-

import isnt a big threat for Sanitaryware. The cost of shipping from China to India and other related charges (not excise duty, not sure if it exists) is about 10-20% of the cost of the product because of the size and bulky nature of product, making it uncompetitive at the lower end. Faucetware might be a different story since they’re smaller in size

-

as per mgmt, tier 2-3-4 towns have very few trained plumbers and these plumbers are more or less controlled by the distributors of sanitaryware/faucetware products. Cera’s close association with these distributors mean a significant entry barrier to new competition. So customer service could mean anything from installation of product to solving leakage issues etc. for an idea of how much cera values its distributors, just lookup how often they are mentioned by management in the concalls.

The concall for Q3 is out. As per the company, sales have increased by 20%.

There was strong demand in Q2 too but because of lock-out in the factory, they were not able to capitalize much on the demand.

As per the management, there is strong demand after 2012 and it seems that real estate is making a comeback.

Latest management interview (link):

- 50% business is outsourced and rest is done in-house

- Demand is still greater than supply, currently not experiencing any covid impact

- Sales breakup: 50-55% sanitaryware (highest margin); 27% faucetware (high margin); rest is tiles (margins lower than consolidated company margins; commoditized business; <300 cr. annual sales)

- Should double topline in 3.5-4 years

Disclosure: Invested (position size here)

Here are my notes from Q4FY21 concall.

- Domestic demand robust, demand is much higher than supply

- Target 14-15% EBITDA margins

- Operations were not at full capacity in the first 45 days due to maintenance operations, capacity utilization was 85% for sanitaryware and 92% for faucetware

- Outsourcing was 65% for sanitaryware (50-55% normal) and 59% for faucetware (50-55% normal)

- New product contribution ~ 20% of revenues

- A&P spends ~ 1.5% of revenues (vs 3.5% in FY20). Ad spend strategy has been changed, there are short time periods of spends and marketing team assesses their efficacy and go for these spends multiple times in a year. If the last spend remains effective for 8-9 months, then the team delays the next marketing burst. Currently, there is product shortage which is also why ad spends are lower

- Higher raw material price passed on, 5-7% in sanitaryware and 8-10% in faucetware

Disclosure: Invested

FY21 AR Observations:

Sanitaryware Unit

- Company’s growth was affected due to the nation-wide lockdown after the outbreak of COVID-19.

- After the lifting of lockdown, shortage of workforce restricted its production from reaching its optimum capacity. There was also an illegal stoppage of work by a section of workforce for 85 days, which ended with the Hon’ble High Court’s order for resumption of work.

- Continued to develop new designs of one piece WCs and high-end wall hung WCs, thereby reducing the dependence on import of such products

- After successful implementation of 3D printing and robotic glazing technologies, now added high pressure casting system

- Your Company also implemented high pressure casting, for high end wall hung WCs, which could produce thirty pieces from one mould in a day, as compared to one piece by one worker in a day from conventional casting systems

Faucetsware Unit

expects higher growth in the coming times in its Faucets business

ISVEA

The Italian luxury designer sanitaryware, ISVEA, launched by your Company, exclusively in India, is expected to take off in sales after the Covid pandemic

Modular Kitchens

Sales of Senator Cucine, Italian modular kitchens, launched by your Company, should hopefully take off after the pandemic

Dubai operations : Business operations of Cera Sanitaryware Trading LLC-Dubai (Associate) have been closed / terminated w.e.f. 12th October, 2020 due to continuing unviable business operations. The appropriate Authority at Dubai has commenced the company closure process.The Company has therefore provided for the impairment loss of the entire capital contribution in this LLC of ` 32.10 lakhs

Long-Term Settlement

- Due on 01st September, 2021

- The number of permanent employees on the rolls of Company: 2473; contractual / casual basis - 1431

- Due to COVID-19 pandemic impact, there was no increase in the salaries of the employees at all the levels across the organization.

