A decent article summarising the online automobile platforms. Some figures do not marry with each other and seems lacking in due diligence but nevertheless a good perspective.

ESOPs issued at price as low as Rs. 21/share (98% discount @ CMP of 1280) plus no lock-in on the same. Looks like a very big red-flag to me.

Found a decent article related to Institutional Investors voting against ESOPs.

https://worldfishnews.com/institutional-investors-red-flag-india-inc-s-esop-schemes-227341.html

Disc:- Invested from IPO levels

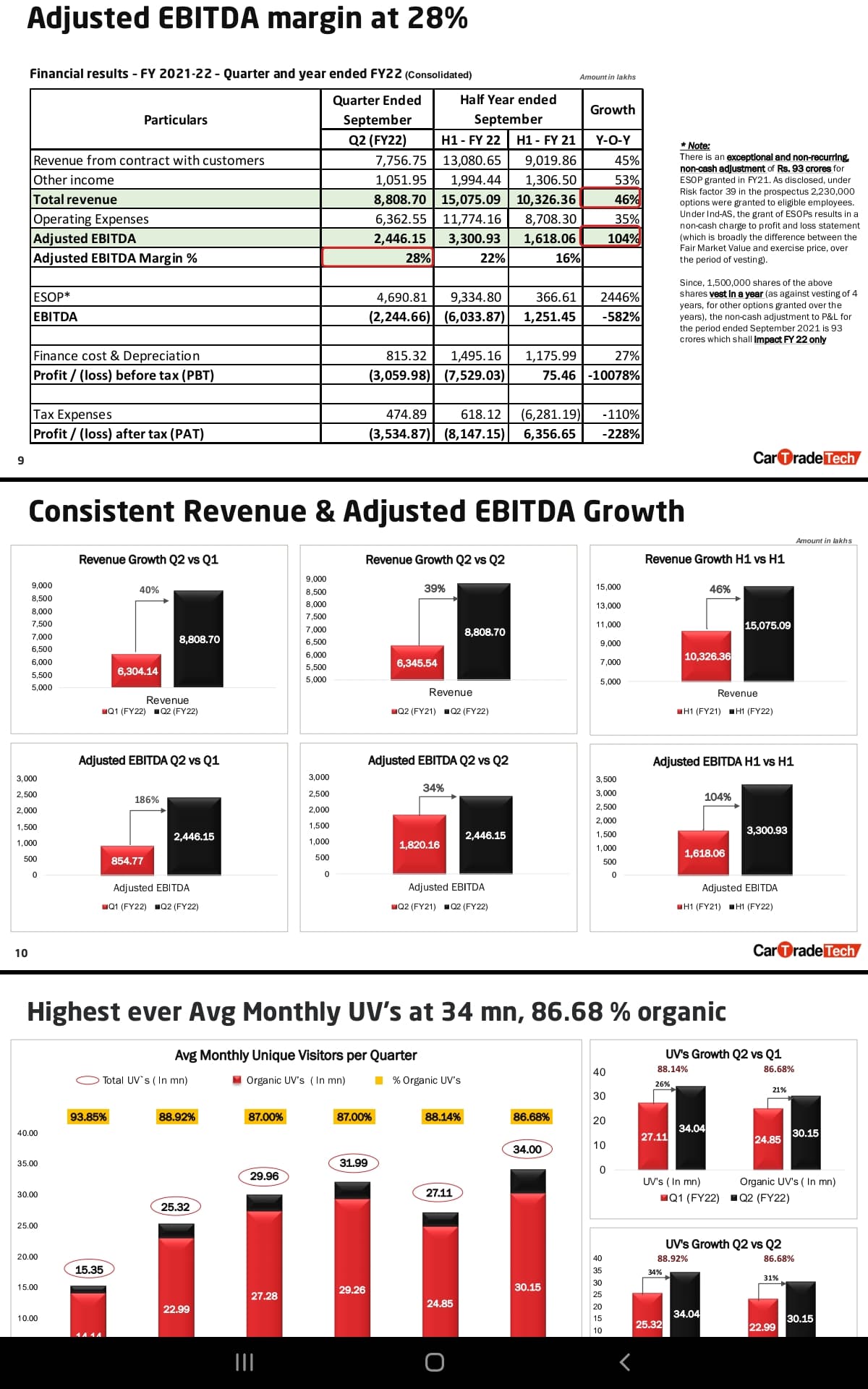

Q2 presentation

Key takeaways

- Operating leverage visible, QoQ and YoY solid growth in revenue, EBIDTA

- Annualized revenue approx 300cr and EBDITA 100cr

- Organic traffic share continue to be in high 80’s ( key monitorable and good to see it holding well)

