Attached chart of careerpoint shows a double bottom formation.

risk reward seems favorable.

comments on charts.

Attached chart of careerpoint shows a double bottom formation.

risk reward seems favorable.

comments on charts.

Conference Callfrom Capital Market

Career Point

Aims to recover the enrollment in FY’14

The company held its conference call on 13th Feb’13 and was addressed by key management

Key highlights

| Conference Call key highlights by Capital Market |

|

|

The conference call on 14thAug'13 and was addressed by Pramod Maheshwari CMD

|

Highlights of Conf Call by Capital Mkt:

The consolidated net sales decreased by 15% to Rs 16.96 crore while net profit declined by 76% to Rs 1.86 crore for Q2 FY14.

The mgmt said it will see improvement in Q3 and Q4 compared to H1 FY14. However, it will not be able to recover the enrolment and revenue loss of H1 FY14.

The company’s margin suffered due to fall in top-line in tutorial business.

Employee cost up because of addition of one resident campus in Kota and rise in salary of faculty members.

Tutorial services division has enrolled more than 6500 new enrollments in the second quarter of current academic session, despite changing market dynamics.

The company owned tutorial centers are 12025 at the end of Q2. Avg. realization per student has increased by 8% to Rs 40000.

The company has rolled out the launch of CP STAR (Scholarship Test for Admissions and Reward) for the next academic session and achieved a phenomenal response from the students.

The first of its kind, CP Gurukul â a residential school cum coaching campus - has attracted more than 700 fresh enrollments in very first year of its operations. Looking at the strong demand, it is going to improve its enrolment from 700 to 1500.

The company has launched tutorial test for GATE with focus on 4 engineering branchs.

In the education business, the company has enrolled more than 1800 students in various 3 to 4 years program.

It has enrollment close to 1000 new enrollments at higher education institutions in their second year of operations demonstrates an academic excellence of these institutions

The launch of two new schools at Kota and Jodhpur in Rajasthan with 200+ enrollments each in the first academic session has created a benchmark in their respective regions.

The company has around Rs 51 crore of net cash and cash equivalent.

The mgmt said that for next year it expects improvement in tutorial business with improving economy, student adjusting to new exam system and residential system started by the company.

There will be no significant capex for tutorial business. In formal education business, capex for next 1.5 years is Rs 20 crore for its university. It will be funded through internal accrual.

Formal education will contribute around 20% of top-line for this year.

For FY15, the mgmt expects 25% top-line growth in tutorial business and 30% growth in formal education business.

Concall was addressed by Mr P Maheshwari CMD. Highlights by Capital Mkt;

The consolidated net sales for 9 months ended Dec’13 was down by 23% largely due to lower enrollments in tutorial divisions, due to lack of clarity on syllabus and examination pattern. However enrollments for Q3 FY’14 stood at 3180 as compared to 1705 enrollments on YoY basis. As per the management, this clearly shows that the tutorials concern is over now and enrollments are coming back once the clarity emerged with the syllabus structure and examination pattern.

As per the management, for the next academic year, the enrollments have already started and they are up by around 50% YoY.

As on Dec’13, the company has total of about 13 company owned centers, 13 franchises, 2 CP live centers and more than 60 test series centers. Company has added 3 new franchises namely in Ahmedabad, Akola and Bareli during Q3 FY’14.

With enrollments coming back for tutorial business and returns started to emerge from the investments made in formal education business, management expects better earnings and margins going forward.

The first of its kind, CP Gurukul â a residential school cum coaching campus - has attracted more than 1500 enrollments as compared to 700 same period last year. It’s operating at nearly 100% capacity utilization rate.

The formal education is a high entry barrier business and initial investment is high. The company has done its investment phase and now the growth phase will begin. Company will leverage upon its assets to increase the overall ROC.

There will see no significant capex for tutorial business. In formal education business, capex for next 1.5 years is Rs 20 crore for its university. It will be funded through internal accrual.

For FY15, the mgmt expects 25% top-line growth in tutorial business and 30% growth in formal education business.

**Call add by Pramod Maheshwari MD.**Key Highlights BY Capital Mkt

For the nine months ended Dec’14, no of enrollments stood at 22108, up by 16% YoY. The company already made up with the lost enrollments that it had to suffer last year. The company has sufficient capacity to make sure the enrollment reaches to around 30000 with same capacity. So lot of operating leverage benefits will arise from here on.

