Thank you for your view, it opened up many questions for me to think about.

On your point -

CRISIL has put out the explanation you might like reading if you have not read already - https://www.crisil.com/content/dam/crisil/our-analysis/reports/Ratings/documents/2019/march/the-AAA-ratings-debate-320-fahrenheit-not-equal-320-celsius.pdf

I would disagree with you that people lost 10s of thousands of dollars because of rating agencies alone. Everyone was greedy Entrepreneur, Investor, Lenders, builders and Rating agencies, Its a much deeper debate than it appears to be.

I would like to think about this unemotionally and in terms of numbers and logic. I take your point that trust is gone and no one wants to get rated by them - Let me slice & dice it numerically so that i can keep your emotions away from what objective reality going to be -

Given the regulation mentioned below lets think about where all the business will go?

- non-government provident funds, superannuation funds, gratuity funds can invest in bonds issued by public financial institutions, public sector companies/banks and private sector companies only when they are dual rated (i.e. rated by at least two different credit rating agencies).

- Further, such provident funds, superannuation funds, gratuity funds can invest in shares of only those companies whose debt is rated investment grade by at least two credit rating agencies on the date of such investments.

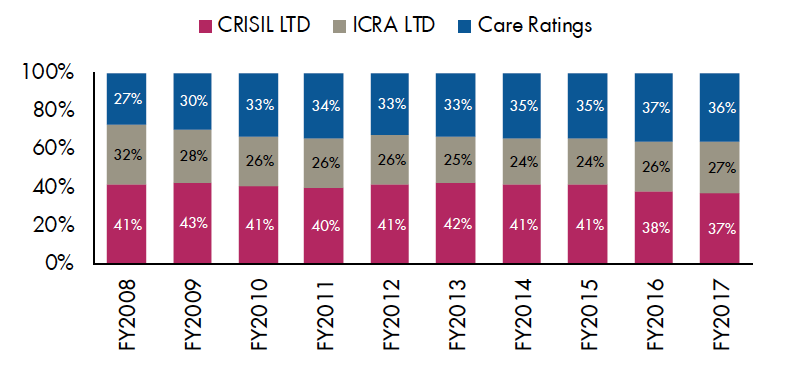

Below three rating agencies dominate the 97% of the market among them- Of that till Fy17 CARE was number 2.

So, I just find it hard to believe its all phony fake companies shopped rating market share.

Do you mean 36% of the overall rating revenue of India is phony and faked? I’ll go to website do what analysis you did but I think if you keep base in the prospective you will find it’s not all very bad. I still believe you are thinking more emotionally (bcoz people lost money) rather than bayesian. ( This homework I’ll do because whatever data I have I think Prof base is against you).

Now coming back to your original hypothesis - Nobody would want to get rated with CARE then by regulations all the ratings will be done by CRISIL & ICRA? Are they going to have a 50-50% market share? ICRA & CRISIL will be allowed to set rate whatever they want as companies have to pick two and they are the only two. I would argue markets won’t work that way and I would say why after the similar condition in U.S during 2007-09 financial crisis where everyone’s was greedy ( Not just rating agencies ) things did get back to normal.

All three rating agencies have a similar market share what they had pre-crisis. why because no one wants just 2 or 1 ( a very honest one) to dictate the prices.

and like you have the feeling all ratings were shopped, I feel the Cash (rating fee) has been delayed & there were some phony ones which are not significant.

A full-year picture will tell the truth.

I am with you on the NBFC point, There was a bubble everyone was greedy not just rating agencies. every tom, dick and harry were opening an NBFC investors were eager to put in equity, which is gone now. Unfortunately, I don’t have DATA to prove it’s indeed the major revenue contributor.

Thanks,

Amit