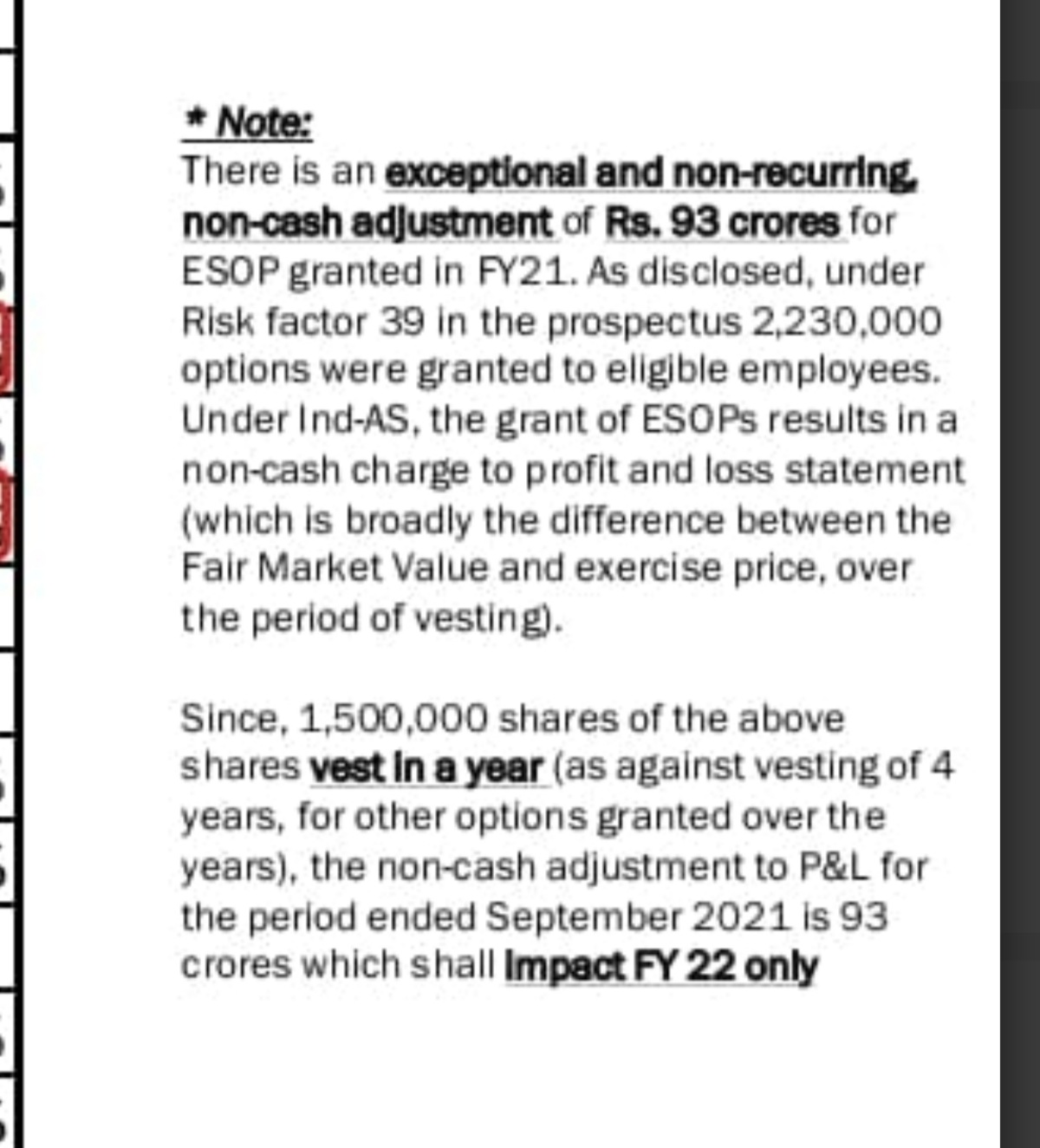

- fresh ESOP cost impact reflects negative PAT, majority share impact absorbed in FY 22 - need to understand more

