I looked at Caplin over the weekend since it looked cheap.

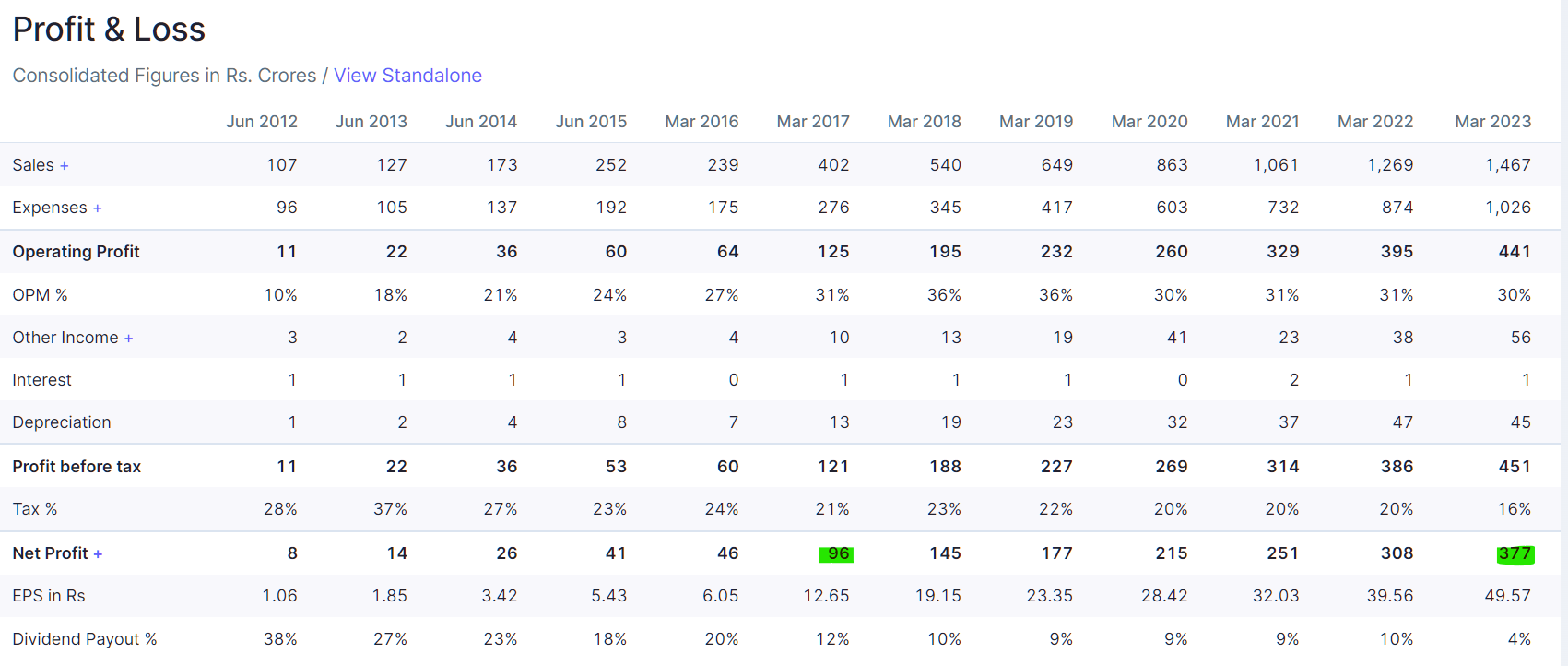

PAT has gone up 4x while price has been stagnant in the same time of 6 yrs

