fe718cca-3c54-4604-b93d-2d5bc67378f9.pdf (833.8 KB)

Results are not good. Can we infer that credit cycle is still not picking up or care losing it’s market share due to ilfs fiasco?

fe718cca-3c54-4604-b93d-2d5bc67378f9.pdf (833.8 KB)

Results are not good. Can we infer that credit cycle is still not picking up or care losing it’s market share due to ilfs fiasco?

Looks like CARE this year going to report worst earnings than it reported during 2012- 2013 economic downturn, whereas CRISIL going to report mild single-digit growth in revenue from their rating business.

Is that means CRISIL gaining market share from CARE?

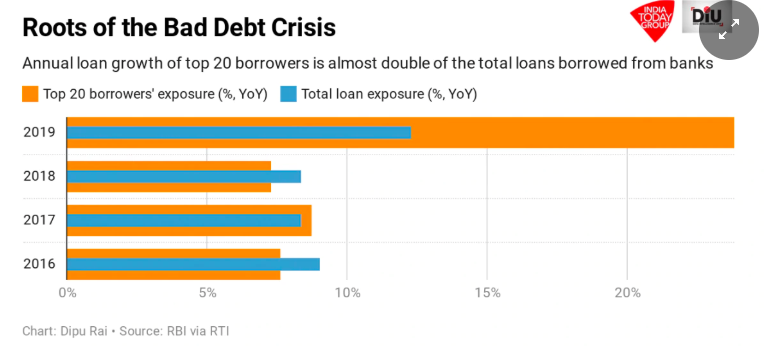

Not only Equity but the Incremental Debt also went into top 20 companies -

During FY12-13 they were doing about Rs 100Cr of net profits and I estimate Fy19-20 they will do around Rs 87-90 Cr of net profits. ( At today’s Mcap Rs1976 Cr, it’s trading around 22x earning, Stock did touch its FY12-13 lows ) , Since listing they have never reported net profits less than Rs100Cr most probably this year they are going to do it.

What is interesting is the inflation/interest rates were very high during Fy12-13 RBI repo rate peaked around 8.5% Vs 5.15% today, About 40% lower today. Valuations of CARE also 40% higher compared to lows of FY12-13.

Effectively you can say CARE is trading about FY12-13 lows Rs 480/ share, During that time it used to do revenue of Rs 180 Cr, today it does about Rs 260 Cr. The Cash+investment on balance sheet back then was Rs 340 Cr today is Rs 460Cr.

Expenses Employee cost has tripled compared to Fy12-13 from Rs 50 Cr to Rs 150 Cr, Hence we are seeing about a 30% shrink in operating margins.

What was above all analysis about? I was just trying to compare it with the previous cycle lowest point valuations with today.

Is it trading as cheap as it was during the previous cycle low? Yes given where interest rates are it is, If you going to value it in terms of price to sales then its trading cheaper than it was before.

I am looking forward to earning bottoming out in the financial year. I still can’t foresee any earnings growth in the near future given how bad the state of the economy is.

Do I see rating business will become duo-poly (CRISIL / ICRA), no CARE will have its own significance as discussed earlier in the thread.

What happened between Q2 and Q3 for such a drastic drop in sales? I think fund raising activity has actually improved after easing of credit conditions. The market did not contract as such. This is clearly loss of marketshare here. I have always believed that it is a mediocre company propped up by regulatory hurdles in entering this biz. Once reputation got hit, it has stopped getting rating renewals and hence sales dropped. Has the company disclosed anything for such a drastic performance? Let’s see it could come out of this situation without losing marketshare permanently.

A. We need to find any company moved from CARE to CRISIL/ ICRA ? If yes how many.

B. Bond issuance and Corporate Debt raised YOY data ? To know its a cyclical slowdown or structural slow down for CARE.

I’ll check if i can dig some data out. I would highly appreciate to maintain the quality of discussion here we back our hypothesis by data / facts, that will add 10x more value for all of us.

