com)

Incorporated in 1997, Chatha Foods Limited (CFL) is a frozen food processor. The company offers frozen food products to top QSRs (Quick Serving Restaurants), CDRs (Casual Dining Restaurants), and other players in the HoReCa (Hotel-Restaurant-Catering) segment. Chatha Foods’ product portfolio includes Chicken Appetizers, Meat Patties, Chicken Sausages, Sliced Meat, Toppings & Fillers and more. The company produces more than 70 meat products.

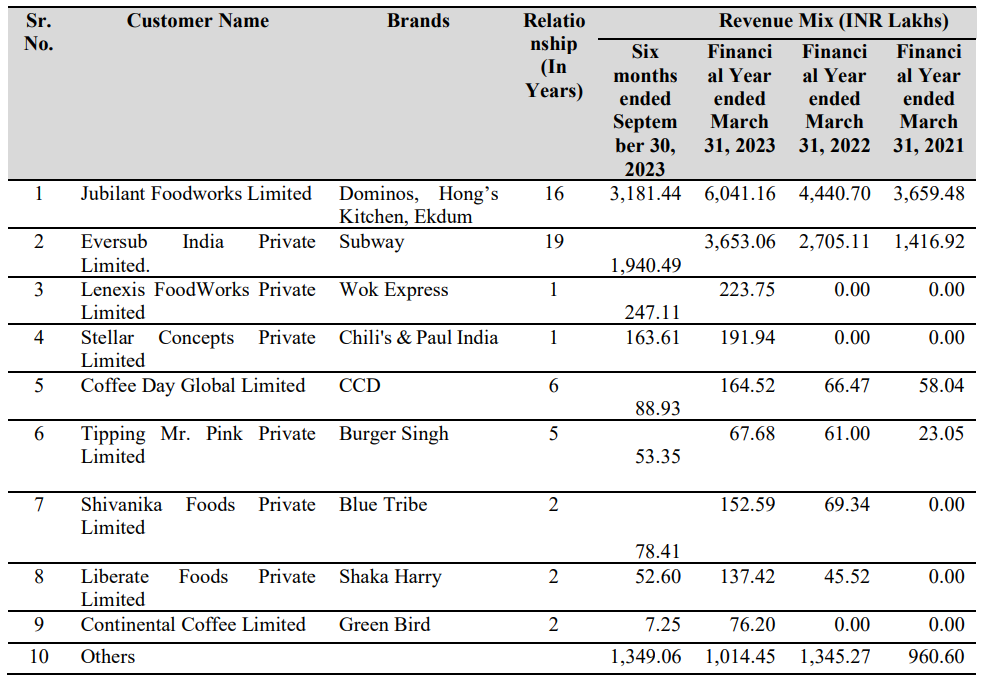

The company sells products under the brand Chatha Foods and distributes through the network of 29 distributors covering 32 cities across India and catering to the needs of 126 mid-segment & standalone small QSR brands.

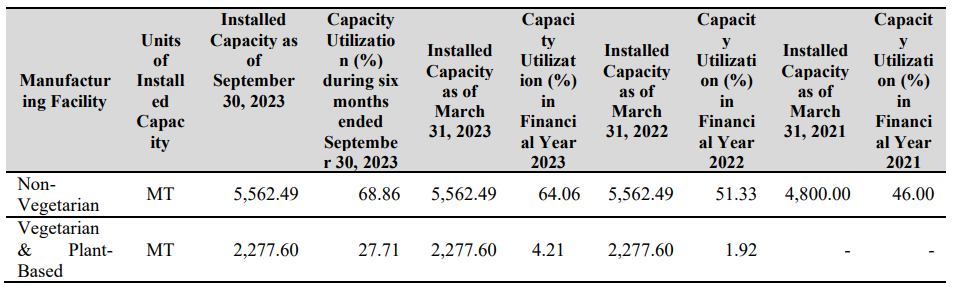

Chatha Foods Limited has a Manufacturing Facility, located in District Mohali, with a production capacity of approximately 7,839 MT for all the frozen food products.

The company is serving top QSRs, CDRs and other players in the Hotel-Restaurant-Catering segment like Domino’s & Subway’s India franchise, Café Coffee Day, Wok Express, etc.

The company does not have any subsidiaries or any Group Companies.