- EMPLOYEE BENEFITS EXPENSE: 144 Cr. (Was 160 Cr. in FY20)

- The manufacturing activities in respect of Sanitaryware Unit have been materially affected, while that of Faucetware Unit have been affected marginally as a result of partial disruption by workers at the Company’s plant located at Kadi, from September 28, 2020 to December 22, 2020

- Your Company had nurtured suppliers because of which even when own production was affected due to an illegal strike resorted to by a section of workforce which lasted 85 days, the supplies to market was less impacted. The entire workforce restarted the work, after the Hon’ble High Court of Gujarat issued an order to the leaders of the striking section of workers that the production cannot be hampered

Others:

-

The Company has entered into agreement with Anjani Tiles Limited (Subsidiary , PAT: Loss of ~5 Cr in FY21) for purchase of its entire production of Tiles. Ageing of past due but not impaired receivables (Beyond 12 months): 40 Cr. (Was 44 Cr. in FY20)

My Opinion: Unable to find any reasons for the current valuation and it’s future sustainability.

Disc: Not Invested.

Happened to listen to the Q1 call recently & must say one of the best calls I have listened to, recently. Disclosure policies of the management are top notch.

-

Business outlook

• 56% growth in revenue yoy (though on a lower base in Jun 20)

• 55 to 60% of topline from tier 3 cities & beyond.

• Capacity utilization: Sanitaryware – 88%; Faucetware – 70%

• Sanitary ware– 10% price hike implemented in Aug 21 ; faucetware – 10% price hike in August. This is further to a price hike implemented in Feb 21.

• Sanitaryware – 50% contribution to revenue; faucetware – 31% in this quarter.

• Within sanitary ware – 55% through outsourcing, 45% own manufacturing ; faucetware – 55% through outsourcing, 45% own manufacturing

• Strong Demand for new prod launches – contributed 21% of revenue

• Cash on books: 470 cr . Free cash flow generation (262 cr in FY 21) far exceeds annual capex requirement (27 cr)

• With healthy cash reserves – portion of cash likely to be used for increasing working capital inventory and increasing inventory gain. 46 cr used in Q1 for increasing WIP inventory and overall working capital

• Current year – capex budget is around 17 cr – of which 6.7 Cr is for sanitaryware automation ; 4.5 Cr is for faucetware automation -

Seeing strong housing demand fueled by - Waiver on stamp duty announced by many state govt. One of the leading banks– announced waiver on processing fee

-

Company Strength: Own manufacturing excellence and strong vendor base for low end products. Took 15 years to build this. Not something that can be replicated by peers easily – entry barriers.

Some peer (with faucetware background) entered sanitaryware on basis of China imports & trade discounting thinking they will make significant inroads - only managed a temporary splash. They have no products / running dry for last 1.5 months and for next 90 days. Any company which is looking for a quick fix – doesn’t work as one of the peer group companies have discovered. This is where strength of Cera (own manufacturing excellence) has come to the fore.

Skill sets to manufacture sanitaryware is available only in 2-3 locations across the country. -

In the topline – 5% is overall import from China. Other companies – that number from China is 50%. Peer group got impacted; topline of 300 -400 cr is up for grabs. Company is likely to gain market share in coming quarters

-

Segment wise revenue

Export 4% vs 2% last yr

Tier wise

a. Tier 1 27% vs 24% Q1 last year

b. Tier 2 14% vs 10% Q1 last year

c. Tier 3 – 55% vs 64% Q1 last year -

Entry range vs premium – (evident that clearly contribution of premium range has increased)

a. Sanitary – Entry 34% vs 41% last year ; mid price 13% vs 13% (same). Premium 53% vs 46% last year

b. Faucet - Entry 29% vs 32% last year; mid price 15% and 15% (same). Premium 56% vs 53% last year -

Demand outlook – from Aug 20 demand has been higher than supply. For industry as well as for Cera. Industry which was growing in single digit for many years is now growing in double digits. Across last many years – the highest July number was achieved in July 19. July 21 is much higher than July 19 numbers. Expecting the trend to continue in Q2, Q3

Aim this year is not to optimize inventory days but to increase inventory days. Ensuring product availability is the main focus this year. -

Strong demand in spite of price hike: Enjoys strong pull. – end consumer driven. A segment where customer loyalty changes after 10 years. Product longevity is around 10 years. So strong customer stickiness

-

Investment: 190 Cr capex was spent on the shop floor from 2015 to 2019 – giving the company the ability of manufacturing complex products and SKUs. That is now bearing fruit and resulting in better offtake.

