This receivable explanation is not good then. Unbilled receivables bucket will not be empty, implying from now on receivables will be rec + unbilled receivables. Thus to maintain high growth, rec will remain elevated. Is my understanding correct?

Thats expected since they are executing two large 300 crores projects over next few quarters .Explanation is perfectly good for the kind of business it is .

4 Likes

115 + 6 = 121 Cr

10 Likes

12 Likes

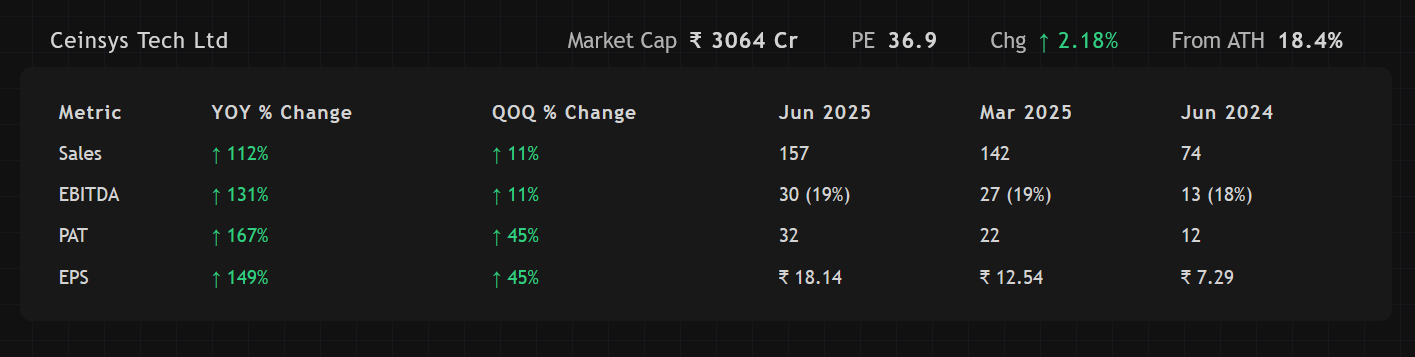

Q1 FY26

Performance

Concall Notes

- Total order book stands at INR 1,209 crores as on June 25, 2025.

- EBITDA margins for Technology Solutions are around 30%, while for Geospatial services they are around 15-16%.

We are focusing on both, but obviously, greater focus remains on development of technology solutions, and that can also be seen from the fact that quarter 1 of last year our turnover on the technology solutions was INR31 crores, and this quarter it is INR84 crores. So it’s more than double.

- Operational cash surplus is INR 127 crores.

- Unbilled revenue for the quarter is approximately 50% of the total revenue of INR 157 crores.

