CFF Fluid Control Ltd is an Engineering Company creating self reliance by Innovating and Manufacturing customized products and solutions for the defense industry of India.

Immediately after inception, a TOT agreement with Coyard SAS France led to the introduction of new-age fluid control and other mechanical equipment on the under-construction Submarine program of the Indian Navy. Subsequently, under a framework agreement with the collaborator and Designer of the Submarine and various partners from around the world, we are able to provide technological solutions ranging from mechanical to electronics power and communication, locally under Make in India.

Industries Served -

- Defense

- Energy

Sevices provided -

a. Manufacturing (Manufacturing Critical components, Assemblies, Sub-Assemblies, Equipments)

b. Support Services (Repair and Maintenance)

c. Strategic Projects

Products -

- Fluid system for submarine

- Antenna and navigation System for submarine

- Weapon systems(Torpedo, Tubes and Fire Controls)

Revenue Breakup (FY 21-22)

- Defense - 89.43%

- Non- Defense - 10.57%

Its manufacturing facility is situated at Khopoli,Maharashtra and is spread over 6,000 sq. mtrs. The facility is approved by Indian Navy, MDL & Naval Group (France) and has ISO 9001:2015 certification for quality management systems.

Important Notes -

They have a robust order book as on December 31, 2022 of Rs.9,004.00 lakhs of which

over 90 % pertains to orders from Indian Navy (including its OEMs)

They have entered into additional product line for submarine which is Towed Wire Antenna (TWA) which is used as an underwater communication device. To manufacture this product we have entered Letter of Intent (LoI) with Nereides, France who is engaged in manufacturing TWA, who will over the years transfer us its technology, process, knowhow and product development. They have agreed to remit amount not exceeding Euro 1 million for the transfer

The projects of Submarines in which they have supplied components have also authorized them for Repair and Maintenance of the same - (Life of a submarine is 30 years)

Indian Navy Fleet Plan - From 137 today to 200 by 2027

Raw Materials required are mostly locally procured and easily available(Nickel- Aluminum- Bronze, Copper- Nickel, Copper Aluminum, Titanium). Only around 8% of the raw materials used are imported.

