The results are good and lets start with the mandatory snapshot

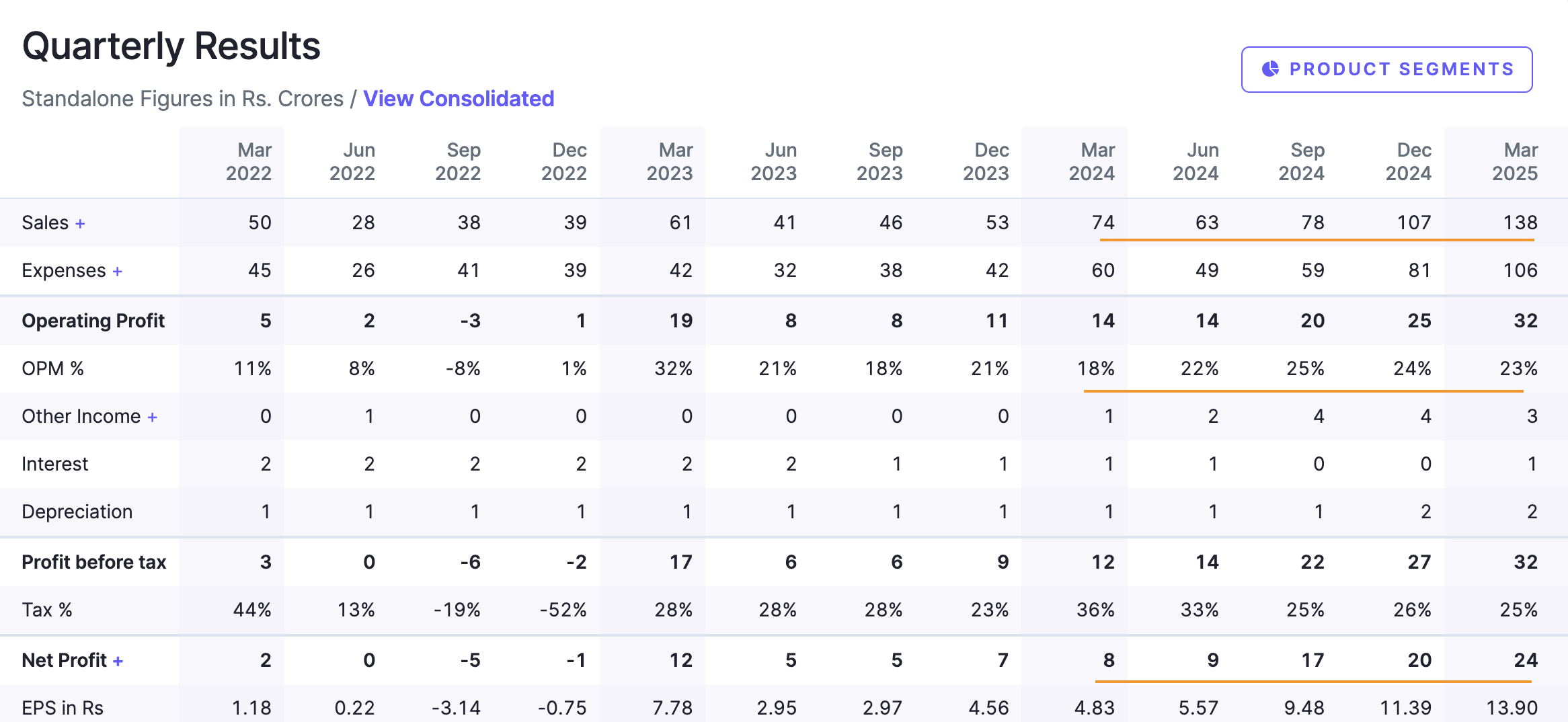

The thing to note is the actual growth is even better when we look at just the standalone