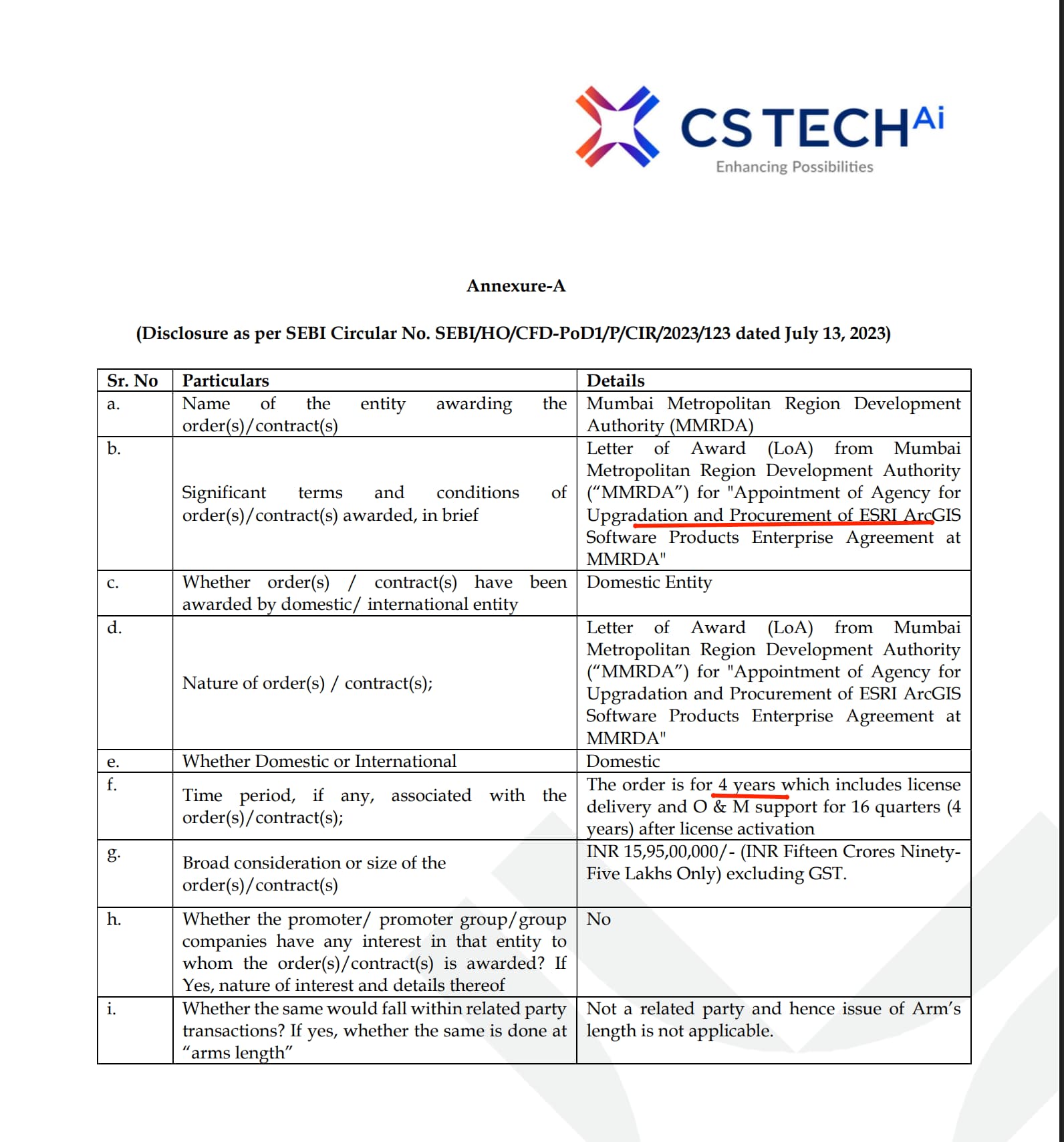

- The company secured a new MMRDA contract worth INR 115 crores for system integration.

- International revenue for the quarter was INR 7.5 crores.

- The tax rate was minimal in Q1 due to a reversal of an INR 8 crore excess provision from the previous year; the normalized tax rate is 22%.

- Operating Leverage: The employee cost as a percentage of revenue declined to 23% in this quarter from 35% on the corresponding quarter of last year.

- A government audit of the Jal Jeevan Mission caused a temporary hold on new order awards, impacting the company’s Q1 order inflow.

- The company is actively identifying targets for inorganic growth to expand in existing domains and has mobilized almost USD 28 million for M&A in geospatial and engineering services.

- Two M&A targets are currently in the due diligence phase, both in the geospatial vertical but with new technologies that CS Tech does not currently possess. Both serve US and Europe.

- An investment of INR 10 crores was made and expensed in Q1 FY26 for U.S. market expansion and business development.

- The company aims to shift its revenue mix from the current 70-30 (India-International) to 40-60 or 30-70 within the next 3 years.

- A new vertical focused on AI-ML, and embedded electronics has been created to develop applications and solutions for existing domains.

- The appointment of Surej K.P. as CEO (taking over Jan 1, 2026) is a key part of the strategy to drive international growth, both organically and inorganically.

- Domestic revenue mix: 85% B2G and 15% B2B.

- The company maintains a 2-year order book visibility (or 18 months, accounting for growth).

- EBITDA to cash flow conversion was high in Q1 FY26, with INR 27 crores of cash flow accretion from a net EBITDA of INR 30 crores.

Risks & Concerns (Personal View):

- Delays in securing large orders, particularly from the Jal Jeevan Mission, which is undergoing a government audit. This caused a miss on previously guided order inflow. Demand from the Jal Jeevan Mission is expected to resume in Q2/Q3 after a temporary pause for a government audit.

- The Vidarbha River linking project execution started slower than anticipated due to delays from the government’s side.

- M&A timelines are subject to uncertainty. Management notes that ‘timeline typically doesn’t stay as optimistic as we would love to’.

