Quarterly Result Update ::

Century Ply aims Rs 5000 crore revenue by FY26 i.e double of it’s current revenue.

Disc : Invested.

Quarterly Result Update ::

Century Ply aims Rs 5000 crore revenue by FY26 i.e double of it’s current revenue.

Disc : Invested.

What’s your thoughts on integrity of the promoters of century?

I have never seen such a elaborate and detailed financial presentation (LINK) giving granules details and transparent communication to investors.

Q3FY23 Result Update ::

@mahesh.kalkar - Can you please explain what are you trying to highlight? the depreciations expenses have fallen by almost half but is this supposed to be alarming?

Century Ply Q3 concall highlights -

Sales - 877 vs 849 cr

Gross Profit - 280 vs 297 cr ( due higher RM prices - basically timber and chemicals prices )

EBITDA - 131 vs 157 cr, Margins at 15 pc vs 18.6 pc

PAT - 81 vs 82 cr ( due lower tax outgo )

Volume, Sales growth iro various segments -

Plywood - 7pc vol, 12pc sales

DecoPly - (-) 2pc vol, 0.5pc sales

Laminates - (-) 3pc vol, 5.6pc sales

MDF - (-)14 pc vol, (-) 8pc sales

Particle board - (-)19 pc vol, (-)8 pc sales

Logistics business - (-)10 pc vol, (-)4 pc sales

Segment wise Sales, EBITDA and EBITDA margins -

Plywood (including decoply )- 482 cr, 59 cr, 11 vs 14 pc

Laminates - 157 cr, 22 cr, 14 vs 12pc

MDF - 165 cr, 37 cr, 22 vs 30 pc

Particle board - 38 cr, 8 cr, 20 vs 27 pc

Logistics business - 19 cr, 6 cr, 29 vs 31 pc

As is evident, steep EBITDA margin contraction seen in MDF and particle board segment

Company net cash positive with a net cash balance of 210 cr

Have taken price hikes in Jan in plywood and price cuts in particle board

Hoshiarpur MDF brownfield facility expected to commence production in Mar 23

South India MDF capex continuing. Likely to commence production by second half of FY 24

Greenfield laminate expansion in AP likely to come on stream in 2 phases. First phase to come up by Q2 FY 24

Greenfield capex in Hoshiarpur planned for Plywood. Land has been acquired

Approved large Greenfield particleboard capacity in Chennai. Investment outlay here is expected to be 550 cr

MDF, Particle boards facing competition from Imports, hence margins are getting hit

Plywood, Laminates are not imported. Hence not affected as much

Company believes, they can still generate 15-20 pc ROCE from the new MDF, Particle board capex even at these ( kind of depressed ) prices

The only advantage that Century has vs others when setting up new MDF, Particle board capacities is that most of Century’s capex are funded by internal accruals hence the risk and return profile are better

Overall demand in Jan has been better than Q3 demand trends

Timber prices continue to remain firm. Likely to come down only after 2 yrs or so. The chemical prices are coming down

Expect slight margin expansion in Q4

Century’s MDF business is concentrated in North, away from costal belt. Hence, impact of MDF imports is lesser vs peers

Timber prices continue to remain firm. Likely to come down only after 2 yrs or so. The chemical prices are coming down

Expect slight margin expansion in Q4

Century’s MDF business is concentrated in North, away from costal belt. Hence, impact of MDF imports is lesser vs peers

If China demand picks up, MDF and Particle board dumping in India may reduce

Century’s cost structure is one of the best in the world wrt manufacturing MDF, Ply, Particle Board. So, import dumping is not such a big challenge. However, it does reduce the margins

Disc: invested, biased

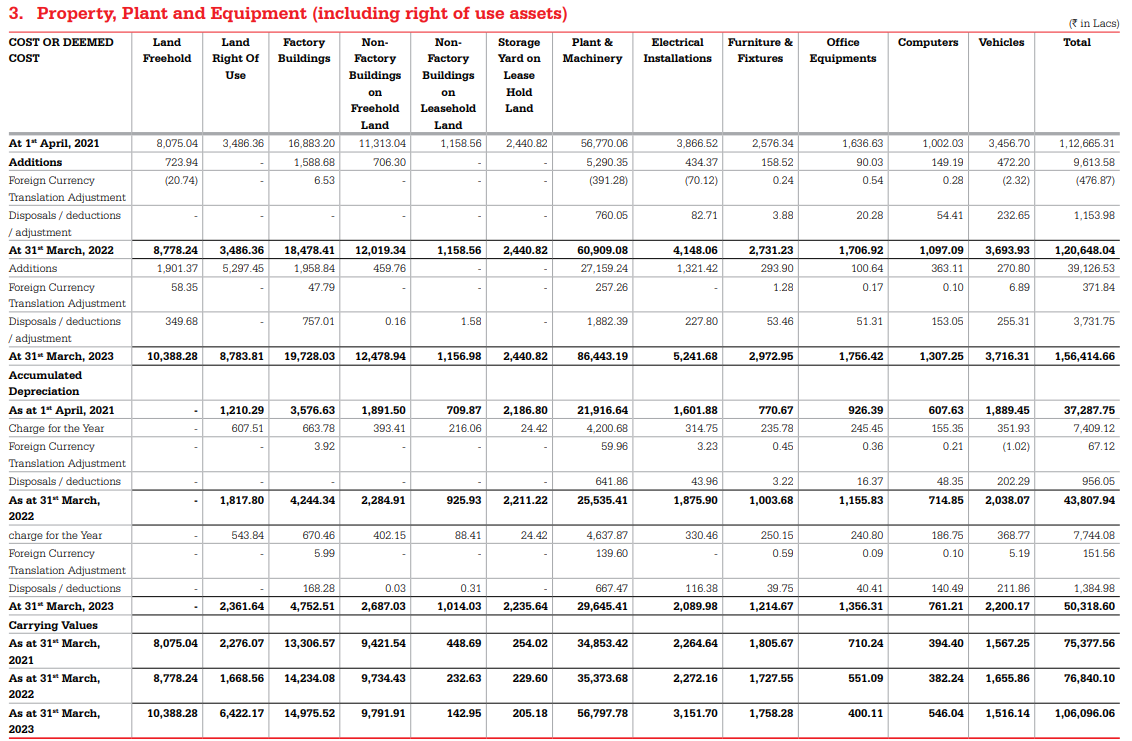

@basumallick I have done a basic forensic analysis but I have a doubt about one thing

Cumulative investments in Fixed assets from FY14 to FY23 is 1974 crores but the gross block difference from FY23 and FY13 is 1163 crores… Where is there a difference of 70% in both these amounts? Shouldn’t the difference be more or less equal to the amount spent on acquiring fixed assets?

What about depreciation? Could that explain the whole difference?

You are not factoring disposals and obsolence or write-off from books as they have been completely depreciated.

PS: Lastly forex

Example:

The gross block is reported before depreciation. We subtract accumulated depreciation from it to reach the net block figure.

Oh cool, thank you so much for this information.

But still why too much difference? Is the company acquiring and disposing of assets in a short span of time?