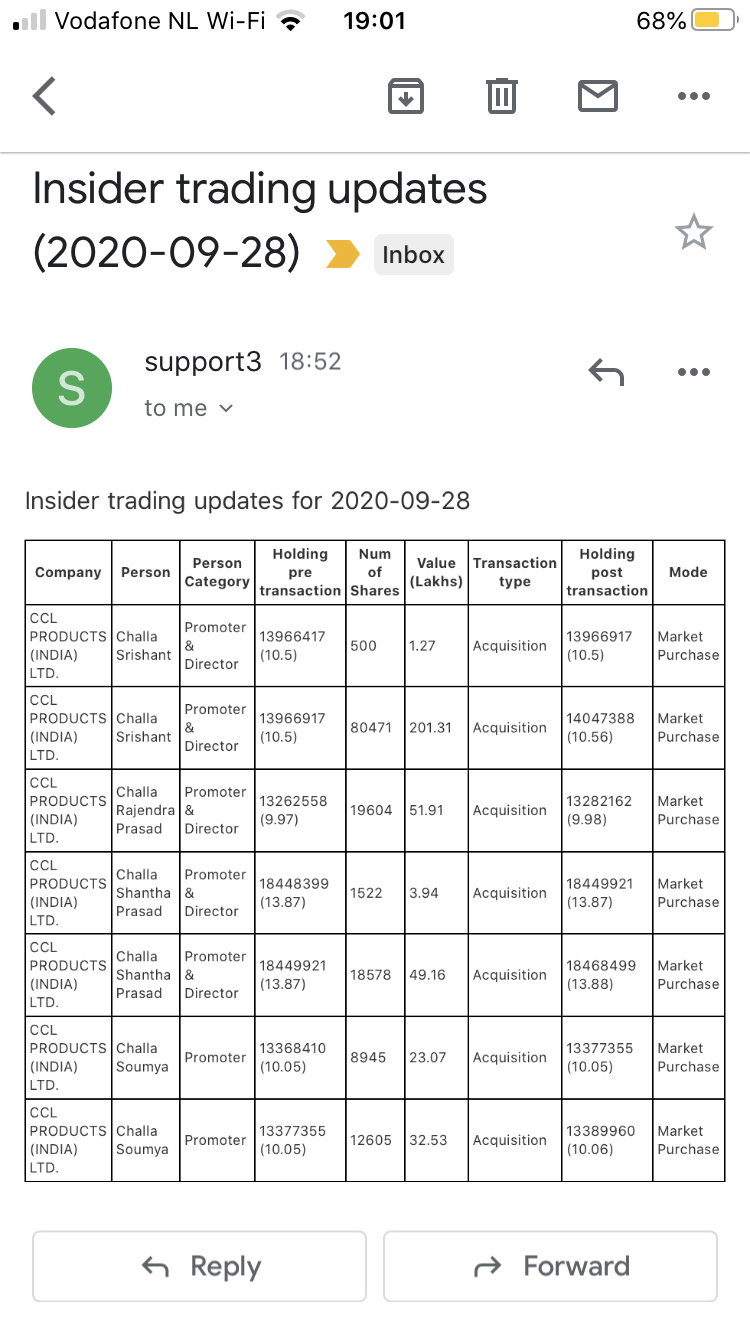

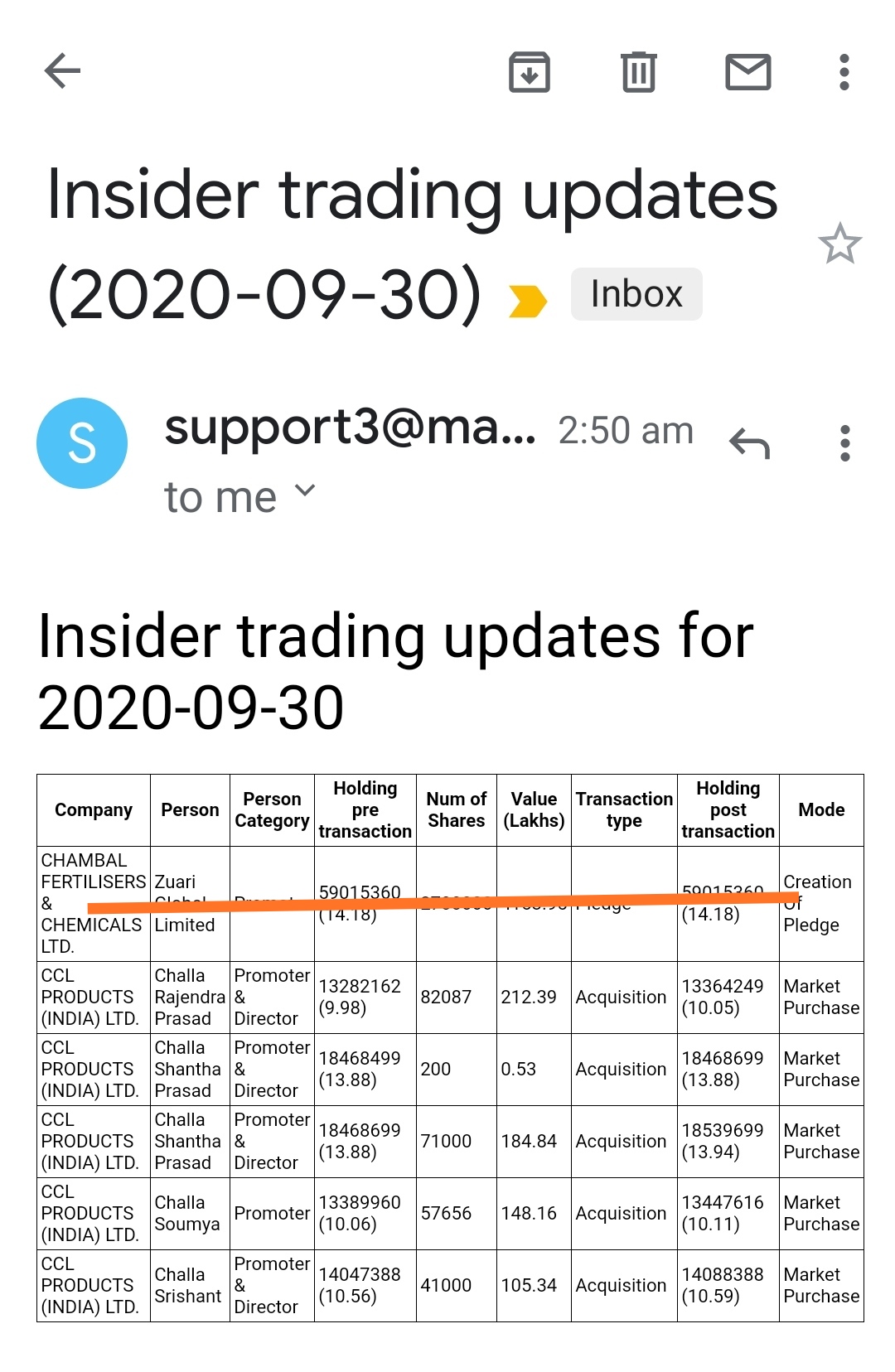

Promoters continue to buy aggressively from market.

4 Likes

How to get this kind of updates on email? Please suggest.

Icicidirect sends notification to customers. You can ask your broker

3 Likes

https://www.screener.in.

Follow company under watch list and you will get daily email of the companies which you are following. Amazing service.

2 Likes

This was from bsealerts.in

2 Likes

CD equisearch report on ccl products

4 Likes

Ltd Webinar")

Disc: Invested

3 Likes

Funds reducing their stake in CCL:

Prof. Sanjay Bakshi has been reducing his stake consistently. Jun 2020: 1.83 to 1.76% Sept 2020: 1.76 to 1.15%

MALABAR INDIA FUND LIMITED has also been reducing their stake. Jun 2020: 2.29 to 1.60% Sept 2020: 1.60 to 1.48%