- High dependence on government business (85% of domestic turnover) poses a risk of delays in execution and payments, although management states they have not faced bad debts.

- The company’s strategy to diversify risk by increasing international business is a multi-year plan (3 years) so in the meanwhile the B2G risk remains.

Q4 FY25 Guidance Status

-

Target to achieve INR 300-400 crores worth of new order book every quarter. [Not Met]

- Q1 FY26 new order inflow was approximately INR 169 crores, below the guided range. Management attributed the shortfall to a temporary hold on Jal Jeevan Mission projects due to a government audit.

-

Expect due diligence for two M&A targets to be completed by April or May 2025. [Delayed]

Disclaimer: Invested & Biased.

27 Likes

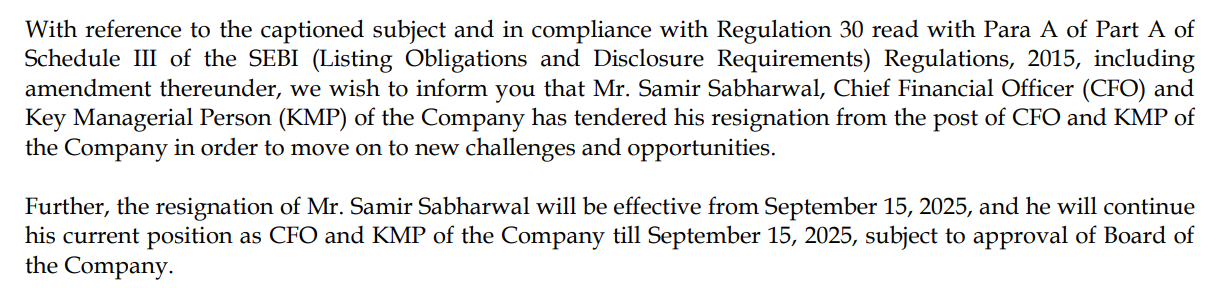

Ceinsys Tech Ltd. announced the resignation of Mr. Samir Sabharwal from his role as Chief Financial Officer (CFO) and Key Managerial Personnel (KMP). His resignation will be effective from September 15, 2025. The company stated that Mr. Sabharwal is leaving to pursue new opportunities.

Should the sentiment be neutral or are we looking for some short term correction?

3 Likes

26 Likes

Ceinsys is the probable AOC for the installation of water meters, further strengthening its presence in the water sector. The company has prior experience in this domain, having successfully executed similar project in Thane: Smart Water Meters - Thane.

16 Likes

Hi, few questions – where did you check this and has this been announced on the exchange?

It’s available on public tender portals, but I haven’t come across any announcement on the exchange yet.

2 Likes

I am reading through the AR and some of my observations:

- Reading through the overall vision and direction from board, it is quite surprising to see no mention of data center services business that they talked about different calls last year i.e. they are looking for DC services and not that requires any capex/physical DC setup. This is more so when a new CEO mainly from the DC/Hyperscalar background is being onboarded for future growth and no mention in AR in the direction of utilizing his expertise in this area.

This is what the statement from Mr Kamat says about future (no mentions of DC services or relevant areas).

-

I getting a sense from details / intentions mentioned at various places in AR and the level of details of reporting (to exchanges/investors) about various aspects, that the company strongly focuses on good corporate governance and the team is making efforts in this direction. There is a focus on integrity, good governance, good investor relations and in turn efforts towards becoming a global standards fostering company. This is a good sign which will help company achieve the global leadership position in the industry.