Management exuded confidence on all ingredients being in place for consistent volume growth & value growth for next 2-3 years – both from end consumers & projects

While valuations seem a little stretched, interesting that the counter did not see a significant correction in the recent volatility phase.

Disc: Tracking

Challenges abound. One more challenge for the company to pass by - with a wide distribution network and working on similar product area already, this would be a challenge to watch out of. As a shareholder - it is good time to evaluate management resolve when such challenges are thrown.

I would say this is similar to Grasim vs Asian Paints conditional playing out. A well heeled credible player challenging an established player.

Disc : Invested at much lower levels. Not a recommendation to buy/sell.

Some views on this covered here - Indigo Paints: Upcoming Star - #50 by zygo23554

Building materials will see the respective category leaders encroaching into each other’s turf over the medium term. Brand extension into adjacencies is credible and they already have the distribution and channel might to be able to create a market for themselves.

Isn’t this how HUL and ITC built adjacent brands over a period of time?

If the dealer wants to sell Fair & Lovely/Cigarette he should stock and push the newer products too

Isn’t this how managements implement a cross selling framework for their sales teams?

If you want your incentive for this year, 5% of the fee you generate should come from life insurance

Using principles of inversion, any business that can deliver respectable growth in their new verticals has a lot of clout within their channel. Only the strongest of businesses will think they can pull off something like this, an average business which has neither the brand value nor the channel clout will not even try to do something like this.

Building materials categories have a long tail of unorganized players who will cede market share to the organized ones over the next 10 years. The battle is for this pie which is a growing market.

Interesting part here is that Astral hired CERA CEO Atul Singhvi to lead their forey into this business. Atul Singhvi resigned from CERA in August.

Astral is a formidable player - they expanded into Adhesives business about 5 years back and it has been a very successful venture for them. Now they are entering Faucets & Sanitaryware. Clearly they are capitalising on their powerful distribution-network and strong brand that they have built over the years.

While the pie is large here and strong organised players will keep capturing market share from unorganised sector but will be interesting to see how/if Astral’s entry impacts CERA.

Disc: Invested in both for a decade. Astral >> CERA in my portfolio.

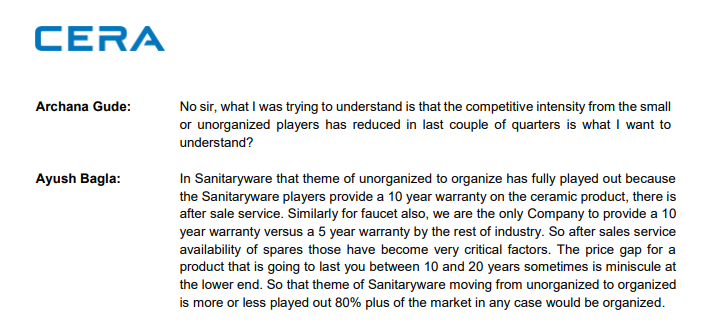

Management has clearly told in the Q4 FY20-21 earnings call about the Unorganized to Organized transition. They have indicated its clearly played out!

FY22Q2 concall notes

- Margin expansion has happened due to topline growth, pricing power (2 price hikes taken this year and 1 more planned in November)

- Will need expansion for faucetware and sanitaryware (have land that was bought last year) as currently they are operating at 90%+ utilization

- Gail provides 59% of gas requirement and gas prices have gone up from Rs. 9.8/m3 in September 2021 to 13.4/m3 in October 2021. Sabarmati pricing has gone up from 41-42 to 50/m3 (supplying 41% of demand)

- FY21 capex: 9.84 cr., FY22 capex budget: 17.19 cr.

- Have significantly strengthened the management team

- 30% sales are from Tier I markets, 50% from Tier 2, 15% from Tier 3 and rest from exports

- Couple of companies have been unable to cater to market due to very high Chinese dependence which is benefitting existing players