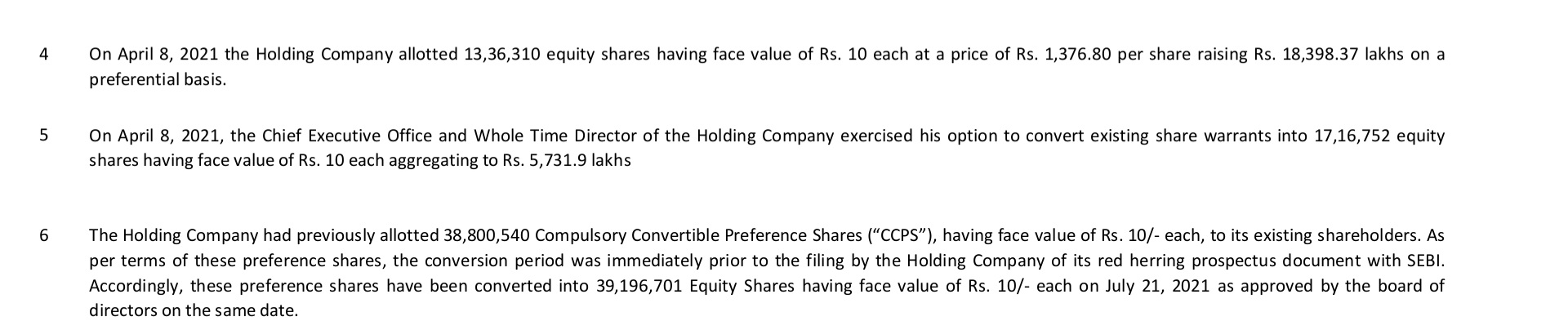

- preferential allotment in June to IIFL wax at 1376/ share - which seems fair

All in all good results for first Qtr

Invested

Hi. Don’t you think this is unfair to the retail investors if ESOPs are issued at such a huge discount? Pre-IPO, they just have an expense of 3.66 Cr for ESOPs in H1-FY21 and now, it has zoomed up to 46.9 Cr in H2-FY22 (15x). Need to investigate further on what basis these ESOPs were issued and how did they arrive at such a low price.

We are likely to see ESOP issues, multiple fund raise right before IPO raising valuations etc, in all of these new age companies- in their defense they do disclose in RHP.

As investors it’s up to us to pick what works for us within our risk framework , there is cleatly appetite in market no matter how illogical or unfair it seems.

