Carysil Q2 concall highlights -

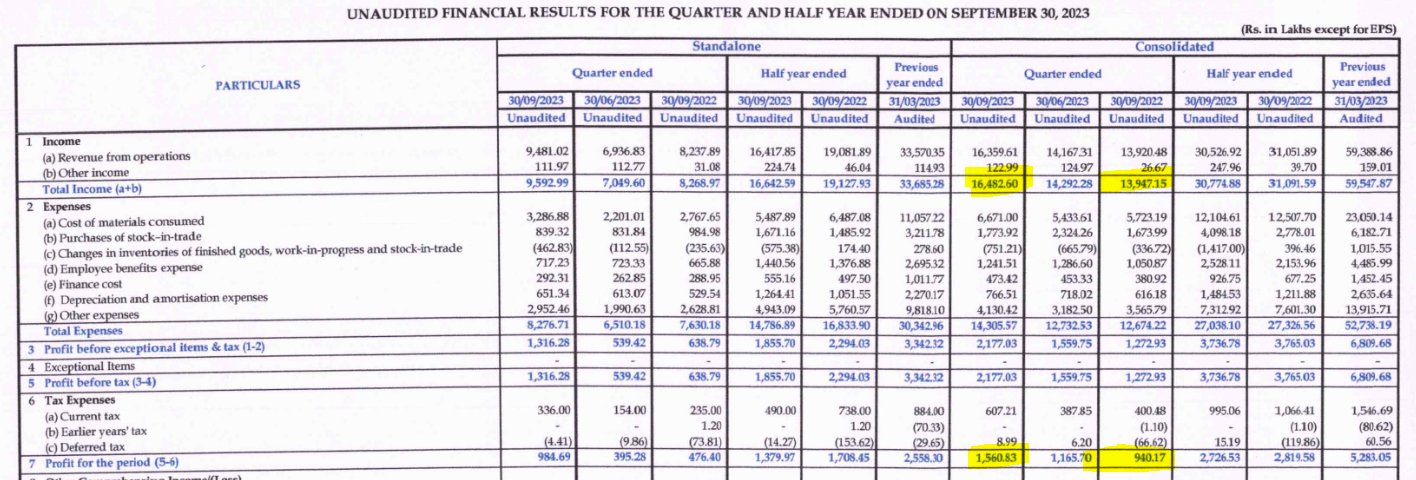

Sales - 164 vs 140 cr, up 18 pc

EBITDA - 33 vs 22 cr (up 50 pc, Margins @ 20 vs 16 pc)

Net Profit - 16 vs 9 cr

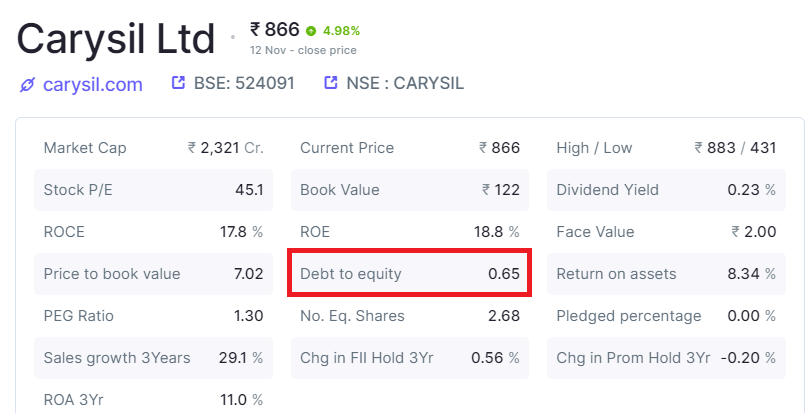

Gross Debt @ 210 cr

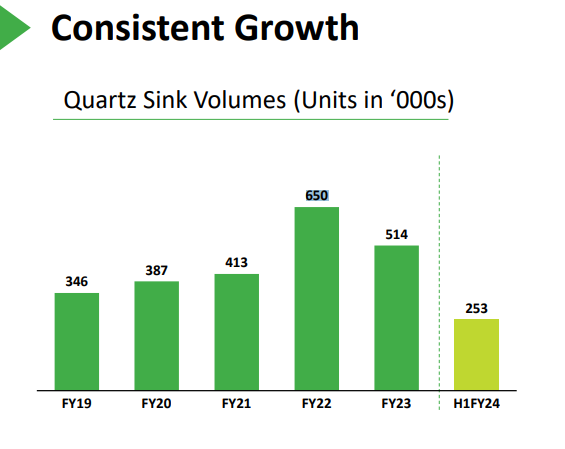

Sales growth led by increased orders for Quartz sinks from developed markets. UK subsidiary doing well. Additional Stainless Steel sink capacity has been commercialised. Have started building an order book for the same

