Isn’t the 6th point in the AGM notice shared yesterday that I have shared as screenshot say they intend to increase? Am I missing something?

Yes, they are increasing the authorised capital. This needs to be done first before they can issue further shares. At this point (where auth. capital is being increased) no shares will be issued. It is a procedural thing.

In layman’s terms - they are seeking permission to cut the pizza which currently has 4 slices such that it will have 6 slices. How and when the new 2 slices will be shared isn’t mentioned in that clause. Once permission is received from shareholders, the company can use it to raise cash by way of QIP, Pref allotment, rights issue etc. These new slices (shares) will not be given out for free to existing shareholders (Bonus issue) as this resolution most likely has been brought to enhance the strength of the Balance Sheet by raising equity investment so that they can deliver the Orderbook and also improve their Credit Rating

2 Likes

Has Capacite infra won any project today?

The stock has risen 6% suddenly anyone have any news?

No but the directors have given a comfort letter for unsecured loans to the company. Liquidity is more important than orders for the company

2 Likes

Results seems to be in line as suggested in last concall. I was expecting nothing but a flat quarter, though I expected them to have some positive commentary on their NFB limits. But I know things at sanctioning level works little slow. Hopefully they would deliver that 2100 revenue and 18 per margin by the end of the year

1 Like

All impatient souls taken out today. Is there any updates on concall. Did promoters gave any byte to TV channels

4% dilution with conversion of warrants by Rohit and Sakshi last week. Some additional cash infusion in the process, and the price has remained flat, and in fact has gone up 3-4% since last week. Good signs.

1 Like

Their order book says Majority is

1.Public Order book

2. High Rise Buildings.

Can someone give an example of Public High Rise Projects?

Are they all Mhada projects?

Please refer the presentations. They have highlighted all the projects…including oberai and raymond and few godrej

Anyone invested and tracking this company closely?

Company posted decent Q4 results with sales increasing from 62 to 87Cr and profit 20 to 30 Cr. Company has provided good guidance for next 2 years growth (30%)

1 Like

company has a standalone order book of roughly Rs 8,800 crore in September with 70% of the projects from the government and the remaining 30% from the private sector

Managmnet interview

2 Likes

Hi All,

Seems like not much traction here recently. I think many contractor businesses have been doing well & should keep doing well over the next many quarters. Capacite has good reputation & has been gaining orders from multiple states & real estate developers. Revenue to order book is strong >4 times & has been executing well since over a year now. Good capex support from both govt & private, good order book to revenue ratio maintenance & reasonable valuations have been supporting the stock rallies so far. Of course it’s a highly cyclical & risky space but the management seems very competent, hungry & transparent. Which makes a good cocktail with infra upswing.

Disc: Holding

5 Likes

𝗖𝗮𝗽𝗮𝗰𝗶𝘁𝗲 𝗜𝗻𝗳𝗿𝗮 𝗟𝗶𝗺𝗶𝘁𝗲𝗱 – Company is a Tier 1 EPC contractor with specialization in high rises projects & urban infrastructure.

𝗖𝘂𝗿𝗿𝗲𝗻𝘁 𝗺𝗮𝗿𝗸𝗲𝘁 𝗰𝗮𝗽𝗶𝘁𝗮𝗹𝗶𝘀𝗮𝘁𝗶𝗼𝗻 – ₹𝟯,𝟭𝟯𝟬 𝗖𝗿𝘀

𝗦𝗼𝗺𝗲 𝗸𝗲𝘆 𝗶𝗻𝘀𝗶𝗴𝗵𝘁𝘀 𝗳𝗿𝗼𝗺 𝗹𝗮𝘁𝗲𝘀𝘁 𝗺𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗰𝗼𝗻𝗰𝗮𝗹𝗹 & 𝗽𝗿𝗲𝘀𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻 𝗳𝗼𝗿 𝗤𝟮𝗙𝗬𝟮𝟱-

- Current order book is approximately ₹9,000 crs + (4.5 times FY24 Revenue ), additionally looking at order inflow of ₹3,000 crs for FY25, excluding MHADA order which is expected to be another ₹3,000 crs

- Management expects to maintain margins & reduce working capital days, along with increasing order book at 20-25% growth rate annually

- Company has signed new clients including likes of Signature Global during FY25

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗵𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀:

- H1FY25 Revenue ₹1,088 Crs with H2 being seasonally better for industry & company

- Expected FY25 Revenue at current run rate should be ₹2,200 Crs

- H1FY25 operating margins are 18.5% compared to 17% in FY24

- Expected operating profits for FY25 should be ₹400 Crs

- TTM Earnings per share is ₹21.5, implying TTM P/E of 17 times

- Annualized Earnings per share for FY25 should be ₹23, implying FY25 forward P/E 16 times

Source: SBI securities report & company published data & interviews with exchanges

5 Likes

Recently started tracking this company. It says to also have construction work for data centers which is nice to have considering the opportunity. Says to have a balance between private and government projects in the future.

And with government supporting if not boosting the capex in Infra, this seems like a good bet for now.

Disc - Invested today

-

Management reiterated their guidance of 25% revenue growth for FY25 and are confident they will achieve this, aiming for at least ₹700 crores of execution in Q4 FY25.

