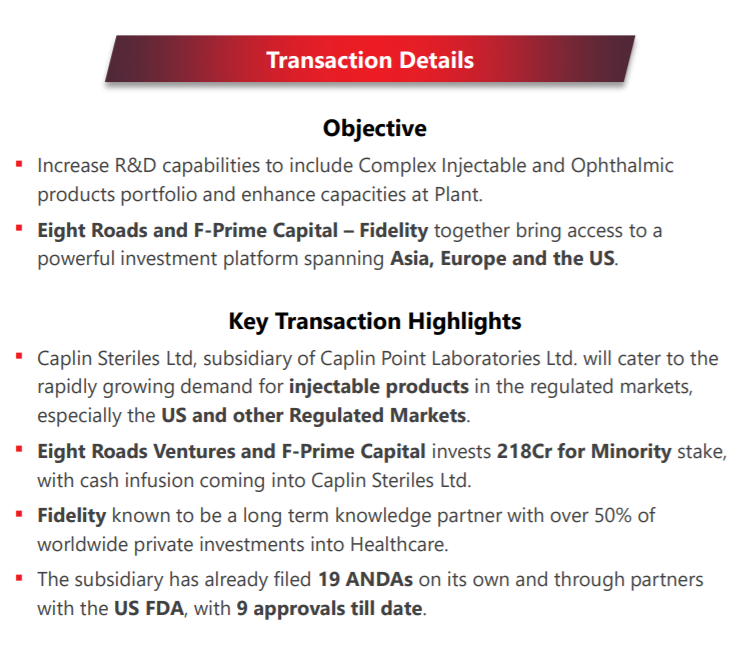

This is actually mentioned in the q4 slides page 31 of pdf they had posted as well but somehow all of us (including me) seem to have missed it. You can search for “QueTenX” in this pdf. Then, I google searched for “QueTenX Caplin” and found the website mentioned above. Since most of their revenues come from LatAm, the website is in Spanish.

Thanks for sharing. Is this publicly available? If so can you please share the public resource? If not, I suggest removing the screenshot since it is probably only meant for PMS clients.

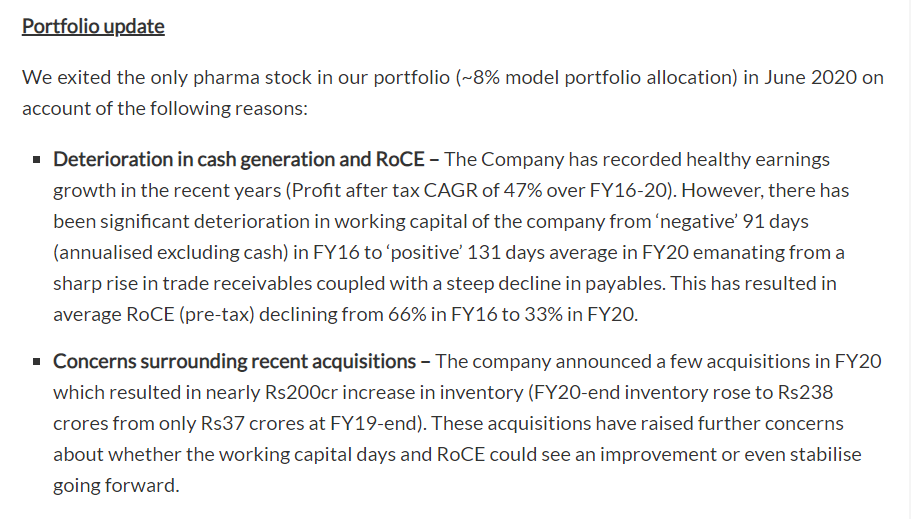

On the updates since, there is nothing new in this for me, if Marcellus exited the stock for these reasons, it makes me question their investment process. Because the signs of these things were visible even a year ago. Even on the acquisition front, I disagree with them but understand why they would want to exit.

This is still quite useful to know for people whos investment decision was based on Marcellus investing.

Thanks for sharing. Agree with @sahil_vi that these reasons have been fairly evident for sometime now. And the uncertainty around their US business and foray into other regulated markets will also be there for sometime. Marcellus does not like uncertainty and makes sense for them to exit.

My big takeaway from the fact that Marcellus decided to invest in Caplin in the first place is that the corporate governance and promotor integrity is robust, havig passed the famed Marcellus forensic evaluation. Assessing this I think is the single biggest challenge for retail investors, especialy for small cap companies. And this stays in tact.

Very valid reasons. I exited the stock in June exactly due to these reasons. I will renter if the stock price corrects to a lower level to increase my margin of safety. Still on my watchlist.