4 Likes

10 Likes

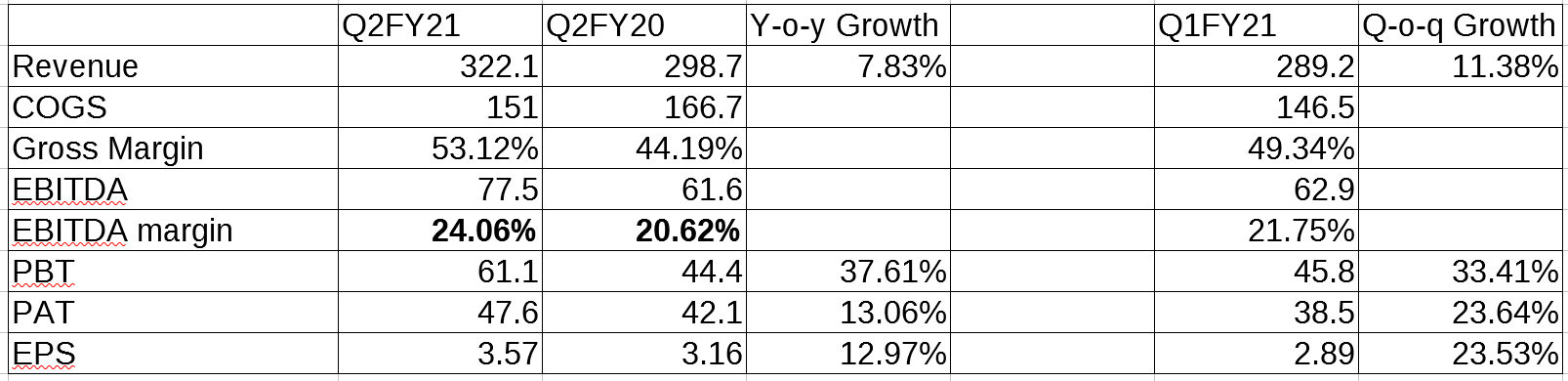

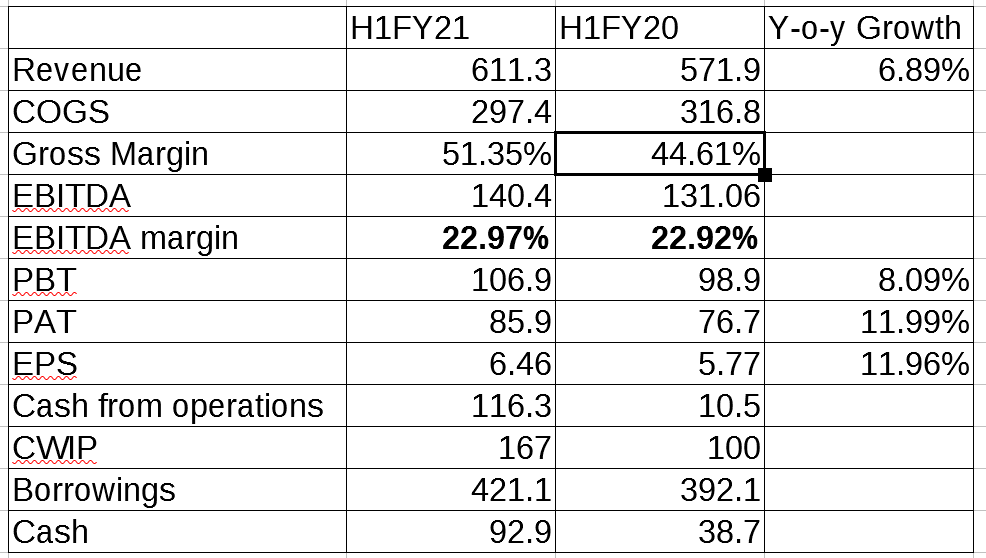

Q2FY21 concall and CNBC interview

-

7% volume growth in Q2, because of Vietnam. Target was 10% vol growth in FY21, trying best to achieve that. To achieve 10%, need to do 13% in H2. FY22-23 if things get normalised, we can grow volumes by 15-20%. Current year Order book is full. Targeted 10% growth for the year. There may be some deferment from some customers

-

Vietnam did well while domestic was down 8%. Did 100% CU in Q2 also. Is it sustainable? Where is demand coming from? Major order from US so expecting full utilization this year. So doing line balancing and expanding capacity to 13500 tons. For full year, we will do at least 9000 tons (which is more than optimum utilization), if not 10,000 tons. H2FY20 was at 60% utilization, H2FY21 can be 80-90% utilization.

