valuation is slightly brought down now and it is definitely on the radar list for a new entry, and the reason for this could definitely be the result after Q2 and the ESOP they allotted and they posted a loss and by then it created a negative impression around… IoT-based companies will reach the ‘J’ curve only when it posts the successive quarter results one after every quarter and once it establishes this path it is definitely the key trigger to reach the new highs every now and then, I suggest not to average until the next quarter results are promising and maintain hold for few more days.

1 Like

The supply crunch of semiconductor chips could last upto the first half of 2022.

Decent analysis on the used car market in India.

PS:- CarTrade is still not a unicorn so far, yet they are a profitable company (as of 31 March 2021)

Disc:- Invested

4 Likes

@MHS Hey, Can you share the more context of your attachment, whose opinion got crafted in your attachment? Looks interesting but would like to cite the source or reference for the benefits of larger audience. Anyways, This is really interesting and thanks for sharing it

It was the view of Warburg Pincus. You can watch the interview here:

1 Like

@jsrvivek_k, I shared relevant car trade discussion of money control interview in the above post, it’s by Vishal Mahadevia, MD and India Head, Warburg Pincus.

See below link and please read the full interview for car trade info:

1 Like

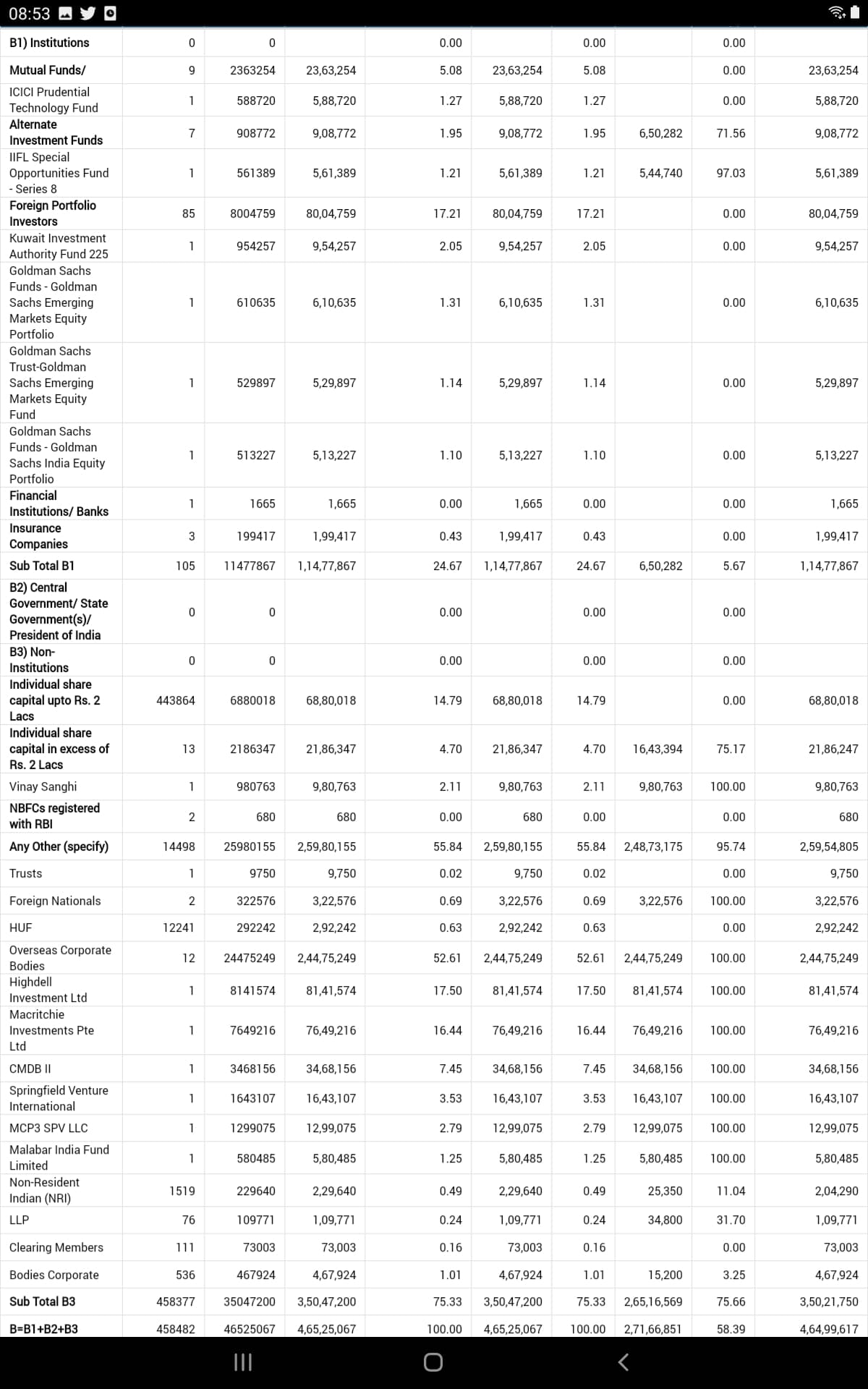

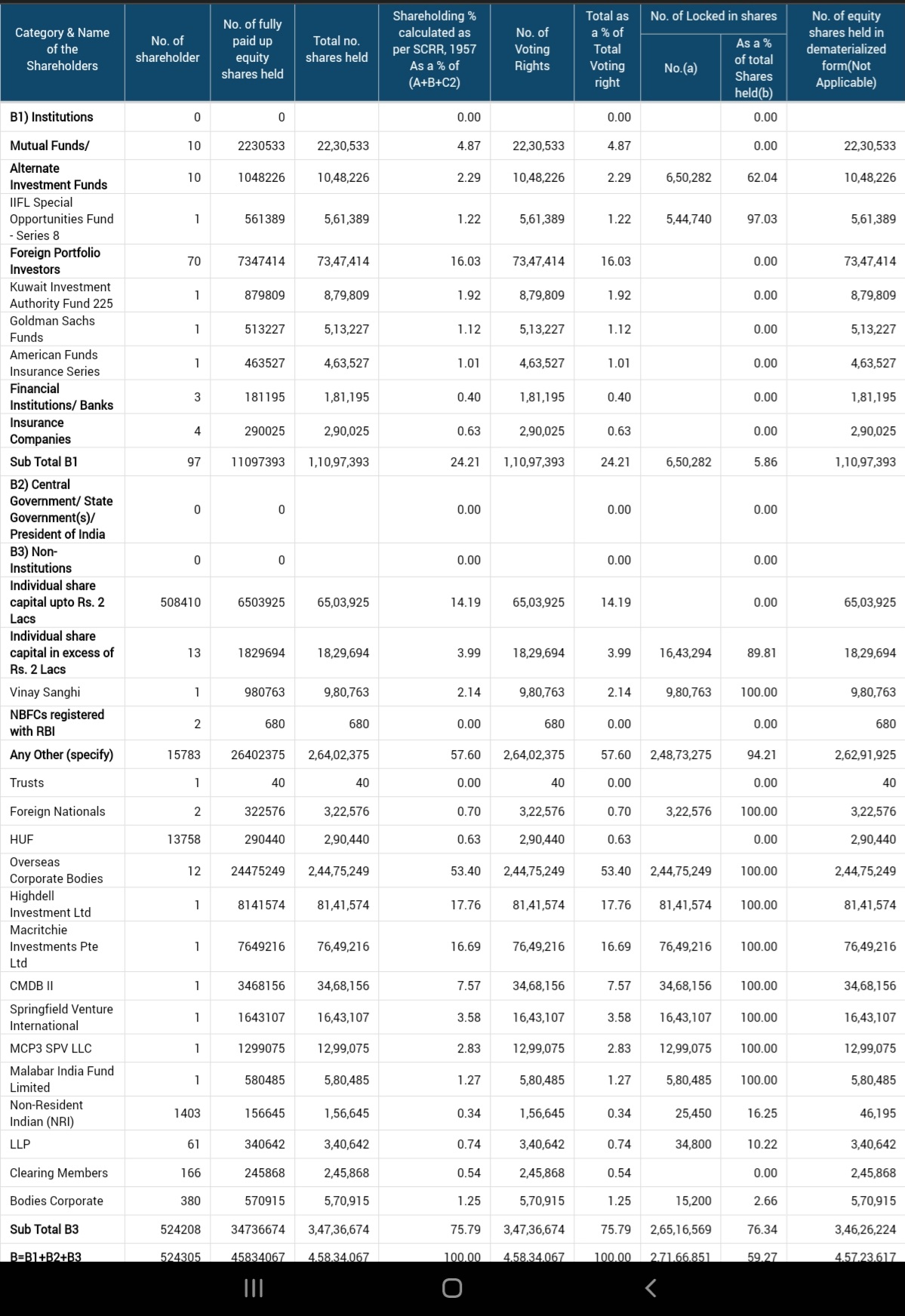

Cartradw SHP - Now Dec 21

Vs Sept 21

MF holding up by 22.3 L to 23.6L

Retail( 2L below and above together) up by 6L

FPI 73L to 80L+

Financial institutions/ banks + insurance + bodies corporate have sold 4L

Total issued capital itself is up by 7L

58% of total holding is locked ( Believe should be for 1 year).