-

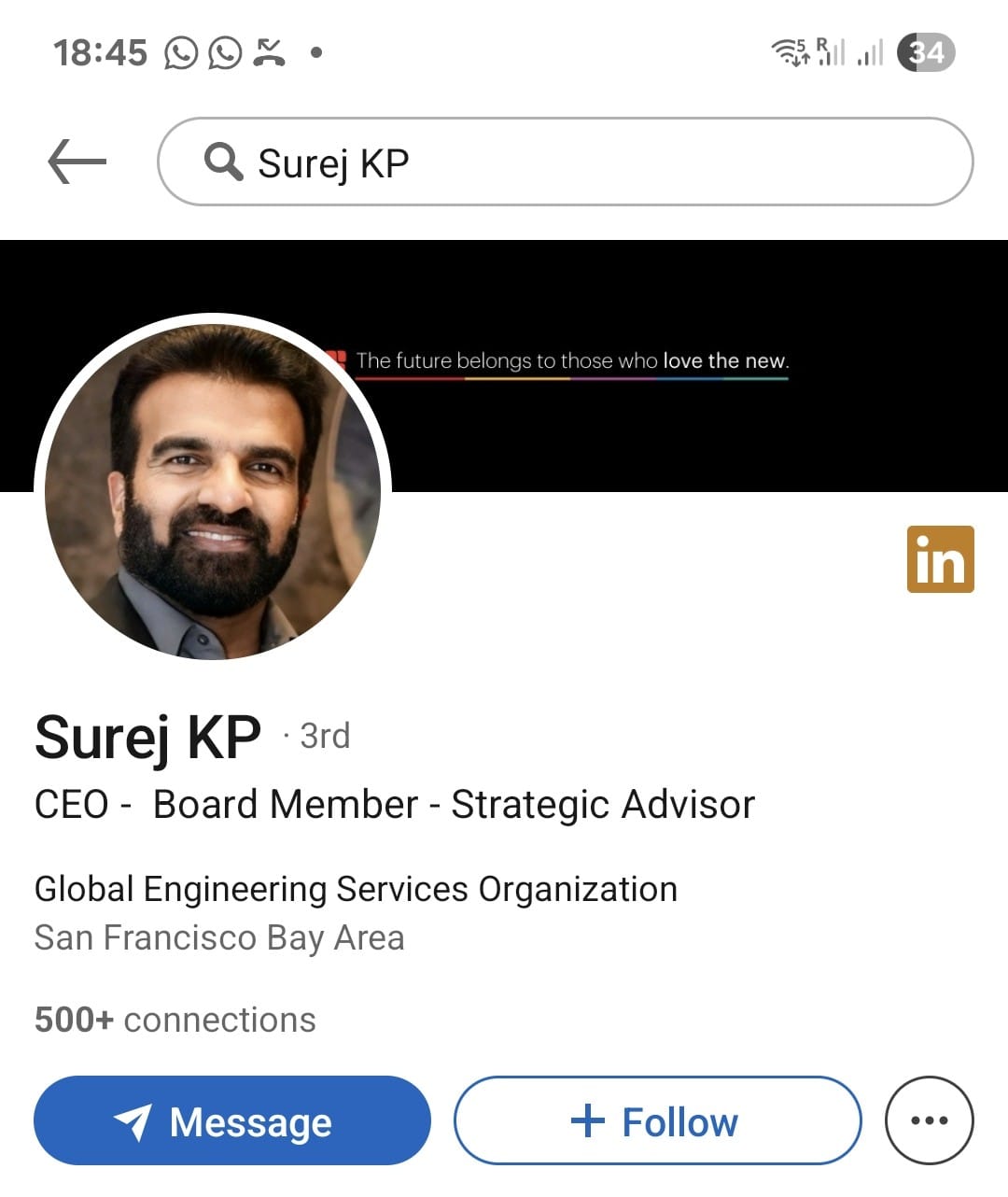

Not relevant but just an observation that the new CEO, Surej has not mentioned the name of the company in his Linkedin profile, while he had mentioned the same when he was with Intelliswift. Not sure what stops him from doing this. As @phreakv6 has mentioned on other thread his musing " a valley guy who ran a 1000 Cr+ PnL (Surej KP of Intelliswift) would join here as CEO", can there be any relevance?

Disc: Not invested. Tracking closely for taking position.

They initially said investment in data center alongside geospatial and technology solutions domains and then later said they are not going to do it.

