I was looking at the financial numbers of Triveni Engineering and Industries. The cumulative cash flow from operations of the company for period 2006-2017 is almost double of net profit for the same period. Data source is Screener.in. I have also re-checked number for some year from annual reports and number seems to be correct. In 2013 company changed its financial year ending from September to March therefore Mar-14 may be results for 18 months.

I am reproducing the calculation for ease of community below

My understanding is over long period of time say 10 years cumulative CFO and NP should match closely.

Therefore my question is why cCFO for this company is almost double of cNP and what does it indicate/point to?

Sir, this number is good but there is other income and the company is showing negative tax figures from 2012 to 2016. Major cash is received in 2007 and 2009. So there is no regularity in cash from operation

Over long periods cfo should match cash profits not net profits. Cash profits are net profits plus ( or minus as the case may be) any non cash items in p&l like depreciation, amortization, loan loss provisions etc.

Typically if you add net profits and depreciation it should match cfo for a company that is growing at average rate. For fast growing companies and companies that are working capital intensive, cfo will lag as working capital investment will reduce cfo.

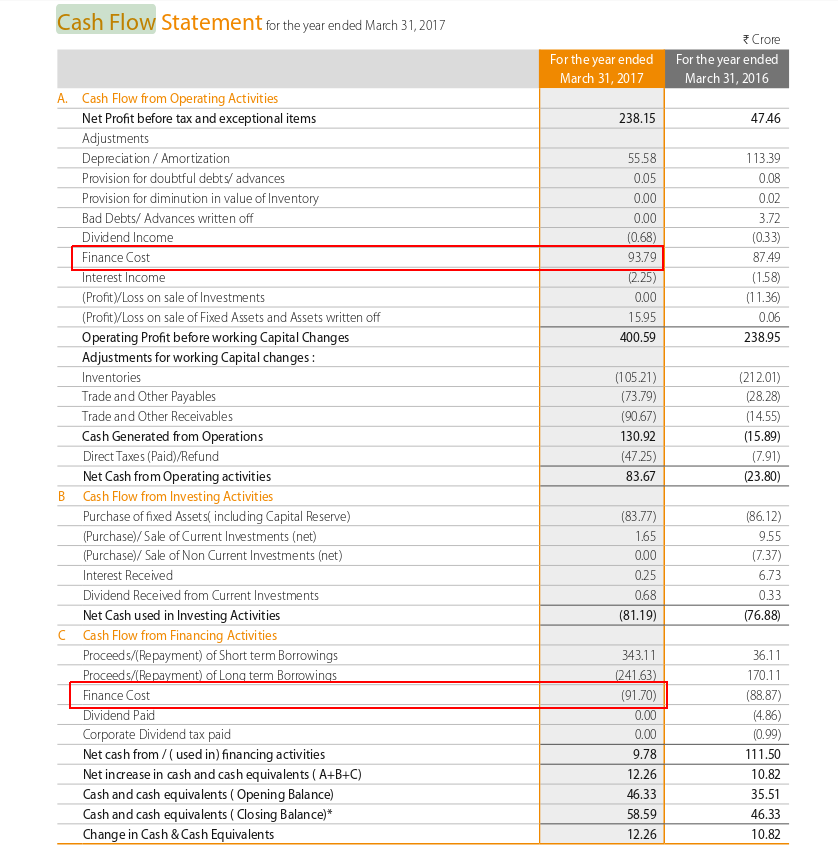

I will be thankful, if any member could look at the attached Cash Flow Statement of Dalmia Sugar. Profit and Loss and Balance is available on screener.in and help me understand why Finance cost is added back to PBT in Cash from Operating activity?

Also why does a similar amount and NOT same is deducted in Cash flow from Financing activity?

While preparing cash flow, since the bottomline PAT is taken as a base (which is already after deducting interest), the interest is added back to be given a separate impact under the financing activities section in compliance with accounting requirements. Also, the finance cost that is deducted is the ‘actual cash outflow’ while the one which appears in income statement is more of an accounting interest (after considering ‘matching concept’) - basically it also includes accruals and alike.

Finance costs actually belong to CFF as the nature of the amount is financing. It is like the company is initially (or even later) financed by debt & equity. Debt incurs interest (or finance cost).

If you look at the income statement, they would have first deducted the same amount in the interest or finance costs. But the nature of expense is not operating expense, it is financing in nature. Hence when you look at the CFO, it is added back here. But it still needs to be accounted, which is done in the CFF section

Generally CFO= PBT+adjustments due to P&L+ adjustments from BS (mostly working capital adjustment)

adjustments from P&L include adding back depreciation, interest costs, subtracting interest received, dividend received (again these are not incomes due to operations) , any expense adjusted for write off (this number is counted as expense in P&L, which is reversed here) etc, any expense incurred towards disposal of an asset (shown as expense in P&L, again added back in CFO). If you look at 4-5 companies CFO, you will understand the general pattern.

The place where I usually get tripped is adjustments from the Balance sheet (usually trade payables).