CG-VAK is providing cutting-edge solutions for more than 25 years to companies around the globe.

They are a group of around 300 people thriving on the 3 tenets “IDEATE, INNOVATE, CREATE”.

They help transform businesses and organizations by delivering Digital Innovation, Product Innovation, and Modernization at business speed.

They are growing continuously quarter after quarter as well as Year after Year.

Mcap - 175 Cr. Promoter Holding is 53.64%. The free float Market cap is around 81 Cr

In my opinion, what is the differentiating factor is considering the size of the company:

-

Writes Blog

-

Case Studies. One case study example - Automated Email System for Marketing

Management

The company is managed by a well-experienced Board of Directors who have vast experience in creating many success stories in varied businesses.

They have over 30 years of business experience including 23 years in the IT business, Manufacturing and International trade. The business units are headed by Vice Presidents and Managers who are well-qualified and experienced in their respective fields.

Qualitative thought: A brief description of each member on their website Management Info. Very few companies under a 200 Cr Market Cap provide this information.

Resource retaining is always a challenge for any IT company. If we see this company’s top-level management, all are associated with this company for a long time which is eventually benefiting to company

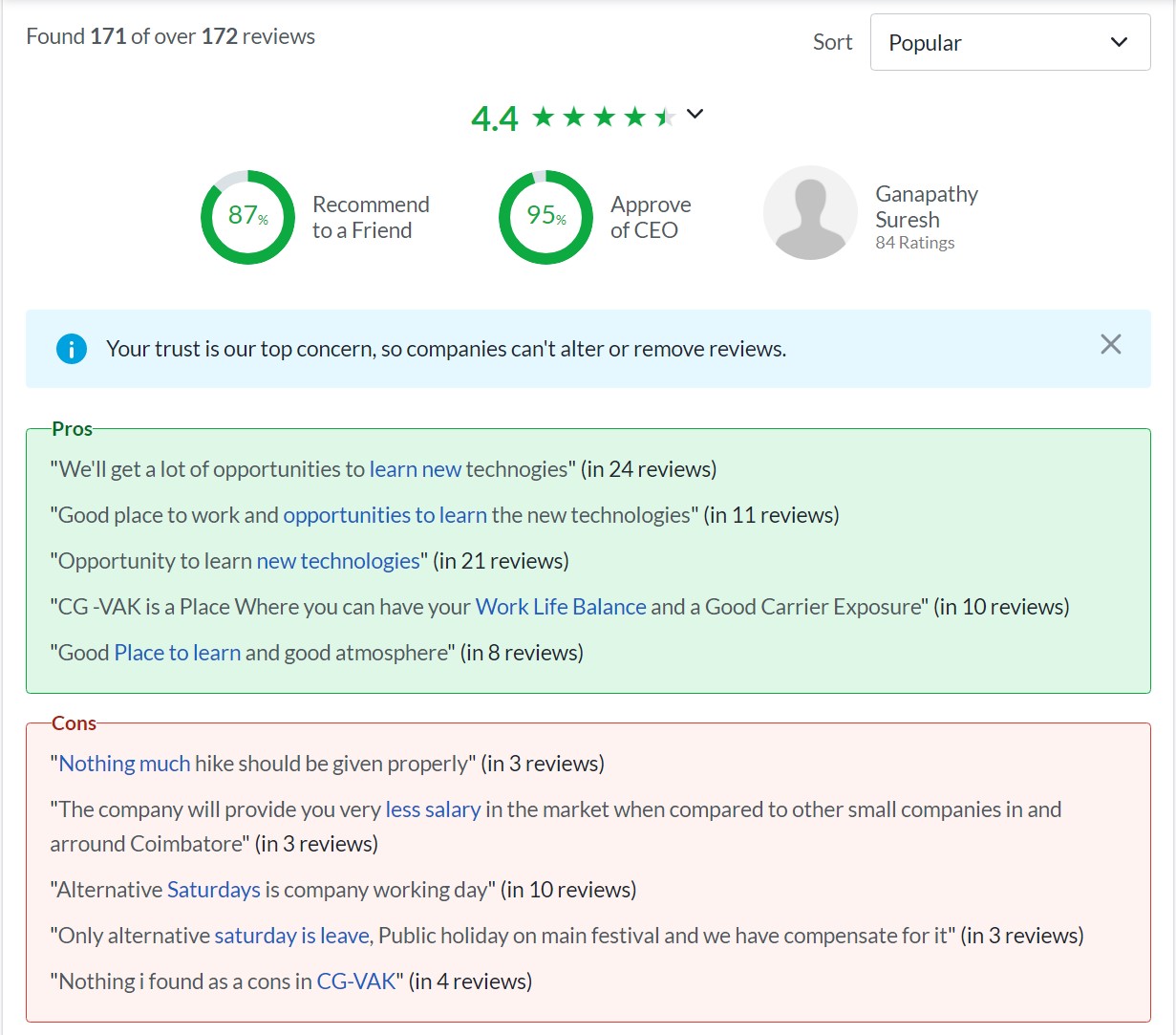

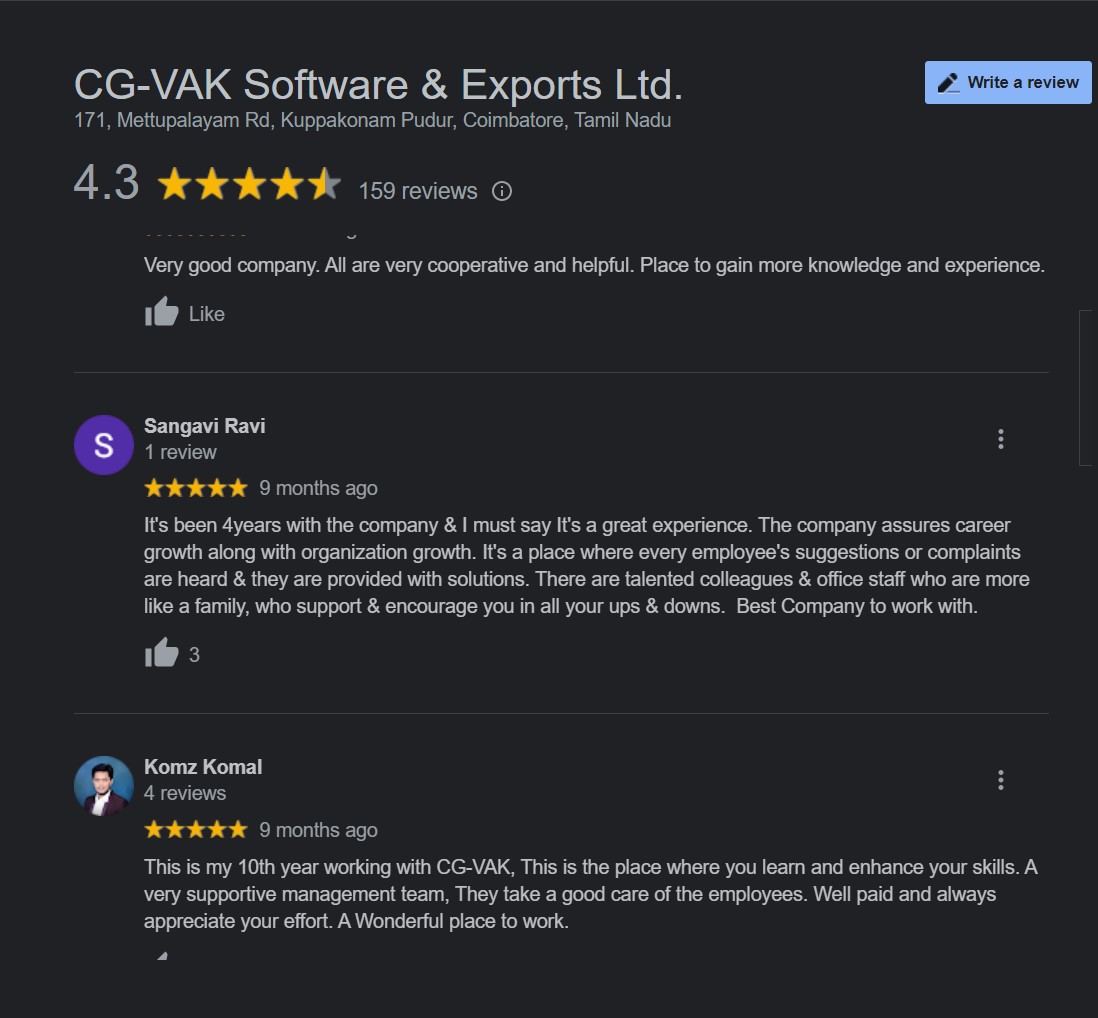

Company Reviews from Employees