Big Investments

- Negen Undiscovered Value Fund → ~10.43%

- Persistent Growth Fund-Varsu India Growth Story Scheme 1 → ~3.65%

- Aurum Sme Trust → ~1.73%

Financial Information

Figures in Rs. Crores

| Mar 2019 | Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | |

|---|---|---|---|---|---|

| Sales + | 91 | 85 | 61 | 87 | 117 |

| Expenses + | 81 | 80 | 63 | 83 | 110 |

| Operating Profit | 10 | 5 | -2 | 5 | 7 |

| OPM % | 11% | 6% | -3% | 5% | 6% |

| Other Income + | -0 | -0 | 0 | -0 | -0 |

| Interest | 2 | 2 | 1 | 1 | 1 |

| Depreciation | 2 | 2 | 3 | 3 | 3 |

| Profit before tax | 6 | 1 | -6 | 1 | 3 |

| Tax % | 29% | 27% | 27% | 36% | 27% |

| Net Profit + | 4 | 1 | -4 | 1 | 2 |

| EPS in Rs | 3.50 | 0.83 | -3.23 | 0.54 | 1.98 |

| Dividend Payout % | 0% | 0% | 0% | 0% | 0% |

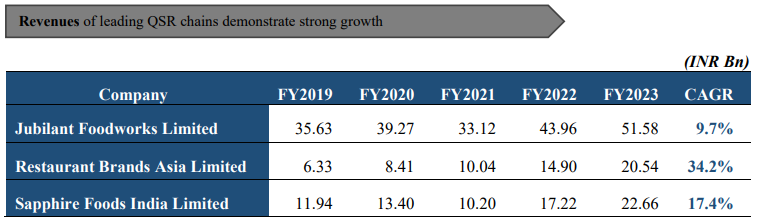

Industry and Competition (Ref: Chatha Foods RHP)

Market overview

The global QSR market was valued at INR 25.05 Trn in FY 2022. It is expected to reach INR 54.53 Trn by FY 2027, expanding at a CAGR of ~17.41% during the FY 2023 ─ FY 2027 forecast period. The requirement for a wide variety of fast-food items and the growth of the market both contribute to the quick-service restaurants market’s expansion globally. The QSR market in India was valued at INR 171.90 Bn in FY 2022. It is expected to reach INR 431.27 Bn in FY 2027, expanding at a CAGR of ~20.47% during the FY 2022 ─ FY 2027 forecast period. The current decade is overseeing a shift to a larger organized sector. Customer retention and a higher range and depth of offerings are new goals among the organized market players of QSR.

QSR Market in India

• The QSR market in India was valued at INR 171.90 Bn in FY 2022. It is expected to reach INR 431.27 Bn in FY 2027, expanding at a CAGR of ~20.47% during the FY 2022 ─ FY 2027 forecast period.

Major quick food-service chains, such as McDonald’s, Burger King, and Domino’s, among others, are

deepening their reach in India’s smaller cities and benefiting from a younger demography, thereby further aiding the growth of the market.

• The QSR segment will see its next big growth come from consumers in tier II and tier III cities. Annual spends on eating out at QSR chains in non-metros are expected to surge 150% to INR 3,750/- per household over the next three years.

Competition

Our industry comprises of both organized and unorganized players, therefore we face competition from both small players who belongs to unorganized sector and big players who have better resources availability.

Promoters

Promoters are Paramjit Singh Chatha, Gurcharan Singh Gosal, Gurpreet Chatha and Anmoldeep Singh.

Paramjit Singh Chatha aged 55 years, the Chairman and Managing Director of the Company and a member of the Promoter Category, has founded the Company. He was appointed the Managing Director of our Company, w.e.f. April 01, 1998. He has been actively involved in business planning, strategy development and expansion activities since the inception of our Company. He has an experience of 25 years and has been instrumental in expanding the operations of our Company. His leadership has contributed to the growth of our business and the establishment of long term relationships with our customers. As the Managing Director, Paramjit Singh Chatha is responsible for

developing and maintaining the company’s vision, mission statement, and strategic plan. He reviews financial statements and other reports to evaluate the Company’s performance. Furthermore, he identifies new opportunities for revenue growth, such as the introduction of new products, new customers and new businesses. He effectively communicates with employees to ensure they understand the Company’s goals, objectives, and policies.

Additionally, he evaluates new technologies and business practices to assess their potential impact on the Company’s operations and effective marketing strategy to promote the products offered by the Company.