Further, this year there were more enrollments in Class 11 and hence the pace for next achedemic session enrollment is already visible.Unlike in past years where enrollment used to be focused and dominated more only on engineering side, the enrollments now are more or less even out in between Pre engineering, Pre medical and Pre foundation exams.

Enrollment in branch and company own centers have shown decent growth, while there was a decline in growth in franchisee enrollments. Company had shut down 2 of its franchisees. Going forward, the focus will be more on company owned centers.

On CP gurukul residential coaching and campus business, full capacity has been reached in 2 years time with total enrollments of around 1320 with tutorials and schools both. Higher growth was seen in students enrolling for both schools and tutorials leading to higher realization per student.

In Formal education business, for 9 months, the school education enrollment stood at 2627 and higher education enrollment stood at 2307. New enrollments have resulted in increase of around 40% YoY in auxiliary education fee income. Universities and Other higher education institutions are in just 3rdyear of operation. 2 schools are in 2ndyear of operations. Hence growth momentum will continue in subsequent years.For 9 months ended Dec’15, the formal education income stood at Rs 2.45 crore vis a vis Rs 1.74 crore YoY.University projects are already out of gestation in their 3rdyear of operations against industry trend of 5 years.

Company has some land parcel with book value of about Rs 44 crore, which it plans to sell in next couple of years. It has market value of more than Rs 125 crore.Capex requirement in formal education will be around Rs 5-10 crore in next year.Company is a net debt free company at consolidated level.

Going forward, the focus will remain on margins from almost all the segments. On sales side, management expects sales to grow around 25-30% going forward.

Hi Hemant,

what do you think of the valuation? It trades at 300 crs. for negligible profits (roughly 7 odd crs. in F15?). What do you think is the medium term cash flows which would make it either attractive or perhaps not so attractive?

Also, ICICI and Reliance AMCs have been selling down their ownership. I would view that as a negative. On the flip side, I have sometimes found institutional selling to be a contrarian buying signal. Depends upon how tired the institutions are.

In summary, what are your key buying arguments for Career Point?

Thanks, Anil

I would add my worries for the stock.

Why do this company need to venture into NBFC which is essentially a low RoCE business. This way it will take additional burden of receivables of few yrs’ tenure. I fear it might be going Jain irrigation way when the stock was punished heavily for venturing into NBFC space. They should have exited cash guzzling real estate stuck in schools biz as well. It seems recent run up is due to quality investors (Ajay Relan, Sandeep Sabharwal … ) jumping.

It would continue to show stellar growth due to the size of opportunity but quality of business has gone down by one notch.

Hi Hemant,

what do you think of the valuation? It trades at 300 crs. for negligible profits (roughly 7 odd crs. in F15?). What do you think is the medium term cash flows which would make it either attractive or perhaps not so attractive?

Also, ICICI and Reliance AMCs have been selling down their ownership. I would view that as a negative. On the flip side, I have sometimes found institutional selling to be a contrarian buying signal. Depends upon how tired the institutions are.

In summary, what are your key buying arguments for Career Point?

Thanks, Anil

Sumit,

Actually I am not so negative on NBFC front. Some of these NBFCs are quite profitable. A major cost for NBFC is client acquisition, which is zero in case of captive NBFC. Later on, it can be spun off at a multiple of book. But that assumes they will make a success of NBFC. It has a clear negative that initial equity would have to be provided by CP, burdening their balance sheet.

Management have declared their intention to sell and lease back the school land. Though I am underwhelmed by the loss on their first sale transaction. Hopefully they will make profits on the remaining sale and lease back transactions. While margins would decline (due to lease rentals), the capital efficiency would rise. Theoretically, some of that released capital can be used to fund the NBFC.

But I would love to understand the reason for sharp decline in fortunes in the past few years. FUrther, what are the chances of such decline in fortunes being experienced in future?

All in all, education businesses are high margin, and enjoy high valuations. I dont know whether the current valuation leaves enough on the table for new investors.