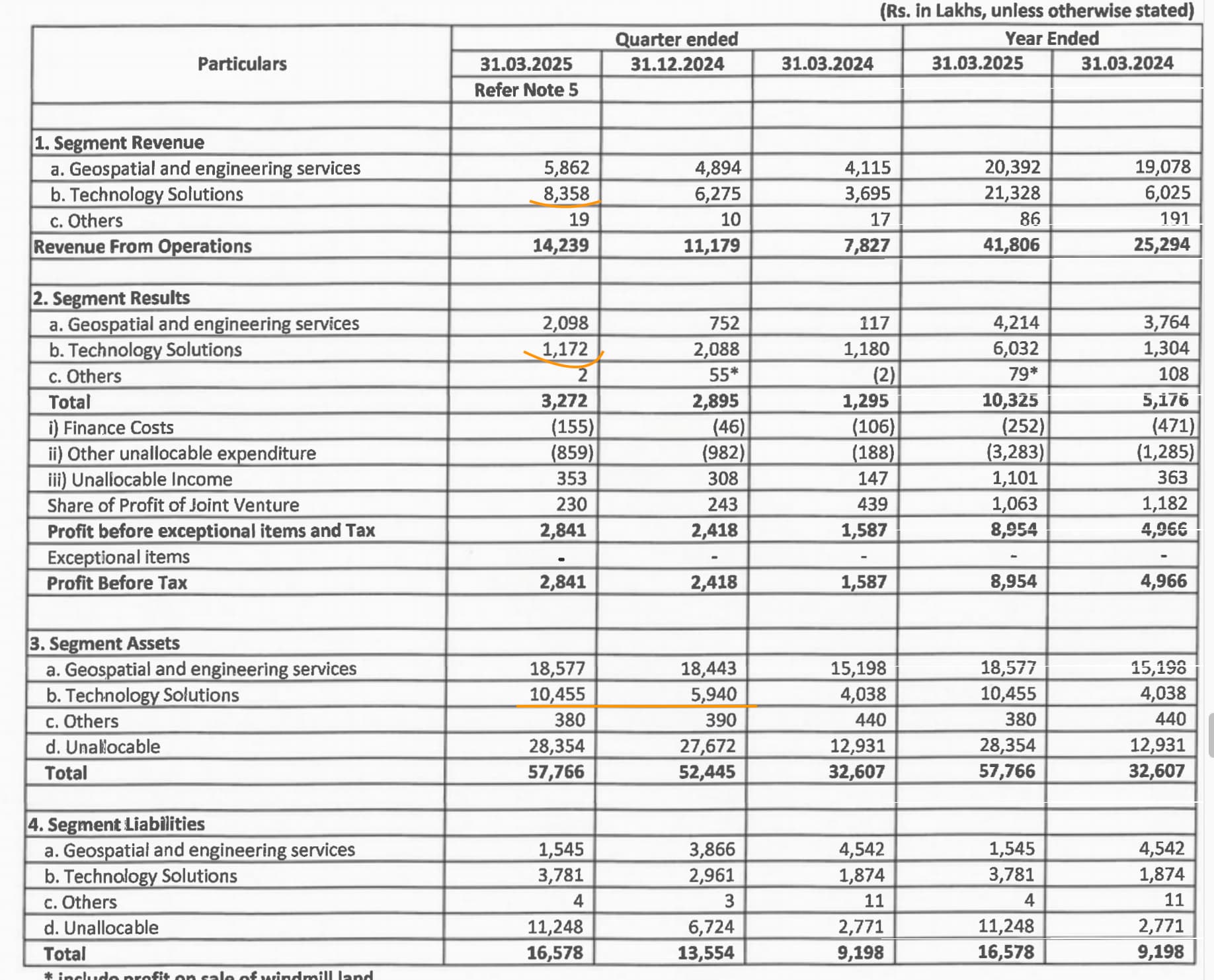

86% topline growth, 129% EBIDT and 300% PAT growth. This is the actual growth from the India business. Growth is actually muted at the consol level and is looking great despite that - we will explore into the reasons why this might be, later in this post.