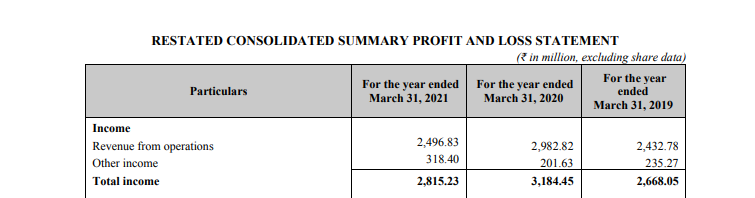

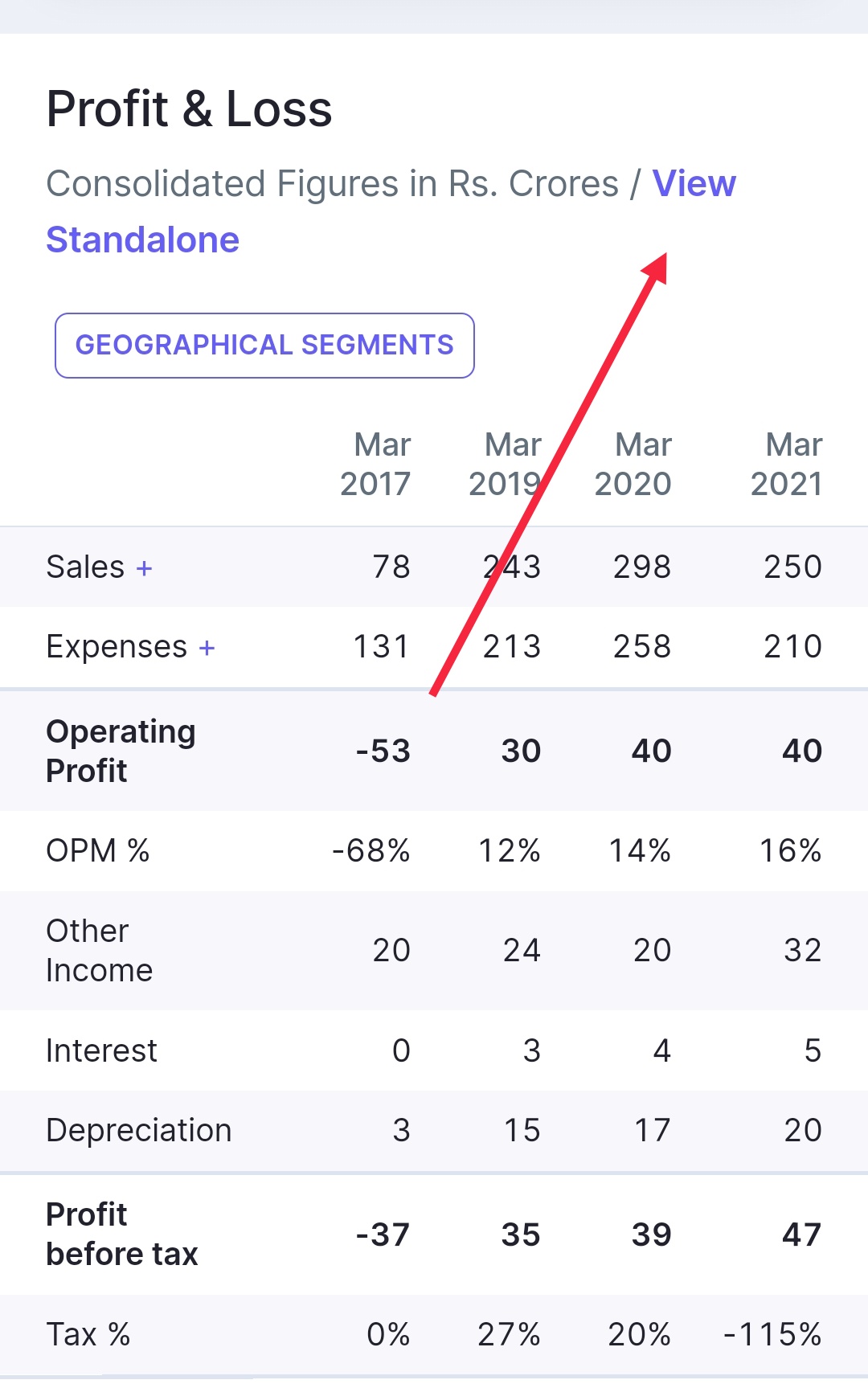

What is interesting to note here that the H1 results indicate that CarTrade remains the 3rd largest player in the space (based purely on revenue) behind Cars24 and CarDekho and most probably ahead of Droom and obviously the only profitable one. Although there has not been much reports about FY21 numbers for CarDekho but from 700+ crores revenue it is unlikely to fall behind so quickly.

It would also be interesting to see how true are assertions of market shares by various players in the future. Droom has been making various contradictory claims about market size and market share , here (Droom founder explains why he is considering a US IPO and where he intends to spend the money) and here ( Droom looks to raise ₹1,000 cr from share sale early next year)

With Droom’s planned listing more market numbers should shed light on the sector and the players. Personally, CarTrade valuations are still on the higher side and am waiting to see revenue growth trends, market shares and CarTrade’s own upscaling (these results seem decently encouraging in terms of revenue growth, cyclical nature means that H2 should be even better)

@sai_sirish : On the ESOP allocations certainly not ideal but I am afraid this is what will increasingly happen in the new age Fintechs/Digital companies immediately post listing. If this trend (ESOPs at disproportionate discounts) continues beyond 9-12 months after listing it would worry me significantly.

Note:

- All revenue numbers are from articles in this thread

- Invested with a small tracking position.