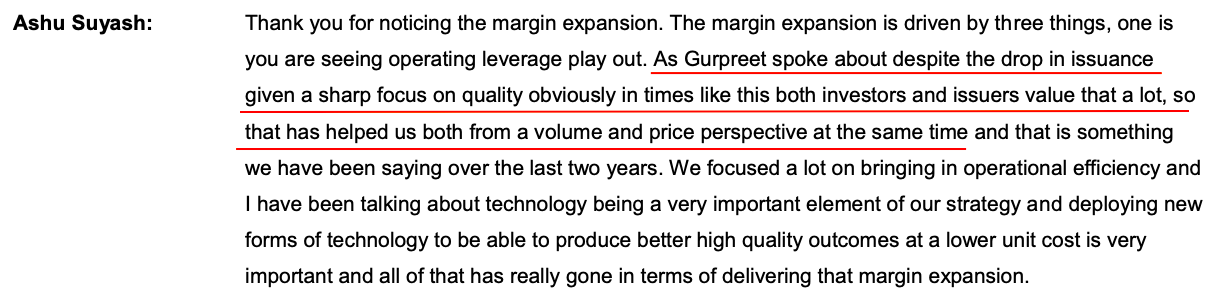

I don’t have hard data yet, but this insight from CRISIL conf call might help.

There is a drop in issuance and all incremental issuance went to CRISIL and they had more bargaining power as Customers want them.

unfortunately, CRISIL didn’t mention anywhere in the call they are gaining Customers from others ( They might be I don’t have data yet).

Again CRISIL, pointing out they are finding this market very favorable.

I think this information is very known to markets already as been playing out from 2 years, hence the price differential b/w the two.

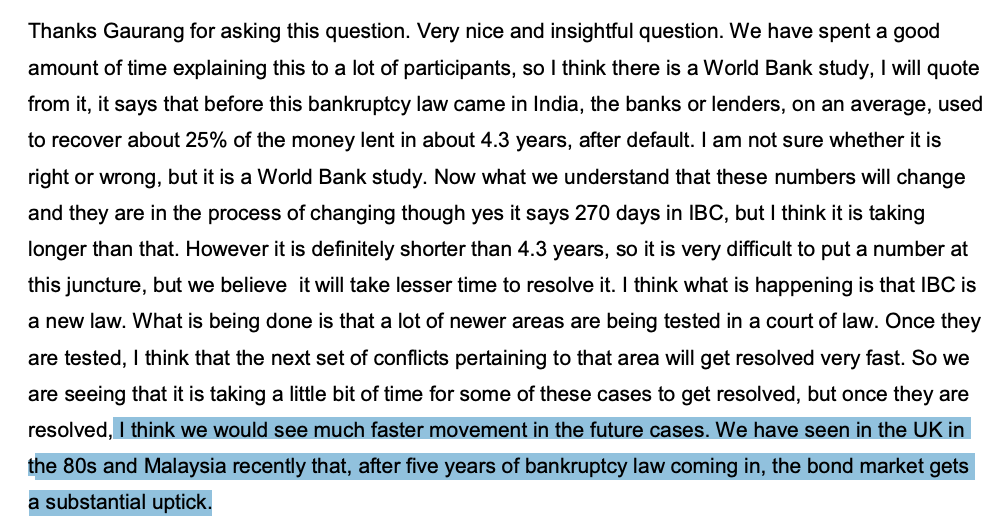

One thing which we should always keep in mind is in rest of world deepening of bond markets happened after 5 years of IBC, should happen in India too -

Also, We should not forget this what doesn’t kill you makes you stronger ( vaccines work on same principle as well), Even though this crisis killed IL&FS, DHFLs of the world but agencing which were rating them survived and this whole episode going to make everyone better including CARE.

because earlier they don’t have to work hard to make money they were not working hard, Now CARE had to and they must working hard ( anyone from Industry can validate my hypothesis if that is the case. )

While I agree on most of your points but Reputation impact is also on ICRA not only on CARE …

Icra has still put a decent result as against care. Net profit of care down 50%.