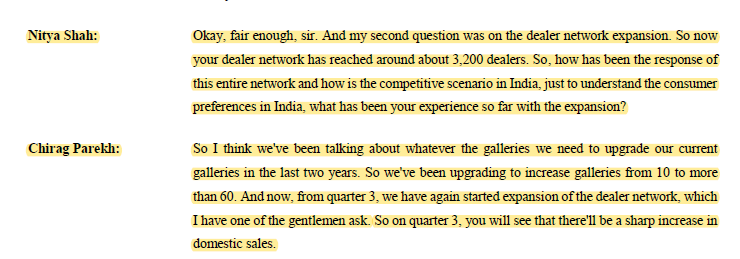

Expanding dealer networks in India. Domestic business likely to be a key growth driver going forward

Exports revenues @ 129 cr, up 21 pc

Domestic revenues @ 35 cr, up 6 pc

Product wise sales mix -

Quartz sinks - 49 pc

SS sinks - 13 pc

Appliances - 11 pc

Solid surfaces - 26 pc

Quartz sink capacity @ 10 lakh sinks / yr

SS sink capacity @ 1.8 lakh sinks / yr

Kitchen appliances that company is selling under Carysil brand - Chimneys, Wine Chillers, Dish Washers, Hoods, Cook Tops, Built-in Owens, Microwave Owens

Company has also entered bath segment - to sell washbasins, facets, premium sanitary ware

Company purchases Moulds ( imported ) to manufacture over 400 SKUs ( uses over 150 Moulds )

Moulds have an avg life of 15+ yrs

Current Pan India Dealer network @ 3200+, Distributor network @ 82

Expecting domestic business growth likely to see a sharp increase from Q3 onwards. Oct 23 saw good sales volumes in Domestic Mkts

H2 sales likely to be better than H1. EBITDA margins may see some expansion due operating leverage

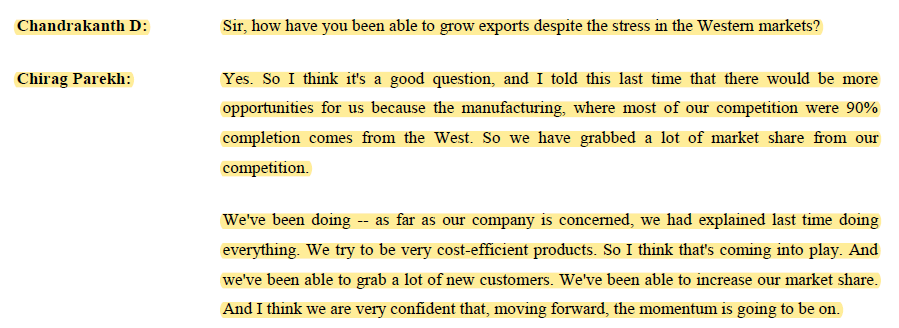

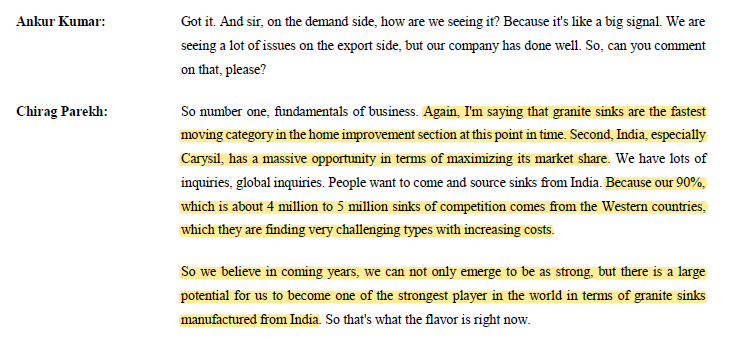

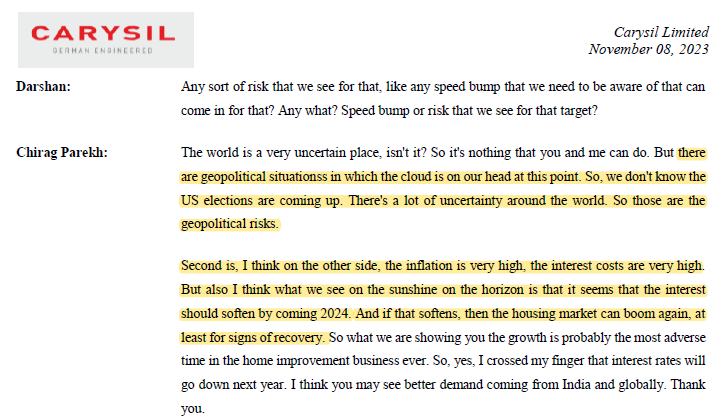

Company is gaining mkt share from its competitors in the developed markets ( most competitors are from Europe ) due product quality and lower costs - this has been the key for company’s growth despite Developed mkts witnessing broad based slowdown