IPO Issue Size - Approx 85 cr

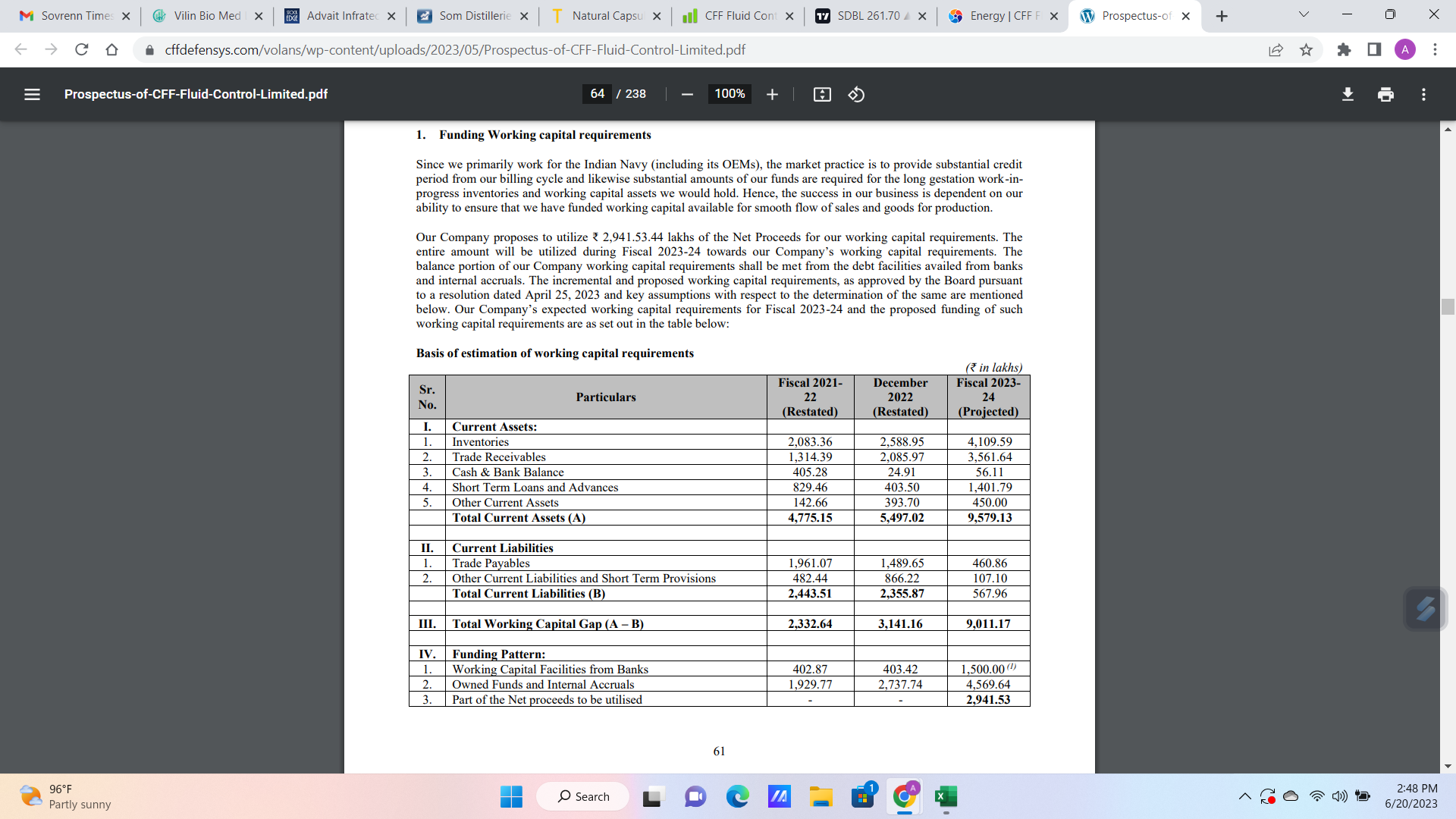

Funding WC requirements - 29.41 cr

Repayment of Loans - 21 cr

Purchase of Plant and MAchinery(Capacity expansion) - 9 cr

Acquire Technology of TWA - 8.5 cr

General Corporate Purpose - 16.71 cr

EBITDA - 24% app, PAT - 14% app, P/E - 45.7 , CMP - Rs.183

Risk Factors -

- 74% of the Total Borrowings are unsecured borrowings.

- Some Licenses and permits are required to be re-issued from time to time.