Lets not worry way too much into net profits, They can always fire employee increase the margins ( its foolish to do as in upcycle they will going to need more)

You should look at how much is the revenue decline ?

Its around 20 - 30%, but we will need to see if it stops here, There will be a day when operating leverage will also come into play.

Thanks for the views. Still for the sake of argument, even ICRAs top line decline is only 6-7% compared to big decline in CARE

ICRA’s revenue don’t only dependent on Ratings business while thats the case for CARE …just fyi

The operational data figures clearly shows that the short term ratings, bank loans and bonds rated have fallen by 50%

Yes, thats what i don’t like they blame Economy for their poor performance whereas if you read CRISIL their rating business is growing with margins improving as they say environment for quality rating never been this good.

Was holding care ratings since two years… Realised it was time to bite the bullet… Sold my holdings with 30 % loss…

Thesis for investment…

Oligopolistic sector.

Entry barriers present.

Company did not need a lot of capex…

Majority of the expenses were employees… Of the ratings agency revenue per employee was max for care ratings…

No equity dilution .

Good dividends were there…

And cash from operations converted to free cash flow was staggering…

I don’t think there are many companies which can do it better than care…( will be happy if anyone can let me know)…

Conversion rate was almost North of 90%( from 2013 to 2019 it converted 92% of cfo to fcf… I would stick my neck and say probably there is no company which can do a conversion like this…)

And the bond markets in India are still evolving…

Won’t go into the nitty gritties… As it’s already been discussed vastly in this thread.

WHAT MARKETS THOUGHT ME…

Quality without growth won’t fetch u anything…

Even though company was reasonably priced the purchase price becomes expensive when the profits shrink…

Credit rating industry is facing headwinds this is my thesis… Its always debatable…

But quoting Mr Basant Maheswari here " If the sector has tailwinds every tom dick and harry and me too sort of a company too will make profits…

If a sector is facing headwinds only the leaders make money… It is plainly evident here… Barring crisil — icra and care ( not tracking icra by the way) are struggling…also the whole industry as a whole is growing at 5-6%…

Care is going through a tough time… I feel still there is a lot of pain left…

I guess it will be too early to tell if care has lost market share…but if it does then where will the growth come in a sector that is growing at 5-6% is anbody’s guess…Risk reward not in favour…

Might lead to a lot of opportunity costs…

I feel investing in care should be a proper value buy…

I feel getting back in to these companies should be when they start showing first signs of growth…

Market fee paid for the lesson=30% ![]()

![]() …

…

tracking this counter and willing to get back if I get a throw away price…

In an interview heard Mr ramdeo agarwal telling in the long run ur returns will mirror ur company’s growth…

Discl= invested and continue to hold crisil… Divested from care… Not a sebi analyst…

CARE got show cause notice from SEBI, calling upon the reasons why the penalty amount should not be enhanced? Could not understand what is the intention behind this? Was not the case with SEBI finalized?

8[(3) The Board may call for and examine the record of any proceedings under this section and if it considers that the order passed by the adjudicating officer is erroneous to the extent it is not in the interests of the securities market, it may, after making or causing to be made such inquiry as it deems necessary, pass an order enhancing the quantum of penalty, if the circumstances of the case so justify:

Provided that no such order shall be passed unless the person concerned has been given an

opportunity of being heard in the matter:

Provided further that nothing contained in this sub-section shall be applicable after an expiry of a period of three months from the date of the order passed by the adjudicating officer or

disposal of the appeal under section 15T, whichever is earlier.

basically invoking the provisions to enhance the penalty. we dont know how much more is the proposal in the show cause notice.

Can someone throw light on what does this mean, how can it lead to lower revenue? How does issuances from financial sector impact CARE

All new issuance went to CRISIL & ICRA … thats why it leads to lower revenue.

ICRA revenue in Q3, 2020 has fallen from 95cr to 91cr, and PAT has also fallen from 30cr to 22 cr. in Q3, 2020. Q3 of Crisil is not out, but in H1, 2020; CRISIL has maintained revenue with a tad higher profit. CARE result, as compared to them is really bad.