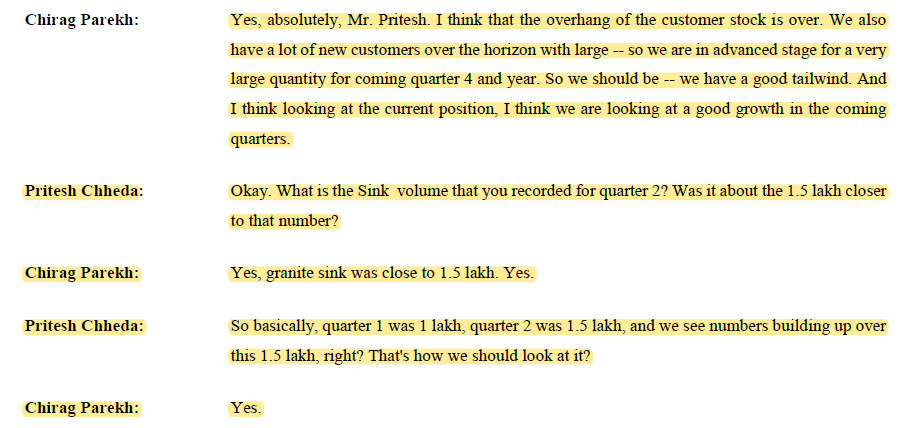

Inventory liquidation overhang in the developed Mkts is now over

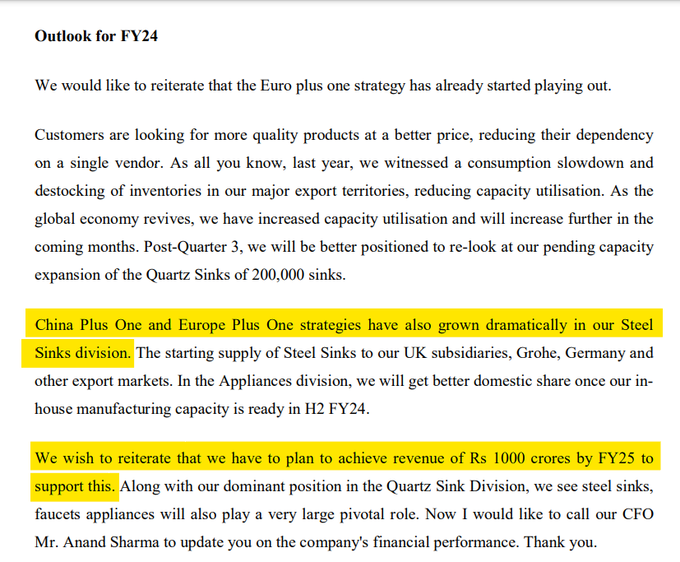

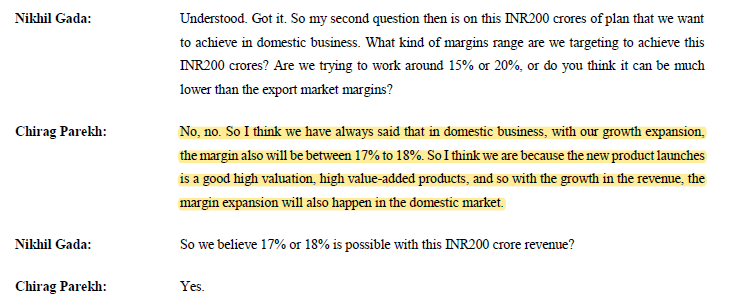

Aim to cross 200 cr sales in domestic Mkts in FY 25

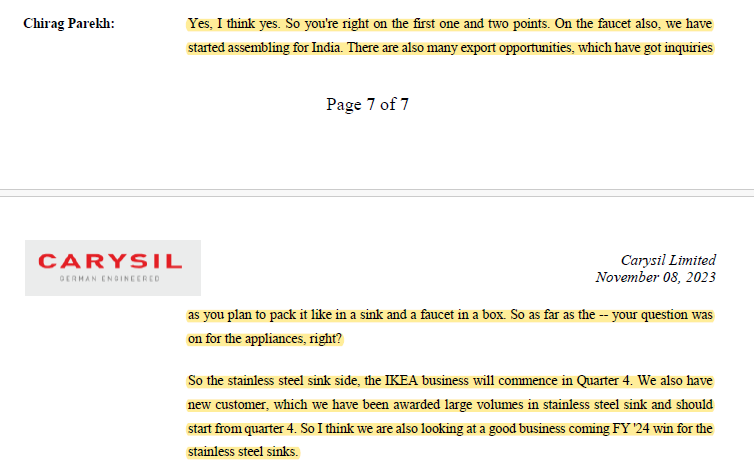

The Ikea business ( supply of SS Sinks ) will commence in Q4. Have a few more customers that are likely to buy good volumes of SS Sinks. This business is also likely to commence in Q4