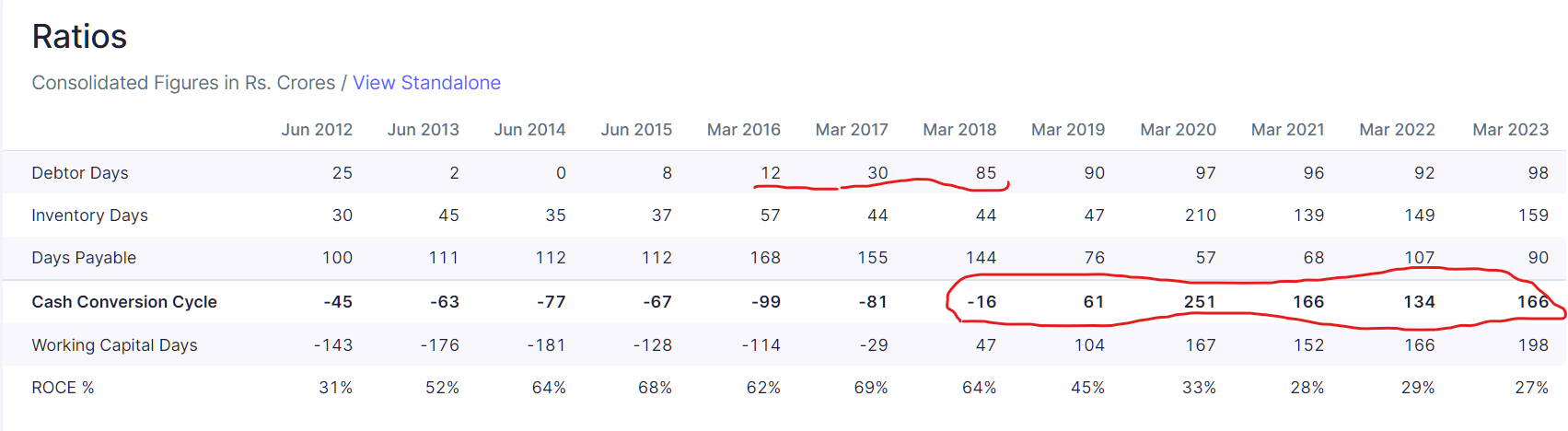

What stood out immediately in early checks was this. Why has the cash conversion become so worse since FY17 or so?