My understanding of this business model is that online platform space is not the diffrenciator anymore but only the one who can execute the brick and mortar version of in a very asset light way. This will define who eats the largest pie of cash flows, which enables scale up of this model with least financial cost which in turn generates larger cash flows and cycle goes on. But its a good fairy tale as now we have foreign investors and cash flows of Ola - problem of plenty of cash to burn in this space which creates a scenarios “Hum bhi nahi kamayenge, tumhe bhi nahi kamane denge” as we have piles of cash to burn in name of "acquire market Share, irrespective what we make net net " - eventually customer will win but that may break CarTrade offline model as being a public setup now this investor base is not aligned with “Market share first” theory.

Long story short - When there are entrents with huge cash and market-share first KRAs “baisa nahi banta kisi ka bhi”.

Disc - Invested since IPO but now questioning my earlier theory myself.

CarTrade is currently trading at a valuation of ~$750mm, which is still cheaper when compared to peers like Cars24. This is at a discount of 23% to even the pre IPO round done in April.

There seems to have been a panic selling by some of the investors after the company reported loss in Q2. IMO, going by the valuations of other internet companies CarTrade is not expensive especially if one is looking at a 2-3 year horizon.

That’s like saying Indigo paints is cheaper than Asian paints ![]() Absolute numbers tell us nothing about valuation. Please check CARS24 revenue and you lll understand

Absolute numbers tell us nothing about valuation. Please check CARS24 revenue and you lll understand

Cars24 uses a different revenue recognition policy as compared to CarTrade, which is why their revenue is higher. The same was discussed by the management in one of their calls. Here’s the link. CarTrade Tech - A Multi-Channel Auto Platform - #16 by Fiddly

And from valuation POV, it’s not cheap at all. At the upper price band of their issue price, the Price to Sales was a mind-boggling 30x. It’s like saying for every 1 rupee of their sales, they want you to pay 30 rupees. Current price to sales is still high at 22x. Hope this clarifies.

Thanks for clarifying🙂

Kindly re-check.Screeners shows that FY21 sales were around 250 Cr. Current market cap is 5500 cr. But you are right.it’s still a very expensive stock

Data on Screener.in is incorrect. As per RHP, Sales are around 250Cr. Thanks for the clarification. Will update the numbers accordingly.

Revenue recognition for both companies are different. The key differences between the two companies business model is a) Cars24 is present in international markets (which justifies a higher multiple), b) CarTrade is also into commercial equipment reselling which Cars24 does not offer at present.

Institutional investors typically have a different way of valuing companies. Ratios like Mcap /TTM Sales and P/e are given low weightage for companies in high potential markets growing revenue at 30-40% yoy.

You are right. I checked and found that after adjustments,their topline is comparable (Mr sai was kind enough to point it out to me earlier). Apologies

Most VC/ PE firms only care about potential valuation at exit. The greater fool theory

Although this has been commented on quite a bit but still let me clarify my meaning of high valuations here. I believe both the IPO price of CarTrade and the valuations of new-age Fintechs/Digital companies in general (more so someone like Cars24 or Droom) are too high. I did not mean to make a comparison between peers but rather speak from the context of how I would value a business. Even accounting for some premium I would not be comfortable on a stretch case paying anything above 7-8x sales.

My fundamental thesis is that some mean reversion will happen in CarTrade (and also others like Zomato etc.) at some stage and that’s why (although I like CarTrade’s business) I only have a tracking position currently. Where I am torn is that there are increasingly businesses which do well and continue to trade at very high PE multiples so I am not sure whether valuations will ever reach my comfort zone here.

So although I think some mean reversion will happen (a significant amount has already happened here) I would wait a bit more and also look out for some more data on CarTrade’s business progress. That’s why I would also closely want to look at Droom’s listing and RHP as it would give even more data about this business segment. Would probably take a much more decisive position here after Q3 results or Droom’s RHP (whichever happens earlier)

Hope this clarifies the context.

CarTrade sites always show up in top 2 results while searching Google for any car in India market. Their SEO capabilities seem to be top notch. I think growth will catch up soon with the valuation. These companies have multi decade of growth opportunities in front of them. Only execution is the key to unleash the potential.

I want to know like why someone would hold it as there is zero percent stakes which is acquired by promoters, I have also invested in this since IPO, so I would like to if it will rise even up to its listing price?