Company has started its assembly operations of built in appliances in Q3. Expect to see good contribution from this segment as well in Q3

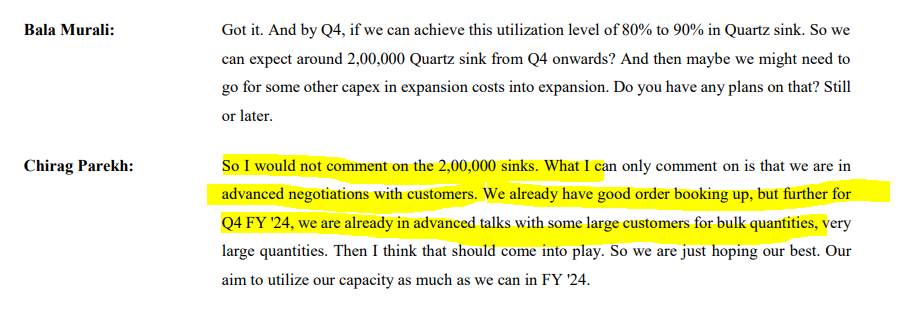

Company in advanced negotiations with big customers for bulk quantities of Quartz sinks. Things likely to materialise by Q4. This should sharply increase company’s Quartz sinks capacity utilisation

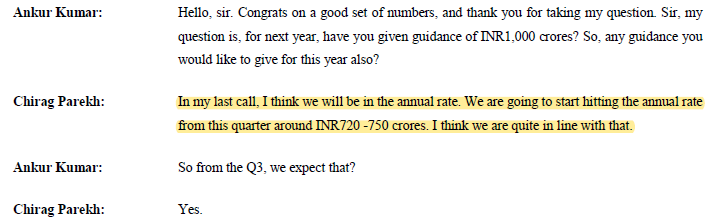

Management still maintaining its guidance of Rs 1000 cr topline by end of FY 25 with EBITDA margins of around 20 pc

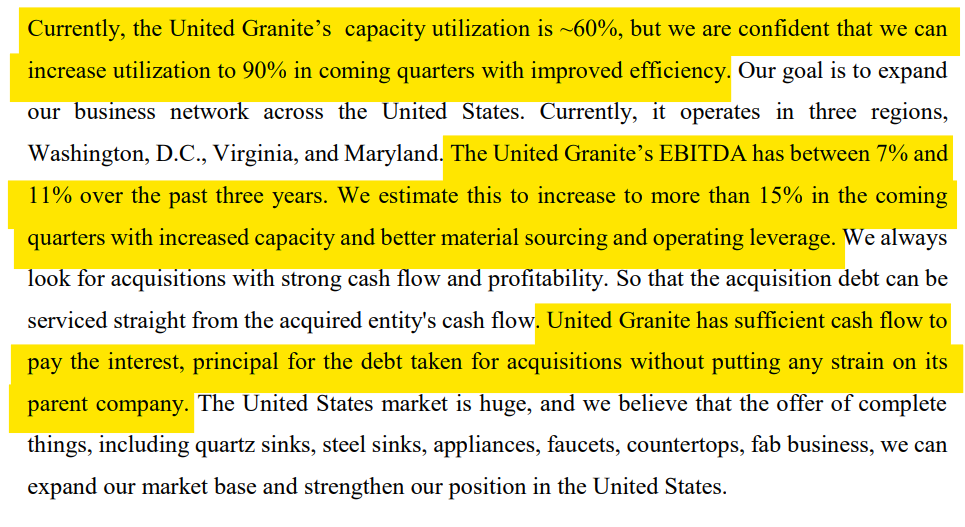

Company acquired United Granite LLC in US Mkt in Q2. Currently running at 60 pc capacity. At full capacity, this can do a revenue of about 120-130 cr. Company is engaged in fabrication of Kitchen tops for retail, residential and commercial projects. Carysil is confident of turning it around

Domestic business margins should remain in the 17-18 pc kind of band

Looks like Russia-Ukraine has been a huge blessing for the company - making European competition uncompetitive

Overall - good results with bullish commentary

Disc: holding from lower levels (25 pc lower than CMP), biased, not SEBI registered