-

A minimum of 25% growth for FY26, potentially reaching 30-32%. This growth is underpinned by a strong order book and expected faster execution on newer projects.

-

The company has already secured new projects worth ₹2579 crores YTD. They are confident of exceeding their guided order book addition for FY25, expecting to surpass ₹3000 crores easily and even potentially reach ₹4000 crores with Maada project additions. Next financial year, they are aiming for ₹4000 crores of new order inflow.

-

Significant revenue contribution is expected from projects with SITCO (aiming for ₹85 crore/month billing in FY26), Maada (approx. ₹400 crore for FY26), Signature Global (approx. ₹240 crore for FY26), and the new NBCC project.

-

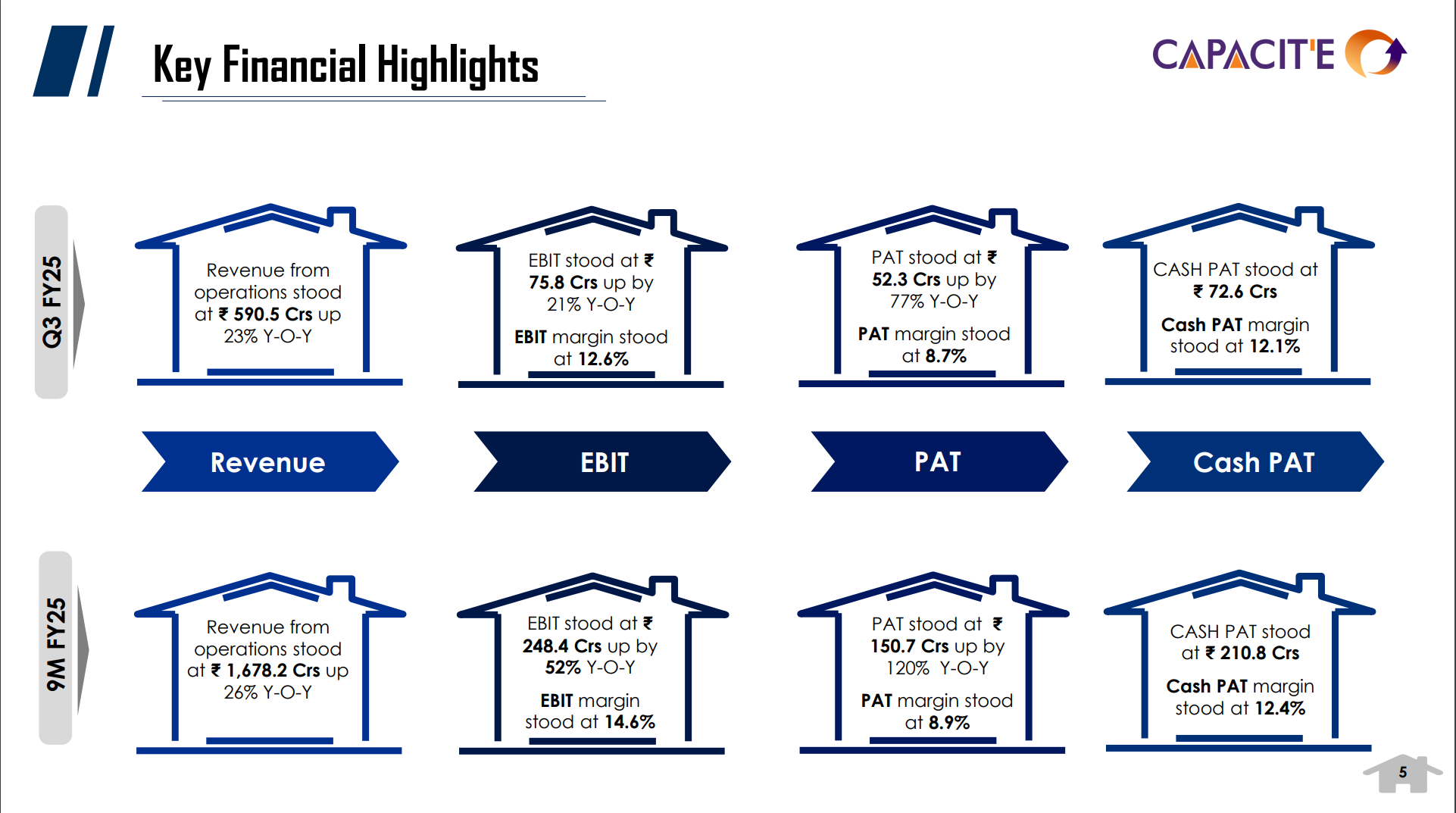

Margins Were Down in Q3 FY25:

-

A one-time expense of ₹12 crores related to differential GST rates for a public sector contract (Bhagwati project of MCGM).

-

This expense pertains to the increase in GST rate from 12% to 18% which has not yet been reimbursed by the client.

-

While the company believes the client is legally obligated to bear this differential GST cost and industry representations support this view, they booked the expense as a matter of prudence due to a lack of written documentation and to be conservative

-

Excluding this one-time expense, the EBITDA margin for Q3 FY25 would have been approximately 18.7%, in line with previous periods.

-

Very tempted to buy it give the valuations and strong management commentary.

2 Likes