Hi, is anyone tracking this company closely? The stock has been down for a long time. I heard that company is good. But now there is lot of local competition in term of non-branded plywood. But still people who wants branded plywood will go for century plyboard. Another feedback I heard from one of my relative who is a woodwork contractor is that Century has so many options to choose from that people get confused. I am not sure if it is a good thing or bad. Anyone see any other challenges with the company?

The company has recently put up capacity in MDF and the offtake is in the process of stabilizing. They are planning to add more capacity in MDF in the near future. Also, Century is a end-to-end play in the home furniture market as they are in plywood, MDF and laminates, unlike Green, which has 2 separate listed entities for ply and laminates.

The overall market has been subdued as the real estate market is down. Major pickup possibly will happen once real estate picks up. Secondly, the company has now started moving aggressively into tier-2 and tier-3 cities to expand their distribution footprint. This should help but will have a lag effect, maybe after a couple of years.

They are also now focusing on the mid-market segment with their Sainik brand and they will be mostly pushing this brand in the tier-2 and tier-3 cities.

Having looked at both Greenply & Centuryply, it seems to me that:

a. Greenply’s focus is on its MDF products, trying to capture the low end of the plywood market by replacing it with MDF. Its premium products are doing very well anyway and the recent capex focus has been on MDF.

b. Century’s focus is on capturing the unorganised mid-segment plywood market (which is almost 50% of the total plywood market) through its Sainik brand.

c. The EBITDA margins for both are shrinking due to their focus on mass market products.

In Greenply’s case EBITDA is shrinking due to overcapacity in MDF market (13 lakh cu. meter per year total capacity + 3.2 lakh cu. meter of imports) and lower capacity utilisation due to its big new MDF plant in South India. Greenply itself has about 5.4 lakh cu. meter capacity per year (In Oct 2018 it commissioned a plant of 3.6 lakh cu. meter per year capacity.)

In Century’s case EBITDA margin is shrinking due to its focus on reaching out to the bigger mass market & price compromise. Their thesis is that with GST the gap between organised and unorganised prices has shrunk to 20% to 25% and thus those buying mid-segment unorganised ply would consider a branded better quality ply at a slightly higher cost.

d. My query to those invested in Century Ply is what is the trigger for growth and higher bottomline? When the sluggiesh real estate market will turn is anybody’s guess. The effort to capture mid-segment is a long haul one and may or may not work out. At current valuations it seems to be a decent business but I’m unable to envision, with conviction, how the company is going to grow its top line and bottom line significantly?

@jprasun You are right. This will be a long haul. In the short term, it seems unlikely that either Century or Green will be able to pull the rabbit out of the hat in terms of growth. The bet is on the longevity of growth, since the opportunity size is very large. With GST coming in, we are slowly seeing a formalisation in the sector, though not as fast as we would want to.

With urbanisation, the need to first-time furniture and replacement furniture will be sustained for a long time. Since, everyone is expanding on MDF capacity now, there is an oversupply situation. Once the oversupply in the MDF segment reduces, the price realization should improve. But t may take a few years for that to happen.

Management expects rapid growth in laminates segment to continue with 15% revenue growth in FY20 and a 14% margin.

The plywood segment’s revenue growth is likely to remain muted at 2–3%.

MDF segment can post a healthy revenue growth of 20% with a 20% margin.

Particle board is likely to report 10% revenue growth with a 25% EBITDA margin.

The real estate scenario continues to worsen, and the company is hopeful of strong growth once the macroeconomic environment improves.

The company remains confident of the shift from unorganised segment to organised segment upon strict implementation of GST.

Greenfield capacity expansion at UP: Given optimum capacity utilisation of its MDF and particle board plant, CPBI is planning a greenfield expansion for MDF and particle board in UP. The company is working on the project and is yet to announce the final details of the plant. With the licence already in place, the company is working on finding suitable land.

Laos uncertainty continues: The company has invested INR762.5mn in Laos for raw material security. According to communication dated 10 June, 2019, the Laos government has asked to ensure production of finished goods, i.e. plywood instead of face veneer. Management has shared a proposal with the Laos government for manufacturing of plywood at Laos along with sale of remaining veneer from the country. If the country does not agree, management believes only selling plywood from Laos will be a loss-making business and it will thus have to exit these projects.

Gabon likely to get commissioned in FY20: Management is adding capacity in Gabon and believes the cost of procuring face veneer would be lower (-30% compared to Garjan) than sourcing it from other countries. The facility – being set up at total cost of INR200–250mn – is likely to start production from February or early March 2020.

CPBI decided to take an impairment loss of ~Rs 460mn on Laos operations

during the quarter. The company continues to explore ways to use this plant

but felt it prudent to book the loss now.

The company has improved its working capital cycle sequentially by 6 days.

Management expects 5-6% revenue growth in FY20 with blended operating

margins of 16%.

Plywood

A subdued real estate market is dampening growth.

Management expects the plywood segment to be flattish in FY20 due to

pressure on the face veneer market. Operating margins are guided at ~13%.

For FY21, core plywood is guided to grow in mid-single digits aided by

recently launched loyalty programmes, whereas face veneer should also see

some uptick due to commissioning of the Gabon facility.

The face veneer facility in Gabon will be operational by Apr’20 against the

earlier planned Q4FY20. The company has delayed the expansion as veneer

prices have fallen in India.

Formalisation of the sector post-GST is not panning out as expected given

that weak enforcement is leaving unorganised players free to operate as they

did prior to GST implementation.

