Hoteling company from the stable of K Raheja group, Chalet Hotels Limited (CHL) is an owner, developer and asset manager of high-end hotels in key metro cities in India.

Company has 6 hotels, 1 service apartment, 2 commercial projects and 2 retails projects spread across Mumbai, Pune, Bengaluru & Hyderabad.

| Started | Name | Location | Property | Capacity |

|---|---|---|---|---|

| 2000 | Lakeside Chalet, Mumbai - Marriott Executive Apartments | Powai, Mumbai | Service residence | 173 keys |

| 2001 | Renaissance Mumbai Convention Centre Hotel | Powai, Mumbai | Hotel | 600 keys |

| 2009 | Four points by Sheraton | Navi Mumbai, Vashi | Hotel | 152 keys |

| 2009 | The Westin Hyderabad Mindspace | Hyderabad | Hotel | 427 keys |

| 2012 | Inorbit Mall | whitefield, Bengaluru | Retail | |

| 2013 | Bengaluru Marriott Hotel | whitefield, Bengaluru | Hotel | 391 keys |

| 2014 | Commercial Tower | whitefield, Bengaluru | Commercial | |

| 2015 | JW Marriott | Mumbai, Sahar | Hotel | 588 keys |

| 2018 | Business Centre & Office | Sahar, Mumbai | Commercial | |

| 2018 | The Orb | Sahar, Mumbai | Retail | |

| 2020 | Novotel | Pune, Nagar Road | Hotel | 223 keys |

Novotel was acquired in Feb 2020.

Apart from the above, company has 2 residential projects at Madhapur (Hyderabad) and Koramangala (Bengaluru). The residential development project at Bengaluru is on hold as the matter is sub-judice before the Hon’ble Karnataka High Court on account of a dispute on the permissible height of the structure.

CHL have branding and operational tie-up with leading global hospitality chains having strong brand name. (JW Marriott, Westin, Marriott, Marriott Executive Apartments, Renaissance, Four Points by Sheraton and Novotel, which are held by Marriott Group and the Accor Group)

Company has entered into a memorandum of understanding with Marriott Hotels India Private Limited for rebranding w.e.f. April 1, 2020, of the existing hotel viz. Renaissance Mumbai Convention Centre Hotel as ‘Westin Mumbai Powai’.

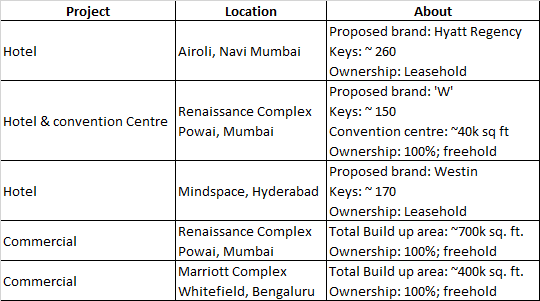

Company is in the process of developing 3 additional hotels and 2 commercial office spaces. Below are the details:

Company has a subsidiary Chalet Hotels & Properties (Kerala) Pvt. Ltd. Although there is insignificant business in this subsidiary. (Not sure why this subsidiary was started.)

For securing the supply of renewable energy, Company has acquired 20.8% of the Equity Share Capital of Krishna Valley Power Private Limited and 26% of the Equity Share Capital of Sahyadri Renewable Energy Private Limited, being entities engaged in generation of hydro power. (Not sure how much saving does it really accrue and what is the impact on bottomline.)

Some of the down sides as presented in Q3 presentation:

- Sluggish consumer spends

- General economic slowdown

- Lower banquet & MICE revenue (for CHL)

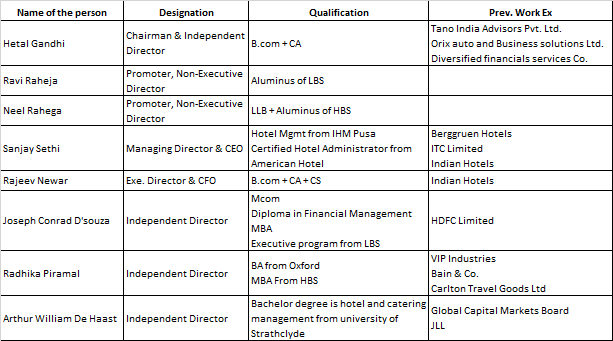

Board of Directors:

