If the QoQ performance and the YoY performance have been good for CAMS , is there anything in the guidance not good that is driving the stock down lately?

6 Likes

I just think its correcting to a more reasonable valuation. With my (very) limited ability, I see positives for this company in the longer term

Disc: Actively tracking

3 Likes

4 Likes

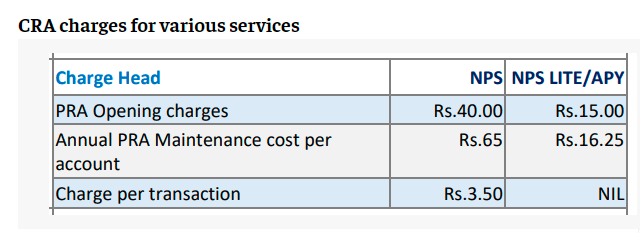

Addtional revenue from this

6 Likes

2 Likes

To all those who follow CAMS from a long time, Is there anything worrisome going on with the fundamentals of the company that’s being predicted by the market?

How do you think the IPO of the competitor Kfintech might affect CAMS?

Requesting answers.

There’s a nice IPO review for CAMS by CA Rachana Ranade that explains it’s business and also compares with kfintech.

3 Likes

I had a small position some time back but have exited it now. I don’t think there is anything wrong with the business. It is a stable business but by its very nature it cannot grow too fast. Moreover, growth is dependent on external factors over which the management has no control. The various new business lines it has ventured into will take time to fructify, and their real earning potential is not known, it may not all that great. A lot of stock price gains last year came from PE expansion and a one-time bump up due to Franklin Templeton. Otherwise, generic earnings growth will be slow – at best single digits only.

Last year, the so-called “platform stocks” were all the rage. Now that craze seems to have died down. So the PE is correcting back to more normalized levels. These things keep happening in the markets all the time. There may also be some hangover of the impending Great Terrain exit.

If one of the new business lines makes it big, the stock will fire again. Until then one will have to be patient.

9 Likes

I have a counter argument here. Mutual fund(MF) participation in India is low as compared to US or China. So, there is a lot of headroom to grow here & CAMS being the market leader (monopolistic company, in fact) can benefit a lot from this opportunity.

But, I agree to your point. It is a moderately growing business and the management has no control over the external factors, especially in terms of fees (regulated by SEBI) or manipulating the demand.

I also agree to your point about the PE expansion. The PE expanded quite a lot, making the stock very expensive. Part of it can be blamed on the liquidity fueled rally after pandemic. But, I think it has corrected a lot since then.

But, I think the management is doing a great job by venturing into different business lines. It will add more streams of revenue, if not in the short term, at least in the long term. They have ventured into NPS platform, insurance & tied up with banks to create a platform that provides loans with mutual funds as collaterals. I think these are good initiatives. Management is also optimistic about the demand, which is why they have opened new centers and recruited more people.

Also, Great Terrain is a Private Equity fund. So, it might have exited CAMS to pursue a better investment opportunity. This doesn’t necessarily mean CAMS is bad company. It just means Great Terrain got a better company than CAMS to invest. I think there was an overreaction in the market to this news.

Disc: Invested. So, I might be biased here.