Hopefully churn is over and weak hands are out.

Disc - re-entered with tracking qty based on technicals, Q3 performance snd commentary is key. Valuations are approx 10X sales and 30X EBDITAQ2 annualized) - closer to reasonable as long as high growth trajectory continues.

5 Likes

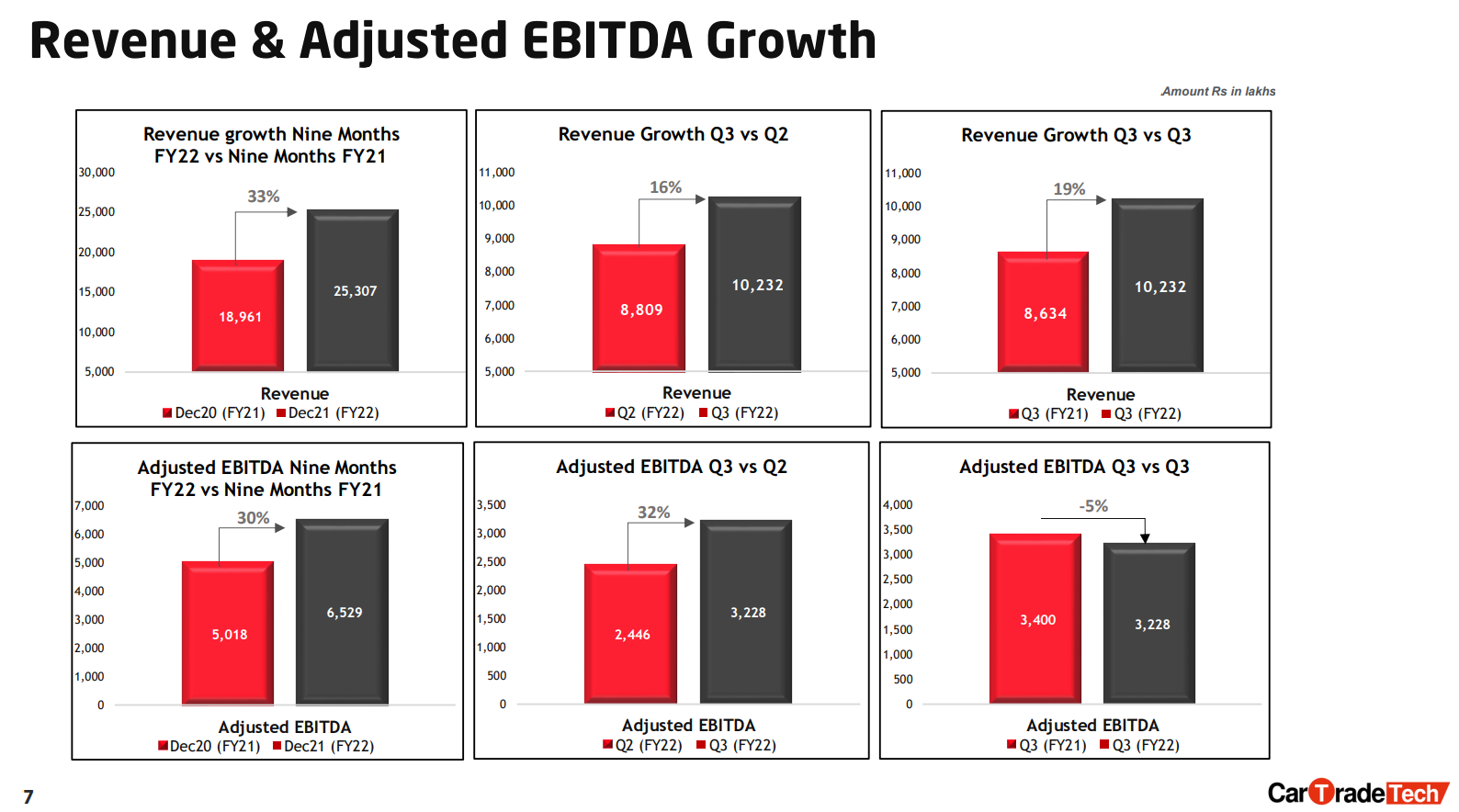

Key Highlights from Q3-FY22:

-

Revenue growth of 33% YoY for the nine-month period ended 31 December 2021

-

53% growth in the number of auction listings vs Q3-FY21

-

60% growth in the number of vehicles sold through auctions vs Q3-FY21

-

Expanding abSure outlets from 22 (currently present in 18 cities) to 200 over the next 2 years.

