I recently sold CCL Products and here is my rationale for selling:

I would like to start with framework used in Bharat Shah’s book, ‘Of Long-Term Value & Wealth Creation From Equity Investing’ for opportunity size using size of fish and pond as example to fit in CCL Products (India) Ltd.

There are four categories for opportunity size:

Large Fish in a Large Pond: This is the most desirable situation as there are plenty of resources for the fish to growth and being a big fish it also has the potential to get maximum resources for itself.

Large Fish in a Small Pond: Here the future growth of the company has a upper limit as it has already become a giant in a small pond.

Small Fish in a Large Pond: This is also a desirable option, if there is no fight for resources between the players.

Small Fish in a Small Pond: This is the worst combination. There are not enough resources available and you being a small fish has a high chance of getting eaten by others.

I feel CCL Products (India) ltd falls into the second category of Large Fish in a Small Pond.

Such companies are perfect for wealth preservation but not for wealth generation. Perhaps this could be the reason why Prof. Sanjay Bakshi might have invested in it. He might handling people’s money who want wealth preservation for 30-40 years.

“Investor of today will not benefit from the profits of the past but only from the profits of the future.” - Warren Buffett

I feel that I was late to the party and was looking at the rear view mirror instead of watching from windshield.

In 2012 & 13 the company had grown by 38% & 29% respectively. Followed by 22% in 2015. But then, that growth never return as their size got much bigger.

Will the previous growth of CCL return back?

“A high growth company rarely goes back to the high growth stage after it starts to slow down on the growth curve.” - Basant Maheshwari

Why exactly I sold CCL Products (India) Ltd ?

The main reason was opportunity size available for this company.

CCL is already a market leader with 10% market share in globally. Coffee industry being very fragment it is very difficult for them to get bigger than this.

In such an industry one does not expect a market share of 50%.

Now if the industry would have been growing at a good rate then CCL would be the first one to get the benefit as being the market leader. But the coffee industry is growing at 2-3% only.

Reason being that there is already over capacity in the industry.

In my initially thesis I had overlooked this point as I had estimated that CCL would still achieve growth from the below points mentioned:

Entry in USA: Demand for instant coffee is 75,000-80,000 ton USA alone and currently CCL is supplying 2000 ton only.

Entry in Switzerland: Large retail businesses in Switzerland don’t depend on one supplier, instead they keep minimum five suppliers with them. Therefore, this provides opportunity for CCL as to be one of the five suppliers.

Growth in India: The consumption of coffee is only 20,000 tons compared to Japan at 35,000 and USA at 80,000 tons. A positive change in consumer lifestyle (specifically driven by western culture) with increasing higher disposable income could increase the coffee consuming in our country.

B2C business: Here I was expecting that, if luck plays out, it could turn out to be a FMCG player like Nestle.

Counter arguments

Taking Market Share Globally?

USA is surely a great coffee consumption market and is huge but majority of that market is fresh and ground coffee.

Only 40% of the US market is addressable where they would face competition from Nestle, Folgers, Kraft Heinz Foods, etc.

They have been trying to enter Switzerland for a very long time and have been facing problems. But they have recently hired new CEO for their subsidiary and started taking few orders.

Now, the first two points can still play out and the company can do well but we must remember the stickiness in the product which I stated as an advantage in my analysis is a double edge sword.

If the product is sticky and there is high switching cost for CCL’s products then it would also be for Nestle and other players. Therefore, taking market share from other player would be much more difficult than any other industry.

Now, I understand that the company does have an economic moat of being the lowest cost producer and has the capability to take away market share but that would take a long time.

Once company had lost a customer who had set up their own plant. Soon after that customer had to return back as CCL’s price was lower than that customer’s cost.

But that customer returned back only for the premium blend and not for the bulk product. Perhaps, fragmentation in this industry is sustainable?

Another vantage point would be coffee prices.

Generally when prices of a commodity hit the lowest level revenues of companies in that field must increase, which is not visible with CCL.

India Story: Next Nestle?

Somewhere deep down I knew that CCL’s B2B business was not growing and even the management was aware of this, which led them to entering into B2C in India.

So, my back up plan was that there B2C business could play out a game changer and become market leader until then they would gain growth throw margin expansion or value added products from B2B.