It points out caplins unique business model of catering to uncatered population often at great personal risk to the management. It talks about how their business model is slowly evolving now wherein US revenues are becoming larger part of the pie, and move from smaller latam to larger latam countries is also a big change for the business model. Instead of selling through importers they roped in small retailers and distributors which helped improve margins. Even for the larger latam countries caplins end game is go gain enough trust and build enough of a brand value that they can start working with direct retailers and distributors in those countries (these sections are not that powerful in these countries as compared to current countries where caplin operates such as Guatemala). The article talks about the fact that even for US expansion caplin is targetting the high margin injectibles where the shortage exists currently (favorable demand supply dynamics).

Some analysts commented that they understand caplins play wrt becoming an e2e player in these markets, but aquiring the distributors has added working capital days and putting pressure on roce.

The company is praised for creating the US injectibles facility based only on internal accruals and some equity injection . Initially the chairman was skeptical but his son convinced him about the partnership since they’d be sharing the risk as well. Even for the US injectibles they are targetting individual drugs where market size is small (< 50M$) and hence they would not face much competition from large generics companies.

At a very abstract I’d say this article is a great 15 minute summary of this thread.

I cant understand how these people consistently get numbers wrong… In Q4 it was cashflow statement…

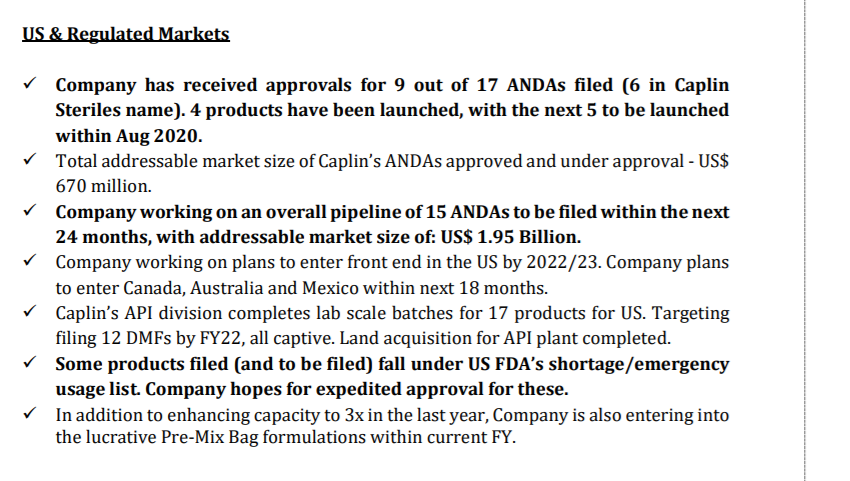

They told 9 out of 17 filed ANDA approved after Q4FY20

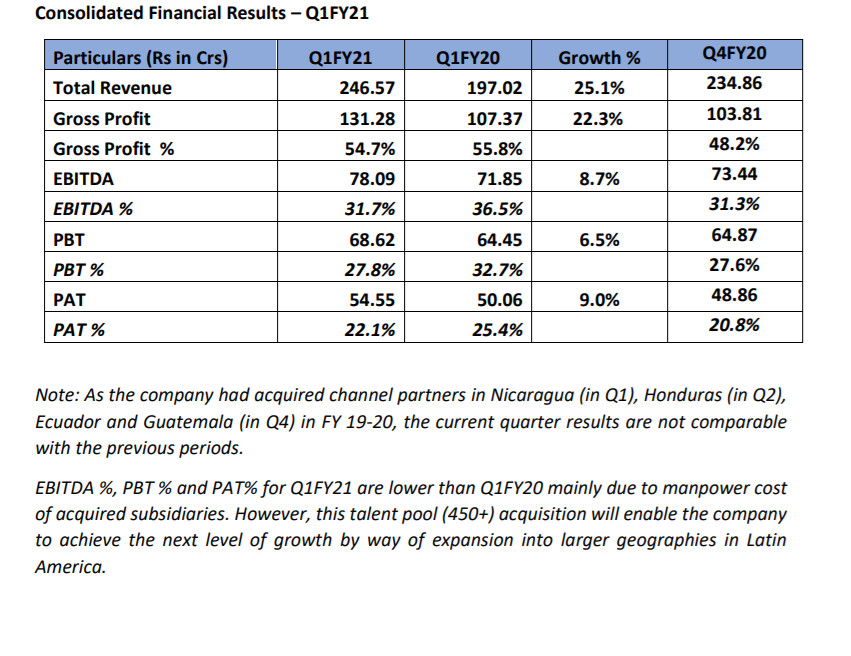

What do they mean by non-comparable… are they saying it double book entry… last year we sold to channel partner → we did acquisition and again we selling to customer so its not comparable…

Likewise, are these 450+ going to migrate from their origin nation to neighbouring countries…

I think they are saying totally 9 has been approved so far out of which 2 were approved within q1. Due to delay in q4 investor presentation maybe there is some overlap.

