CenLube Industries:

CMP:56.50

MCap: 23.28Cr

Consolidated March 2017: Sales: 35.53Cr, Net Profit: 1.74Cr

http://www.cenlub.in/

Annual Reports

Lubrication is a prime requirement for all machines, equipments or plants as it adds to the life and efficiency of the the machine by reducing wear and tear of its parts. The lubricating oil forms a film between the moving parts which results in lesser friction and correspondingly less heat generation in the machine, thereby keeping the working temperature of machine parts within safe operating limits. Wear and tear of parts is thus greatly reduced resulting in fewer breakdowns, greater machine utility, lower maintenance cost and longer machine life.

Cenlub Industries Limited, a Public Limited Company having its registered office at Plot No. 233-234, Sector-58, Ballabgarh, Faridabad - 121 004, Haryana. Basically the company is in the field of design, manufacture and supply of Centralised Lubrication System for various Machines, Plants and Equipments.

Registered office / Plant-1

It is a listed company at Bombay Stock Exchange incorporated under the Companies Act, 1956 by Registrar of Companies, Delhi & Haryana in the year 1992.

The company has been promoted, mainly, by Mr. V.K. Mittal , Managing Director - a Mechanical Engineer with M.Sc. (Physics), M.Sc. Mech. Engg. specialization in Machine Tools from Moscow. He has worked at senior position in TELCO for more than a decade. He started working on import-substitution of lubrication systems for machine tools in 1977 and has been instrumental in making the company a profitable concern in this field. In recognition of his capabilities, Haryana Government bestowed “Prize for Enterpreneurship” on him for 1987 - 88. He has widely travelled overseas and is fully aware of the latest trends in this field.

The company has 17 offices all over India to take care of Sales and Service i.e. Aurangabad, Ahmedabad, Bangalore, Bhuvaneshwar, Dhanbad, Chandigarh, Chennai, Coimbatore, Faridabad, Hyderabad, Jamshedpur, Kolkata, Mumbai, Pune, Rourkela, Rajkot and Visakhapatnam.

The company is having 3 manufacturing units as under, which are totally independent:-

The total number of employees are around 225.

The company has its own proprietary items of Lubrication Pumps and Accessories and most of them are existing for the last 35 years.

The company has the capability to take turn-key projects from concept to commissioning. These projects are basically related to Plant Lubrications for Steel, Power, Paper, Sugar etc. which are normally approved on blue print stage before taking up for manufacturing.

The company has bagged the following prestigious awards :-

“FIE foundation” award for import substitution activity at IMTEX’86 exhibition.

Transworld Trade Fair “Gold Medal” selection award in the year 1987.

“Entrepreneurship” award by Government of Haryana in the year 1987-88.

“Best display” award in the 9th Indian Engineering Trade Fair in the year 1991.

“Business Sphere” award for the year 2008-2009 for most respected No.1 Company in Lubrication System.

“Udyog Ratan” award by Institute of Economic Studies (IES) in the year 2009.

Client lists is like the who-who’s of indian industry:

Machine tools:

ACE DESIGNERS, ACE SYSTEM, ALEX,BATLIBOI,BFW,CADMACH,EMTL (ELECTRONICA MACHINE),GALAXY,GEDEE WEILER,GH INDUCTION, HARISH,HEC,HILDEN, HMT, IMPACT, ISGEC, JYOTI CNC, LMW,LOKESH, MAC POWER, MARSHALL, MICROMATIC,NUGEN,PARI, PMT, PRECIHOLE, PREMIER, SCARLO, TAL MANUFACTURING, WINDSOR, ETC.

Steel Plants:

ADHUNIK METALLIC,ARMECH,BEEKAY ENGG.,BHUSHAN STEEL, BHUVEE PROFILES, BHUWALKA STEEL, ELECTROSTEEL CASTING, ELECTROSTEEL STEELS, ESSAR STEEL, GRADUATE AGRO, H.N. CONSTRUCTION, HULAS STEEL INDS., INDIAN METAL FERRO ALLOYS, ISPAT METALLIC, JINDAL ISPAT STEEL,JINDAL STEEL- HISSAR, JINDAL STEEL-RAIGARH, KINNERA STEEL, KUDERMUKH IRON & STEEL, LLOYDS STEEL,LOI WESMAN, MAHARASHTRA SEAMLESS, MAHINDRA UGINE, MALVIKA STEEL, MIDEAST INTEGRATED STEEL, MUKAND, MULTIFORM MACHINERY, REMI METAL, RENUKA EQUIPMENTS, REYMONDS STEEL, ROLLCON INTERNATIONAL, SAIL - ALLOY STEEL PLANT, SAIL - BHILAI STEEL PLANT, SAIL - BOKARO STEEL PLANT, SAIL - DURGAPUR STEEL PLANT, SAIL - INDIAN IRON & STEEL CO., SAIL - ROURKELA STEEL PLANT, SAIL - SALEM STEEL PLANT, SAIL - VISVESVARAYA IRON & STEEL, SARDA ENERGY & MINERALS, SUNFLAG IRON & STEEL, TATA METALLIC, TATA STEEL GROWTH SHOP., TISCO, TRF, TUNGBHADRA STEEL, UNITED SEAMLESS TUBULAAR, VIDYUT METALLICS,VISAKHAPATNAM STEEL PLANT, WELSPUN STEEL, ETC.

Sponge Iron Plants:

A.S.R. MULTIMETALS,ACTION ISPAT & POWER, AGNI STEEL,AIRAN STEEL & POWER, AMBAY SPONGE, AMOD SPONGE, ANAND ISPAT, ANIDITA TRADE & INVESTMENT, ANKIT METAL & POWER, AYARSE PLC, ETHIOPIA, BASAI STEEL, BHAGWATI SPONGE, BHASKAR STEEL, BIMALDEEP STEEL, BINDAL SPONGE, BMM ISPAT, BS SPONGE, CP SPONGE IRON, CREST STEEL & POWER, DAMODAR ISPAT, EVEREST IRON & STEEL-ETHIOPIA, GAGAN RESOURCES, GRACE INDS. LTD., GREWAL ASSOCIATES, HIMA ISPAT, HINDUSTAN CALCINED, HI-TECH MINERAL, HYDERABAD INDS., IDCOL KALINGA IRON, IND AGRO SYNERGY, IST STEEL & POWER, JANKI CORP LTD., JHARKHAND ISPAT, JINDAL SPONGE, KHETAN SPONGE, KOHINOOR ISPAT AND POWER, LAKSHMI GAYATRI STEEL,MA CHHINNAMASTIKA STEEL, MA SAMLESHWARI, MAA CHINNAMASTIKA ISPAT, MAA MAHAMAYA INDUSTRIES, MONNET ISPAT LTD., NAVKAAR ISPAT, NR SPONGE, OCL, PADMAVATI FERROUS, PHIL ISPAT PVT. LTD.,PT DELTA, INDONESIA, RAIGARH ISPAT & POWER, RAJURI STEELS & ALLOYS, RASHMI METALIKS,REACTIVE METAL, REAL ISPAT, RELIABLE SPONGE IRON, RLJ CONCAST, RUNGTA MINES, S.K. SARAWAGI & CO.,SAI SINDHU SPONGE IRON, SATYA POWER AND ISPAT, SEN FERRO ALLOYS, SESHA SAI ISPAT, SHIVALAY ISPAT & POWER, SHREE BAJRANG POWER & ISPAT, SHREE METALLIC, SHREE NAKODA ISPAT, SHREE RADHA INDS.,SHREE SHIVSHAKTI STEEL, SHYAM STEEL, SMC POWER, SUMI VAYAPAAR, SUNVIK STEEL, SURANA INDUSTRIES, THAKUR PRASAD SAO & SONS, TIRUPATI UDYOG, TRIMULA SPONGE IRON, USHA MARTIN, VENKATESHWARA SPONGE, VIJAYA SPONGE & ISPAT,VINAYAK STEEL, ETC.,

Cement Plants:

ABG CEMENT, ACC, BHAVYA CEMENT, BINANI CEMENT, CHUNAR CEMENT (JAYPEE),DALMIA CEMENT - ARIYALUR, DALMIA CEMENT - DALMIA PURAM,DALMIA CEMENT - KADAPPA,ECO CEMENT, FALCON - BEHRAIN., GRASIM CEMENT, GUJARAT AMBUJA, J.K. CEMENT, JAYPEE BALAJI CEMENT, KAMDHENU CEMENT, KARCEMENT, KAZAKHSTAN, LAKSHMI CEMENT, MADRAS CEMENT, MAIHAR CEMENT, MILLENIUM CEMENT, ORIENT CEMENT, PRISM CEMENT, SAGAR CEMENT, CEMENT, SHREE CEMENT, STAR CEMENT, ULTRATECH, VASAVADATTA CEMENT, VIKRAM CEMENT, ZUARI CEMENT, ETC,