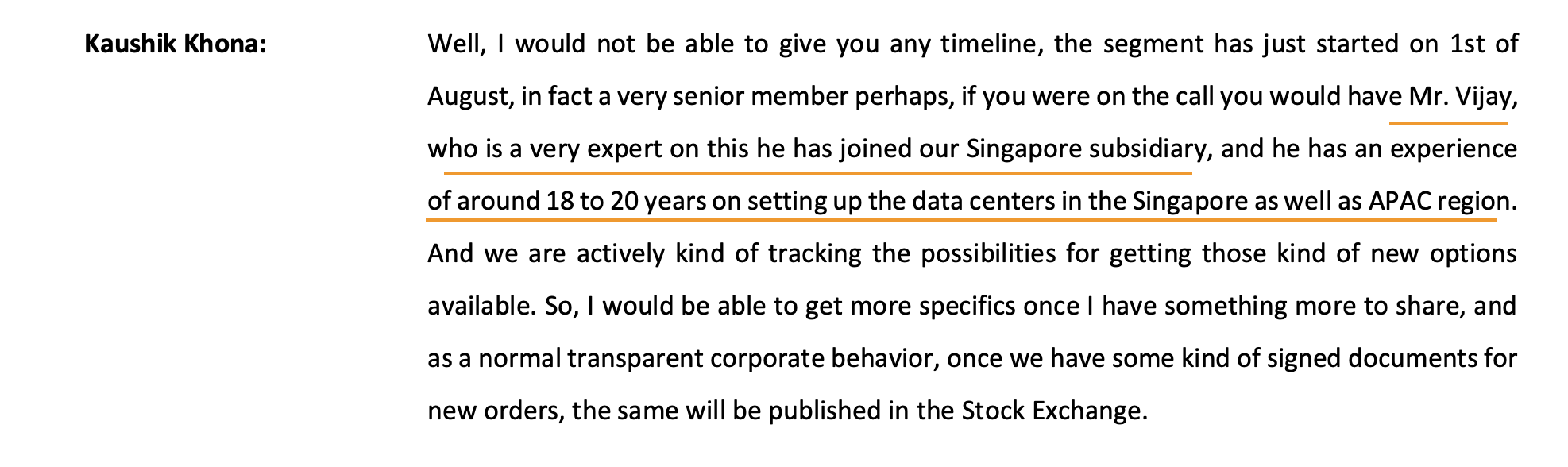

This is the initial mention in Aug '24 call. They mentioned having hired a senior resource.

This Vijay should be the same one who has since then founded Advanzit. The reason am confident is most of the people in this company are ex-Rahi. This company was founded in March '25. I am not sure if acquisition plans are still on or fell off but this one is a high likelihood candidate for acquisition in this space if it does happen. The sort of work they do also is exactly what was described in the earlier calls.