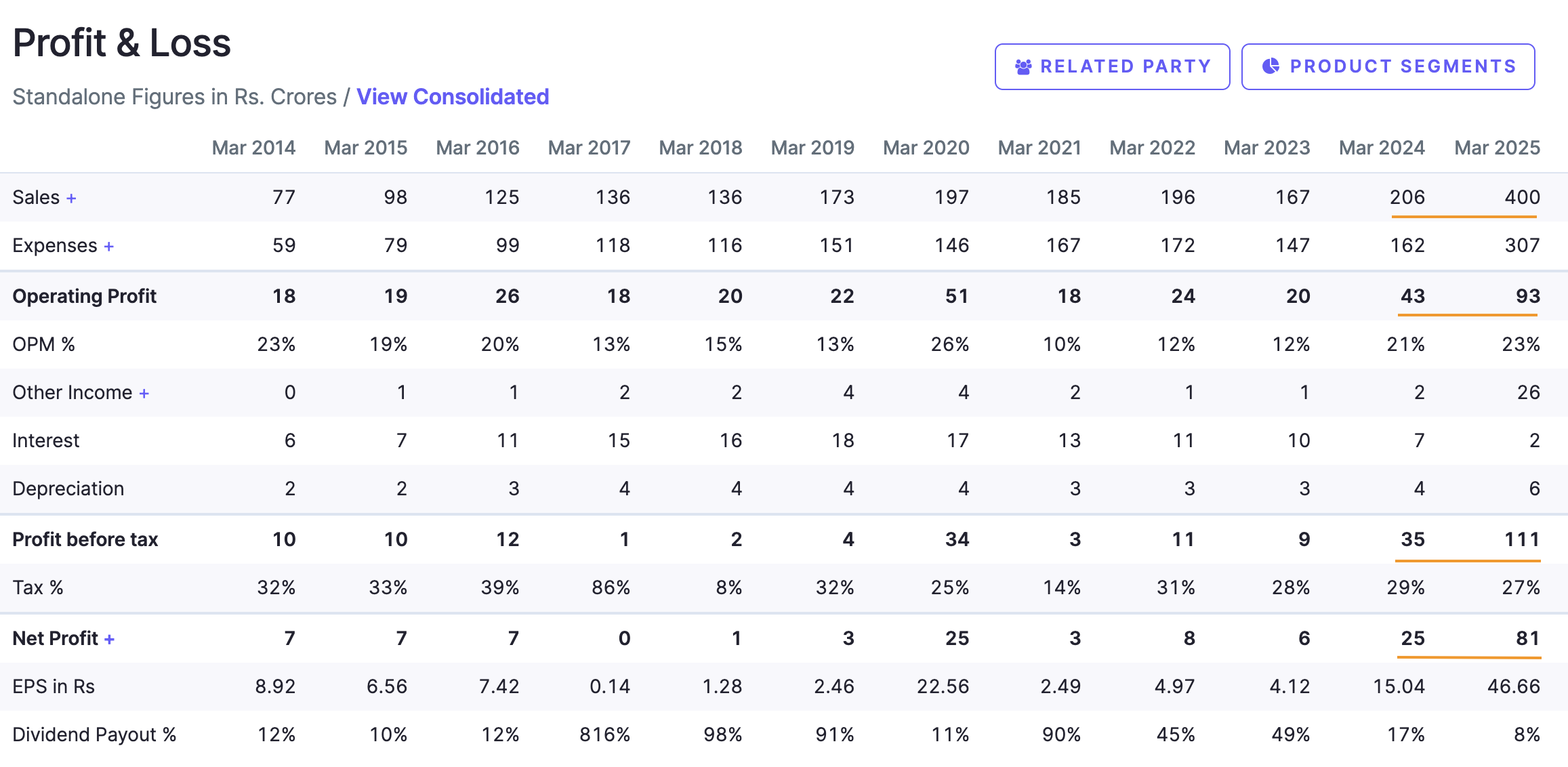

At a yearly level, on standalone the topline has nearly doubled and bottomline has more than tripled (324%) which is phenomenal, considering several large projects in the standalone business are yet to contribute.

It doesn’t look like there was a big contribution from the river linking project which should likely show up in Q1/Q2 (150 Cr initial bit) and rest probably in H2 FY26 making FY26 a pretty loaded year for CS Tech Ai (whatever!). The management had mentioned that it was waiting for approval for river linking project - I doubt if it came in time.

