I went through the RBI paper and here are my notes:

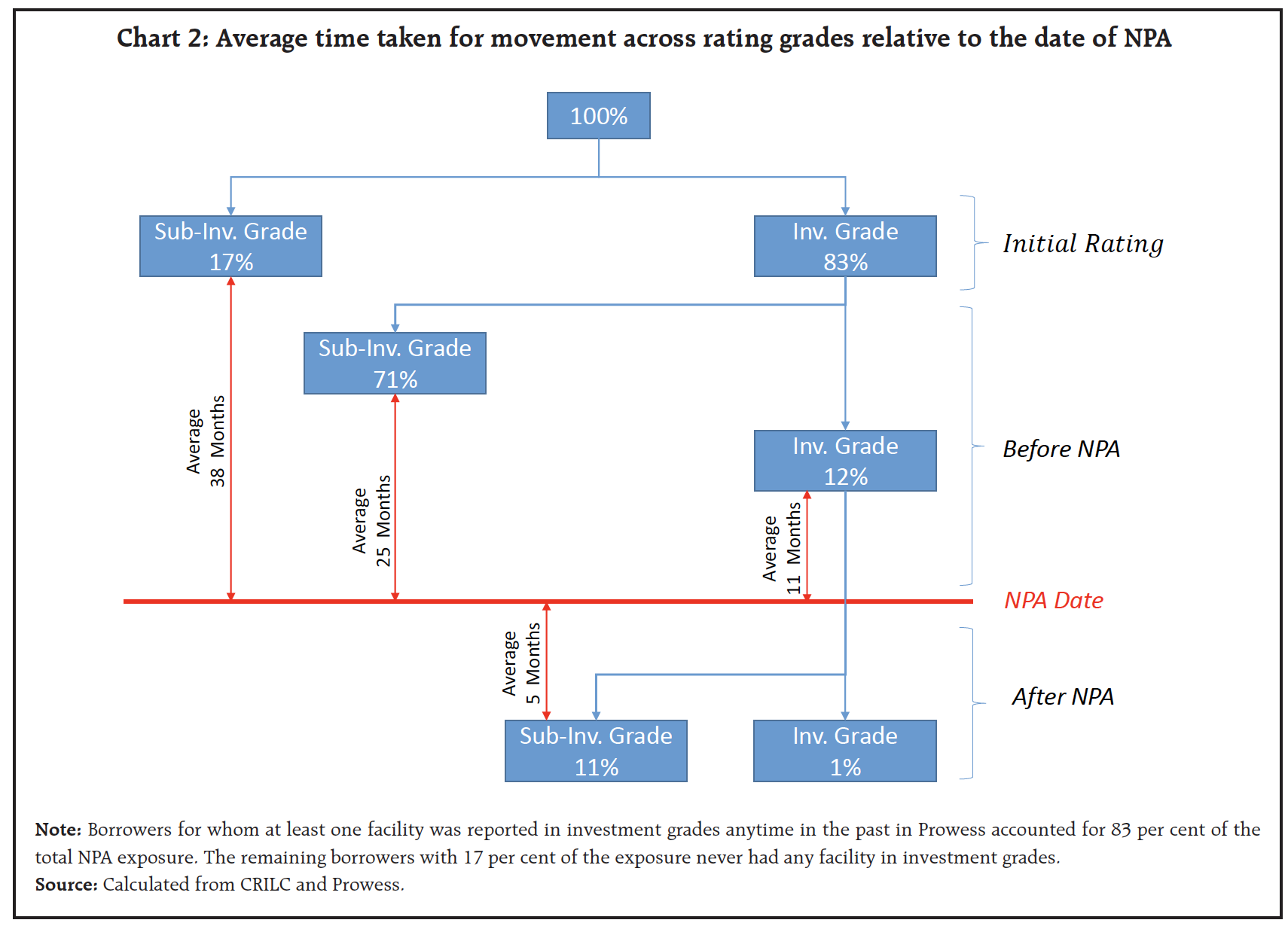

- 24% of NPAs came from borrowers carrying investment grade rating.

- 60% of bank borrowings (in value term) have been rated since 2014

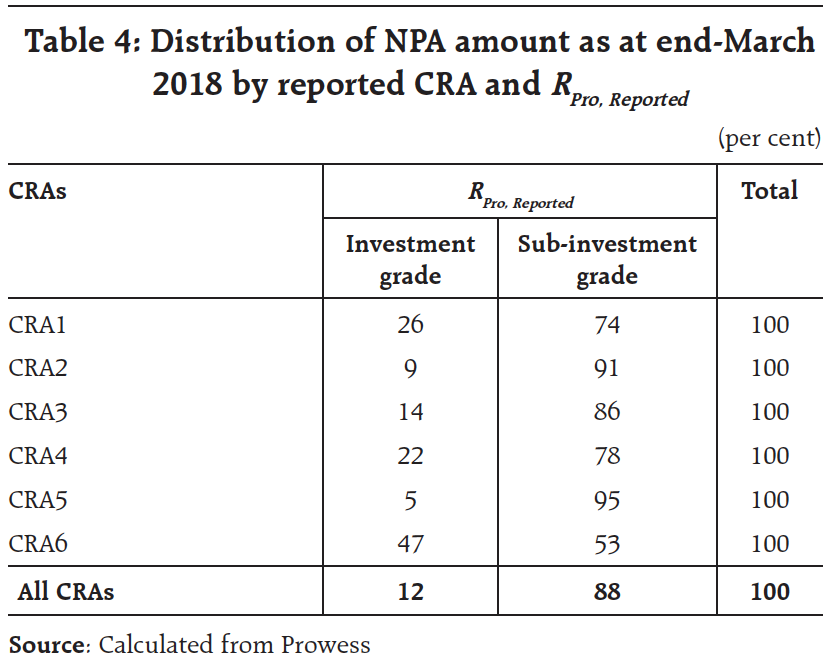

- 6 credit rating agencies were evaluated (names not disclosed) and they can separated into 2 categories (of 3 each)

- In the first category, <15% of NPAs were rated investment grade before they defaulted

- In the second category, >20% of NPAs were rated investment grade with the worse agency having 47% of defaulters having an investment grade rating (this guy did a horrific job!)

- 83% of borrowers who defaulted were at some point of time rated investment grade

In the picture below, who is CRA6?

This is the average timeline for movement across different rating grades to NPA.

@nirav565 Have I missed something?

https://m.rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=18704