You can see the sort of work this company does

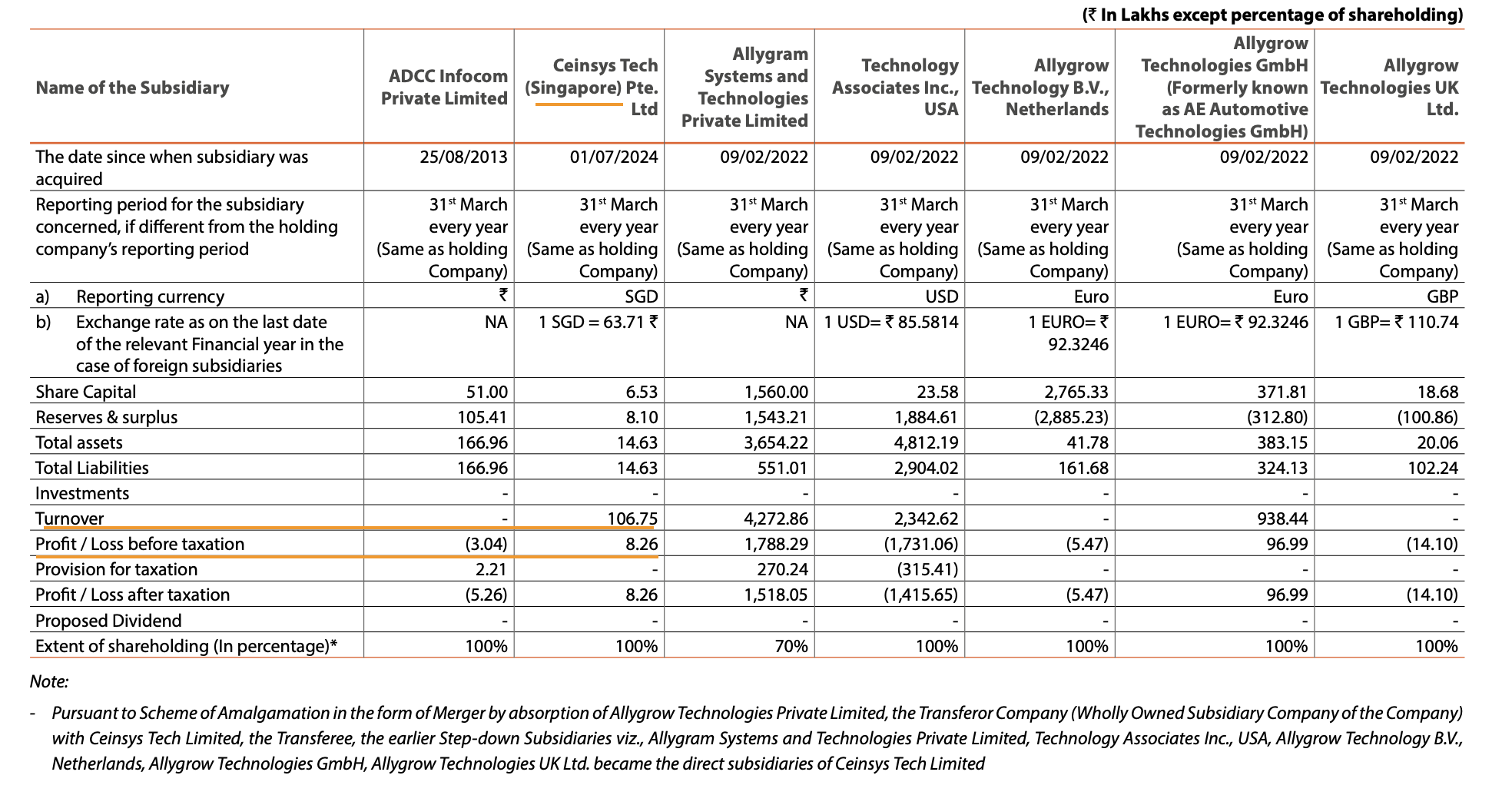

Another interesting thing I noticed is this Singapore subsdiary having 1 Cr turnover and 8 lakhs profit. There shouldn’t be any business here if they abandoned the data center plans. My guess is Advanzit it is being funded by Ceinsys Singapore subsidiary until acquisition and numbers are recorded informally. There are negligible declared assets. The people hired are deeply experienced, so am hoping I am right and price paid is not much.

But take my speculating with a pinch of salt because management has mentioned this in one of the calls around May '25.

I am still hopeful because there’s tremendous scope in data centers and to me it sounds dumb that they wouldn’t capitalise when they have the expertise in this field - but its possible Tarun has a non-compete clause for 3 years (since selling Rahi) and so all these things have to be kept under wraps. Also, CFO of Rahi with deep expertise in data centers is still employed with Ceinsys and leading the acquisitions - so I keep my hopes up.

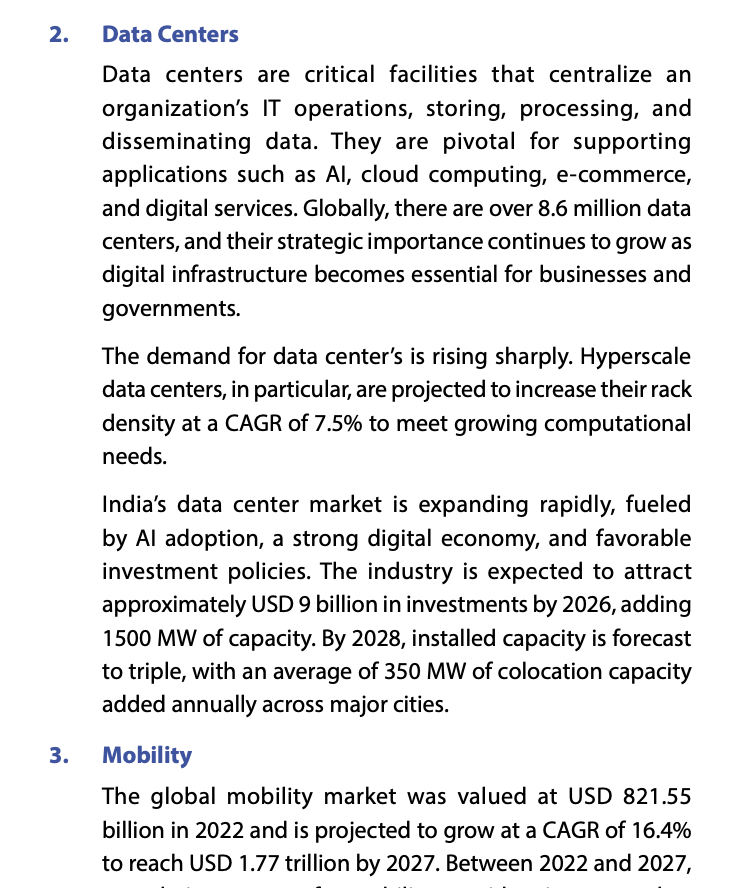

Another reason, in recent AR, between #1 - Geospatial and #3 - Mobility is #2 - Data centers. This is very recent AR and this cannot be an error.