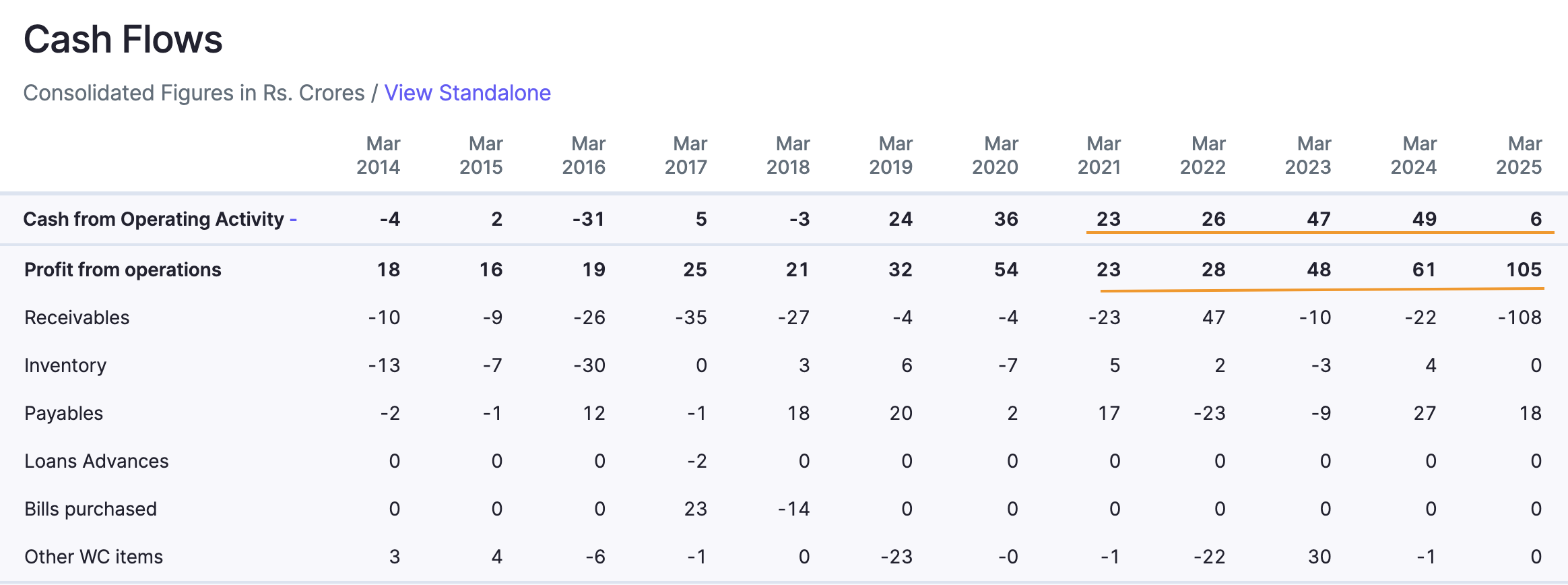

Moving next to the CFO, this time there’s a big drop as compared to previous years. (Note, a drop in CFO is 1 random year is not a concern. CFO/EBITDA conversion should be done over longer periods. A -ve or poor conversion over 10 yrs, is definitely a concern. So we should know when and how to use the tools and not use any one metric as a hammer)

Generally when this happens, there’s a lot of money locked up in working capital. Let’s see if that’s the case

Turns out receivables days has actually improved quite a lot in FY25 and is down to just 104 days. So its not the WC (before we point fingers at govt and JJM issues)

The other thing to note is the management mentioned that CFO for 9m was 124 Cr in the Feb concall. So clearly its the execution in Q4 that has contributed to the drop in CFO. My initial guess is that the river linking project execution has started but revenue cannot yet to recognised and so it should show up as unbilled revenues. Here the managed clarifies in Nov concall

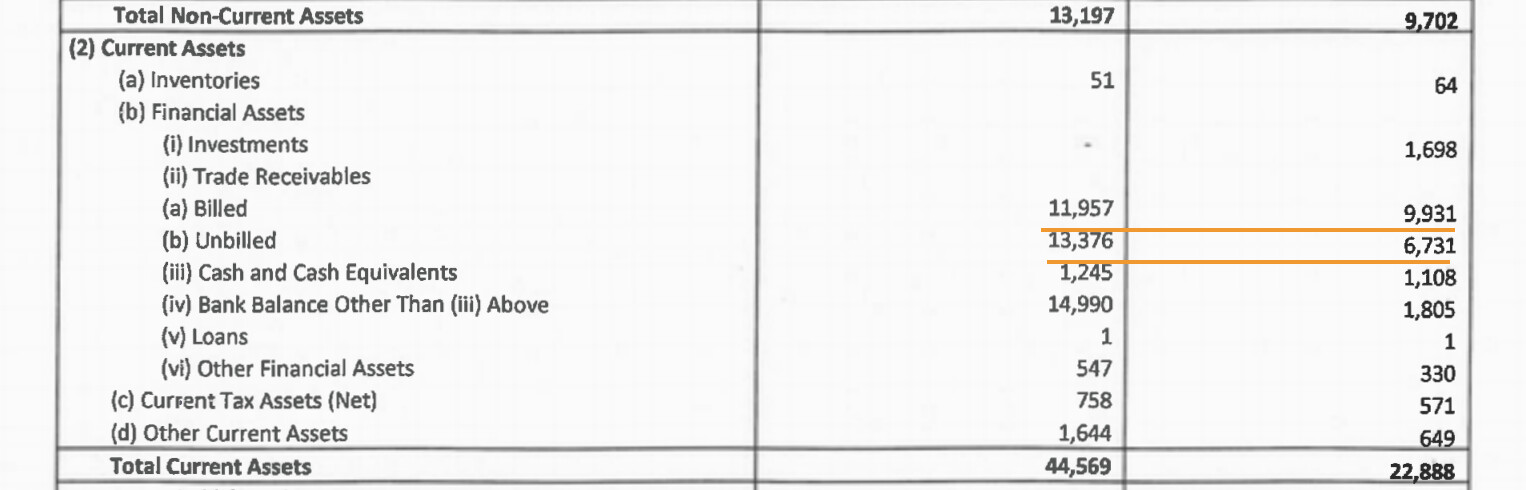

There’s a ~70 Cr jump in unbilled revenues which is the likely cause for the reduction in cash flows (or the major cause based on standalone CFO - what’s happening at the consol level that we discuss later contributes to the rest)

The same can be seen in the Technology solutions (which is where the river-linking project will fall) margins as well. My guess is the employee cost is expensed out in Q4 while the revenue is not yet recognised (which means margins might be good in Q1/Q2 but we shouldn’t extrapolate that and should look on a rolling 12mo basis only for businesses like this - good or bad). The segment assets going up as well confirms that the unbilled revenue jump is mostly from the river-linking project.