-

India Composite CU at 65% right now, and will reach reach 75% for full year

-

Spray dried used 75%. Will reach 80% CU for the year. Optimum is 80-85%. Seeing better traction even on the domestic front

-

Duggirala Freeze dried Plant was shut for 2 months maintenance because customers asked for postponement. Restarted plant in September. impact of 50cr but we were carrying inventory which was liquidated in Q1. Capacity was lost but sales was 60-70% of normal. H2 we should be doing 70% or so.

-

Small packs packaging - delays in commisioning and it will be operational in Q1FY22.

-

-

Currently we have minimum inventory.

-

Freeze dried margin is 2-2.5x of spray dried. Current capacity FD= 11000tons, SD=20,000 tons. Adding 3500 tons in Vietnam (commissioning in Q4), and small pack capacity in India.

-

Postponed orders from Russia- will be executed in H2. Slight improvement now.

-

Branded business did very well 60cr in H1, growth of 70% yoy. Profitability- will be able to comment in Q3. Expecting close to break even. FY20 full year was 60cr, EBITDA loss 3.5cr. Institutional business was washout in H1 and now its picking up slowly. Getting repeat orders from distributors so product is selling well. Growth from all channels. Last year 55000 outlets, this year 70000, end of this year plan to reach 1 lakh outlets. Basic distribution network will be in place to reach all towns with 10 lakh population.

-

Started supplying first private label small pack business to US retailer- unique product.

-

Europe-renewed existing supermarket contract

-

Value add products, innovations–pre-mix coffee, flavored coffee. Currently less than 5%, hope that it will increase in future. Started because customers requested solutions. Cold bru costed 150$ per kg, and we brought down cost to 30$, customer paying 50$. Volumes for these products will take time to build up. No one else can make some of these products.

-

Single serve sachets with instant coffee - we are already exporting. Pods are a regional business today because shelf life is very imp. There is opportunity to explore pods market in India but there is no market today for pods in India.

-

Short term borrowing increase- for WC. Sot of capital is 1.5%.

-

Contingent liabilities - sharp rise is due to income tax assessment

-

MEIS benefit was 8.5cr in Q2. Govt can cap it to 2cr for Q3 and then increase it on Q4. If govt doesnt impose further curbs, we will get 10-15cr in H2. Next year impact? 40cr per year MEIS over past year. New scheme can cover 30-35% of this benefit. Additionally, some can be passed on to some of the customers. Trying to minimize the damage and 10-12 cr can be total MEIS impact

-

Competitive dynamics vs Brazilian suppliers because of large depreciation of Brazil currency? World over, Coffee is bought and sold in dollar terms. Only impact can be in conversion terms. Brazil quality is very different from what we supply. They supply Robusta, our supply is mainly Arabica

-

Many capacities have come online but there is increase in demand for freeze dried. Not a drastic change in dynamics.