Sugar Plants: We are the original equipment supplier to Sugar Plant machine manufacturers such as ISGEC, KAY IRON, CIMMCO, TRIVENI etc. We have already supplied our lubrication systems to various major Sugar Plants in India as well as abroad and some of them are:

ACUCAREIRE XINAVANE, MOZAMBIQUE, AMR SANGAM SUGAR, AP SUGAR, BAJAJ HINDUSTAN, BIJNORE SUGAR MILL, CHADHA SUGAR MILL, CHANDPUR SUGAR MILL, CONSOLIDATED FARMING, ZAMBIA, D. S. M. SUGAR MILL, DALMIA SUGAR, DAURALA SUGAR, DHAMPUR SUGAR MILLS, DSCL SUGAR, EASTERN SUGAR, NEPAL, ENERAGRO PROJECT, ECUADOR, HUTATMA KISAN AHIR SAHAKARI, INDIAN CANE POWER, J.K. SUGAR, JAY MAHESH SUGAR,KAMLAPUR SUGAR MILL, KHOTOLI SUGAR, KISAN SAHKARI CHINI MILL, LOKMANGAL SUGAR, MAWANA SUGAR, MODI SUGAR, MUKERIAN SUGAR, MUZAFFARNAGAR SUGAR MILL, NANDGANJ SIHORI SUGAR MILL, NORTHLAND SUGAR, PALWAL SUGAR MILL, RAMGARH SUGAR, RAVALGAON SUGAR, RELIANCE SUGAR, NEPAL, SAKHOTITANDA, SAKTHI SUGAR, SARASWATI SUGAR MILLS, SARAYA SUGAR MILLS, SHAMBAHOLI SUGAR MILL, SHREE TATYASAHEB KORE WARANA, SIEL SUGAR, SRI RAM SUGAR MILLS, NEPAL, SUGAR CORPORATION, UGANDA, SUPREME RENEWABLE ENERGY, SYAN SUGAR, TITAWAI SUGAR, ETC

Power Plants:

ADAMTILLA, ADHUNIK TPS, ADITYA MAHAN, AMARKANTAK, ANPARA TPS, APGENCO RAMAGUNDAM PS, AZARBIZAN HEP, BAIRA SIUL, BAJAJ HINDUSTAN, BAKRESWAR, BANSAGAR, BARAGRAN, BASKANDI, BHOOPALAPALLY THER.POWER, BHUSAWAL TPS, BUDGE-BUDGE, CHAMERA, CHANDIL, COAL INDIA,DB POWER, DEHARKHAND, DVC- CHANDRAPURA, DVC DURGAPUR, GANGUWAL, GGSR BHATINDA, GIRAL LIGNITE POWER, GNTPS, BHATINDA, GOKAK FALL HYDRO, GUNGWAL & KOTLA, GGS REFINERY(CAPTIVE POWER), HARIDWAGANJTPS, HARINAGAR, IOCL - PANIPAT, JINDAL DERANG, JPL RAIGARH, KALI NADI, KAPHERKHEDA TPS, KHADANA, KHANDONG, KODERMA TPS, KOPILI, KOTLA, KUTTIYADI, MALANA, MATHON TPS, MODIPONE, MUKERIAN, NAJHARI, NTPC ARAVALLI, NTPC BONGAIGAON, NTPC DADRI, NTPC ENNORE, NTPC MAUDA, NTPC NABI NAGAR, NTPC RIHAND, NTPC SIMAHDHRI, NTPC VINDYACHAL, PARAS TPS, PARBATI, PARLI TPS, RAICHUR TPS, RAIPUR POWER N ISPAT, RAJGHAT, RANJIT SAGAR, REL DAHANU, RELIANCE ENERGY, ROURKELA STEEL PLANT, ROURKELA TPS, SANTHALDI TPS, SANTHALDIH TPS, SARAVATI HYDRO ELECTRIC, SARDAR SAROVAR, SATPURA, SHREE SINGAJI, SIKKA TPS, TALA, TAMILNADU STATE ELECTRICITY BOARD, TATA JOJOBERA TPS, UKAI TPS, VASANTHARAO DADA PATIL SSK, VIJAYAWADA THERMAL POWER, VIKAS SSK, ETC

Paper Plants/Mills:

ANDHRA PAPER MILL, BINDLAS PAPER MILL, CENTURY PAPER MILL, GRD PAPER, ITC- BHADRACHALAM, K.R. PULP & PAPER, MADHUBATI PAPER MILL, MAGNUM VENTURES,MECANO PAPER, MOHIT PAPER MILL, MUKERIAN, MULTIWAL PULP & PAPER, ORIENT PAPER MILL, RAMA PAPER MILL, RAMA SHYAMA PAPER, SATIA PAPER, STAR PAPER MILL, UNITED PAPER MILL, ETC.