The reason Surej hasn’t yet disclosed the company name on linkedin is probably because Kamat is still CEO. He did join the last call though, so I think there’s no speculation about him taking over as CEO.

Disc: Invested since Oct '23. No recent transactions

48 Likes

Ceinsys tech Call highlights:

More strategic focus on technology-driven, large-value projects (100–150 crore minimum ticket size) versus earlier smaller projects.

Guidance of 800–900 crore of incremental order inflows in h2, active bids in progress, 400 crore from jal jeevan mission expected in this. Execution pipeline remains active in states such as Uttar Pradesh, Maharashtra, Gujarat, Delhi, Rajasthan, Madhya Pradesh for govt tenders.

New growth areas: telecom (BharatNet via subcontracts), land record digitization, and energy RDSS projects.

US subsidiary currently loss-making (investment phase due to BD spend + earlier acquisition VTS in telecom).

- Management expects breakeven from Q3–Q4 FY25.

Technology Deployment (AI & IoT)

• AI used to reduce processing time for LiDAR and asset data (road, utilities), lowering manpower and cost.

• Patent filed for AI-based road asset management tool.

• 75 engineers in AI team, 75 in software development.

27 Likes

Company withdraws AGM agenda item - Surej’s appointment as CEO designate and Whole Time Director. Is this bad news for the investors?

1 Like

My understanding is appointment of him as whole time director has got stuck in some procedural/technical clarification.

So it might get delayed a bit.

Most likely the issue might be due to his renumeration being high and also payment to be made in USD, and his appointment as CEO and WTD residing in USA might have triggered some additional regulatory approvals without which they might not be allowed to go with the resolutions.

Most likely they will do an EGM later for this if regulators clear his appointment.

If anyone has a better explanation please do share your view, I am not an expert on these matters.

3 Likes

It’s the biggest customer is MH Govt which is struggling with all the promises to be delivered during polls..which is around 90000crs+…if not wrong. Meaning..very bad finanical situation.

It will be very interesting to see receivables situation in H1. Also understand about future orders, that they promised to come.

7 Likes

Ceinsys Tech 2025 AGM highlights:

Order Book and Pipeline

- Orderbook is at 1200 + crores, geospatial and engineering solutions at 830 cr., technology solutions at 375 crores.

- Apart form above orderbook company also has , Mobility at 80 cr and other product services at 80 crores not included in the orderbook.

- Water domain is at 75% of Orderbook and enterprise solutions is at 20%.

- Bid pipeline is at 800 crores with expected conversion ratio of 75%.

- Execution timelines is in the range of 12-24 months.

- The average ticket size for orders has substantially increased from ₹25-30 crores to over ₹100 crores in the last two years.

Subsidiaries Performance :

- Singapore entity has 0 revenues. Not much traction/focus on data centre business right now.

- Allygrow is stable.

- US entities will breakeven this year.

Acquisitions plan :

- Expect positive updates by q3/q4. Acquisitions are focused on global markets of US and Europe and it will be operated from India.

AI initiatives :

-

Company has 75 coders for AI and 75 for software tech development aggressively working on these new initiatives.

-

50% revenues expected from digital platform-based solutions which have higher margins than geospatial based traditional services.

-

Working capital cycle improved from 300 days to 125 days in last few quarters as Company was able to bid and target opportunities where the customer has the funding arrangement already tied up or there is a visibility of tying up in the short term. And also got projects which had multiple billing cycles based on project milestones.

-

No Impact from H1B visa policies.

-

99% of the unbilled revenues is less than 6 months old.

JJM:

JJM audit is completed and finsings are not adverse. Expect unlocking of pending orders soon.

NOTE : This is not a transcript of the AGM, I have made notes based on what i understood from the AGM call.

42 Likes

Any comments about Surej’s appointment ?

He was the first person to join the meeting and was present all though out , but he didn’t speak. There was no discussion on his role from MD/Chairman and no shareholder had asked any Questions on his role.

9 Likes