But I missed a very basic thing here too: Size of Opportunity

Branded business market in India is only of 2000cr. As there are well established players here (Nestle & HUL), if CCL takes 20% market share (with advertising expenditure) it would not contribute much to the revenues. (But it would certainly improve the profit as B2C is a higher margin business)

Building a brand takes years of branding which the competitors have already done.

Second assumption I made here was growth of coffee consumption.

I believed that as there is adoption of western culture, hectic work life, higher disposable income, etc. the demand for coffee would increase.

But I never paid attention to numbers. They tell a different story.

2-3% growth shows that India is tea consuming country and coffee at only 20,000 ton is going to stay there for a long time.

People won’t just suddenly shift to drinking coffee and leave tea which is cheaper and has been go to drink for everyone for ages in India.

Conclusion:

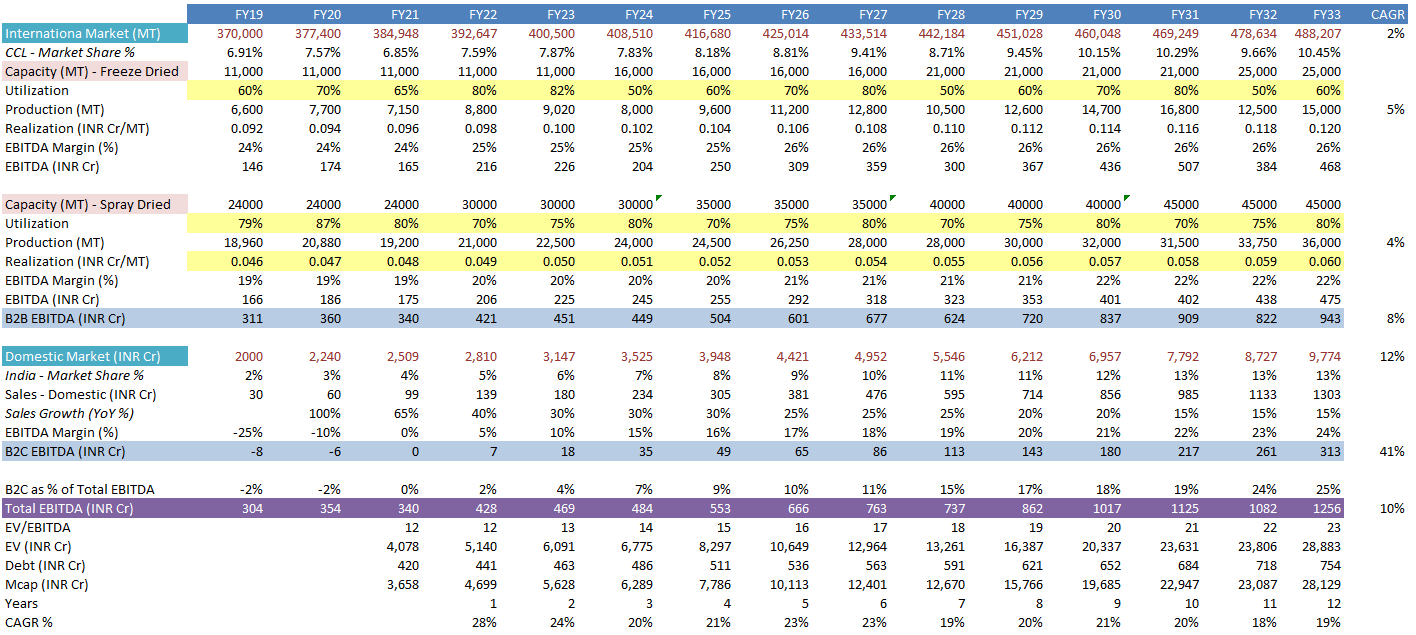

Here is how I think this company’s market cap would turn out to be after 10 years:

CAGR for 10yr Expected Market Cap (Approx)

5% 5,000-6,000cr

8% 7,000-8000cr

10% 8,000-9,000cr

12% 10,00-11,000cr

15% 13,000-14,000

(Exit P/E Multiple of 20)

I would like to end with a quote:

“When growth goes away, equities reduce to a bond. It will be treated like a bond for a while. If the picture deteriorates further, then it will be treated worse than a bond.”- Bharat Shah

(Same goes for coffee lovers!)

(Same goes for coffee lovers!)