Financials:

| ADR (Rs.) | FY18 | FY19 | FY20 9M |

|---|---|---|---|

| MMR | 7629 | 8086 | 8149 |

| Bengaluru | 8620 | 8756 | 8995 |

| Hyderabad | 7896 | 8205 | 8547 |

| Combined | 7840 | 8218 | 8366 |

ADR represents revenue from room rentals at the hotel divided by total number of room nights.

| Occupancy (%) | FY18 | FY19 | FY20 9M |

|---|---|---|---|

| MMR | 73% | 76% | 75% |

| Bengaluru | 75% | 77% | 76% |

| Hyderabad | 72% | 76% | 74% |

| Combined | 73% | 76% | 75% |

Average occupancy represents the total number of room nights sold divided by the total number of room nights available.

| RevPAR | FY18 | FY19 | FY20 9M |

|---|---|---|---|

| MMR | 5543 | 6178 | 6075 |

| Bengaluru | 6447 | 6757 | 6846 |

| Hyderabad | 5694 | 6234 | 6301 |

| Combined | 5716 | 6283 | 6245 |

RevPAR is calculated by multiplying ADR and average occupancy available at the Hotels.

Total revenue mix is:

| Total Income Mix | FY19 | FY20 9M |

|---|---|---|

| Hospitality | 88% | 87% |

| Retail & Commercial | 4% | 10% |

| Others | 8% | 3% |

Hospitality Revenue Mix is:

| Hospitality Revenue Mix | FY19 | FY20 9M |

|---|---|---|

| Room Revenue | 58% | 59% |

| Food & Beverage | 33% | 32% |

| Others | 9% | 9% |

Financial:

| Particular (Rs. Mn.) | FY18 | FY19 | FY20 9M |

|---|---|---|---|

| Total Income | 8,513 | 10,348 | 7,714 |

| EBIDTA | 3,005 | 3,668 | 2,910 |

| EBIDTA % | 35.3% | 35.5% | 37.7% |

| PAT | -914 | -84 | 569 |

Company’s D/E has improved from 5.5 (FY18) to 1.0 (FY19). It stands at 1.0 as on 31st Dec 19.

Reduction in debt is due to equity raising (IPO).

Similarly, Debt / EBIDTA also improved from 9.1 (FY18) to 4.1 (FY19). If we prorate 9 months FY20 EBIDTA to 12 months, this ratio further improves to 3.8.

Q-on-Q movement:

| Particular (Rs. Mn.) | FY19 Q1 | FY19 Q2 | FY19 Q3 | FY19 Q4 | FY20 Q1 | FY20 Q2 | FY20 Q3 |

|---|---|---|---|---|---|---|---|

| Total Income | 2,456 | 2,572 | 2,549 | 2,771 | 2,462 | 2,405 | 2,847 |

| PAT | -229 | -126 | 141 | 130 | 137 | 101 | 331 |

| PAT % | -9% | -5% | 6% | 5% | 6% | 4% | 12% |

| EPS | -1.3 | -0.7 | 0.8 | 0.8 | 0.7 | 0.5 | 1.6 |

FY20 Q3 has been exceptional quarter. Improvement in revenue is directly flowing into PAT. Largely the improvement is from Retail & office business. Q-o-Q there has been more store opening at The Orb and also the improvement at Inorbit Mall Bengaluru.

| Particular (Rs. Mn.) | FY19 Q1 | FY19 Q2 | FY19 Q3 | FY19 Q4 | FY20 Q1 | FY20 Q2 | FY20 Q3 |

|---|---|---|---|---|---|---|---|

| Hospitality | 2170 | 2075 | 2326 | 2566 | 2198 | 2046 | 2500 |

| Retail & office | 65 | 105 | 130 | 91 | 152 | 307 | 281 |

For TTM EPS of Rs. 3.6, current price of Rs. 340 is trading at PE of 94.4.

Disclosure: invested @ Rs. 328.