22 Likes

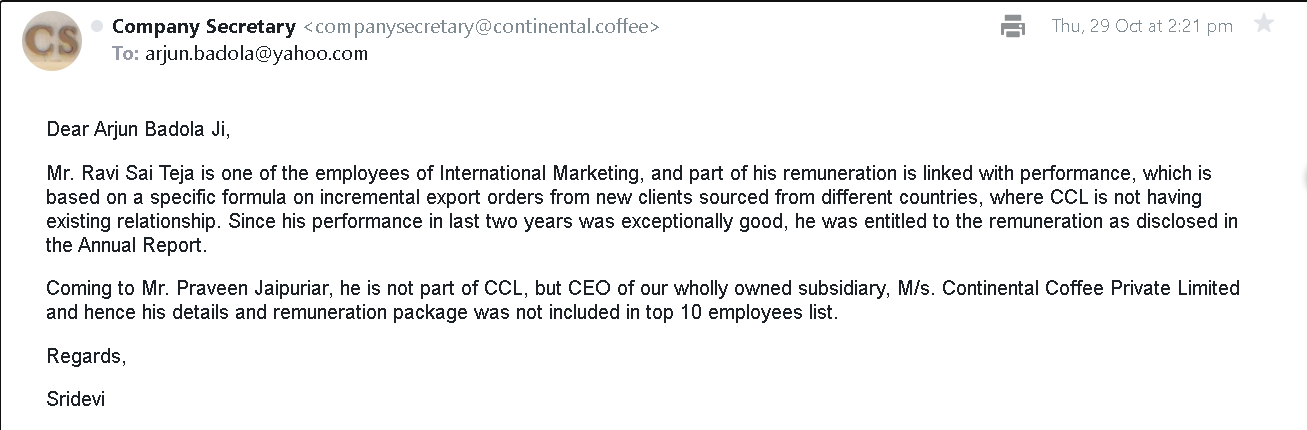

Hello guys someone on my blog just brought this into my notice about one of the CCL products’s employee remuneration seems off.

If you check the remuneration of “Manager - Business Develeopment” this guy has the least experience among any employee present in top 10 category and he has been with the company only for 5 years but he is the third highest paid employee of the company. (For FY19-20)

Has anyone else noticed this?

6 Likes

Hi Arjun,

Thank you for this.

I tried going down the rabbit hole for this but couldn’t find any plausible explanation for this either. The concerned employee is active on LinkedIn and Twitter but absolutely nothing suggests a compensation this high - neither the amount of corporate experience nor the quality of it.

Another thing that seems odd to me is that there is no mention of Mr. Jaipuriar Praveen in that list. Looking at the gross renumeration, it is a given that his name should be there; the last person on the list earns roughly as much as an MBA from a top tier college would (in his initial years).

Hence the list is as perplexing to me as it looks to you. I also see that they have not put this information on the exchanges but on their internal server, hence doubt if any outsider would know more about it. Maybe writing to the management inquiring about this would be the most logical step in this regard to conclude the speculation.

3 Likes

Thanks Shashank, even I think Mr. Praveen’s should have been there unless he is taking ESOP instead of salary as he only joined from 2017. If we look at the 2018-19, Mr. V.Lakshmi Narayana join in 2018 itself and become the second highest paid.

CEO or CFO top management high salary could be understandable but it is odd to see that other guy getting paid so much. Plus if you look at the 2018-2019 list this guy is not present there. I don’t what miracle he did for the company last year which made him the third highest paid.

I will try to write to the company and get back you. I would request you also to do the same, as they still haven’t replied to a email which I wrote few weeks back.

2 Likes

Its ridiculous that a Business Analyst from a IT company(Serco Pvt Limited) is hired as a BDM for a coffee company, who has no sales experience and comes from a tech background(should have an MBA atleast). Not sure how he will sell coffee, build distribution network and grow sales.

Such moves appear to be favors in my opinion, lets see what the management has to says.

3 Likes

In his Linkedin bio, he has mentioned that he has been at the company for the last 5 years. He has been at the present position since the Apr 2019. So, he is not a new hire. It could be a false alarm, but keep sleuthing folks!

We are aware of that but 5 years seems less if compared with others.

This guy is getting paid higher than people who have much more experience and have been with company for much longer time.

2 Likes

Hi,

Thanks for this. @pikrohit has already provided an excellent summary above. My takeaways from this, from overall business prespective:

- India trade capacity utilisation at 75% (optimum 80% to 85%). Y-o-Y basis, should be reaching about 80% on the spray dried capacity. As of now, the composite utilization level between SEZ and main plant, Duggirala plant is about 65% (due to earlier plant shutdown for 2 months).

- Not much growth expected in the FD segment. Better traction this year also in the domestic market for SD segment. The volume growth could be slightly better in the spray-dried segment. Both in India and in Vietnam, this year, the volume growth wherever is there, it is mainly on the spray-dried.