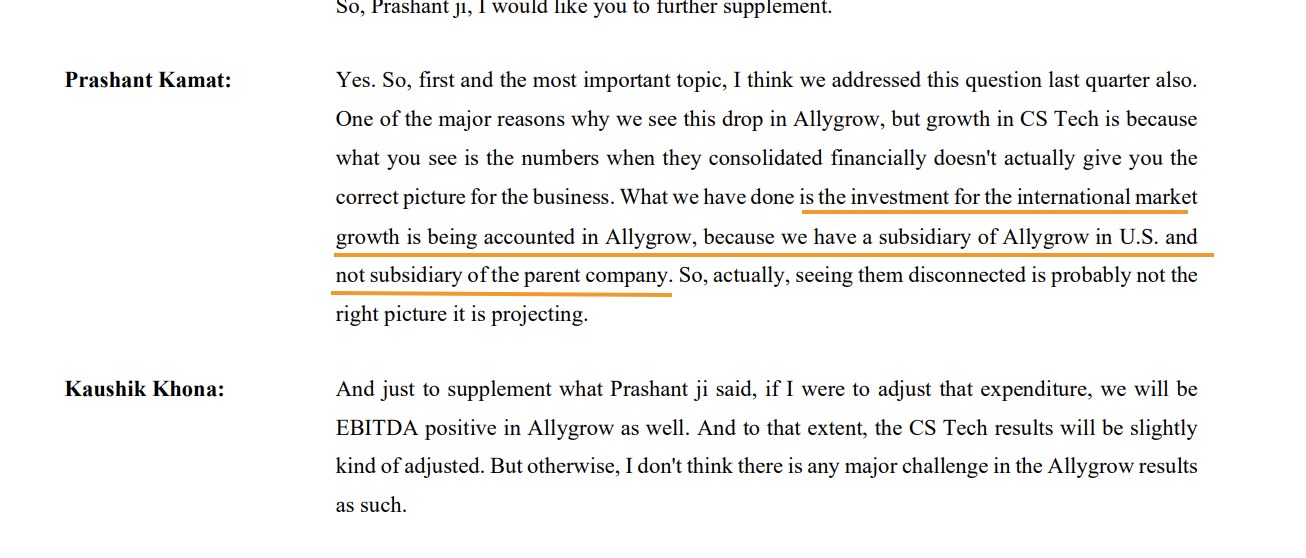

Lets now look at what’s causing the consol level hit almost every quarter now. There’s a 4 Cr contribution at consol level for which the employee cost alone has gone up by 8 Cr for just Q4. For overall year, the diff between consol and standalone topline is 18 Cr for which there’s a 27 Cr employee cost. Does this mean the subsidiary is loss-making? Again, this was discussed in the last call

