Be cautious of all those companies posting super normal growth despite industry headwinds. It is very difficult for a small company in a particular sector to keep marching ahead with crazy numbers when all giants in the sector are falling apart.

Recent disclosure by caplin management to make topline of year x to be bottomline of year y are kinds of mgmt one should stay away from. This is just one red flag! If you do not understand the reasons for such abnormal growth, better do more research.

This have had a spectacular run but one should avoid confirmation bias. It proves fatal in stock investing.

yes , totally agree with you , thats why I sold some of my long term holdings after seeing huge increase in receivables. Will wait for few quarters to build convection and than take a position.

I think the growth momentum is valid. The generics market in South America has really boomed in the last 3-4 years. This has led to several large companies acquiring local names in Latin American countries to make in roads. A quick google search would confirm this. So as a company that has been in these markets for two decades has given Caplin the opportunity and the head start to ride this wave. I am reasonably convinced of that.

However, the story of how this company turned from a negative work capital firm to one with a large receivables account is the mystery I am finding hard to digest. I have read this whole thread and the only plausible explanation I can find is that the firm controls the importer in South America and transferred excess profit back as advance payment. Now why did this trend reverse - possibly for two reasons a) Price is the only lever of competition on generics. So while the competition increased in South America, prices went down and the only way to hold on to existing customer base would have been to roll our flexible payment terms. If this hypothesis is true, then there is no going back to the good old days. b) The complexion of revenue could have changed and I have not checked this. If this has, then this would be the new normal.

Either way, I find the lack of transparency will keep a risk averse investor like myself away.

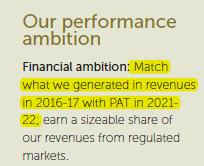

Hi Mridul, the ambition of making the topline to bottomline was earlier mentioned in their 2016 annual report. If we look at the numbers, they are not very far from achieving it.

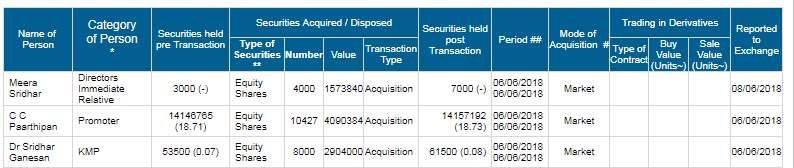

Promoters did some shopping in recent correction below 400 rs. It increases little confidence when their were doubts of high receivables and growth slowing down . Would like to know more what others think about it.

Not sure if this is just a typo or they are revising their guidance lower. Moreover, 2015-16 had only 9 months as they switched from June to March year end so reported revenue of 245 Cr for the FY16 was only for 9 months. PAT for FY 18 was 145 Cr so as per the most recent guidance, PAT will grow at a CAGR of 13% much lower than historical rate of 35% and their own guidance of 20-25% growth rate.

Result rating may be considered as neutral. However, as the Company consolidating its business in Latin America, it can be considered as long term bet? Any Comment on this.

I have spoken to Caplin. I think their announcements are pretty confusing.

To further clarify, they are setting up these subsidiaries with investments - so this is not going to be an expense on the P&L. They plan to buy distributors and distributors mostly hold caplin stock. So in effect its like re-purchasing some stock and end customer relationships.

They will only acquire distributors if prices are reasonable. Some ditributors are asking too high of a price which Caplin will not pay.

With respect to China, this JV gives them an opportunity to sell into Chinese market. This is a new opportunity and is not factored into their projections.

Based on current plans they expect to do net profit of 300+cr by 2021 (without including China)

Clearly the company is diversifying and want to increase profit margins. Higher profits can only come if more capital is invested as most of the low hanging fruits have already been taken. So return on capital ratios will decrease but you get stability of profits.

however their capital ratios compared to other pharma companies still look reasonable. Overall it does seem like the company is taking on new businesses and projects which would be good if its successful.

As these two announcements are deviation from Caplin norman philosophy of growth, why management is not keeping investors con call or giving more info through TV interviews?

Proper disclosure at right time will enhance investors’ confidence instead management force to give justification after sharp correction in stock price (as happened in recent past)

High PE was based on high ROCE, negative working capital cycle and high ROE model of Caplin. As now model has changed with high receivables and more investment reducing ROE and ROCE, Caplin PE will de-rated. Hence, investors need to keep return expectations accordingly

Also, wondering how Caplin going to have high profitable business in China compared to Latin America. If u see the Jointown financial its net margin single low digit inspite of biggest network the company has in China https://quotes.wsj.com/CN/600998/financials

I agree. We should not expect high return on capital going forward. It will be more in line with other pharma companies. When I spoke to management, they also did not seem to care too much about return on capital but more interested in topline growth and profit margins.

Jointown is a distributor and distributors will work on small profit margins especially in a competitive market like China. Caplin’s profit margin will not be affected as they being a manufacturer operate on higher profit margins.

Essentially Jointown will give more volumes to Caplin.

Based on past business philosophy : Caplin was buying more from China and selling in Latin America and earning huge profit. As Chinese markets is highly competitive, how can Caplin sell through Jointown in China with good profit?

Caplin can earn excess profit than other pharma only if it buy medicine from China and selling in Latin America , not by producing in their own plant.

Did u get any thing on this aspect from management? Please talk with Mgt. and post your feedback here.

As I came to know that now local distributors in Latin America buying directly from China and increasing competition for Caplin; which might be one reason of increasing receivables in recent past.

Not sure if its that simple. There’s a huge amount of work involved with the development and registration (IP) for Pharma products in these regions. I dont think any regular distribution company can simply buy product from China and sell in Latin America. The entry barriers are high these days, which is why not many Indian companies are successful there, except maybe Torrent, DRL and Lupin.

On China - the space seems very hot right now, with an Indian delegation recently visiting China to sign an MoU with their MoH (I think), so will be interesting to see what comes out of this. My personal opinion is China is a complex space and would be good to have a strong partner if Caplin wants to enter their domestic market.

Nearly half of Caplin’s revenue comes from outsourced meds. It has contracted with Chinese manufacturers for cephalosporin and penicillin, which it then sells in Latin America. “We’ll never be able to compete with the Chinese in the unregulated markets,” says 31-year-old Vivek, who is the chief operating officer. “But the top Chinese manufacturers have massive capacities. So we tap into their spare capacity.”

would have liked to see as to why Caplin is under scanner?? Sudden increase in recievables? Doubts over Latin America business and its solidity. On data sheet,past ten years performance is flawless but something is jarring.Does the market knows something that we don’t?

Their annual report says “The entire Trade Receivables are good and have since been realized.”

The have a large factory that has been funded from accruals without debt or equity. This factory recently got usfda approved. The management is keen to put this asset to use in the near future. As well as the last update of Chinese collaboration

I think Caplin is available at a good price at the moment