- FD has higher margins as compared to SD (1:2.5) but incorrect to assume that all margin expansion only due to this. Higher gross margins since they started supplying first private label small pack business to the U.S. to one of the large retailers. This is now permanent and will lead to higher operating performance from the Vietnam Unit (>90% utilisation for the year) on a sustainable basis. During FY21, they will also be doing line balancing and expanding the capacity to some 13,500 tonnes from 10k tonnes (commissioning expected by March 2021, benefits by Q1FY22).

- Other international orders : A Russian client had postponed order earlier this year. Those orders are going to get executed during the rest half of the year. Indonesian government has given a big stimulus and some export companies in India have been benefited. The exports to Indonesia over the last year has been encouraging. Unique product created for the US customer (proprietary blend). My take: Recurring revenue from customers who don’t know the formulation.

- As far as instant coffee consumption is concerned , even after COVID there is no real reduction in consumption that is there across the world . Advancement of orders in Europe as they anticipated a sharp off-take; slowly that gets tapered down for the rest of the year. Every year there is a slight increase in demand for freeze-dried, which is there like even this year as well.

- Already operating at peak capacity for small packs. Exploring third-party packing for some products, because exceeding existing capacity right now.

- Non-linear returns on R&D:

- Several new products, starting from flavored coffees, micro-blend coffees to cold brews, instant cold brews (highend products). New cos and even existing customers who want to increase their portfolio of products, they have started buying these new niche products from CCL. Volumes will start slow, but they should pick up going forward.

- Once they create the product, can offer that product to other customers in different territories as well. Been doing over the years. Innovations started because of our customers. E.g. cold brew is a product where a customer is costing them about $150 per kilo, which CCL brought down the cost to something like $30 a kilo for them. So this is a convenient product which is there for CCL. And the customer also, there is a cost saving, which is why they come to CCL with $50. This is not a volume play right now (less than 5%), but will grow to it in the long term.

- Very limited impact of macro factors: There was a question on impact of Brazilian Real/INR/USD and if INR appreciation will be an advantage for Brazil. Mr. Srishant mentioned that throughout the world, the coffee is bought and sold in dollar terms only. So, impact only to the extent of conversion rate. Also, the product mix is different (Brazil grows 90% Arabica coffee vs CCL 95% is Robusta coffee). Additionally, their strategy has always been cost plus basis, so overall stability for the company.

- Lot of chatter on MEIS benefits reducing/going away. The company has maintained that they will recover 34-40% of that from other government schemes. For the rest, they had subsidised their prices earlier to the tune of MEIS benefits they were getting. Now, they will recover the same from the customers in terms of commensurate pricing (because they can)! From a long-term investor perspective, MEIS will go away one day. No point fretting over it so much.

- Short term borrowings in the balance sheet are working capital limits, both at Swiss facility and the Vietnam facility also. Cost of funds is 1.5%. Any contingent liabilities are relating to the income tax assessments. Other than that, there are no other contingencies.

- Branded business A&P at 11 crores per year. This year 5cr has already been spent. 1HY FY21 sales at 60-70 cr (retail + institutional, 70% yoy growth). Branded retail has doubled this year, 100% growth since institutional was muted in 1HY FY21. Institutional business has now started to pick up now but not a pre-Covid levels. 100-120 cr sales expected total this year. That will be very close to the break-even for India branded business . My view: High A&P justified since in the brand building stage.

- Distribution circle in India was at 55k outlets in FY20, 75k currently and expecting to reach 1 lakh outlets by end of FY21. Intends to reach all 10 lakh plus population towns in the rest of India by the end of this year. 4% market share in the top 10% outlets as a percentage of the sales of coffee for CCL brand . Will be trying to reach the 10% market share which will be the inflection point for the brand.

- T he company will not take all the burden of being the market maker in the domestic market , as mentioned by Mr. Jaipuriar. When asked about explosion of domestic direct-to-retail kind of coffee brands in India at a premium range, he mentions that its favourable that they are developing the category because after all, all of them help to increase the category size. This is a big plus since it helps them maintain margins without heavy spends on A&P for a new category.

.

8 Likes