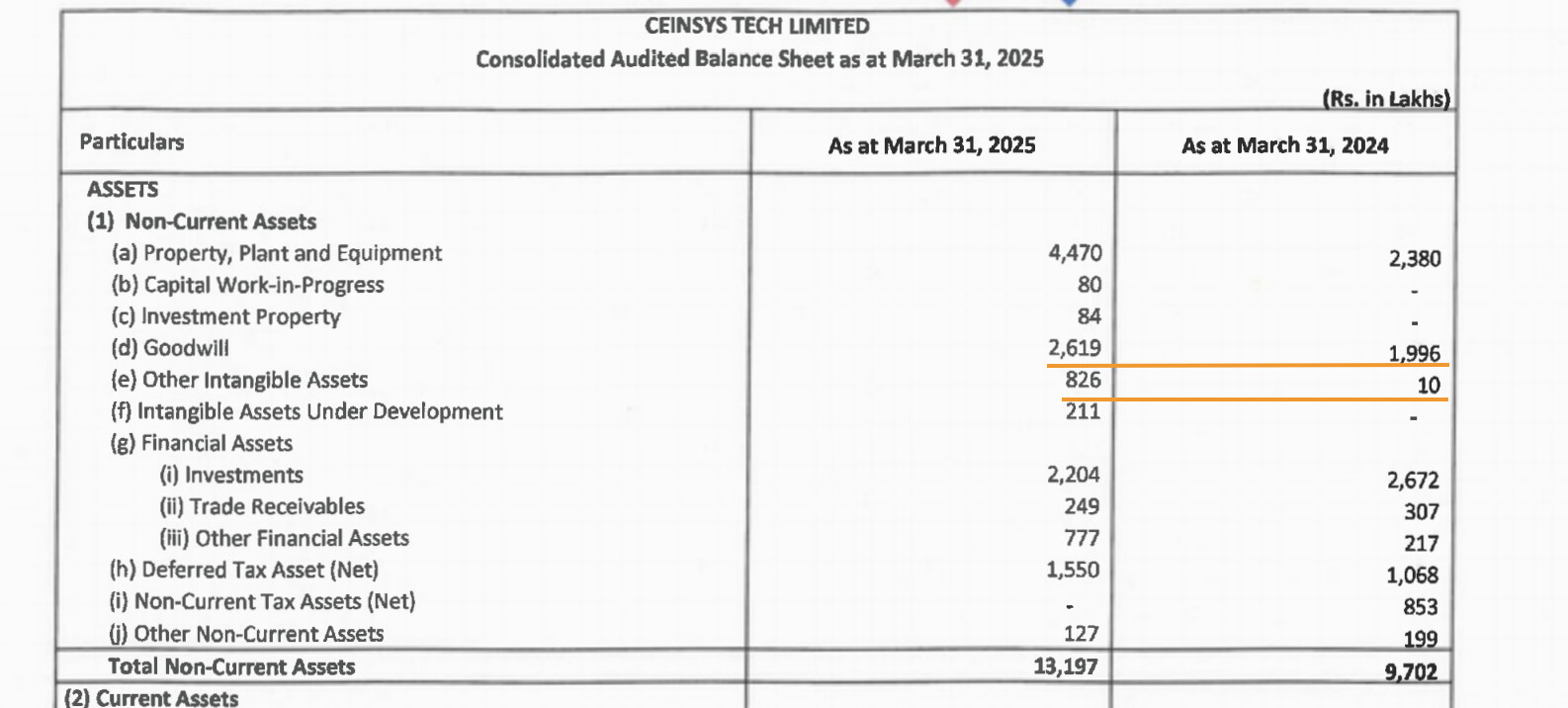

It looks like whatever growth investments are happening in Technology Associates is yet to contribute to growth. However, there are some intangibles in the BS. I am not sure what business development is happening in the US but definitely something is

The company is expensing these things instead of capitalising which is good. What this pertains to, however is unknown but I have some speculations.

That takes us to the next part of the puzzle in the results doc .

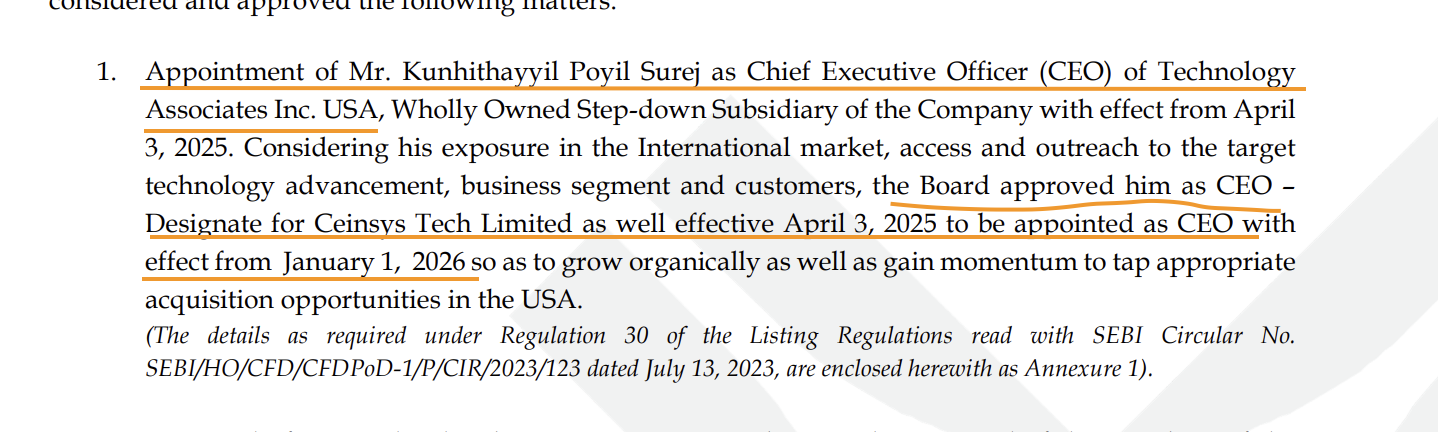

It looks like Rashi Mehta has resigned and has given up the options. Also, it looks like Prashant Kamat has also surrendered a part of the options granted to him last year.

My guess is Prashant Kamat won’t be CEO next year and Surej will likely take over.

So this gives heft to my hunch that whatever is happening in the US subsidiary is going to be big for the company - in pretty much the same way that AllyGrow acquisition was back in 2021.

Very recently AllyGrow got amalgamated (or got NCLT approval for it) with parent Ceinsys. This I think marks a completion of the acquisition. It is likely that Kamat was given options as additional payout for the acquisition since it was acquired for very cheap on the surface. Now I think he has fulfilled his commitments and could be getting a move on (Or might stay on as vice chairman) - this is entirely my speculation.