- Lead time for putting up a faucet facility is ~12 months

Disclosure: Not invested

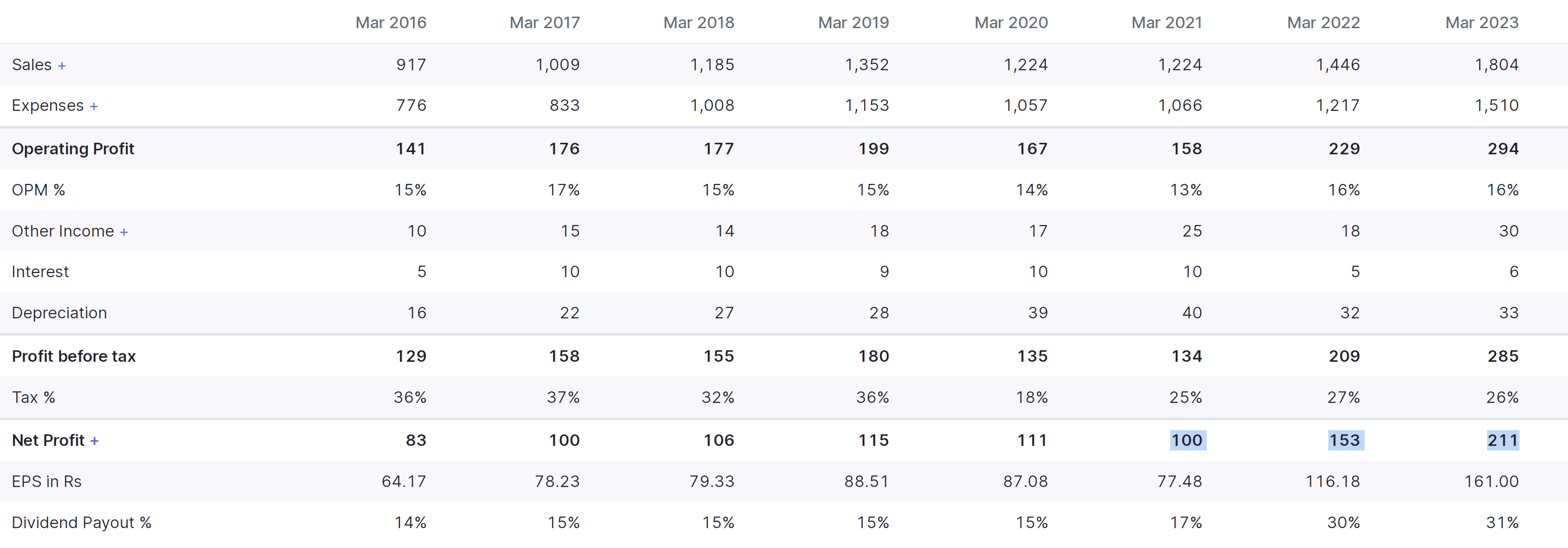

Very strong results, 28% sales growth and 43% PAT growth. Also, Kajaria has reported stellar numbers. Building material space seems to be doing very good. Here are my notes from the CNBC interview.

- Faucetware unorganized market ~ 4000 cr. of total market size of 10’000 – 11’000 cr. For cera this segment is growing at 40-50% (mostly demand from home upgradation)

- B2B is 30% of sales, B2C is 70% of sales

- New product (last 18-24 months) sales are 20% of topline

- Industry growth has increased to 10-12% this year (from earlier levels of 5-6%). Cera wants to grow at double of industry growth (20-22% annual revenue growth rate over the next 3-years)

Disclosure: Not invested

Results were reasonable with base business growing by 12% in Q4. Consolidated sales growth looks muted because of tiles business divestment. Management is confident of doubling sales in next 3.5 years.

FY22Q4 concall notes

- Sales guidance is to double over 3.5 years

- Consolidated quarterly sales took into account divestment of tiles business, that’s why looks a little bit muted

- Revenue growth from facuetware + sanitaryware + wellness products grew from 346 cr. in Q4FY21 to 389 cr. in Q4FY22 (12%)

- Gas price: Gail gas price is 13.26/m3 in March 2022 and provided 44% of requirement and Sabarmati price is currently 70/m3 (Q4 was 65/m3)

- Gas cost as a % of sales was 2.43% in FY22 (and 2.79% of costs)

- Operating at 110% capacity utilization, confident of 20-25% topline growth and higher bottom-line growth

- Faucetware: 1.6 lakh unit monthly has been ramped up to 2.7 lakh monthly units. This is being increased to 4 lakh monthly units at 69 cr. cost (June 2023 commissioning, brownfield, asset turns 2.5-3x, expect incremental revenues of 150-180 cr.),