Regards, Anil

Anil,

The sharp decline in business is well documented. It was due to changes in format of IIT entrance exams where emphasis is being given on +2 marks as well. They seem to have recovered but competition has also grown in the meantime. I would say that education is high margin business for sure but not necessarily high RoCE business. Look what happened to Tree house and others. They keep diluting equity to maintain growth. I would love CP to remain a vocational and coaching entity rather than running schools where scalability is low.

Hi Anil, I had merely gave the highlights of concall, so if any one tracks the co , it might helps them.I am not holding any shares , nor i am tracking this company.Hope this clarifies the matter.

Conference Call - from Capital Markets

See around 20% growth in net sales and higher operating margins in FY’16

The company held its conference call on 27th May 2015 and was addressed by Pramod Maheshwari MD

Key Highlights

• Tutorial Enrollments grew by 9% to 22412 in FY'15 on YoY basis. Average Ebidta margin which used to be around 35%, had dipped to as low as 3% in FY'14, now reached at around 17% in FY'15. As per the management, the issues on change in syllabus and education pattern etc were a past thing and now things have stabilized.

• The growth was led by contribution from all the verticals including Pre-engineering, Pre-medical and Pre-foundation. There is a significant rise in 2 years long term classroom programs which sets a base for next year's enrollment growth in advance.

• Class room enrollments grew by 17% to 12946 in FY'15 on YoY basis. Gurukul Campus Enrollments in FY'15, which is the 2nd year of operations show enrollments of 1320 as compared to 674 in FY'14. Higher growth was seen in students who opt for both school and tutorial services vis a vis only tutorials in the past

• As per the management, there is a good amount of scope for operating leverage to start in the business.

• In Formal education also, enrollments in FY'15, grew by 53% to 4954. 2 schools are in 2nd year of operations and universities and higher education institutions are in their 3rd year of operations.

• The company has started a day school in Billaspur in Q3 FY'15. The company will provide and built the entire infrastructure and the institute will operate on its own. The company will charge a onetime fee along with a 10% of revenue as its fees every year. There is no capex involved in this model of business.

• The company has also launched new courses in Kota namely MS in lifesciencs, Diploma in law etc and is also planning aggressive in skill development programs which the management expect to kick start from H2 FY'16.

• Adjusted on like to like basis, after removing the subsidiary performance which was sold off in FY'15, consolidated income was up by 20% YoY to Rs 65.52 crore and consolidated PBT was up by 441% to Rs 10.09 crore YoY.

• As per the management, when the company reached about 32000 enrollments, its operating EBIDTA would be back in the range of around 35%.

• For FY'16, management expects about 25% growth in tutorial enrollments YoY and about 33% growth in formal education business. Growth in vocational program enrollment would depend upon government sponsorship program. So far the company has received training order of 1500 students and 200 are receiving the training currently.

• In FY'16, management expects operating leverage to come in and margins to grow much higher than topline growth. Thus overall for FY'16, topline growth will be around 20% with higher Operating Ebidta margins.

• No significant capex in FY'16, Rs 7 crore capex for up keeping and construction activities

• As per the management, Kota is a gold mine as far as formal and informal education is concerned. There is a significant surplus capacity in Kota and the first strategy is to leverage upon the enrollments and margins in this place. Then the company has plans to venture outside Kota as and when the capacity is filled up and used optimally.

• The company is carrying debt of about Rs 43 crore and liquid investments of around Rs 50 crore as on Mar'15.

• The company is also sitting on land parcel of more than Rs 44 crore, with market value much higher than the books. At appropriate plans the land parcel will be sold off.

• The company is carrying a MAT credit of Rs 4 crore as on Mar'15. So while normal tax rate for the company is about 30%, effective tax rate for FY'16 will also be lower.

Disc: Was Invested, but sold off in market correction due to low conviction and pf consolidation.

FY15 Investor presentation by Career Point - http://www.bseindia.com/xml-data/corpfiling/AttachLive/3225CD45_6FB2_4110_9630_12C9F68720D9_110444.pdf.

On track in turning around and becoming an asset light model company.

Disc: Invested and may be biased.