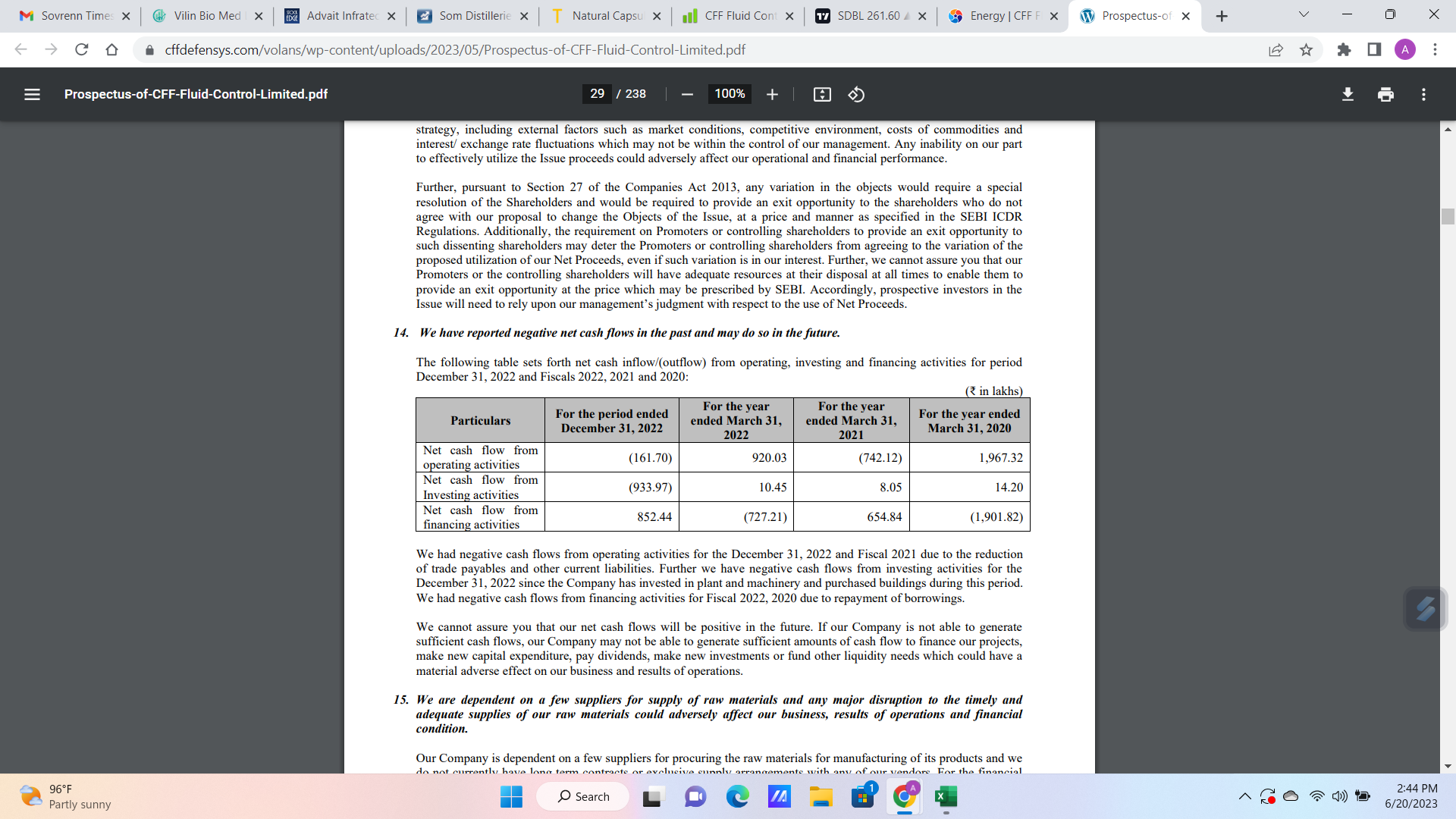

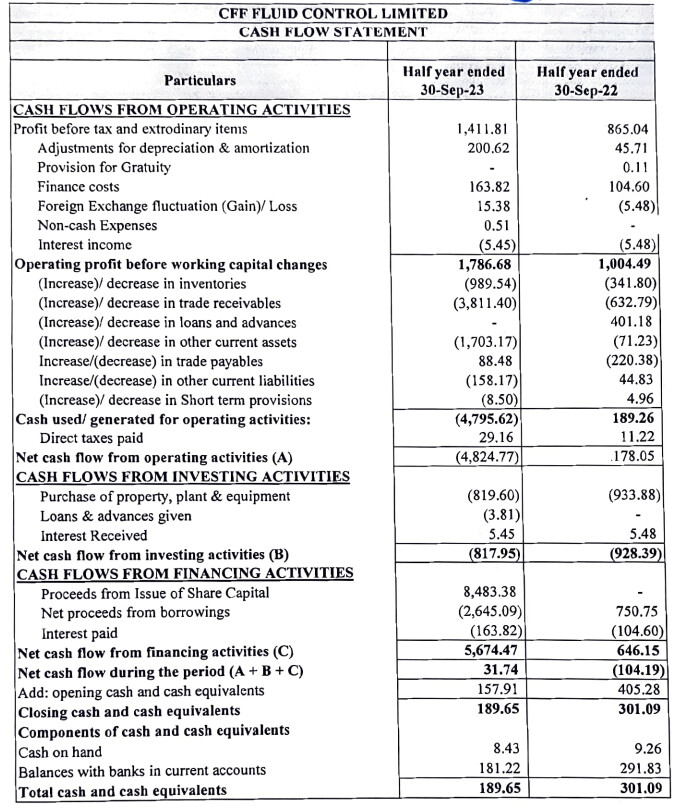

- As mentioned in the Prospectus - it has Negative cash flow from Operating Activities

