Hi pragnesh, I would urge you to please go through the full thread. All issues and their fundamental reasons will definitely become clear to you.

The TL;DR of the answer is a change in the client composition and bidding for more government contracts (and governments do not pay up front).

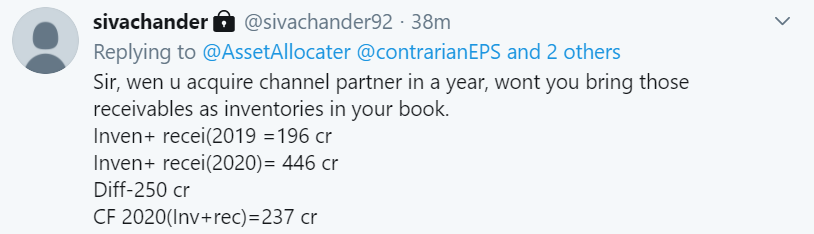

@Pragnesh Increasing receivables is due to acquisitions of channel partners and also due to foray into government contracts. This is within expected lines and will only improve from here. It is not comparable with the earlier negative working capital cycle

Two concerns I noticed in annual report is

- Lease rent for the land owned by promoters increased from 1 cr to 2 cr. Since promoters dont take salary instead they pay for their work by this lease rent (tax benefit is the reason i think).

- Auditor fees which was 10 lakh in 2017 , 15 lakh in 2019, now 30 lakh 2020.

@sahil_vi Regarding income and cashflow statement mismatch which we were talking during full year result.

I cant find the reason even after going through annual report.

Disc : invested heavily

4 Likes

Siva yes I noticed same things regarding the increase in rental and consultation fee to promoters. Also increase in audit fees but % wrt to turnover is not bad hence was not worried.

Regarding the government tenders I do not have any issue it makes perfect sense. My worry is with the channel partners. Technically the company could show high sales to channel partners without reconciliation of the cash flows, this could create an illusion of sales growth when actual cash generation is left lagging. I suppose we have to trust the management to not indulge in this type of fudging however…

I agree, this is definitely a concern. Since you had written to management and we did not hear back, this is definitely a cause for concern. At best it is shoddy accounting, at worst it might be some kind of a way to siphon off funds.

Accounting hygiene is definitely quite important. Given the lack of hygiene and management apathy for investors, I have decided to exit the company for now. There are many good companies which compete for capital.

Disc: Sold today, Full PF here.

1…Receivables increasing

2…rental increasing

3…auditor fees increasing

4…negative working capital cycle(in past)

I think,No pharma company having negative working capital cycle in industry

If we have good opportunities, why should we hold stock or do fresh investment in such company.

I had studied this post from beginning

Many members had raised questions

Even if this stock become multibagger,I will not have FOMO

My thoughts are

- crooked promoter wont be doing such a silly mistake in hiding their accounts.

- Being a listed company for more than 20 years, its very hard to hide things

- After listening to concall / explanation in ARs, management is very ambitous to become a major player in pharma (although not like laurus where they want to grow at break neck speed by taking debt). Since these ppl had bad experience with debt, they wont use debt in good way

- If I am a promoter, I will take my salary like this only (to avoid tax). Even youtubers (of course HNI) are registering their channel as company and avoiding tax

Ya but on proportionality it seem higher ( 15 lakh for 550 cr turnover and 30 lakh for 900 cr turnover )

Ya you are right. This happens with all companies.

LTTS : L & T is taking money out for the trademark usage. Lot of ESOPs

Laurus labs & polymed: promoter is taking large huge amount as salary

2 Likes

This might very well be true. At best this is shoddy accounting and makes our lives difficult as investors to understand what is really happening with the receivables and inventories. Also, when I have a company with a clear 3-5 year growth visibility available at similar valuation, better accounting, then as an investor, I prefer that.

I checked randomly, the corresponding figures of Alembic Pharmaceuticals ( Consolidated) for FY 20. Mismatch is there also.

As per BS

TR FY 20: 864.75 Cr, TR FY 19: 488.92 Cr, Diff: 375.83 Cr

As per Cash Flow Statement, Increase in TR: 358.26 Cr.

The cause may be change in Accounting Standards w.e.f 1st April 19, or something else. In AR FY 19 of Caplin, the corresponding figures are matching, however there is a minor difference in those of Alembic Pharma for FY 19: 37.45 Cr vs 35.61 Cr.

Persons well versed with Accounting System may be able to explain.

3 Likes

Take with a dollop of salt, any claims that high sustainable profitability can be achieved just by being in geographies that others are "too scared" to enter.

— Amit Mantri (@amitmantri) September 4, 2020

Indian cos will even compete in Antartica if it makes economic sense. If they don't it's because it doesn't make sense. https://t.co/JjagGF6oH9

2 Likes

This stock has been a wealth creator despite lot of investing people dislike it because of Cash Flow issues

It is more of a Africa dependent pharma company as of now.

Not going ahead like the good ones like Torrent, Alembic

The management also admits about challenges of working in LATAM countries. 90% of their business is with private sector. 10% only in Govt. tenders as lobbies are involved there. Even they have admitted that there are certain territories in LATAM, where business will be difficult for them.

Further , the company must be generating money, otherwise difficult to consistently pay dividends.

In Q1 FY 21 Concall, it mentioned that a company exports worth $ 150 million annually to LATAM. which is that Company and the customers are Govt. or Private?

Thanks

3 Likes

Q2 Results

2 Likes

New tie up with Canadian partner -

3 Likes

Ashish Kacholia holding some 1.08% shares as per Q3 shareholding pattern released y’day. Some smart investor action might be meaningful in near future. Obviously one need to do her own research before investment and can’t rely solely on these datapoints.

Disclosure: invested with 10% portfolio allocation

7 Likes

Thanks marmalade for the info

I have been holding CP for sometime now, fundamentally if one see 5 years comparative its been a good improvement at all level

1 Like

10 Likes

Q3 FY21 Highlights:

• Cash equivalents at 426 Cr vs 443cr of previous quarter end

• Inventory at 152 Cr vs 180 Cr of previous quarter end

• Receivable days stable at 93 vs 94 of previous quarter

• Margins are also stable comparing some pharmas in US are seeing some margin pressure

• US contribute 7% of sales and ROW is 93%

• No new capacity went live this quarter

• Currently processing an order for mexico market and betting big on mexico markets

• Company looking for acquisition of API facility in india which is under NCLT. If failed, company would directly constriction on its own. Decision will be taken soo and will not wait for long time, as land are already available.

• Caplin steriles - Signed new deal with Jamp pharmaceuticals for entry into Canada, 6 injectables to be filed and Plans underway for south Africa, Brazil and Australia

5 Likes

Is resignation of the Company secretory and Compliance officer is something to be concerned about? I understand people resign for numerous reasons.

1 Like