Glassdoor

Google

Financials

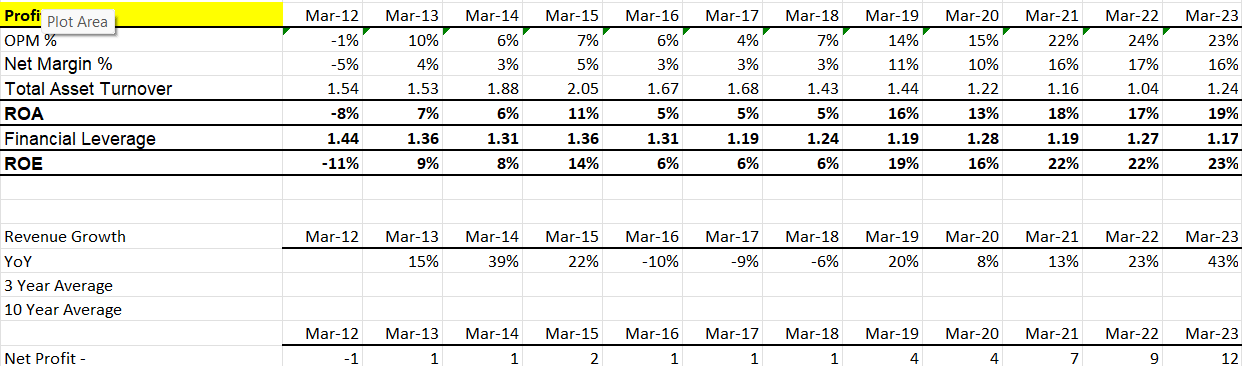

The company did its highest-ever quarterly sales with a decent margin of 22.66%

Sales: 14% CAGR over 3 years. 54% CAGR over TTM

Profits: 36% CAGR over 3 years. 57% over TTM

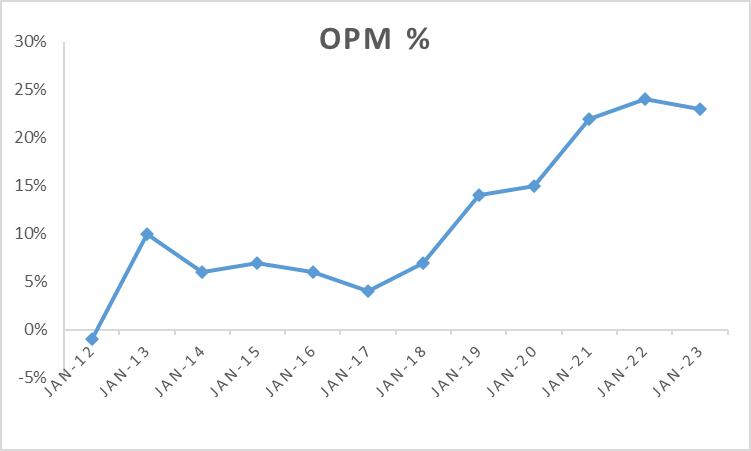

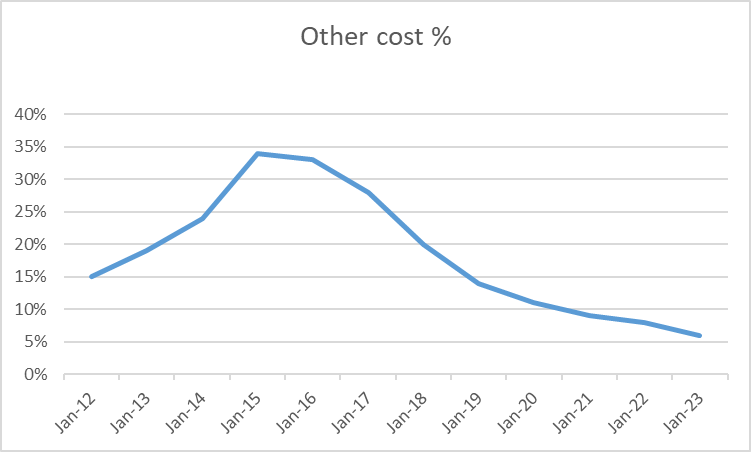

Margins: Maintained over 22% for 3 consecutive years. At their highest margin of 25% this year.

Triggers

- Last 3-4 quarters, each quarterly revenue number has been their highest ever. Benefits of operating leverage kicking in

- Oct 2021: 90 cr Market Cap company buying a 15 cr office with 25 cr cash on the balance sheet

- They are hiring aggressively - 287 employees v 240 YoY AR 22. Saw many LinkedIn and Twitter Hiring Posts