Laminates

The laminates segment had posted weak growth in Q3 due to a high base.

Exports account for ~25% of laminate segment turnover.

The company is hopeful of achieving 13% value growth in this segment with

13% margins in FY20.

MDF

CPBI believes that the MDF unit can be ramped up to 115-120% capacity

utilisation and is working with a consultant to achieve this goal.

Plans are underway to set up a new MDF facility in Uttar Pradesh post a court

decision on the matter. This new facility will have fungible capacity between

MDF and particle board and will take 16-18 months to build.

The total capex envisaged for the new plant is Rs 4.5bn-5bn to be funded

from internal accruals and debt.

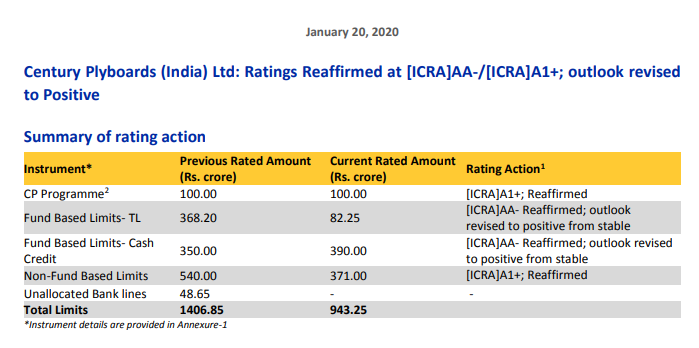

Century Ply’s rating is done by ICRA and not CRISIL. Crisil was its former ratings agency. So, it is standard industry practice for CRISIL to put out a report of non-cooperation.

No fancy words no fancy graphic simple numbers a great presentation of results .Organised sectors are the eating unorganised sector bit and bytes and the opportunity of the sector is more than 20000 cr growing around 9 to 10% per annum …

There are no unorganised players in plywood industry. There are big players and there are small players. This unorganised to organised story has been peddled by management in every concall since the demon and GST days, but nothing has come out of it.

What is bearing fruit for Century is their foray into MDF and lower cost Sainik brand ply.

Centuryply reported consolidated revenue of Rs522 cr, 12.9% lower over 2QFY20 revenue of Rs599 cr but was ahead of our estimate of Rs486 cr. Company witnessed gradual increase in revenue in 2QFY21 with September 2020 revenue being almost similar to revenue reported in September 2019. Amongst segments, medium density fibreboards (MDF) reported strong growth in revenue and particle board segment revenue decline was 2%. Plywood and

laminate segment reported higher yoy decline.

Plywood segment – Revenue in the plywood segment declined by 15% yoy to

Rs268 cr on account of 12% yoy decline in plywood volumes. In 2QFY21, plywood demand pick-up has been gradual post Covid-19 related lockdown.

Management highlighted that the sequential recovery in demand is on account of pent-up demand and introduction of new technology (Virokill) in their inhouse manufactured plywood and laminates.

Laminate segment – Company reported revenue of Rs102 cr in the laminate division – 25% lower yoy due to 22% yoy lower sales volume. Average selling price (ASP) in this segment was lower by 5%. Both the domestic and the export geographies witnessed yoy decline in revenues. Decline in domestic market was steeper than decline in the export market. Management indicated that the laminate demand generally follows plywood demand with a lag. Plywood revenues were down by 15% yoy in 2QFY21.

MDF (Medium-density fibreboard) segment – MDF revenues grew by 20% yoy to Rs94 cr due to sharp improvement in demand and lower base of last year. Overall MDF volumes were higher by 19% yoy. Recovery in the MDF segment has been sharper as compared with other segments on account of strong demand for ready-made furniture market.

Particle board segment – Demand improvement in this segment has also been relatively better than the plywood and laminate segment. In this segment, revenue was down by 2% yoy on a higher 2QFY20 base. While plain particle board revenue was lower by 36% yoy; the prelam particle board segment saw revenue decline of 17% yoy.

Logistics – Revenue in this division declined from Rs21.9 cr in 2QFY20 to Rs19.8 cr in 2QFY21. Decline in revenue was on account of 18% lower Container Freight Station (CFS) volumes yoy.

Consolidated EBITDA in the quarter stood at at Rs87 cr in 2QFY21 as against Rs92 cr in 2QFY20. EBITDA margin improved from 15.4% in 2QFY20 to 16.6% in 2QFY21. Strong operational performance can be attributed to control over cost and strong growth in MDF segment. As against 13% yoy decline in revenue; employee cost and other expenses declined by 14.2% yoy and 15.7% you respectively. Gross margin increased yoy from 50.7% to 51%. MDF segment EBITDA margin increased from 23.2% in 2QFY20 to 28.1% in 2QFY21.

Furthermore, EBITDA margin in MDF segment is higher as compared to plywood/laminate and higher share in the revenue mix yoy supported overall increase in EBITDA margin. Interest cost declined yoy and qoq due to reduction in debt. Company’s debt declined from Rs243.5 cr in 1QFY21 to Rs85.1 cr in 2QFY21. Company reported consolidated net profit of Rs50 cr in 2QFY21 as against Rs48 cr net profit in 2QFY20 and net loss of Rs11 cr in 1QFY21.

Financial Results Update for the Quarter AND NINE MONTHS ended 31St DECEMBER, 2020 : excellent presentation on numbers one must read it .( i am not saying numbers are good but the way put the data is really good )