See, the promoter who sold it is a PE fund, they have to book profits, typically after a 7 year time frame, I don’t this is a cause for concern, as the growth trajectory is still there.

Additionally, the management immediately addressed this by hosting Investor meets and clarifying with Investors why there was such a big fall.

Can we ignore the Investment of Kotak in KFin tech, a competitor of CAMS. What is the impact if Kotak MF Account moves from CAMS to KFin?. This is one issue I am concerned which is witholding me from increasing my allocation to CAMS.

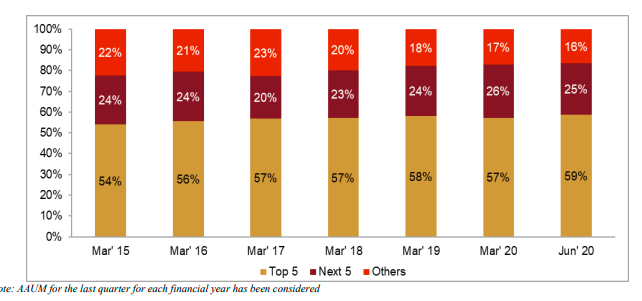

Cams has 70% total MF market share , 70% of revenue comes from top five clients.

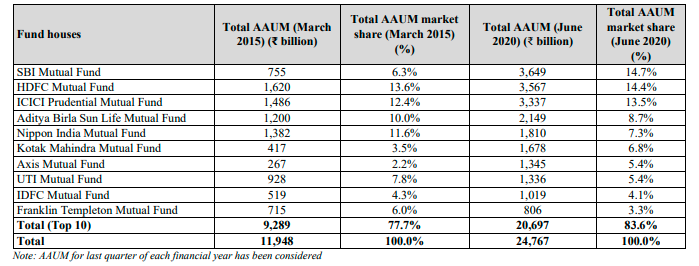

As of the June quarter of 2020, SBI Mutual Fund is the largest AMC in terms of its AUMs. It is followed by HDFC Mutual Fund, ICICI Prudential Mutual Fund, Aditya Birla Sun Life Mutual Fund and Nippon India Mutual Fund which form the top five AMCs. The next five AMCs are Kotak Mahindra Mutual Fund, Axis Mutual Fund, UTI Mutual Fund, IDFC Mutual Fund

and Franklin Templeton Mutual Fund which complete the top 10 AMCs.

Assuming that Kotak moves away . it would reduce 6.8 % market share for CAMS/

I believe Equity & MF penetration in India Is very low when compared with USA. In our country most investors, even many Company’s/ SME’s / Trusts/ HNI’s choose MF route for their investment needs.

And what about these New Age AMC’s “UPSTART’s” which are coming up apart from other new players aiming to start AMC business like Bajaj Finserve, Samco, Alchemy, Helio capital and many others who are planning to enter the business …These new players will help create new investors and expand the overall market …, Cams being the market leader is likely to gain out of the expanded market !

You may be right from the stock performance point of view during last 6 months. But this is mainly due to stake sale of two major stake holders - IIFL & Great terrain.

In any case, in my view the long term story still remains in tact and for a long term investor it is going to be classic case of consistent compounder …given the low level of MF penetration currently …

Short term volatility do happen in most of the stocks due to some reason or other…so a long term investor does not change his view. He is always prepared for a short term volatility as long is one is confident about the story that would play out in future.

I will change my view if there is a drastic policy change in which RTA’s would be dismantled and the respective AMC’s will act like RTA or there is a serious corporate governance issue in the company or the company reports poor growth or negative growth for several quarters.

Discl: It is not an investment advice. Please do your own assessment before investing.

So even though both of them have almost the same distribution of AMCs (CAMS - 13, Kfin -12), since CAMS has bigger fund houses it manages ~66% AUM transactions while Kfin manages ~30%AUM, based on QAAUM numbers.

Actually, we have to correlate revenue with number of transactions processed to judge pricing power. If that figure is not available, one can use number of investor folios. AUM goes up due to price appreciation also, which brings no revenue to CAMS. So this may present a misleading picture.

Ok, so 80% of the revenue is linked to AUM and the inverse relationship is in-built into the pricing structure of CAMS. It’s a feature, not a bug in that case ! Thanks for the clarification !