Miscellaneous:

BALMERLAWRIE, BOSCH, DANIELI,DLW, FL SMIDTH, GODREJ, HINDALCO, HONDA MOTOR, HUMBOLT, HV TRANSMISSION, KIRLOSKAR BROTHERS, L&T, KANSBAHAL, L&T POWAI, LEITNER SHRIRAM, MAHINDRA & MAHINDRA, MOHIT PAPER MILL, MARUTI, NUPOWER, PAHARPUR COOLING TOWER, PARADEEP PHOSPHATE, PP ROLLING, PRAJA MECHANICAL, RCF, RENUKA EQUIPMENTS, RIETER, SAMKRG PISTONS, STEEL STRIPS, TOSHIBA MACHINE, VAYUNANDANA,VELJAN, WMI KONECRANES, ETC

Exports to Countries: Initially for two decades the company was busy in catering to the Indian market and prior to the inception of the company, basically lubrication units were imported. Having catered efficiently the Indian market, the company started contributing to the world market. Now the company is exporting its products to :- BAHRAIN, DUBAI, ETHIOPIA, FINLAND, GERMANY, HOLLAND, HONDURAS, INDONESIA, IRELAND, ITALY, KENYA, MALAYSIA, NEPAL, PHILIPPINES, SAUDI ARABIA, SHARJAH, SOUTH AFRICA, SRI LANKA, TANJANIA, THAILAND, UGANDA, USA, VIETNAM, ZAMBIA, ETC.

Balance Sheet

Income Statement:

CashFlows:

Company seems to be very small considering the client base… so either there are other ways the company management seems to take out benefits … else the client list is rock solid… Capital investment for March 2016 is 3.5Cr out of which 3.4Cr is in buildings… 1Cr invested as advance for flat at Noida and Faridabad, 45 lakhs for a flat in banaglore, so company is moving into the business of property management…

March 2015 3.2Cr spent for plot in Faridabad … wonder where that went in 2016?..

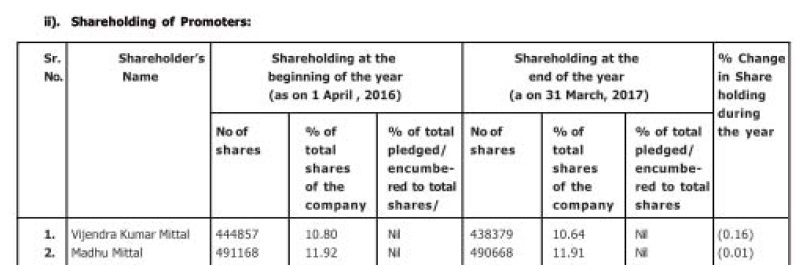

Latest announcement 13 July 2017 to BSE indicate that the subsidiaries and associates have been merged with CenLube Industries. ie. MiniHyd Hydraulics Limited & Ganpati Handtex Pvt limited. If you look at the consolidated data subsidiaries will add additional debt burden to CenLube and zero topline… which is negative but consolidation of nonlisted associates and subsidiaries should result in increase in promoter shareholding… and hopefully better disclosures and higher EPS in the future…

Conclusion: Cenlube Industries and many similar small/microcap companies which are market leaders are feeling the pressure of Modi-nomics. better income disclosure, tightening of loans by basel-III also is reducing the possibility of nonlisted entities from getting credit… if you dont have sufficient income it will be difficult to get credit lines from banks… I expect Cenlube to start reporting “realistic numbers” which should translate to higher topline and bottomline and higher stock prices… Since the merger of associates and subsidiaries is after July we will have to wait for September shareholding data to see how much the promoter shareholding has increased…over past 5 yrs promoter shareholding has increased by 2% I would recommend “BUY Now” as company is undiscovered and still very attractively priced…7-8Cr cash in hand 23.8Cr market cap…its attractively priced… and actual sales numbers and profits should improve in the future.