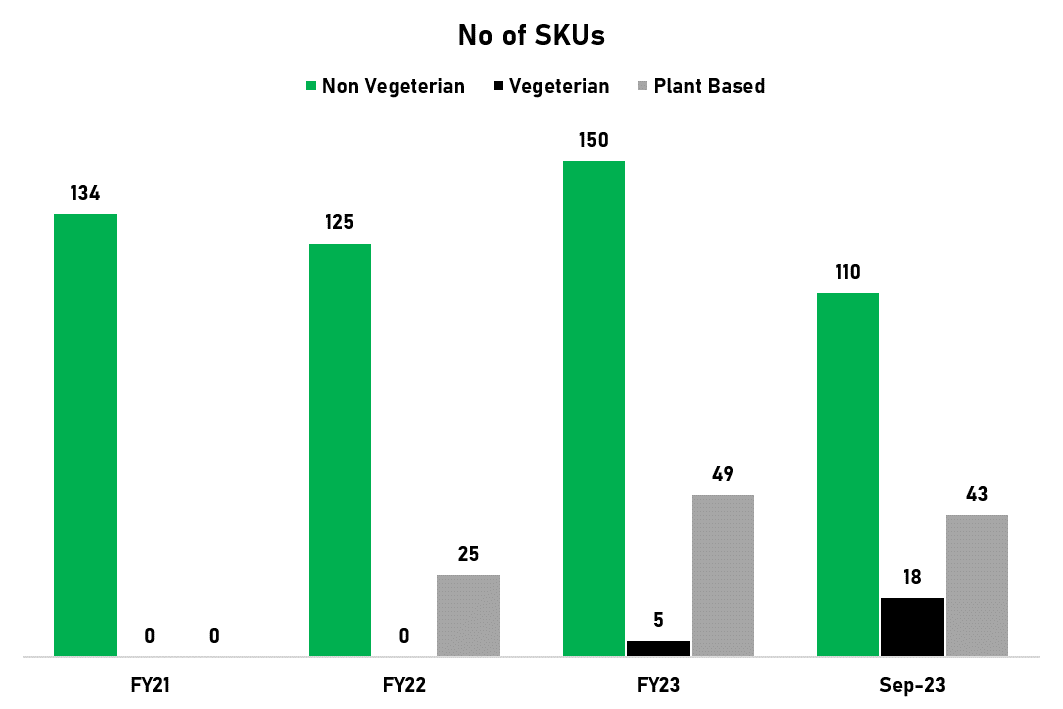

Product Categories

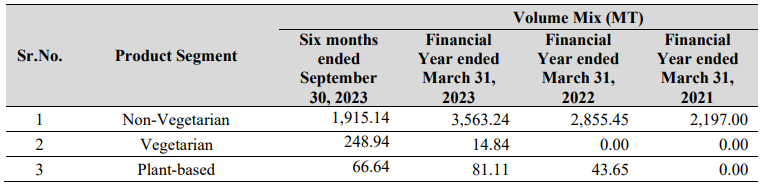

(a) Non-Vegetarian: We manufacture and sell non-vegetarian products such as pizza toppings, sandwich fillings, burger patties, snacks and more to leading QSR’s, CDR’s and other HoReCa segment players.

(b) Vegetarian: We manufacture and sell vegetarian products such as pizza toppings, sandwich fillings, burger patties, taco fillings to leading QSR’s, CDR’s and other HoReCa segment players. We ventured into vegetarian products in the year 2022.

(c) Plant-Based: We manufacture and sell plant-based products such as plant-based sausages, salami, pepperoni; Indian snacks like kebabs, tikkas & samosas; plant-based nuggets & burger patties, grilled burger patties to certain QSRs, CDRs and other HoReCa segment players. Additionally, we supply our products to larger conglomerates and other companies under their own brand names, including Bluetribe (Alkem Group), Shaka Harry (Liberate Foods), Green Bird (Continental Coffee), Plantaway (Graviss Group), and many others. We ventured into plant-based mock meat products in the year 2021.