-

Organic Traffic at 86%

-

Highest ever quarterly revenue of Rs. 102 Cr achieved in Q3-FY22

-

ESOP expense hit on the P&L to continue until March 2022

-

Deployment of $100 million for strategic acquisitions and investments in the automotive industry over the next 5 years.

-

Headwinds due to semi-conductors shortage and supply chain constraints to continue.

Dis:- Invested

1 Like

FY22 revenue 350Cr, I would be surprised if anyone pays more than 7x revenue for these type of business, then Rs 525-550 is where I would invest in this stock, unfortunately it has to correct another 25% before forming a base

1 Like

Curious to know the reasoning and thought process - how did you get 7x revenue valuation? Did you benchmark it agaibst similar businesses? Why not 5x, or 10x?

Usually a multiple of 10-12x is ascribed to forward FY23 sales of Peer companies like carsales.com and Copart Inc.

ESOp treatment was a real disappointment since the adjustments over Fy22 amount to approx Rs 180 cr (of which Rs 140 Cr is provided for in the 9m financials).

What is comforting is the sales growth which continues at 25-30% and on Fy23E, valuations seem attractive at around 7.2x Mcap/sales. Since the company currently has Rs 800 crore of liquid investments on balance sheet, essentially the business is available for 75% of its current market cap.

Disc: invested

2 Likes

Q3 call notes

Not so good

- Numbers aside, mgmt need to establish an Investor friendly perception ( esp being newly listed and stock price halved from issue in matter of months) - call was late, rushed, with fast closing out( this was based on recording- live participants have vented frustration on Twitter as well) - these are manageable aspects.

- Mgmt sounded chest thumping over their own performance multiple times with 30:30narrative ( growth, margins), fact is other income have contributed meaningfully in overall income growth.Nothing wrong but better to split biz vs Treasury as investors eventually catch it and guy from Sundaram fund asked these tough questions, moderator booted him out.

Good parts

- Q3 and 9Mo FY22 they have done well inspite of industry (OEM side) degrowth,

- Retargeting biz- High volume growth YoY but not corresponding revenue and margins growth, Margins are higher in Retargeting biz but growth of bottomline was lower due to realization going down and salary impacts- this Qtr is normal base for realization.

- Media/Ad biz - YoY growth is 12% as Q3 21 had higher base due to pent-up demand, they expect good growth due to digital spend wallet share increase trend( India is 10% compared to 40% other mkts)

- Absure platforms transactions have 1.5 to 3% commissions, with value add services may go up, 20+ outlets now and 200+ in next 2 years - this is branded play

- MG India is using their software platforms - DMS software

Valuations are much more saner now, even if they grow organically at 25% and are able to deliver 30% EBDITA at consol - on q2 annualized 400 cr revenue ( ex of other income) and 3300 cr mkt cap(7000 cr+ cash), 120 cr EBDITA. Inorganic growth with their apparently efficient capital allocation in past( carwale and bikewale) can help growth further.

With 2 consecutive Qtrs results out, valuations thrashing by mkt and associated investors churn would have played out as was visible in Q3 Shareholding as well.

Would be good to see bottom formation on charts first, have tracking positions.

11 Likes

Does anyone have a break up of CarTrade’s revenue viz. commission income, listing fees, etc. or in terms of vehicles - cars, bikes, etc. How many sellers are registered and how many of them are paying. These data is essential to ascertain where the growth is going to come from? If anyone can share any of these details for last 2 years would be very helpful. Thanks in advance.

1 Like

Is it worth holding this stock for long term view? I do understand that currently market is very volatile, but would like to understand whether the fundamentals are strong enough that it will come out of its price downfall.

Many times it is interesting to study similar stocks from the mother market (US). Carvana is USA based company, the stock is down 93% from the recent pick.

Disc: I don’t track Cartreade but seems both have the same business model. I come across Carvana’s story and thought to post it for VP friends. No views nor investments.

4 Likes

I have this question, cartrade has about 1,933 crores in book. is this entire amount parked into fixed deposit and if so what is the mode they paid back? Is it paid yearly or quarterly? In the current quarter I see 9 crore+ in other income category. Does it mean this other income is the credit intrest they received from parked money ? And is it is fair assumption to consider runrate clock is 36 Cr fr an year term.

2 Likes