Since the company is on a growth path with the newly planned acquisitions, the board likely thinks (could be Tarun Raisoni’s decision as well, as a big contributor to funds) Surej might be better suited for the next leg of planned growth.

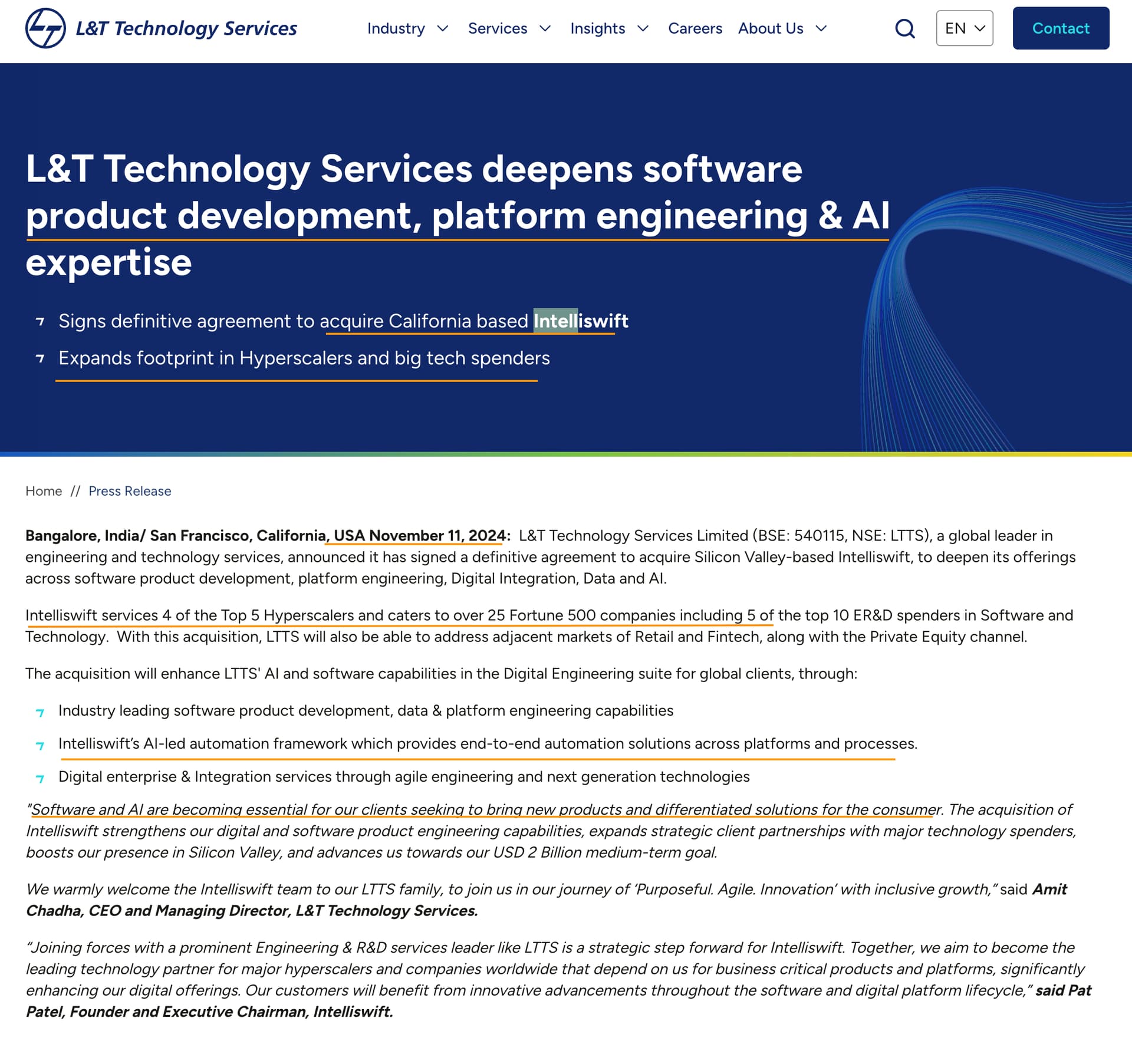

While Kamat came in from AllyGrow which was doing ~$10m revenue, Surej is coming from Intelliswift (was its CEO) that has ~$100m in revenue and was acquired by LTTS recently. So there’s definitely chops to lead the next leg of growth.