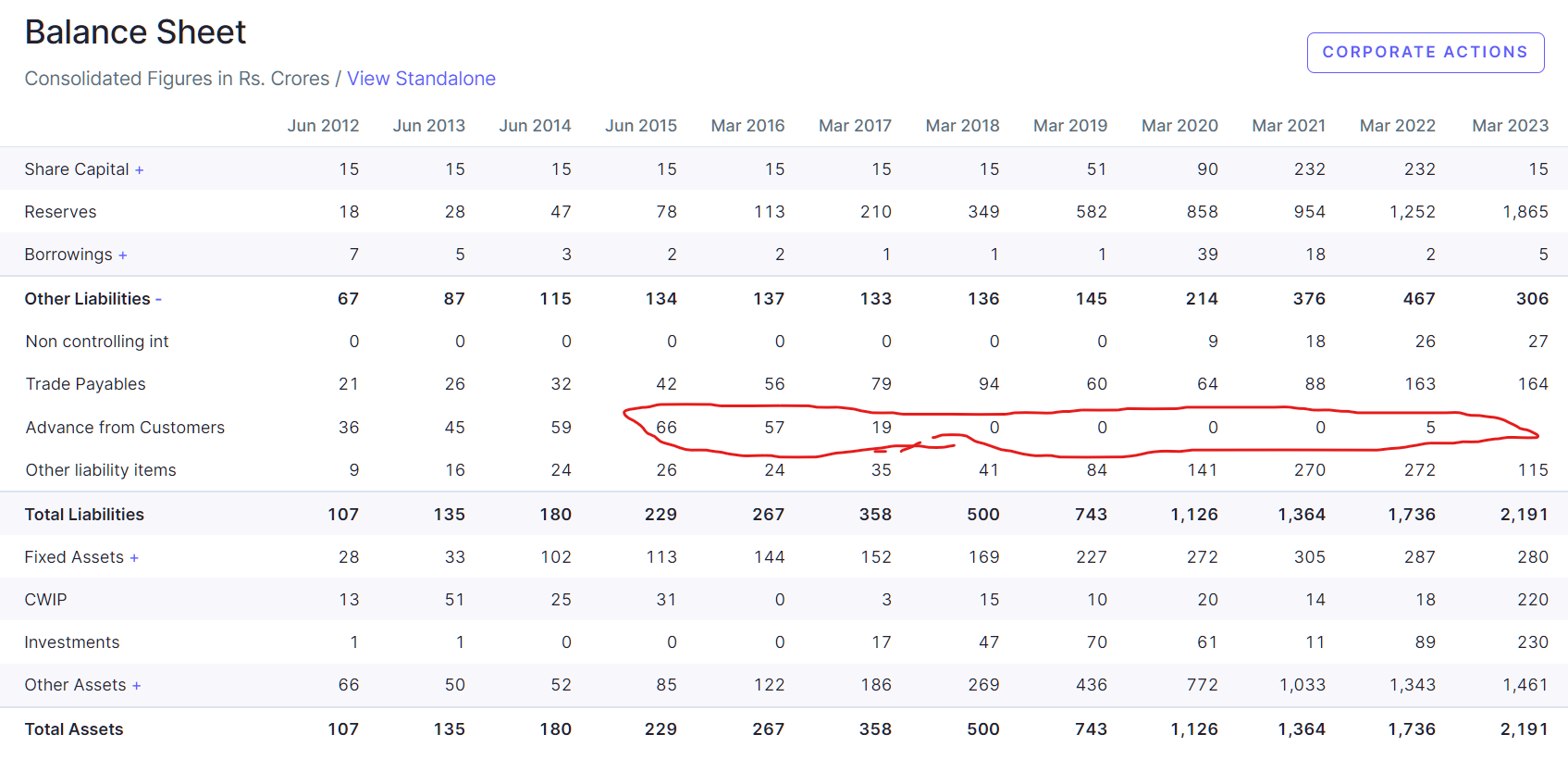

So what’s ailing the price is what I set to find out and ended up reading almost this entire thread. My take is that the company was under-reporting its profits until FY16-17 or so. While it was supplying to its “partners” and booking revenues at those sales numbers, the company also made profits in its distribution along with its partners but this was under-reported in profits but reported as “Advanced from customers”. This has since then become 0. The business seems to have even used these “Advances” to fund capex in the past.

This artificially showed much higher RoCE than what the company was making (~65%), while also depressing the tax it was paying. What should have been assets of the company (cash post tax) was ending up as liabilities (Advances from customers). This should have been outright fraud which is probably why the company refused to open its mouth back in 2011-12 period when VP-ers grilled them how they could get advances on generics. The company was infact probably telling the truth that their strength was avoiding the middleman but hiding the fact on the Advances.

Taking over its partner’s distribution business has brought the inventory and receivables of the distribution business into the company’s books and has suppresed the ratios. The current RoCE of around 25-30% is probably where the actual returns of the business are and is still admirable (Maybe will trend evenlower as US business grows).

So the business has grown from strength to strength in the last 10 yrs and its 150x in returns since the early discussions on the company. While the business itself is probably legit but the poor governance is continuing to haunt the company.