9 Likes

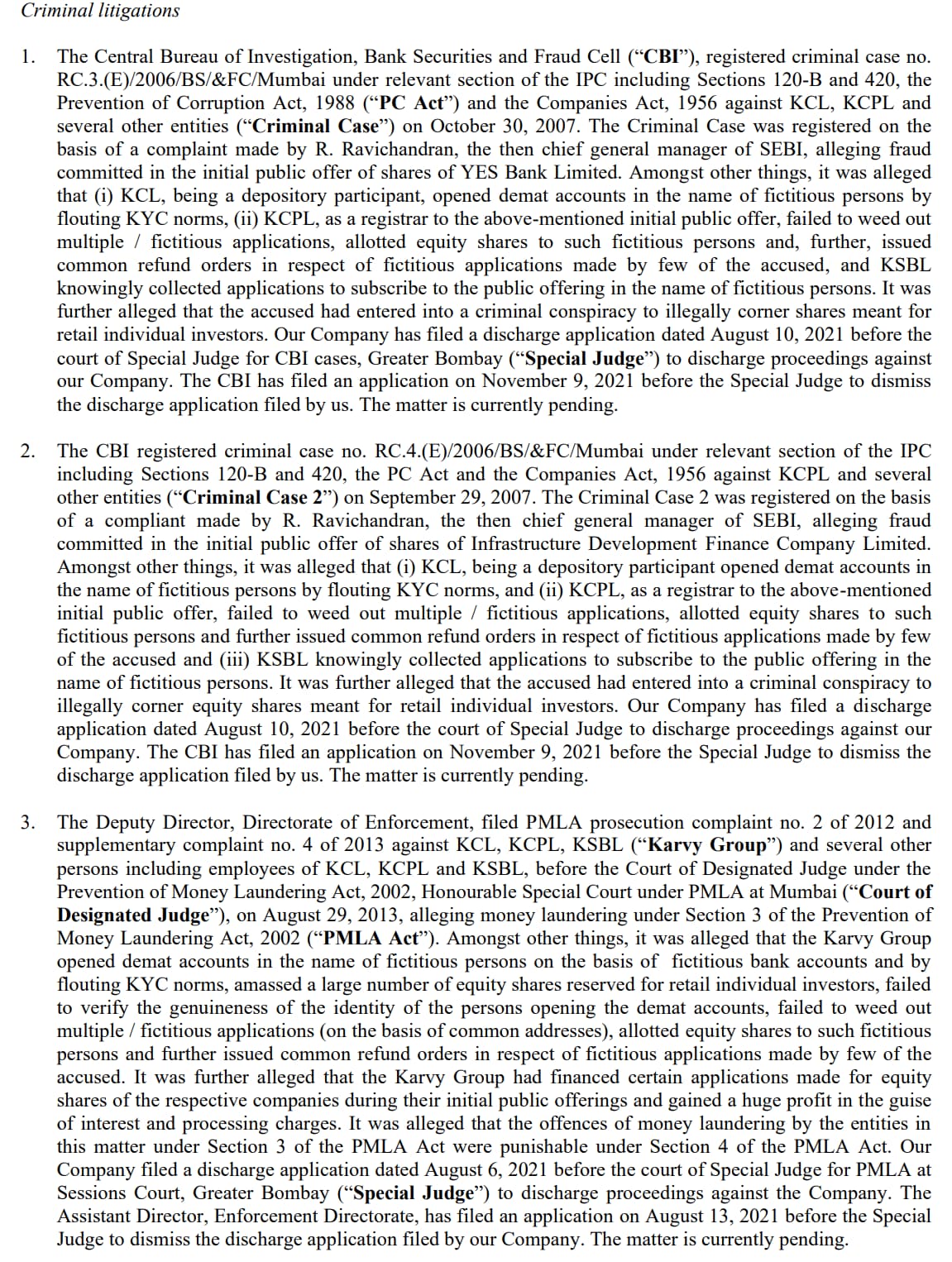

I knows its response to an old comment but for everyone’s awareness; below are the three major litigations against Kfintech (Taken from DHRP). importantly the top 2 issues are same and points to bigger governance problems.

1 Like

7 Likes

Need to see if Zerodha can gain share in the MF business like they did in retail stock broking. If that were to be the case, augurs well for CAMS.

1 Like

Zerodha is smart. They would only launch index funds with the lowest expense ratio… They would try to position them like vanguard… We have to see other drawbacks of it. If the margin of AMC is reduced it would affect CAMS profit also. They will loose the pricing power

5 Likes

Any news about their account aggregator license

not sure - the cost of servicing an index fund provider are also lower to that extent. The incremental business does not hurt and drives op leverage on the overall existing cost structure. The fact that Zerodha chose CAMS speaks a lot about the RTA’s dominance in the industry.

3 Likes

Posted good results. Management also expects to sustain 40% EBIDTA margins going forward.

4 Likes

I was reading through the Annual report. They have mentioned about multiple businesses but don’t give revenue breakup between MF and Other businesses. Like CAMSPay, CRA for Insurance etc…

Any ideas on this?

Form AOC-1 on page 264 has the summary of subsidiary financials.

5 Likes

Thanks for pointing out… I had not reached that point, perhaps asked the question too soon.

2 Likes

Talks about some good things

CAMS Finserv - NBFCs are the main driver here

CAMS in PMS AIF cat gaining traction and they say that they will scale up here in PMS and AIF field.

2 Likes