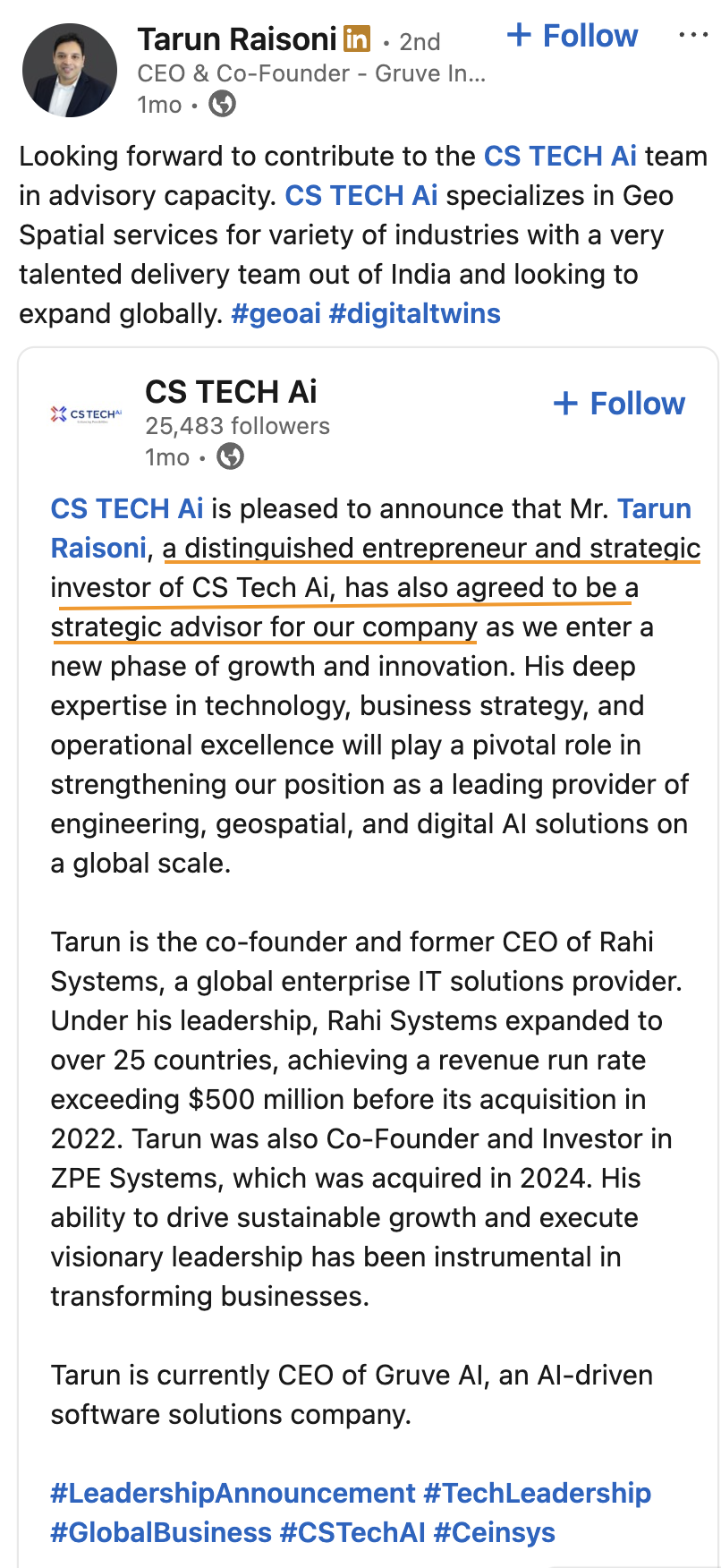

This is what LTTS thinks of Surej’s company

Surej has firm roots in product development, data centers, hyperscalers AI and automation from his previous company and my guess is, he is a reco from Tarun (being a silicon valley guy himself). My hopes are up with whatever they are planning to do. My guess is that it can’t be far away. Maybe there’s a deeper reason for the “AI” bit in company name - at least hiring someone like Surej gives me hope.

The other thing on Rashi’s resignation - I think this was done since Tarun himself as come onboard as advisor (I recently found that Tarun has sold not 1 but 2 companies for big payouts - $270m for Rahi from Wesco and $295m for ZPE from Legrand)

And getting Phaneesh Murthy (global sales head of Infy between '95-'02) as additional director onto the board should also strengthen the tech direction of the company. Turns out Phaneesh Murthy was also on the board of Intelliswift when Surej came onboard as CEO before the LTTS acquisition. All these changes to me point to a company that is thinking way bigger than it is. Lets see how it plays out.

Valuation:

I think valuing the business based on current consol would be incorrect due to the expensing of new business venture which is infact an investment. The way I think about these sort of businesses where there’s a part that’s dragging the overall is based on Kahneman’s dinner set analogy - which is essentially looking at standalone basis and valuing that - At 81 Cr PAT, the standalone business is trading at 34x TTM, 20x 1 yr fwd and ~15x 2yrs fwd - without the optionality of whatever is happening with the new businesses acquired/built.

Disc: Invested from 260 levels. I might be very biased here. Please do your own research