Regarding contraction of margins there is definitely some concern hopefully same will be cleared during con call today.

Conference Call Highlights

Dent in EBITDA due to higher employee costs (+ 450 personnel) due

to acquired subsidiaries in FY20– Nicaragua (in Q1), Honduras (in

Q2), Ecuador and Guatemala (in Q4)

Opex to stabilise, going ahead (ex-R&D costs) as channel partner

acquisition has been completed (Caplin has acquired majority

stake in ~90% of its channel partners in LatAm regions)

Forex gain - | 1.75 crore vs | 16.91 crore in Q4FY20

Cash flow from operation at ~| 100 crore

The company is looking for potential acquisition or greenfield

opportunities in Mexico

Receivable were at 93 days in Q1FY21. Likely to be maintained,

going ahead

500 products in LatAm

The company is embarking on development of 150 new

formulations specifically targeting three therapeutic areas – viz.

injectables used in hospitals, psychiatric and neuropsychiatric

products for brand marketing and anti-cancer products

Manufacturing of own API started in CMO at Vizag, for Latin

American markets, targeting reduction in costs to the extent of

10-15% against current procurement costs, for top 10 products

(top two provide 20% revenues, rest eight provide ~10-15%)

Plans for

API facility for oncology for regulated markets

OSD facility in Chennai

US sales were impacted in April due to lower manpower availability,

reduced productivity with revival seen towards end of Q1

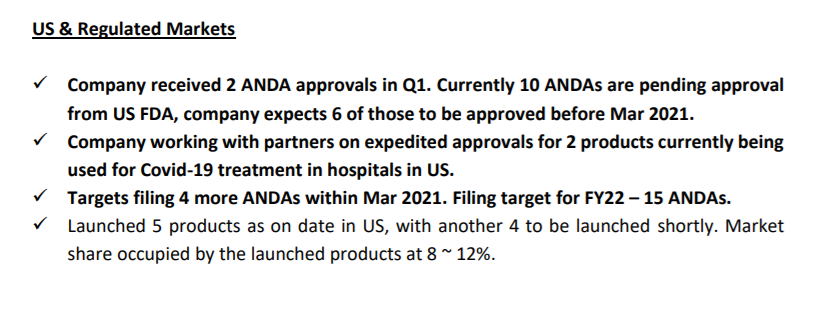

19 ANDAs filed till date with nine already approved

Launched five products as on date in US, with another four to be

launched shortly (one launched in July, another planned in

August). Launched products market share is around ~8-12%

Caplin received two ANDA approvals in Q1 and expects six

ANDA approvals by FY21. It is aiming to file four more ANDAs

in FY21. Filing target for FY22 – 15 ANDAs

US & regulated markets - Plans to launch US products in Canada and

US. Targets filing nine products in Canada and three in Australia

within the next 12 months

Working on two Covid related products – a) one product with a

partner close to launch and b) the other one filed by Caplin has

received 75% of queries within a month (normal 12-13 month

time-frame). Hence, it is likely to be fast tracked

Also, 70-75% profits to be retained with Caplin in the recent Xellia

distribution deal to launch five more products in US in the short to

medium term

Going ahead, the company is looking to focus on

Capacity expansion (vial lines 2 & 3)

Complex products vs simple injectables

Pre-mix formulation bags

Backward integration – construction to take a year for captive

consumption

Front end presence is US

In Q1, the company received orders for Azithromycin, Vitamin C,

Zinc, Iron, and HCQS

Q1 tender business mix went up to 15% vs. 10% amid Covid-19

US business to reach US$100 million in the next five years

Capex plans - ~| 20 crore for Chennai API plant for US + Vizag CMO

plans for greenfield/inorganic acquisition in Mexico for export to

LatAm markets

Mexico acquisition / greenfield could be in the range of ~| 100-

150 crore

Through this acquisition, the company will initially focus on

products not requiring BE/BA studies

Both capex and opex to be managed through internal accruals

Caplin Steriles to breakeven at ~| 125 crore. Cashflow breakeven

likely in FY22

Caplin plans to enter private business (not government tenders) in

larger LatAm markets such as Uruguay, Chile, Brazil, Mexico. The

company expects larger market LatAm market sales to grow to 2x

over four to five years

Was going through the annual report and some worrying trends with respect to receivables in the Balance sheet. After acquiring Channel Partners the trade receivable and inventory has shot up. Is it possible the company is showing high growth by ‘selling’ to distributors and then not fully disclosing actual sales? Is this something to be concerned by?

Increase in receivables was expected due to the acquisitions but even currently the receivables is at around 25% of sales which is normal for the industry. Also they have mentioned in the AR that they have been able to collect most of the receivables reported in March by June.

However,very surprising to see the trend from negative working capital cycle to increasing receivables,the trend we have not seen in any other company of pharma industry