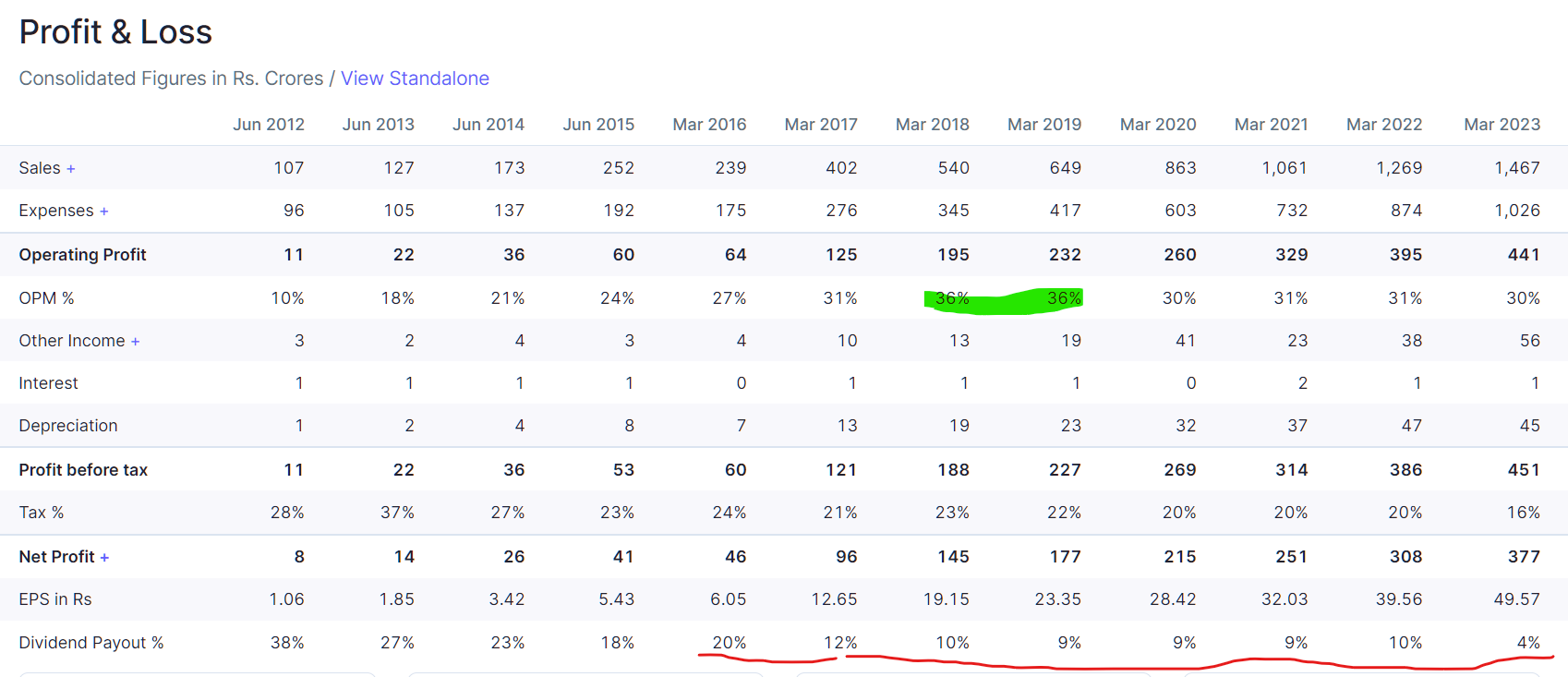

The reason why there are no returns is probably because though there is 4x growth in profits, this is probably just mostly restating of numbers. The growth in sales is probably due to the price the distributor is selling being booked instead of what Caplin was selling to its partner. The growth in margins (in FY1 8 and FY19) towards 37% also aligns with this theory (Advances becoming profits) - though the company seems to have said its due to branded business and so on and cash conversion worsening due to govt. business etc. - All this is probably untrue.

Also, notice how the payouts have reduced from 20-25% levels to all time low 4%. How will this increase the confidence on shareholders that the cash equivalents (770 Cr) is indeed real and shareholders will actually get it?

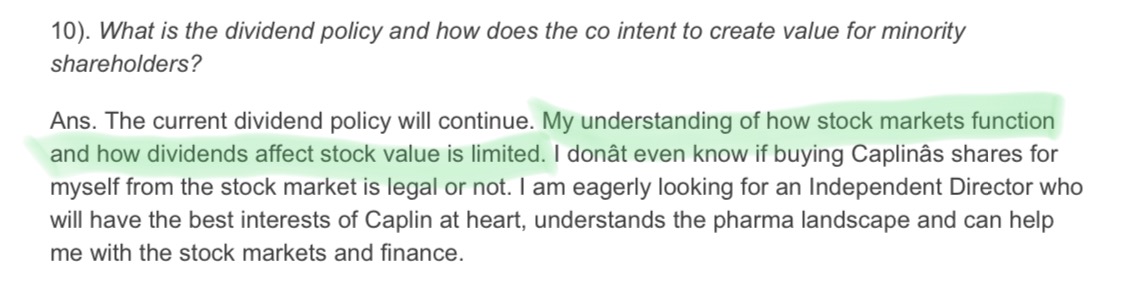

I found this interesting in the 2012 interview by VP-ers.

I don’t think the management has learnt how dividends affect stock value yet. Paying 15 Cr dividend when you have 770 Cr cash - even with a capex outlay of 350 Cr over the next 2 yrs, is poor optics. They should have at the very least paid a 40 Cr dividend and maintained the 10% payout rate. I will be interested here if the payout rates go up above 20% levels and the company puts out a dividend policy. That has the potential to re-rate this stock and make returns for shareholders than any growth in US business can.

Disc: No positions