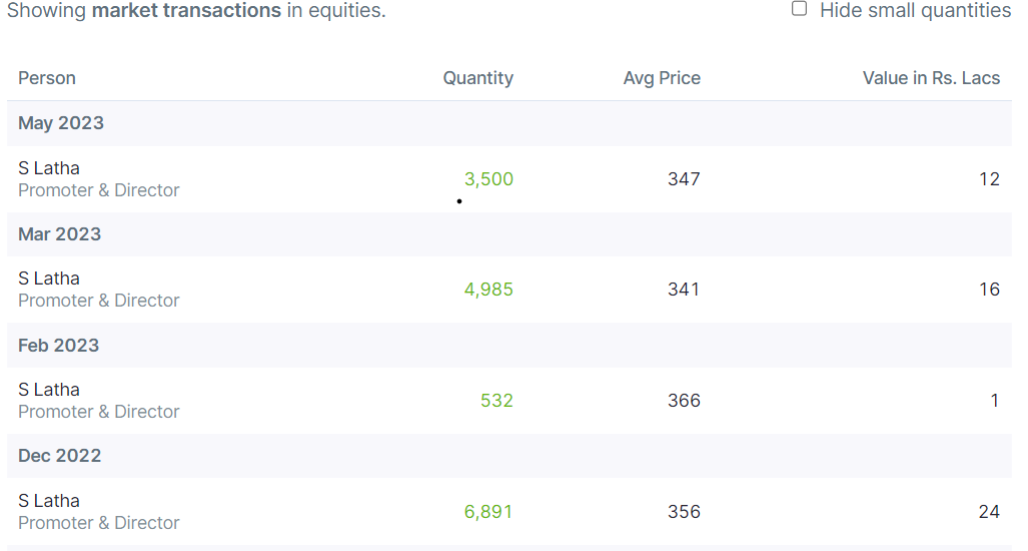

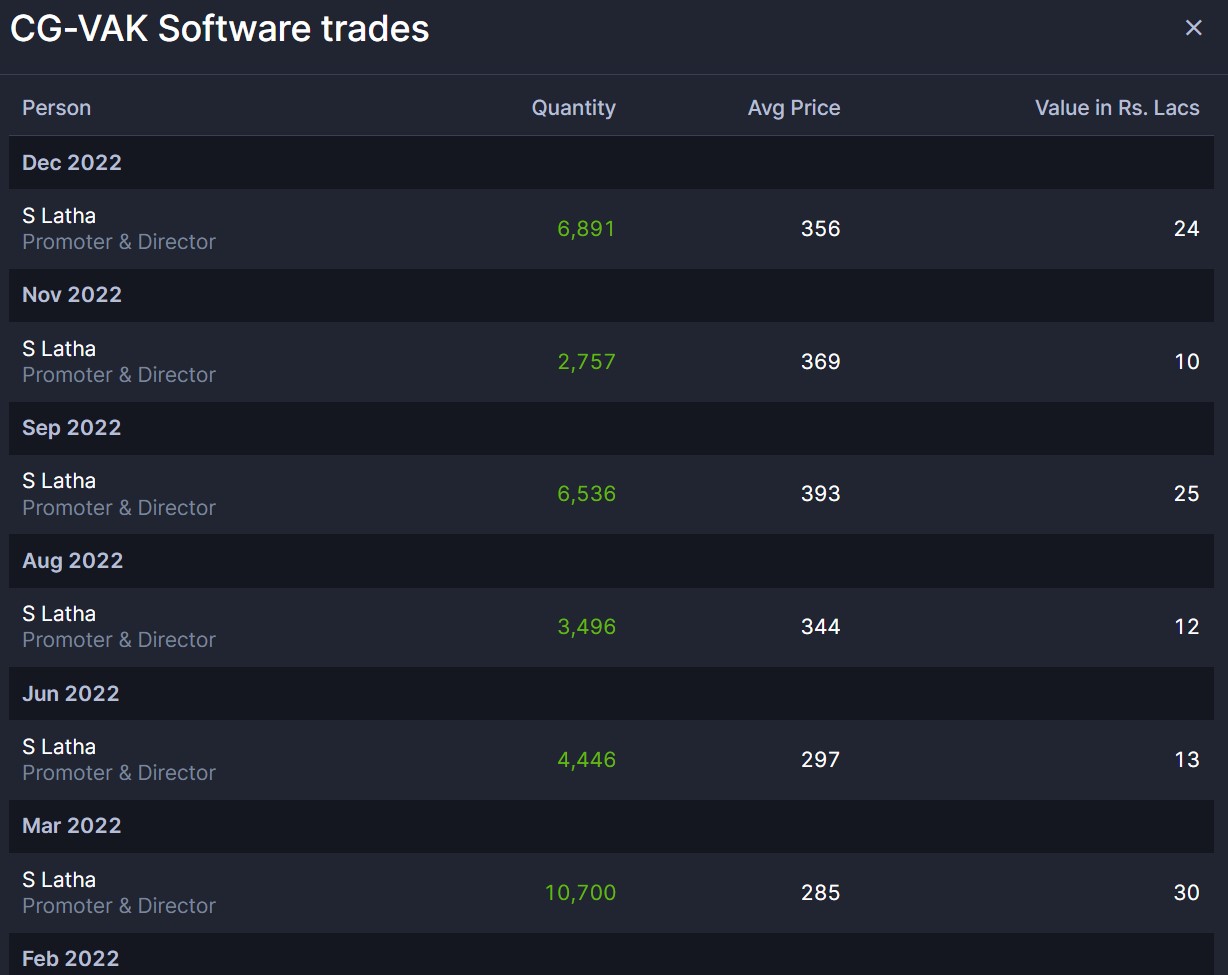

- Promoter Buying - They are buying from the open market every quarter for the last two years

Risks

From their AR one major thing seems is the CEO and his wife are taking 2.2 Cr - 2.6 Cr (1.81Cr in remuneration and the rest as rent as detailed in the third-party transaction) which is around 21% of TTM net profits

Investment disclosures

Initial entry at around 286 Rs.

Invested: Allocated around 7% of my Portfolio at an average of 315 rs.

Want to take the allocation to around 10% if everything goes well

Please feel free to add/correct any information if I missed any.