Pricing power is a question mark definitely? But not the run-way. India’s MF industry size if just 500B USD, while it is 24 Trillion in US, 5 Tn in Australia, 3 Tn in Germany etc. Also, this is precisely the reason why CAMS has explicitly stated that it is repivoting itself to be a full-fledged Technology Solutions provider to the MF industry, and not just RTA

AUM mix vital for earnings, as equity and hybrid schemes fetch 0.06% of AUM as fees, while debt and liquid funds yield a third of it, at 0.02% while ETFs yield much lower. Overall, RTAs earn 0.035% to 0.04% of AUM as fees, which has reduced from 0.045% to 0.05% 5 years ago, but compensated by rising MF industry AUM. In FY20, though, pricing pressure was witnessed post SEBI’s reduction in total expense ratio (TER) that mutual funds were allowed to charge to the investors.

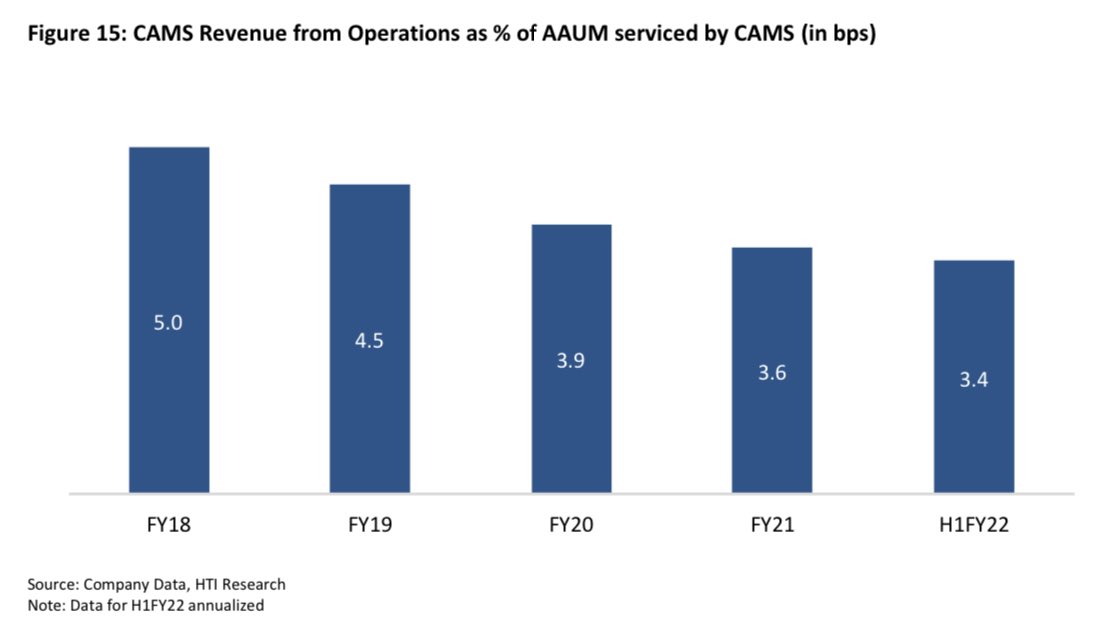

From FY17 to FY20, company’s revenue grew at 14% CAGR to Rs. 700 crore, mirroring MF industry AAUM growth of 14% during this period. Replicating the 15% drop in AAUM of equity oriented schemes, Q1FY21 revenue declined 15% YoY to Rs. 149 crore, resulting in 11% YoY drop in both EBITDA and PBT to Rs. 64 crore and Rs. 53 crore respectively. This highlights volatility in quarterly financials based on broader market conditions, despite secular growth story of MF industry remaining intact.

While CAMS has sound fundamentals and is a play on growing financialisation of domestic savings via the MF route, it is important to understand that company’s growth is primarily dependent on external factors, beyond its control, such as MF AAUM growth (expected to be in low-to-mid teens). FY20 demonstrated limited pricing power in company’s hands, despite duopoly, due to again external factors such as reduction in mutual fund scheme’s TER (total expense ratio). Going forward, growth will be steady-state and not extraordinary, as scope for market share gain is also limited.

Source : IPO note - SP tulsian

Still it’s a better Play on MF , as other listed AMCs are loosing market share and competition intensity is increasing .

Yes, thats right. If anyone wants to play on Mutual Fund Industry, its better to play via CAMS (and/or KFintech when its listed) rather than individual AMCs. Thats because the MF industry is expected to get more competitive with more and more Fintechs (like Paytm, Zerodha etc) and International Players all gearing up to launch their own funds - the pie may be split among many more

Thanks for the clarification !

Thanks for the clarification !