- Sanitaryware: Greenfield at cost of 128 cr., currently annual capacity is 25 lakh unit (operating at 110%) which will be ramped up to 37 lakh unit. Cost of land is 25 cr. which is yet to be acquired (to be finalized in 2-quarters). Expect incremental revenues of 180-200 cr. (fixed asset turns ~ 1.75x)

- B2C business was 67% in FY22, maintain 70:30 mix b/w B2C and B2B

- Sales from new home construction is less than 1/3rd of business, after-market home redecoration is less cyclical than new home sales

- Outsourcing was 46-49% pre-covid which has increased to 59% in sanitaryware and 54% in faucetware. Broad basing of vendor base is a very important theme for company

Disclosure: Not invested

hi, @harsh.beria93 , You have been following this company from long time. I think , you also used to hold around 3% of your portfolio in 2020 around. From that time onwards, most of your posts have been positive and encouraging, but you have disclosed that you dont have investment in it anymore. I am curious to know, whats current position and what must be the reason to sell this company while continue following it with favourable posts. Are you considering buying it back? at todays valuations, how it appears to you?

Hi,

Thank you for seeking my views, I first bought Cera in 2019 because I had a view that residential real estate had bottomed out in India, and Cera was (and is still) one the most well managed building materials company. At that point, it was trading around 28x PE, which optically wasn’t cheap but they were one of the few companies which had grown sales and profits during the downturn.

I ended up selling in 2021 because I was not comfortable with the valuations at which it was trading (~58x trailing PE).

After selling, Cera’s profits more than doubled which suggests that in 2021, there were smarter participants than me who could foresee such a strong growth in profits, which is why it was trading at such multiples in the first place.

The most interesting thing which happened in Cera was they reported increasing margins during the commodity upturn in 2022, when most building material companies suffered. This was because Cera’s price increase was easily accepted by the market, and growth came back in their more profitable segments (sanitaryware, faucetware). Management had guided doubling sales (from FY22 levels) by 2025, which is probably why company continues enjoying higher valuations. However for me, I prefer buying real estate companies (or other building material cos like Stylam) which are exposed to similar tailwinds but are available at much much cheaper valuations. Apart from valuations, I don’t have any other concern w.r.t Cera. I have also attached my notes from FY23 below.

FY23Q1

- Hope to double topline in 40 months

- Cash has increased to 566 cr

- Volume growth ~ 10-15%

- Annual EBITDA margin should be 17-19%

FY23Q2

- H2 generally is 55% of annual revenues, confident of growing over 1600 cr. in FY23

- EBITDA margin guidance is for 15%+

- Gail gas cost price has gone to 33/m3 in October 2022. Average cost in Q2 was 25.7/m3 from GAIL (54% of requirement) and 74.87/m3 for the remainder (Sabarmati gas)

FY23Q4

- Industry grew at 6-7% vs Cera’s growth of 22% (both in sanitaryware and faucetware)

- Target: 2900 cr. revenues by September 2025

- Didn’t have to take price increase since May 2022 because of better cost efficiencies

- Rolled out new ad campaign (increased from 34-35 cr. To 57 cr.). Ad spends will remain at 4-4.5% of sales

- Largest co in sanitaryware and second largest in faucetware

- Dealers in March '22 were 4,260 which in March’23 had become 5,462. And the retailers were around 11,300, which are now around 14,600.

- Looking to improve EBITDA margins by 75 bps in FY24

- Brownfield faucetware expansion ~ 69 cr. (capacity will increase to 48 lakh units by FY24)

- Greenfield sanitaryware expansion ~ 129 cr. (land purchase is 25 cr.)

- Gas costs

Disclosure: Not invested in Cera (no transactions in last-30 days)

Thank you so much for the update. What i get from your post is, its better to invest in SIP form with each dip in price.

One more thing, as you said , in 2021, some investors were smart enough to predict the doubling of profit and hence PE was high. Currently PE is around 45, so does that same logic applies to current valuations too, that something good is still in future and hence such a high PE.

Mr. Ayush Bagla, Executive Director of the Company has tendered his resignation from the services of the Company to pursue new avenues

c8f4fbeb-13d4-4bba-b6a6-6ea47742989d.pdf (361.1 KB)

Hi investor, does anyone know about the Building materials industry’s size?