Hi Arjun,

Many thanks for the great post and clearly articulating your reasons for selling out on this company which according to you seems to be well past its prime growth days and would be a wealth-preserver at best.

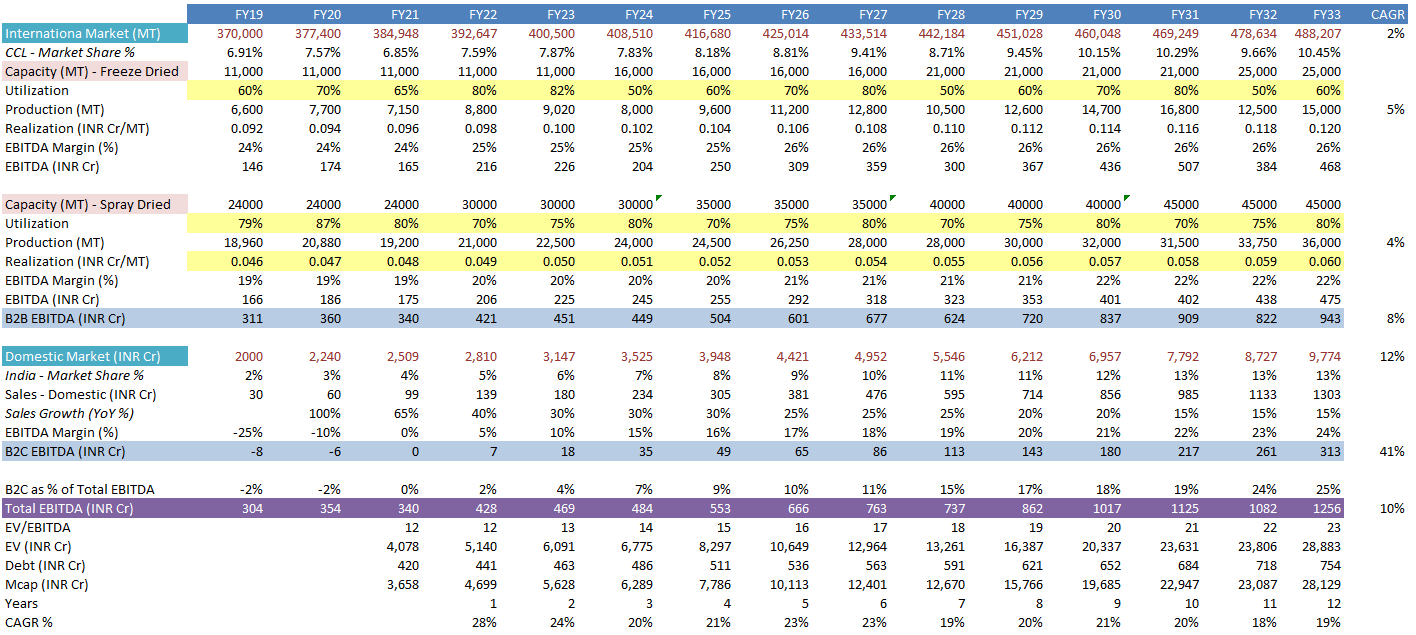

Let’s do a thought experiment on this ![]()

The following is just an illustration of the art of the possible and is by no means be referred as a valuation exercise.

The 2 aspects I would beg to differ with you are as follows:

- CCL already enjoys a ~10% market share in the global Instant Coffee private label market growing at 7% CAGR and can’t endlessly grow while the market is growing at 2-3% CAGR

My take: CCL as we have seen is constantly innovating into margin accretive products and newer blends, so it is not that difficult is assume a volume CAGR of 5% for CCL in the global IC market, especially when it has strong 20+ years of tie-ups with some strong market-leading companies and supermarkets in EU and the US.

- Branded business market in India is only of 2000cr. As there are well-established players here (Nestle & HUL), if CCL takes 20% market share (with advertising expenditure) it would not contribute much to the revenues.

My take: The domestic market is 2000 Cr( IC) + 500 Cr(Filter Coffee in the south) - but more than that what’s important is this pie is growing at 12-15% CAGR with the rise of disposable income, healthy drinking and coffee culture induced by the Starbucks and CCDs of the world. So CCL can continue to grow for a long time even for the much-coveted 10-15% market share (with Nestle & Bru holding on to their coveted leadership)

So back to the thought experiment, how will the future look like.

Another key thing to consider here is the long term potential market cap change from the growth in the branded business. As the B2C part contribution increases, there would be drastic margin improvements (lower A&P spend as % of sales, WC improvements, other economies of scale benefits,…) and hence would be the market perception in attributing the valuation multiples. I am envisaging 10 years hence, markets will attach a much stronger EV/EBITDA multiple to this business with a strong retail pie (~25% of consolidated EBITDA)

Illustrations (12 years into the future!!!)

So as you see in this illustration, there is a strong potential for wealth-creation with wealth being compounded at ~20% (including the dividend yield). It is a long waiting game and that’s why the promoters are so eagerly nibbling the stock at every opportunity.

Happy to hear your thoughts on the same.

Happy Investing!

Rudra Chowdhury