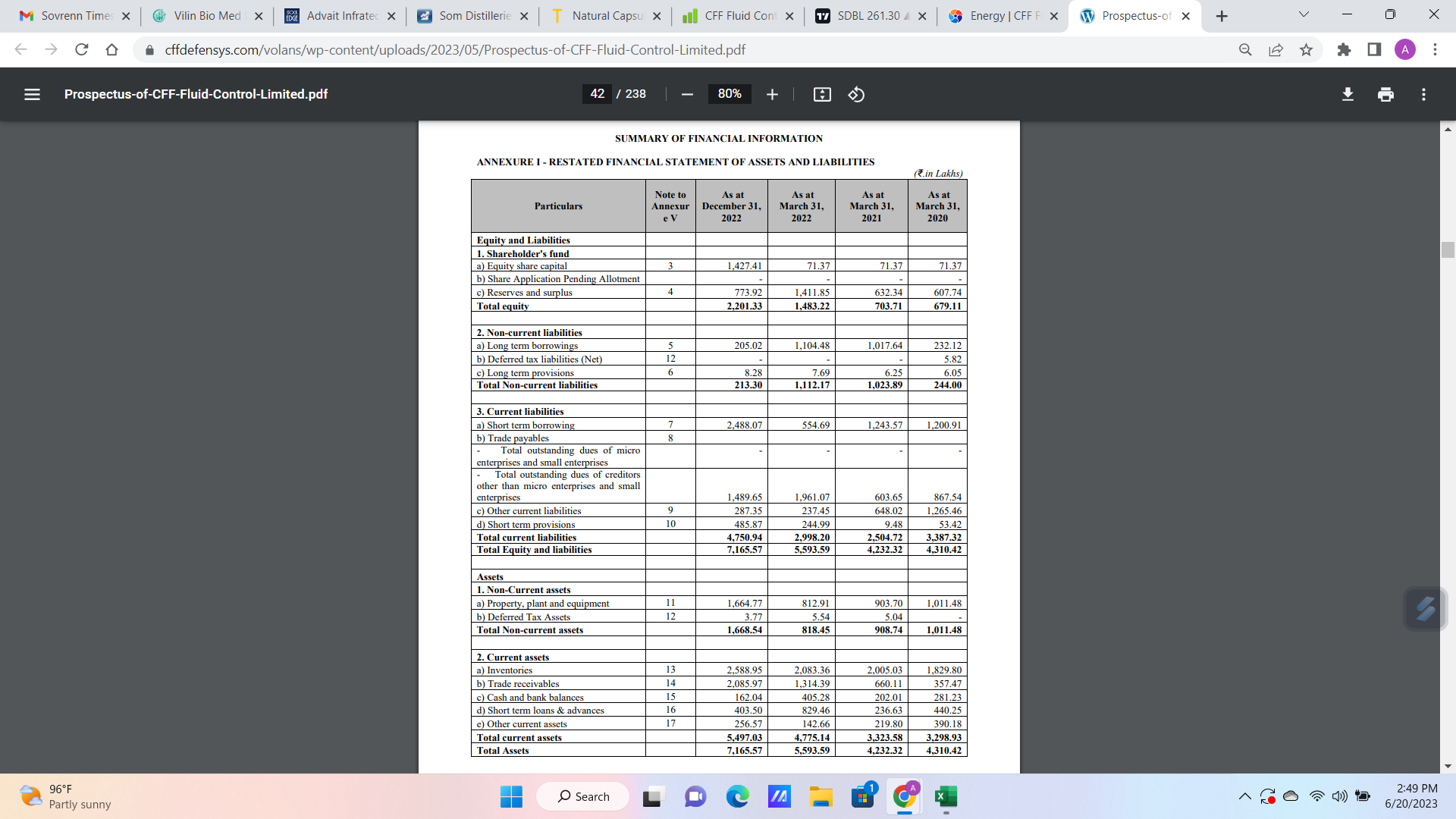

- High Inventories and Trade Receivables- As at December 31,2022

- Very High Working Capital requirements as projected in the prospectus-