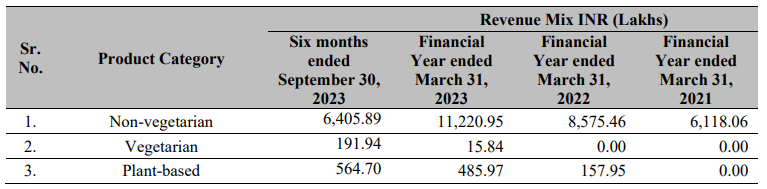

Revenue Mix

Volume Mix

Installed Capacity

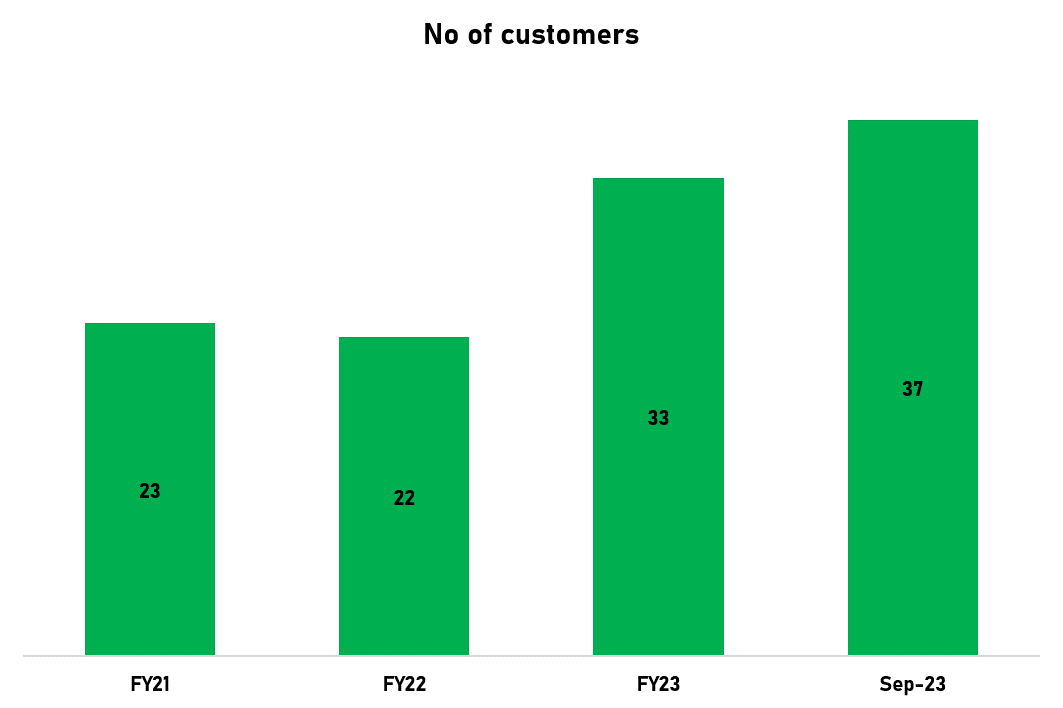

Key Customers

Ratios

Figures in Rs. Crores

| Mar 2019 | Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | |

|---|---|---|---|---|---|

| Debtor Days | 37 | 26 | 39 | 32 | 30 |

| Inventory Days | 27 | 34 | 33 | 38 | 39 |

| Days Payable | 55 | 59 | 64 | 59 | 48 |

| Cash Conversion Cycle | 9 | 1 | 7 | 11 | 21 |

| Working Capital Days | 3 | -5 | 4 | -1 | 15 |

| ROCE % | 10% | -16% | 7% | 15% |

Key Risks:

- Heavy Reliance on Non-Vegetarian Segment: Chatha Foods derives a significant portion of its revenue from non-vegetarian products. A shift in consumer preferences towards vegetarianism or a negative event impacting the meat industry (e.g., disease outbreak) could significantly impact their sales and profitability.

- Financial Performance: The company has a history of negative cash flow and has a low profit margin on its products.

- Competition from Established Players: Large FMCG companies like ITC, Nestle, Unilever etc, plus players like Venky’s Godrej Agrovet, etc. would have strong brand recognition and distribution networks. Also companies like These companies Kare Foods, Prabhat Foods, may target specific niches or offer premium products, which could eat up Chatha’s market share.

- Start-ups in the meat alternatives space: The growing demand for plant-based protein could pose a threat in the long run.

- Low liquidity: Being a small company on the SME board, it has very low liquidity.

- Lack of Analyst Coverage: There is currently a lack of analyst coverage for Chatha Foods, making it difficult to get professional insights into the company’s future prospects.

Disclosure: Have taken a small tracking position in last 10 days.

Thanks,

Dhaval Patel (SMEmitra)