Q1FY16 results are announced: http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/947A550B_FBE8_4ED7_BF1E_C7073094ECAA_083425.pdf

Summary:

Notes:

Disc: Invested

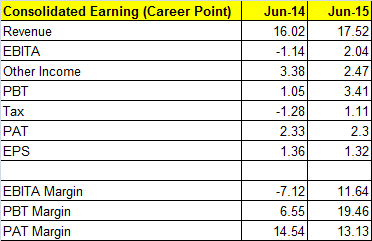

Hi @kmuthu_gct, how did you arrive at EBITDA of Rs.2.04cr. for June 2015??

Profit before interest and Exception Items is Rs. 4.51cr. add depreciation of Rs. 1.32 cr. to it and EBITDA is 5.83cr. implying EBITDA margin of 33% (and not 11.64%)

Even if you take Profit for operations before other income, interest and exceptional items of Rs. 2.04 cr., you missed adding depreciation of Rs. 1.32 cr. to it. EBITDA from this method is 3.36cr implying EBITDA margin of 19%

Thanks @invpriyaa for sharing the correct version. Sorry my bad. Was using EBIT instead of EBITA for margin calculation.

There is an investor presentation shared which is having all the related details - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/F947EBCE_0A27_40F4_B066_CFAA73EDDEE8_120107.pdf

-Muthu

anybody attending forthcoming agm on 26th september.

Just listening to June con call. Mr. Maheshwri says most states have got rid of PETs and gone in JEE route. Looks like its a permanent move, looks a bit worrying

CONFERENCE CALL - from Capital Markets

Career Point

Margins to improve further

The company held its conference call on 8th February 2016 and was addressed by Pramod Maheshwari MD

Key Highlights

For 9 months ended Dec’15, tutorials enrollments grew by 3% to 22743. Growth was seen despite closure of 2 inefficient centers. Ebidta margin of the segment stood at 25% as compared to 16% YoY. For 9 months ended Dec’15, in Formal education also, enrollments stood at 6827 as compared to 4954 enrollments for entire FY’15.

Within formal education, the enrollment for higher education stood at 3455 and school education it stood at 3372. Further, lower enrollment was seen in short term courses while higher enrollments were seen in long term class courses.

For 9 months ended Dec’15, consolidated net sales stood at Rs 56.07 crore, up by 6% YoY. However adjusted for sale of automotive division which was present last year, consolidated net sales have increased by 14% YoY.

Loans and advances stood at Rs 140 crore which is predominately the loans and advances to universities and related parties for setting up schools and other reasons which includes Rs 60 crore towards receivables as well from these universities. Management believes this figure of Rs 140 crore will in next couple of years will reach to around Rs 20 crore.

More gurukul campuses were planned during the quarter with regulatory approvals obtained for Mohali. Company aggressively is building capabilities and scale for the integrated residential coaches.

The company is using online media very aggressively and has built a B2B digital library for schools. It was able to sell first of its license to one of the school as well. Steady board.com website was launched and mobile apps have reached to more than 2500 active users.

The company also launched Global kids in preschool segment with 2 franchisees already confirmed and have started the schooling.

Going forward, the management expects the margins to improve as further operating leverage kicks in. Margins in next couple of years can reach to around 35% from currently around 25-27%.

Management continues to remain optimistic on Enrollment growth and aims to reach the peak level of enrollments of around 30000 achieved in the past, in the next 2 years of time frame.

No significant capex in FY’16, Rs 5.5 crore capex for up keeping and construction activities of which around Rs 5 crore already spent in first 9 months ended Dec’15.

The company so far has received around Rs 4 crore of formal education income and around Rs 6 crore of interest on Rs 140 crore of capital employed in formal education segment.

Kota centre alone is expected to grow around 10-13% on YoY basis as compared to around 5-7% growth expected generally for the coaching centers.

The company has already signed MOU with Central government and Rajasthan government on skill development programs. Already 1500 students have enrolled and it’s a 3 months program wherein the company gets around Rs 10000 average fees from government. Margins hover around 30% in this segment.

The EO item of Rs 0.87 crore for the Dec’15 quarter, represents some book loss on asset sale transaction.

The company has cash and equivalent of Rs 65 crore. A total borrowing stood at Rs 44 crore and an equal amount is lying in the liquid investments.

The company will sell the land, whose book value is around Rs 44 crore, as and when appropriate value is received.